Knight Frank Analyzes the Overview and Trends of the Thai Real Estate Market Q4 2022 - Q1 2023

Knight Frank Thailand held the event “Knight Frank Foresight 2023 It’s Time to Look Beyond the Crisis” to delve into the overview and trends of the Thai real estate market during the fourth quarter of 2022 and into the first quarter of 2023, showing continuous recovery. Positive signals from high-end purchasing power are driving the luxury home market in Bangkok and its suburbs, with sales reaching 19,476 units. Attention is drawn to the villa and condominium markets in Phuket, which are thriving due to interest from Russian and Chinese clients, while the hotel market has begun to recover from its lowest point, ready to embrace the MICE market.

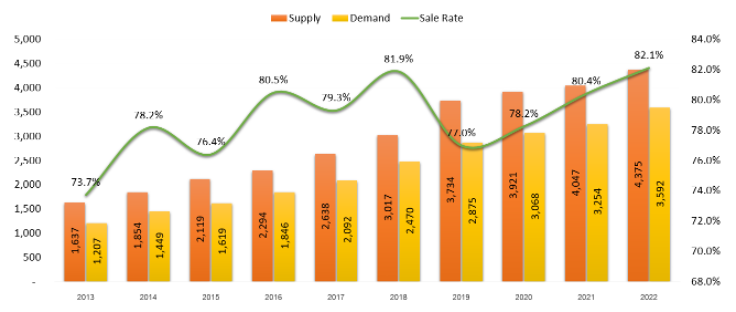

Residential Market

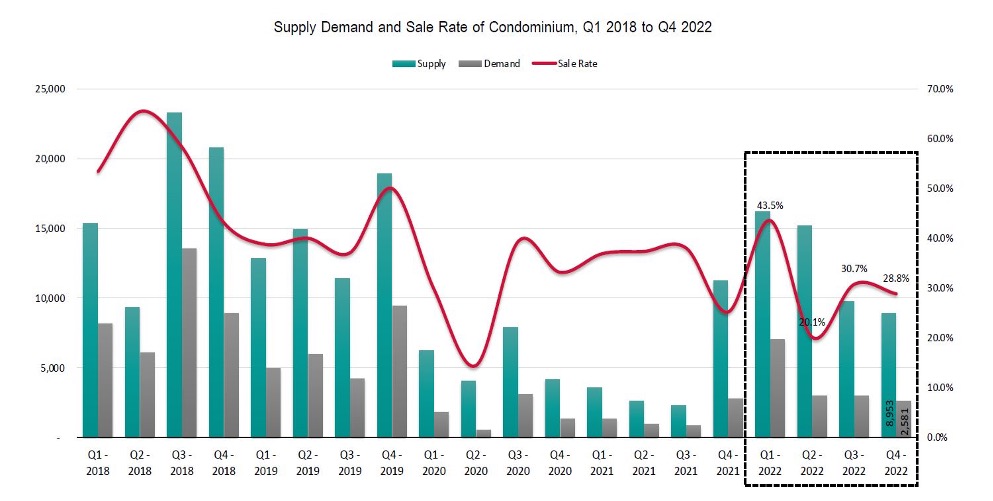

In terms of condominium project development, Q4 2022 has returned to normalcy, with developments primarily occurring in the outskirts, mostly in B and C grade projects priced below 150,000 THB per square meter. Real estate developers remain confident in the affordable market at accessible price points. Overall, in Q4 2022, prices remained stable compared to the previous year as international markets have not yet reopened. Most developments are led by major real estate developers focusing on condominiums in the outskirts, while medium and small developers have not yet returned to the condominium sector.

In the last quarter of 2022, the demand for condominiums had a total supply of 8,953 units, mostly located in suburban Bangkok. The volume of new real estate launches decreased by 9.7 percent compared to Q3 and dropped by 20.4 percent compared to the same period last year. The demand for new real estate projects also decreased to 28.8 percent from 30.7 percent in Q3 2022. The main customer group, especially for ready-to-move-in projects, consists of investors purchasing for rental purposes. The selling prices of condominiums in Q4 2022 slightly decreased across all areas, averaging a drop of 0.29 percent due to the government ending the LTV measures.

