Global Solar Market Outlook (Kasikorn Research Center)

Solar energy will play a key role in driving the transition to a low carbon future due to the rapid decline in solar panel prices and widespread adoption. This article explores the growth trends of solar energy, particularly China's market dominance, the U.S. response, and the strategic impacts on the Thai market amid changing trade policies.

Solar energy will dominate the global renewable energy market due to falling solar panel prices.

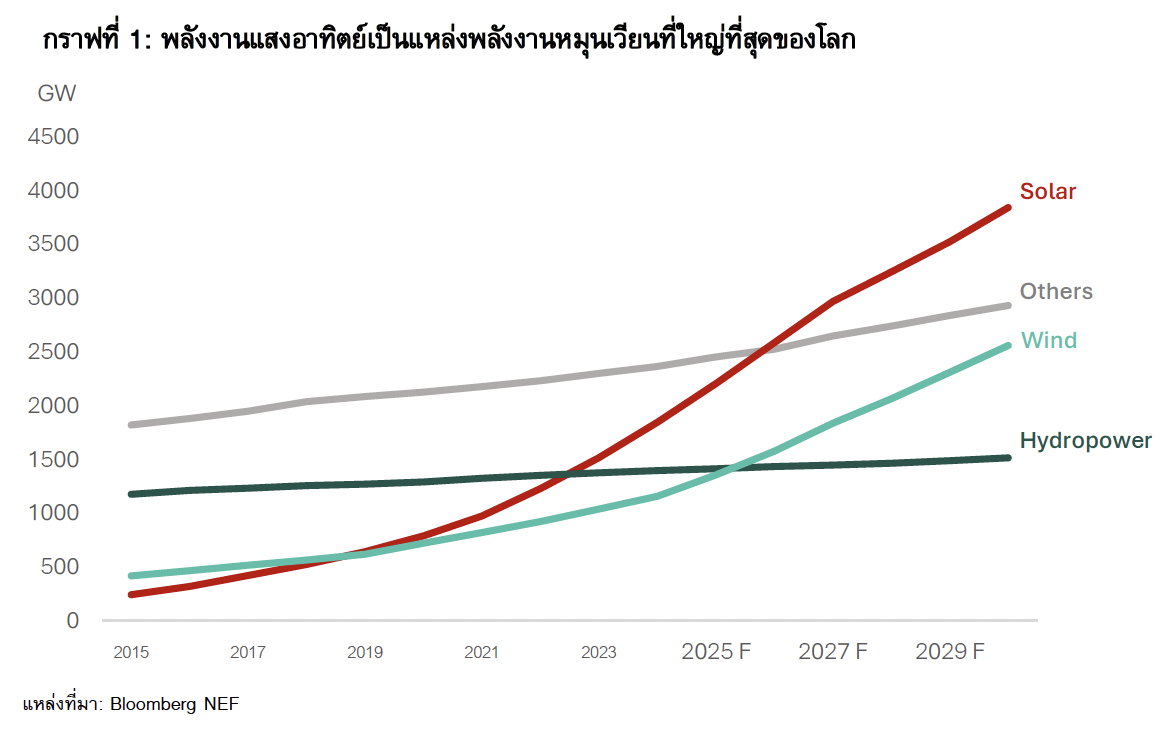

The world is shifting towards clean energy, with the COP 28 conference leading to commitments to increase global renewable energy capacity to 11,000 gigawatts by 2030. As shown in Graph 1, the share of solar energy has surpassed that of hydropower since 2023, becoming the largest renewable energy source. It is expected that the share of solar energy in total renewable energy capacity will rise from 27.9% in 2024 to 35.4% in 2030.

