Can Retirement Happiness Be Designed?

Design is hidden in almost every aspect of our daily lives for convenience and to solve various problems we encounter. For instance, we design our homes and the items we use. Even we have to design our decisions almost every morning, such as what to wear today—whether to choose a shirt with pants or a skirt that suits the day's activities. There are also accessories like shoes, watches, and jewelry. This is just a small matter, yet we face decisions every day. So, what about planning for retirement? Can we afford to wait? Today, let's invite each other to design a plan for a happy retirement for a comfortable life in the future.

The term 'retirement' according to the Royal Institute Dictionary (1999) means "to cease" and is often used in relation to age, such as retirement from government service, which is typically set at 60 years. In the private sector, it may be set at 55 or 60 years. Therefore, life after retirement is something that needs to be designed and planned for when we no longer have income from work, while also facing health issues that decline with age.

'Happiness' according to the Royal Institute Dictionary (1999) means "physical and mental comfort", which is a type of feeling or emotion that varies in levels from slight comfort or satisfaction to a state of enjoyment filled with fun. Each person's happiness differs based on their mindset and perspective on life.

The Royal Institute Dictionary does not provide a definition for the term 'design', but according to Wikipedia, design means "to create something new or to improve and adapt existing things for betterment."

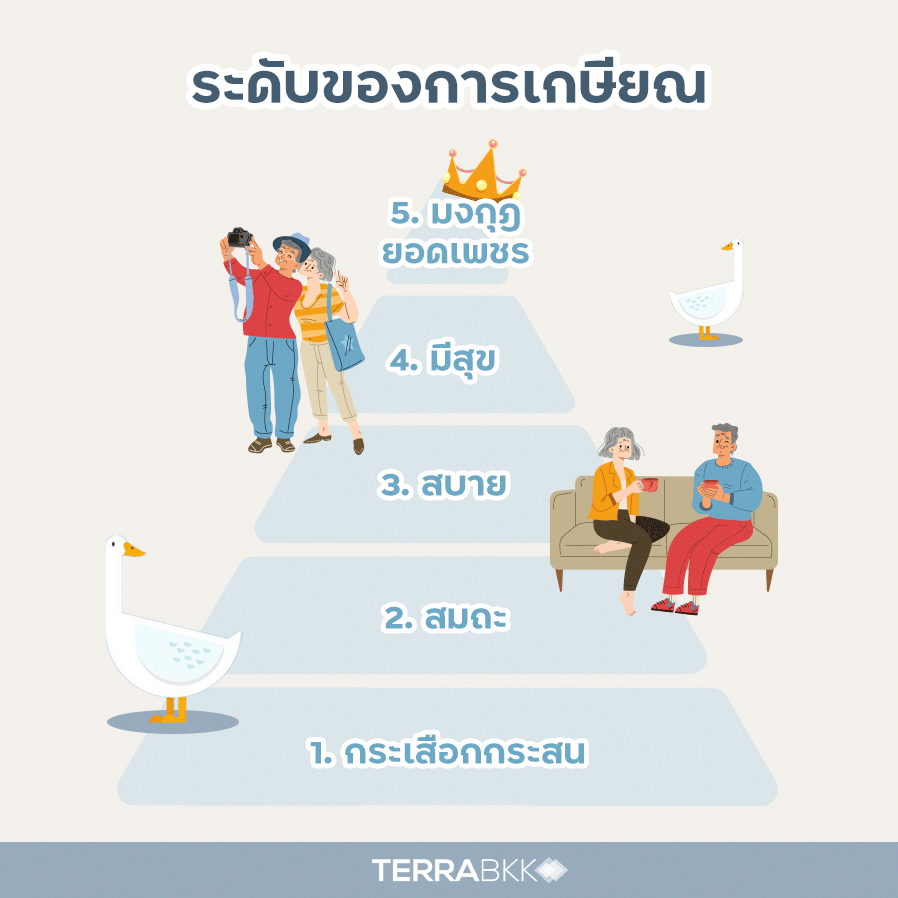

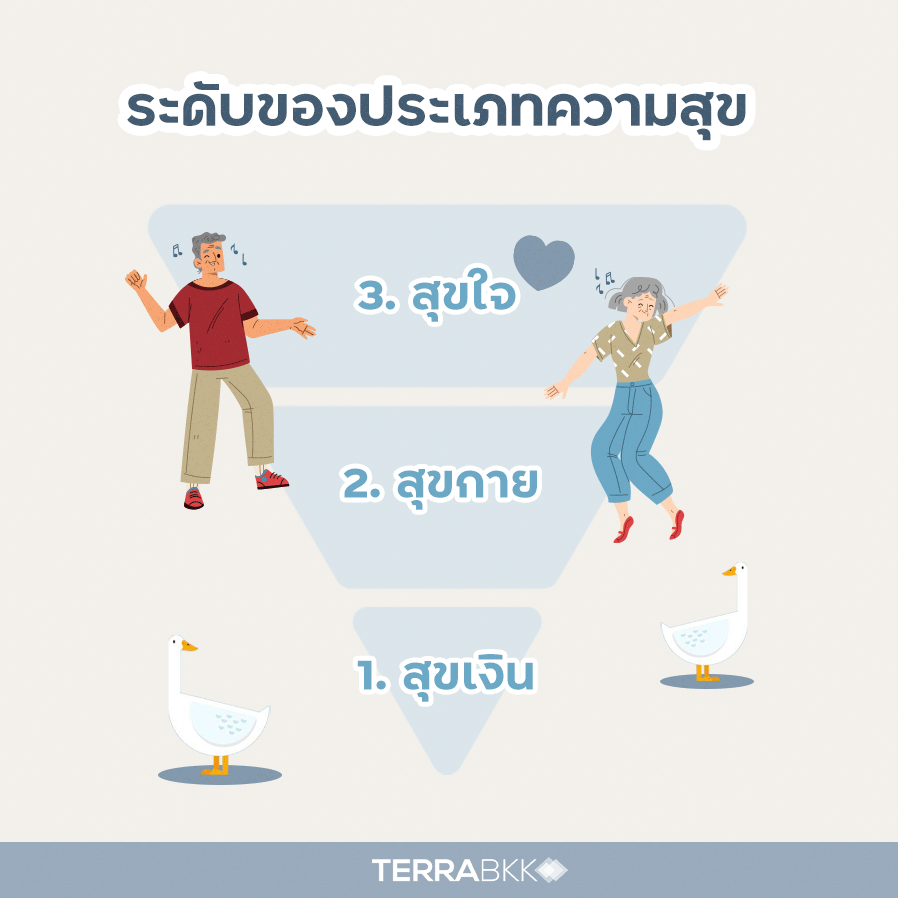

Thus, designing for retirement happiness means "planning to create a post-work life that brings physical and mental happiness according to each individual's circumstances". The key variable is happiness. Each person's retirement goals can be divided into five levels as shown in Figure 1, while the levels of happiness can be divided into three levels as illustrated in Figure 2.

Figure 1

Figure 2

- Struggling Level is a retirement life that is difficult both physically and mentally. This may arise from economic issues, health problems, social issues, or a combination of all aspects. Therefore, options are limited, and one may have to continue working without being able to stop, relying on relatives or the state welfare system.

This level may involve economic difficulties or health issues, leading to a challenging life.

- Moderate Level is a retirement life that is simple and modest. Living a life of sufficiency, not too difficult but also not very comfortable. One cannot live as expected and may have to cut social expenses, such as meeting friends or participating in social activities. This level is often designed by the government to ensure that civil servants can live a modest life after retirement with reasonable state welfare support.

- Comfortable Level is a retirement life that is comfortable both physically and mentally, with enough money for various needs, including healthcare costs. One may mitigate risks by purchasing life insurance or enrolling in a gold card (universal health insurance). There is sufficient money for social expenses.

- Happy Level is a retirement life that aligns with previously set goals, allowing one to live according to their chosen path with physical and mental comfort, having enough money for various needs, including healthcare costs, and possibly mitigating risks through life insurance or a gold card.