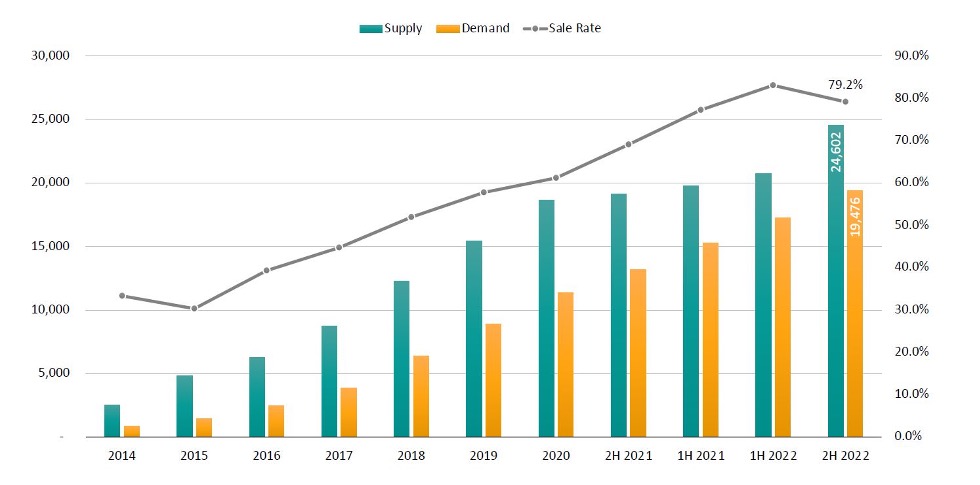

The luxury home market saw growth of 16% in 2021 and 17% in the first half of 2022, primarily in the price range of 10 - 20 million THB, totaling 3,800 units, including homes priced above 20 million THB. It was also noted that homes priced at 41 million THB and above have shown continuous annual growth, although the majority of supply remains in the 10-20 million THB range.

Phuket Condominium Market

As tourism begins to recover, it is expected that the condominium market will return to pre-COVID conditions within 1-2 years, as it awaits the return of tourist numbers to pre-COVID levels. From late 2022 to the present, the villa market has seen high supply for both purchase and rental, with foreigners showing interest in buying homes in Phuket as second homes, preferring to rent villas over condominiums due to family space. Rental prices can yield profits of 8-10 percent per year.

The return of Russian nationals after the country reopened has positively impacted the market significantly. The Phuket villa market has seen higher demand and popularity compared to condominiums, particularly among Europeans and Russians looking for villas priced between 10-20 million THB and above. The popular areas in Phuket include the western side, from Kata Beach, Karon, Laguna, to Cherng Talay, which are favored by Russians who often form communities, buying for personal use and to escape the cold.

Chinese buyers are also starting to enter the market, although their presence is not yet fully established due to restrictions from China. Currently, Chinese buyers prefer to purchase properties to rent out to fellow Chinese tourists visiting Thailand, including condominiums, villas, yachts, and even durian farms, which are particularly popular among Chinese nationals.

Office Market

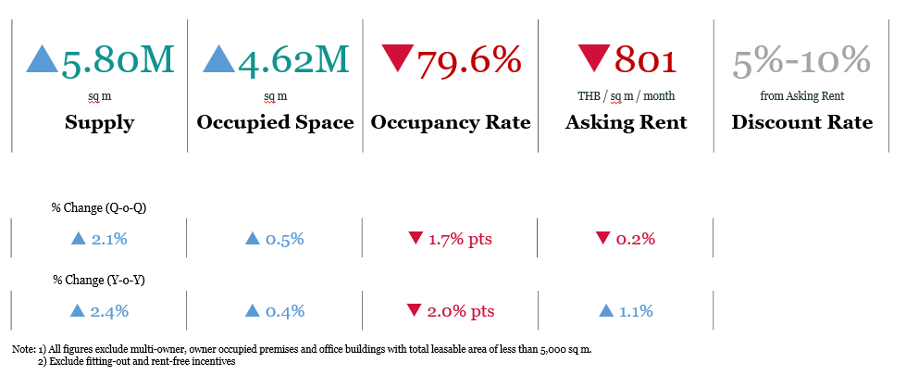

The Thai economy grew slightly in the fourth quarter of 2022, similar to the demand for office buildings in Bangkok. However, the most notable change is the rise of ESG (Environmental, Social, and Governance) principles and sustainability, leading to a high demand for sustainable buildings in 2022, as evidenced by the net absorption rates of green buildings being higher than those of conventional buildings in every quarter.

By the end of 2022, the total area of office buildings expanded by 117,000 square meters, or 2.1 percent quarter-on-quarter, reaching 5.79 million square meters, accounting for two-thirds of the new supply in 2022. Most of the recently constructed projects have received green building certification, resulting in a 11.3 percent quarter-on-quarter increase in leased green office space, totaling 1,180,000 square meters, which represents 20 percent of all leased office space. The total leased area increased by 20,900 square meters, reaching 4.62 million square meters in Q4 2022, with positive absorption rates across all grades. Grade B office space saw the highest absorption increase of 17,200 square meters quarter-on-quarter compared to other grades due to the leasing rates of newly completed buildings. However, the overall rental rate in the market was down by 1.7 percent quarter-on-quarter to 80 percent, with no segment experiencing an increase in leasing. The average rental rate slightly decreased to 801 THB per square meter, with Grade A being the only segment to see a rental increase of 0.6 percent quarter-on-quarter due to high leasing rates.