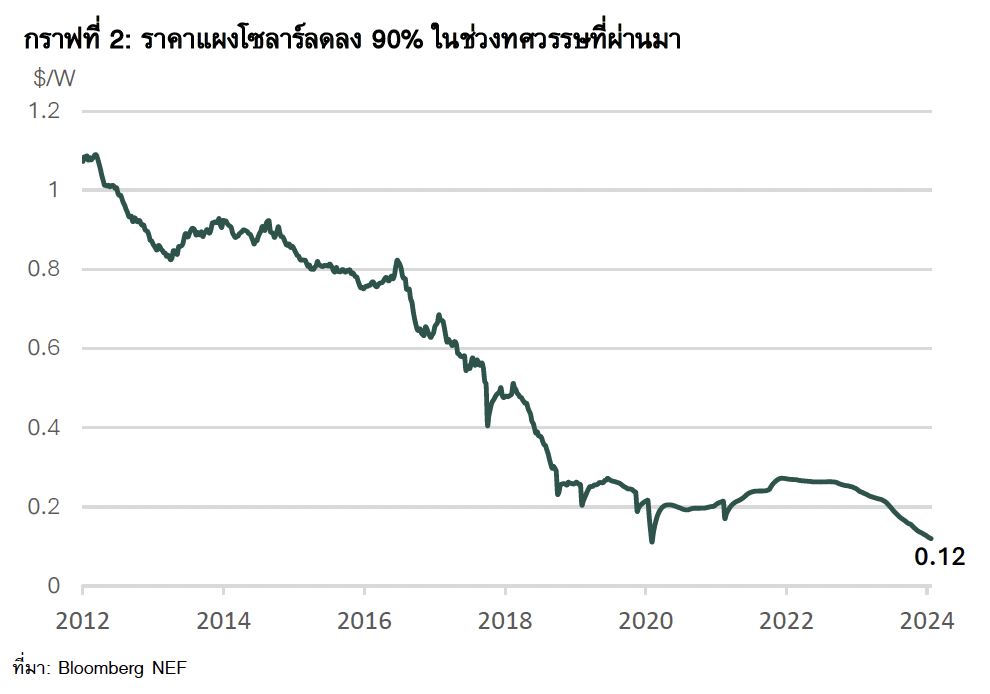

The decline in solar panel prices is a significant reason for the accelerated growth of solar energy (Graph 2). Solar panel prices have dropped nearly 90% over the past 12 years, from $1.07 per watt in 2012 to just $0.12 per watt in 2024. Notably, from 2023 to 2024, prices fell from $0.24 per watt to $0.12 per watt.

This price reduction aligns with Moore’s Law, where technological advancements lead to exponential decreases in production costs. The Kasikorn Research Center predicts that the trend of declining prices may slow down as solar panel production is expected to decelerate.

