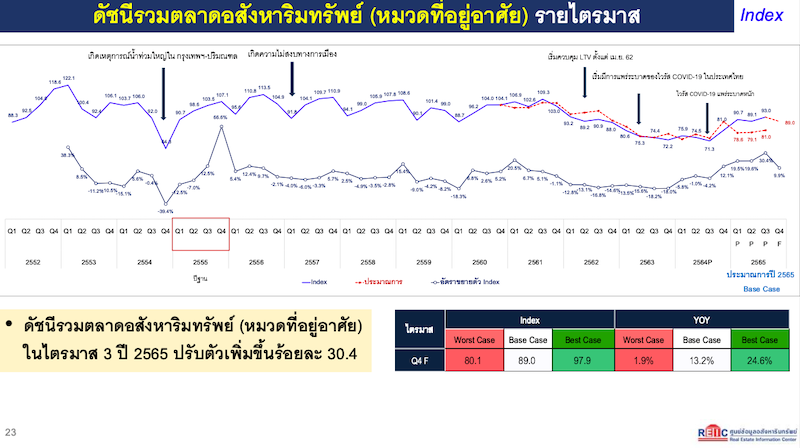

Real Estate Market Index in Q3/2022 Increases by 30.4%

The overall real estate market index (residential category) indicates continuous recovery, with a 30.4% increase in Q3/2022 compared to the previous year. Completed homes registered are expected to continue growing into Q4 in anticipation of transfers at the end of 2022. It is projected that in 2023, LTV measures may lead to a nationwide decrease in transfer units by -14.2% and a reduction in transfer value by -4.4%.

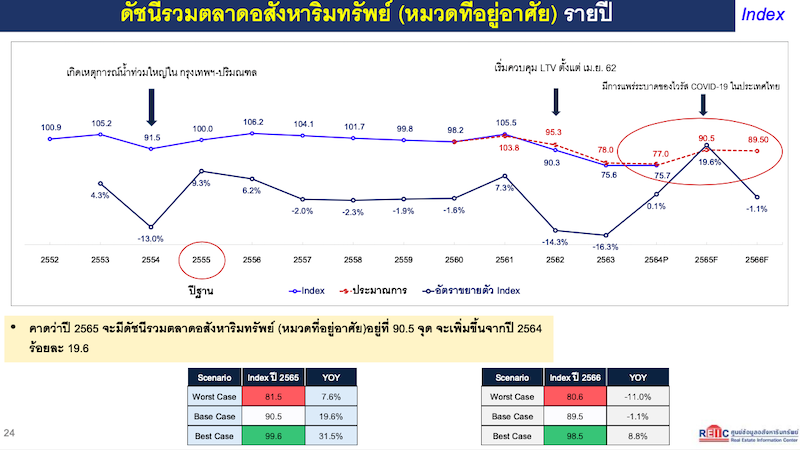

Dr. Vichai Wiratthakhan, Inspector of the Government Housing Bank and Acting Director of the Real Estate Information Center revealed the report titled "Overall Real Estate Market Index (Residential Category)" for Q3 2022, which has an index value of 93.0 points, reflecting a 30.4% increase from the same period last year. This increase is attributed to improved transfers of residential ownership, absorption rates of housing projects, and condominium units. The data on completed residential registrations, the number of residential construction permits issued, and the confidence index of operators in this quarter also contributed to this growth. It is anticipated that the overall index for 2022 will not fall below 90.5 points, representing a growth of 19.6% from the previous year, and could rise to a maximum of 99.6 points (Best Case), reflecting a growth of 31.5%. However, in a worst-case scenario, it is unlikely to drop below 81.5 points, indicating a growth of 7.6%, with ongoing monitoring of key supply and demand indicators for housing.

• Supply and Demand for Housing in Q3 2022

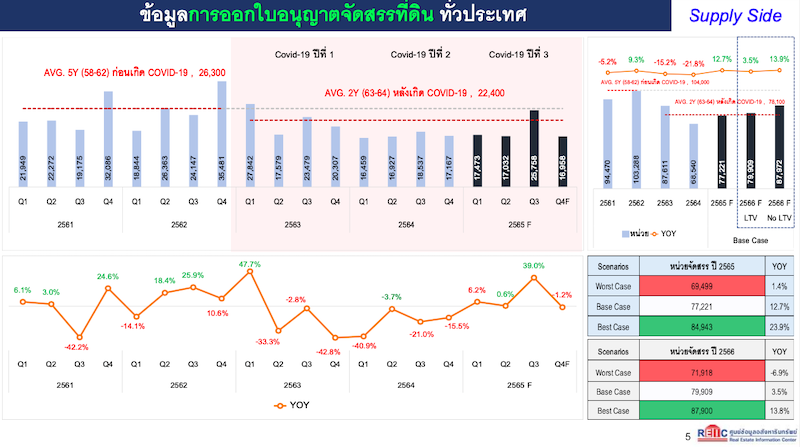

Regarding supply, the REIC reported that the issuance of land allocation permits nationwide in Q3/2022 totaled 25,758 units, the highest in the past 10 quarters, representing a 39.0% increase compared to the same period last year, marking the third consecutive quarter of year-on-year growth.