- Crown Jewel Level involves good health, reputation, and abundant wealth. One can take care of themselves and others, surrounded by family like a king at home, invited to play various social roles such as being a president or advisor in various associations. This is the dream retirement life for many. The triangle with a wide base and a narrow top represents the retired population, where the levels of happiness are fewer than those who are moderately happy and struggling, which are much more numerous. Where we want to be in this triangle depends on our goals and actions.

The levels of happiness can be divided into three levels as follows:

- Financial Happiness means having enough money to spend comfortably and possessing assets that can generate income in the form of passive income, allowing money to work for us during retirement. While money cannot bring happiness in every aspect, a lack of it can lead to suffering in many ways. Therefore, financial happiness is the basic level of happiness for a happy retirement.

- Physical Happiness refers to good health, enabling one to engage in various activities independently without serious chronic illnesses causing physical and mental distress. Even with abundant wealth, poor health is not the goal of many people's retirement happiness. Thus, physical happiness is a middle level of happiness for many.

- Mental Happiness is the comfort of body and mind, with pride in oneself when looking back, having lived a life beneficial to oneself and others. Mental happiness is the highest level of happiness in retirement life.

Steps to Design a Plan for a Happy Retirement are divided into six steps as follows:

- Self-Assessment Step involves taking care of financial health, physical health, reviewing assets and debts, and current spending habits to gather information for future spending plans. Assessing physical health is also essential for planning future health care.

- Goal Setting Step involves defining goals and feasible methods based on the self-assessment, as each person's goals differ.

- Saving and Accumulating Step is a time-consuming and disciplined process to build wealth for oneself and family while also learning about investments to make the accumulated wealth work for us in old age. As the saying goes, "Use labor to make money, use money to work."

- Investment Allocation Step involves placing various assets in appropriate locations, such as emergency funds that can be accessed immediately when needed, investments that generate income, combat inflation, and minimize loss of principal due to expenses.

- Spending According to Goals Step allows one to use money according to their goals, such as daily expenses, social spending, and fulfilling personal desires like travel or charitable donations.

- Monitoring and Evaluation Step involves reviewing the plan after implementation to ensure caution. We should revisit the plan to account for changes due to various factors, such as inflation and changing health conditions.

As mentioned, knowledge about retirement is not hard to find. The most challenging aspect is changing perspectives and creating a suitable mindset that designing for retirement happiness is something everyone can do. Taking disciplined action is the most important factor. Increasing income and reducing expenses are the basic equations for success. I hope everyone can plan and achieve their retirement happiness goals.

Figure 3