China: The Global Leader in Solar Energy Installation and Production

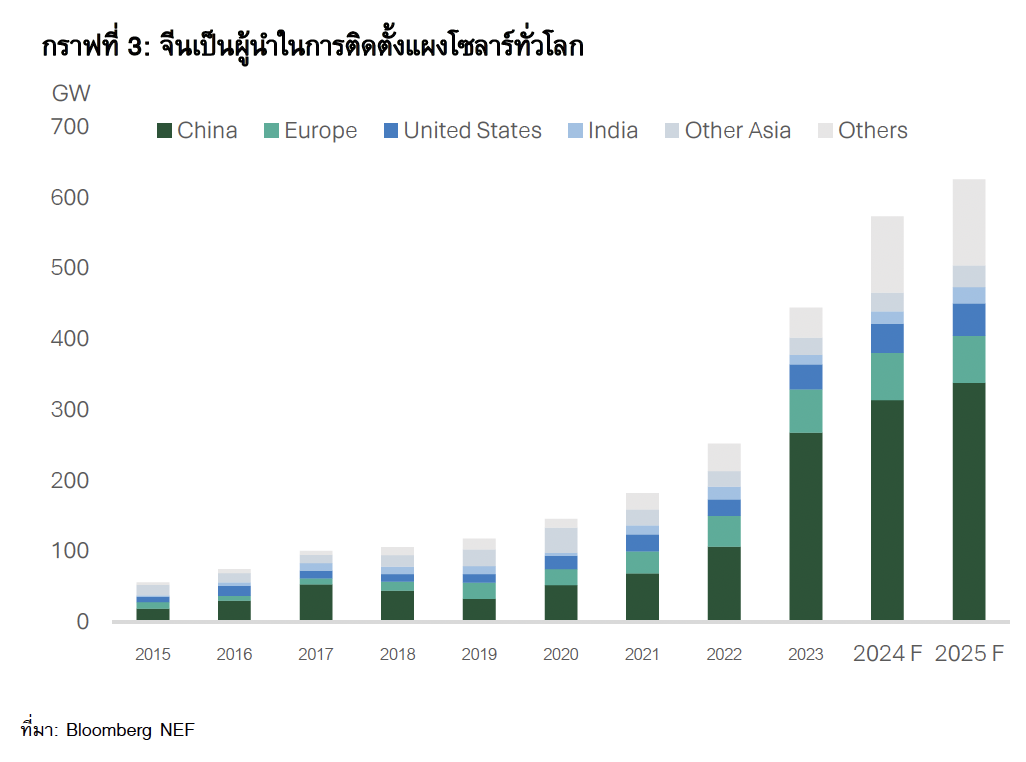

China has installed more solar panels than all other countries combined. In 2023, global solar installations reached 444 gigawatts (Graph 3), with China accounting for 60% of the total installations. China's solar installations are driven by a target to achieve at least 1,200 gigawatts of total renewable energy capacity by 2030, which is expected to be met next year.

China's leadership in solar energy stems from government goals for a transition to clean energy, motivated by severe air pollution, economic opportunities, energy security, and international climate commitments.

Over the past decade, China has been the world's largest investor in renewable energy, investing nearly 760 billion USD from 2010 to 2019, which is double the investment of the United States. In 2023, China's clean energy investment increased by 40% compared to the previous year, reaching 890 billion USD, equivalent to Switzerland's GDP.

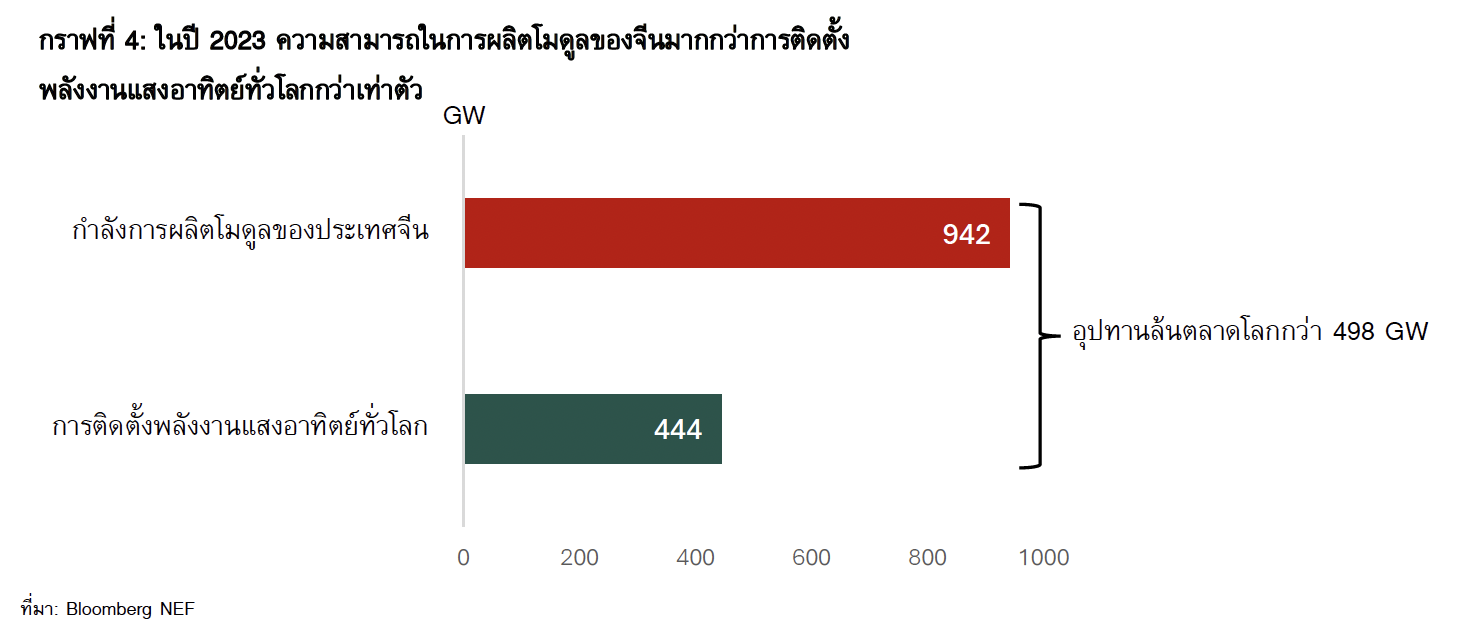

China's dominance in the solar panel market extends across the global solar panel manufacturing supply chain. With government support, production costs have decreased, leading to a global oversupply and record low prices for solar panels. In 2023, China's production exceeded global solar installations by 498 gigawatts, producing more than double the global demand (Graph 4). It is expected that China will hold over 80% of the world's solar panel production capacity in the short term, potentially even more, as Chinese solar panel manufacturers invest in various regions worldwide.