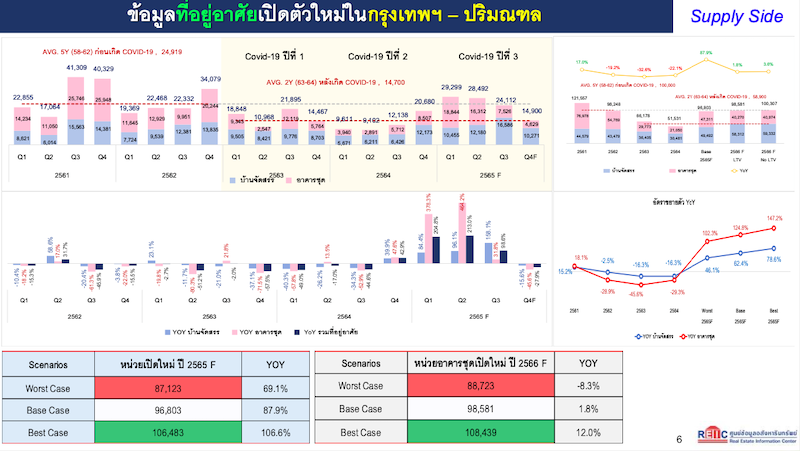

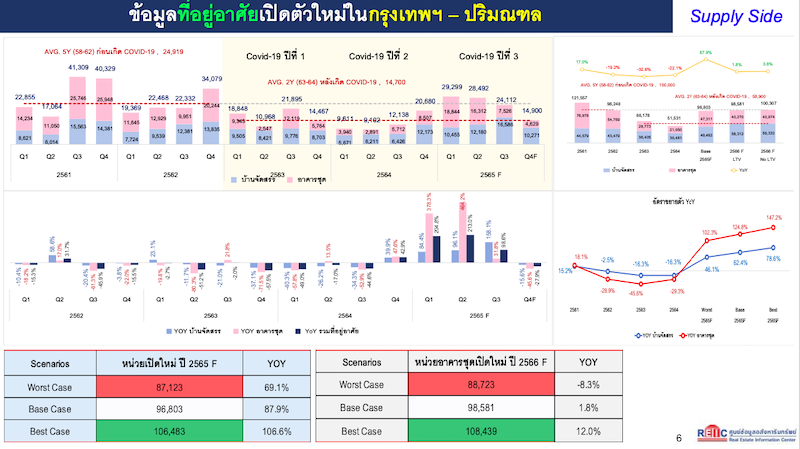

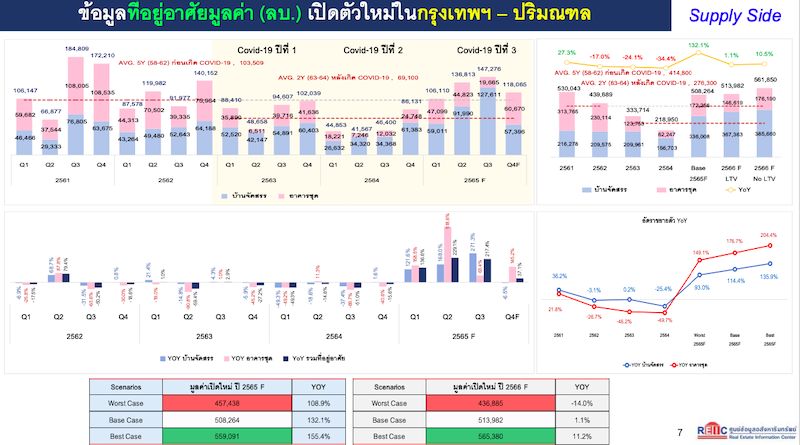

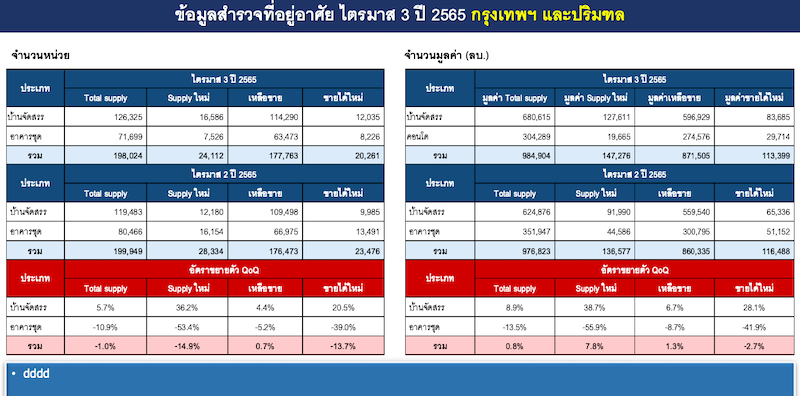

The supply from new residential projects launched in the Bangkok and surrounding areas in Q3/2022 totaled 24,112 units, reflecting a 98.6% growth with a value of 147,276 million baht, which is a 217.4% increase from the same period last year. It was found that housing projects expanded more significantly than condominiums in both unit numbers and value, contrasting with Q1 and Q2, where condominiums had greater growth, indicating a decline in new condominium project launches.