Hotel Market

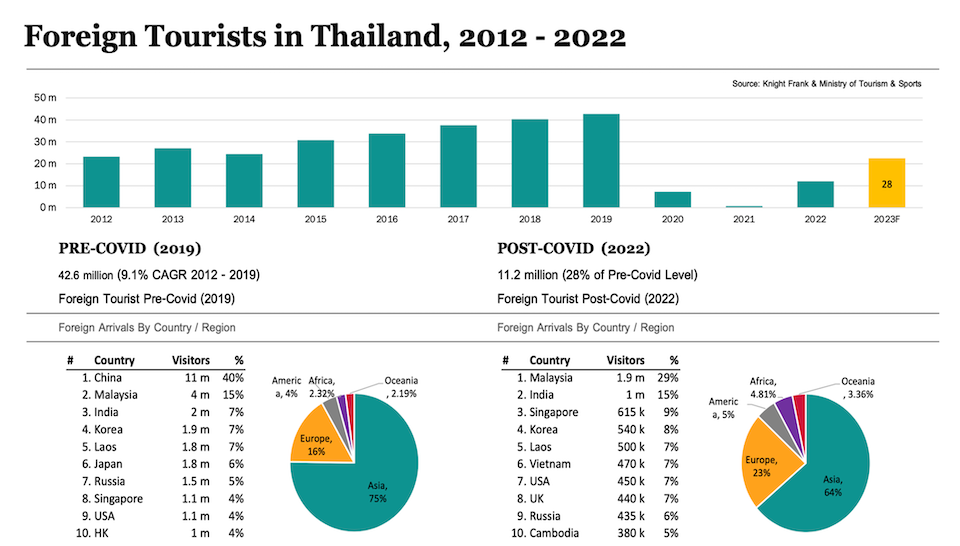

Recent figures indicate that the number of travelers entering the country in January and February 2023 was 60 percent of pre-COVID levels, with the average hotel occupancy rate at 72 percent, up from 36 percent in 2022.

In 2023, it is expected that around 28 million foreign tourists will visit, or 70 percent of pre-COVID levels, with 7-8 million of these tourists coming from China, as the Chinese government lifted COVID measures in early January 2023. The number of Chinese tourists is expected to gradually increase, reaching a peak by the end of this year. The latest figures for January 2023 show 92,000 arrivals, still below the pre-COVID figure of 1.9 million.

Industrial Market

The logistics real estate market in the second half of 2022 remained bright due to the expansion of e-commerce and the full reopening of the country. 3PL logistics companies continued to be significant clients this year, followed by tenants from specialized businesses such as FMCG and industrial manufacturers. Most warehouse providers are shifting towards built-to-suit services instead of speculative builds to avoid long periods of vacancy. It can be said that the future of ready-to-use logistics real estate will continue to align with average annual growth.

The trend of ESG (Environmental, Social, and Governance) awareness and sustainability is expanding in the Thai industrial sector. Some warehouses are integrating sustainability elements, such as water flow reduction techniques, double-skin building coatings, natural ventilation, and rooftop solar panel installations, to reduce carbon footprints and operational costs.

Although the logistics real estate industry in Thailand has begun implementing sustainability measures, it remains limited and lower than other sectors of the real estate business, such as hotels and office buildings, which have a higher proportion of buildings meeting sustainability criteria or receiving green building labels. This may be due to a lack of demand from investors and tenants in logistics and a lack of evidence to justify higher rental rates for green warehouses. It will be interesting to see how the industry adapts to achieve net-zero emissions goals and whether the benefits of these efforts will become clearer in the future.

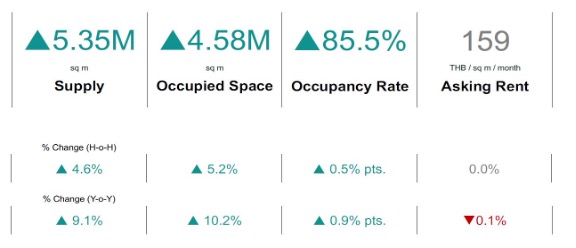

The total supply of ready-to-use warehouses is 5.35 million square meters, an increase of 237,749 square meters over the first six months of the year, representing a growth of 4.6 percent half-year-on-half-year and 9.1 percent year-on-year. The total leased area in Bangkok, currently the largest sub-market, increased by 4.3 percent half-year-on-half-year to 2.4 million square meters, accounting for 48.3 percent of the total ready-to-use warehouse space in Thailand. The total leased area increased by 5.2 percent half-year-on-half-year or 10.2 percent year-on-year to 4.58 million square meters, resulting in a leasing rate of 85.5 percent, the highest in 10 years. The asking rental rate for ready-to-use warehouses in Thailand remains unchanged at 158.6 THB per square meter per month in the second half of 2022.