U.S. Efforts to Revive Domestic Solar Industry and Counter China's Market Dominance

China's high production capacity and low prices for solar panels have raised significant concerns among U.S. authorities, prompting the U.S. to implement measures to protect against solar panel imports from China. In 2012, the U.S. imposed Anti-dumping Duties and Countervailing Duties (AD/CVD) on solar panels produced in China as follows:

-

Anti-dumping duties (ranging from 18.32% to 249.96%)

-

Countervailing Duties (ranging from 14.78% to 15.9%)

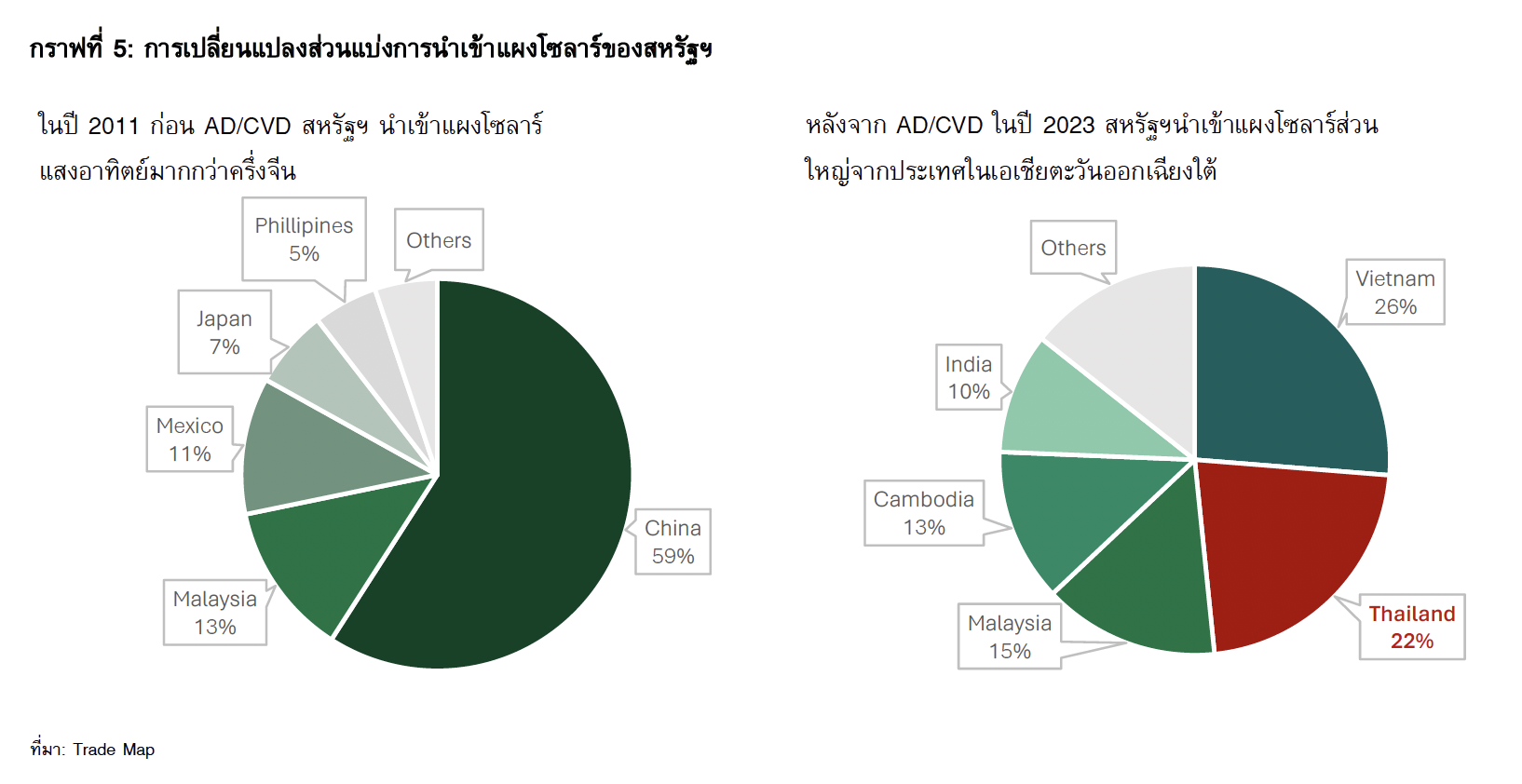

The AD/CVD measures have significantly impacted solar panel imports from China to the U.S., as shown in Graph 5. The U.S. imported 59% of its solar panels from China in 2011, but this dropped to just 0.06% in 2023. As a result, Southeast Asian countries have become the leading suppliers of solar panels to the U.S., with Thailand benefiting from this shift.

In recent years, Chinese solar panel manufacturers have invested in Southeast Asia to avoid U.S. import tariffs. In response, the U.S. has investigated solar panel manufacturers in Southeast Asia, resulting in Anti-dumping duties of up to 254% set to take effect from June this year.

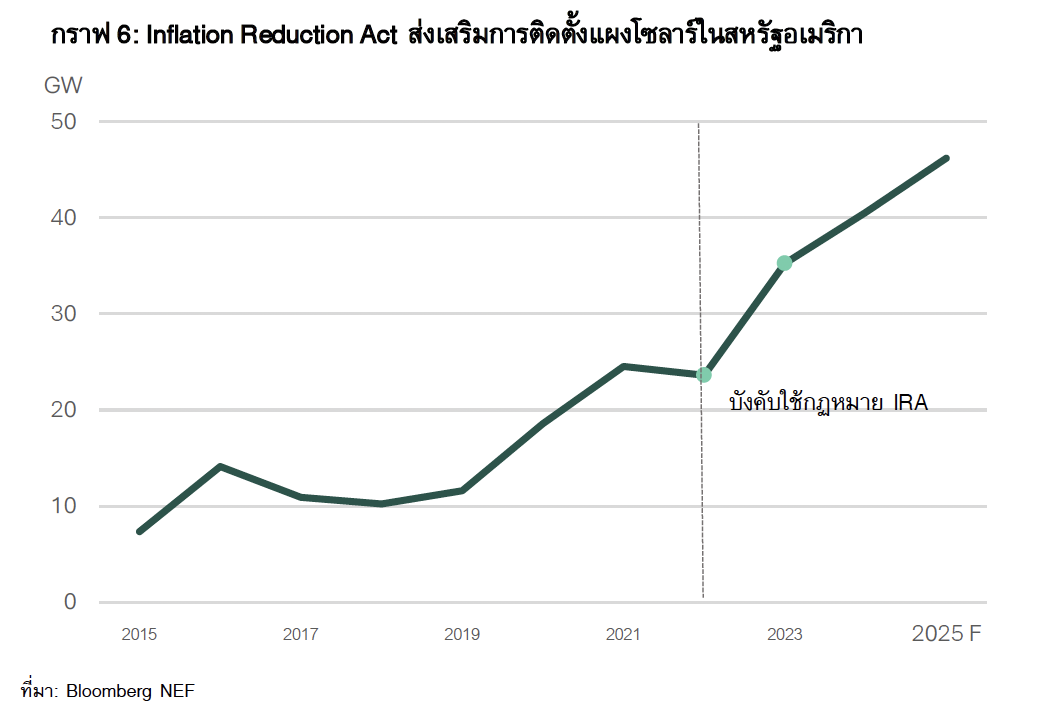

The U.S. also enacted the Inflation Reduction Act (IRA) in 2022 to support the domestic market by providing subsidies and tax benefits to domestic solar panel manufacturers and installers, leading to nearly a 50% increase in solar panel installations the following year (Graph 6).

Although the IRA policy promotes the U.S. solar industry, Bloomberg NEF predicts that solar market growth in the U.S. will be slower than in other regions due to U.S. module prices being 180% higher than the global average and more expensive than imports from Southeast Asia.

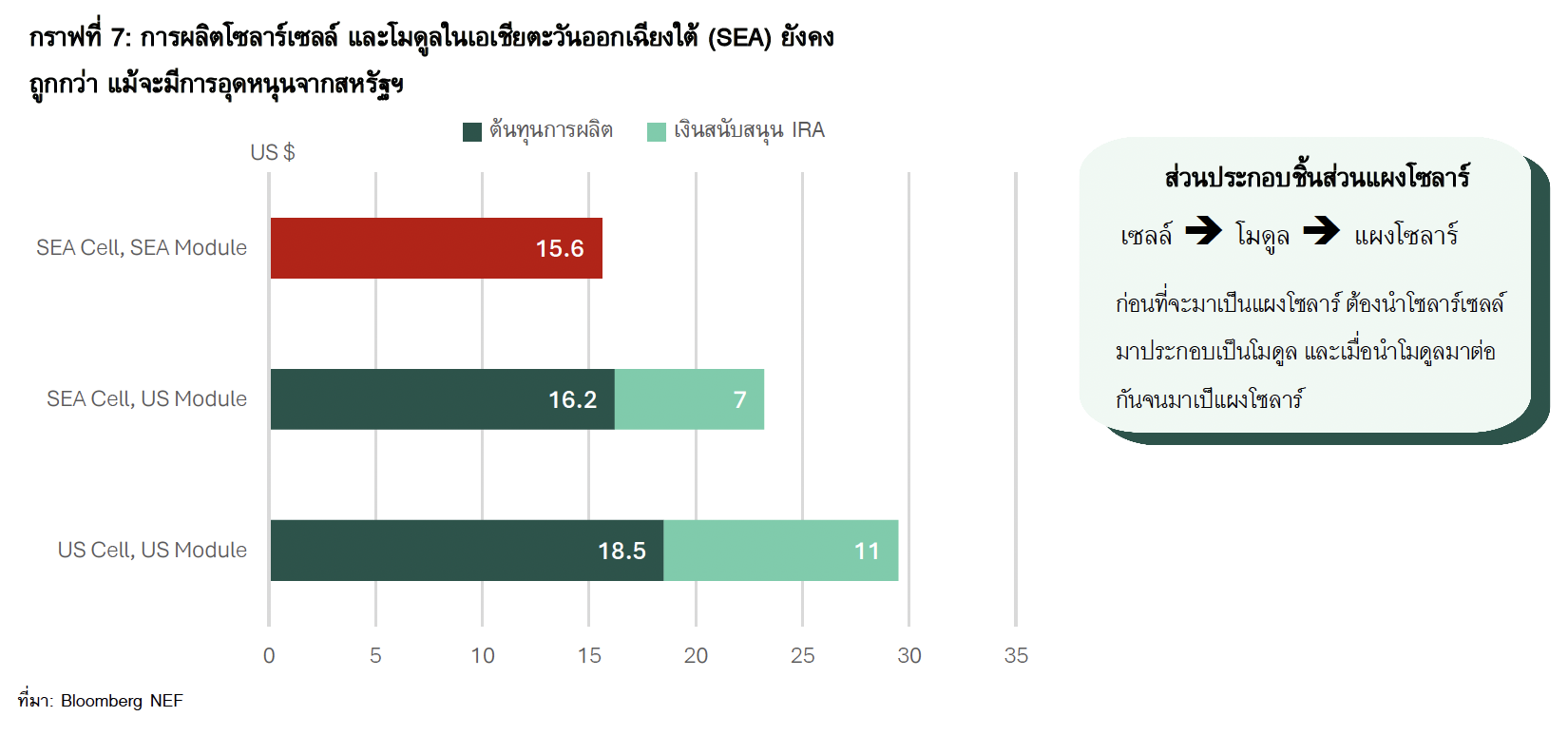

The prices of cells and modules produced in Southeast Asia are lower than those produced in the U.S. by $2.9, even with an $11 subsidy (Graph 7). Additionally, establishing solar cell manufacturing plants in the U.S. will take at least two years, so it is expected that the U.S. will continue to rely on solar panel imports in the short term.

Thai Solar Panel Exporters Significantly Affected by U.S. Protection Measures and Will Face Competition in Other Markets

Thailand needs to develop new strategies for solar panel exports, as Thai solar panel exports are heavily focused on the U.S., accounting for as much as 97.4% of the total value of Thai solar panel exports.

Although the export market for Thai solar panels to the U.S. remains due to the lower prices of Thai solar panels, Thailand's price competitiveness will only be viable if not subjected to Anti-dumping duties. To avoid these tariffs, Thai solar panel manufacturers must comply with strict regulations.

For example, the company Canadian Solar recently established a 5-gigawatt wafer manufacturing plant in Thailand, which may help address these issues.

However, Thailand still needs to explore additional solar panel export markets in other regions, as the U.S. supports domestic manufacturers. Coupled with geopolitical tensions with China, such as the recent increase in U.S. tariffs on solar panels from China from 25% to 50%, this has had minimal impact on China, as China only exports 0.06% to the U.S.

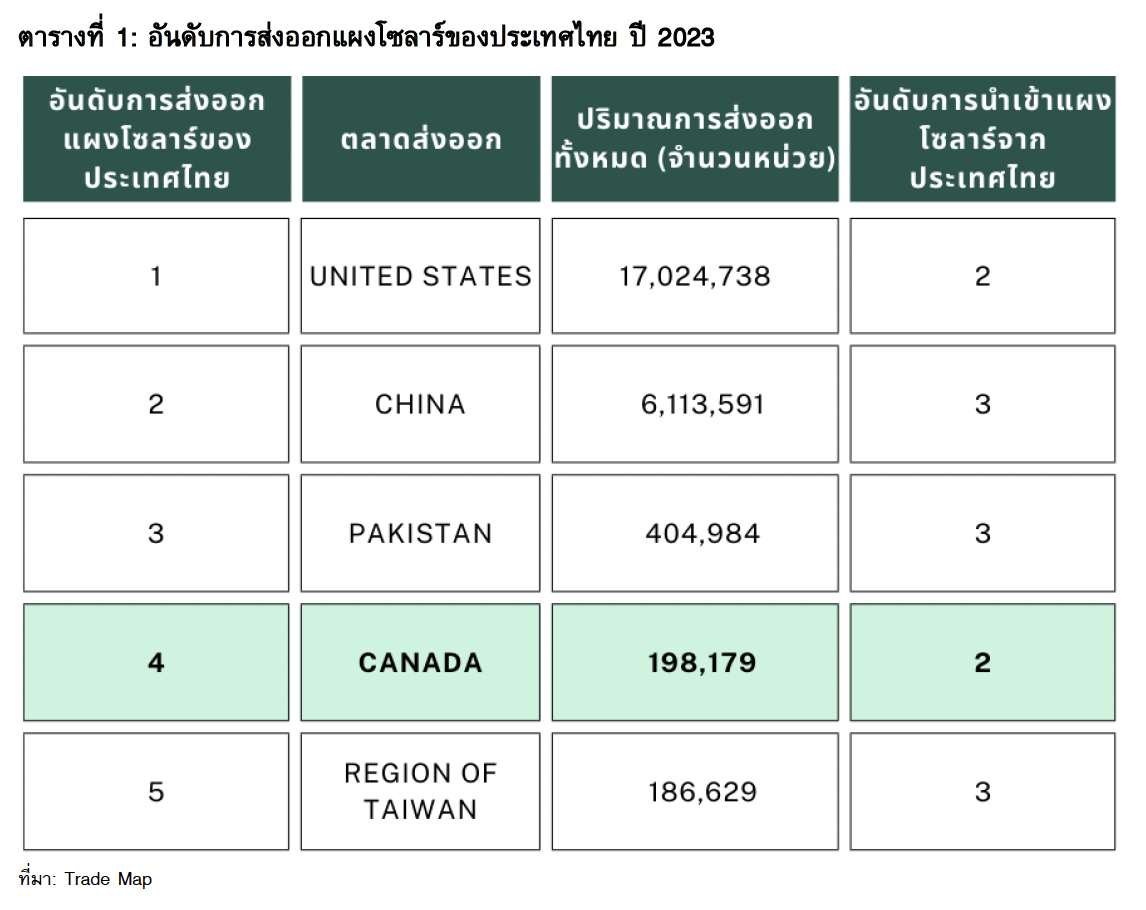

Expanding relationships with countries that are already importers could enhance trade opportunities. For instance, (Table 1) Canada is Thailand's fourth-largest export market, and Thailand is the second-largest supplier of solar panels to Canada. Canada also needs to increase its renewable energy capacity to achieve its Net Zero target, indicating a growing demand for solar panels and representing an opportunity for expanding solar panel export markets. However, Thailand must compete with Vietnam, which is the largest solar panel importer for Canada.

Diversifying some of the solar panel exports to support the domestic market is another strategy. Although the solar energy market in Thailand is not yet sufficient to accommodate all exports, focusing on the domestic market may enhance the growth of Thailand's solar energy market to be adequate in the future.