Meanwhile, the number of building permits for residential buildings nationwide in Q3/2022 totaled 75,336 units, divided into 63,801 units for horizontal housing and 11,535 units for condominiums, representing a decrease of -14.3% compared to the same period last year.

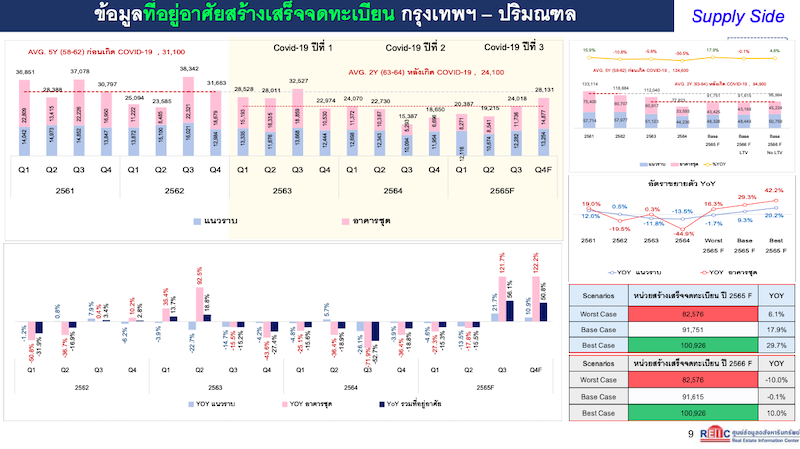

However, it was found that the number of completed residential registrations in Bangkok and surrounding areas was 24,018 units, an increase of 56.1% compared to the same period in 2021, divided into 12,282 units for horizontal housing and 11,736 units for residential condominiums. It is expected that the significant increase in completed residential registrations this quarter resulted from the accumulation of units that were delayed in construction previously and the acceleration of registrations leading to ownership transfers in Q3 and Q4 of 2022.

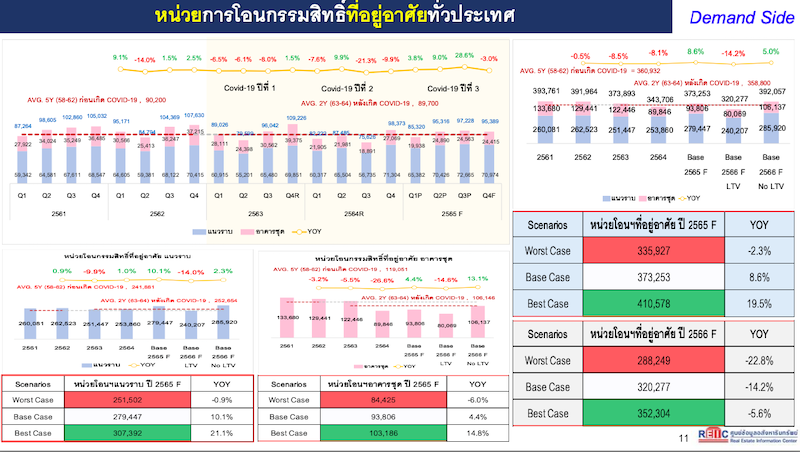

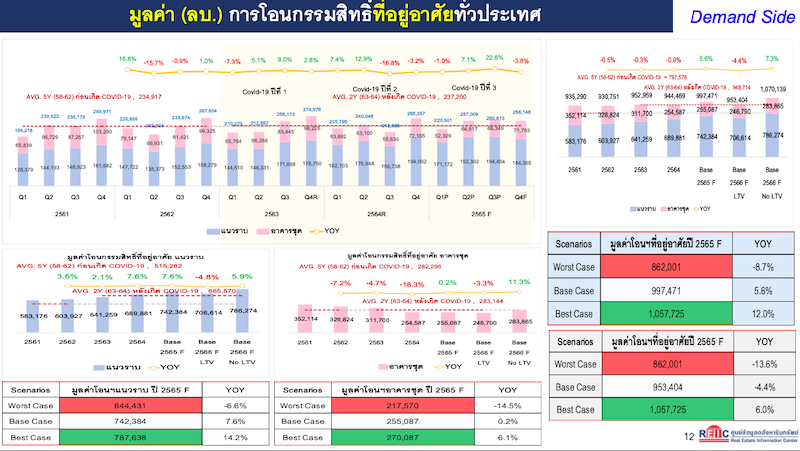

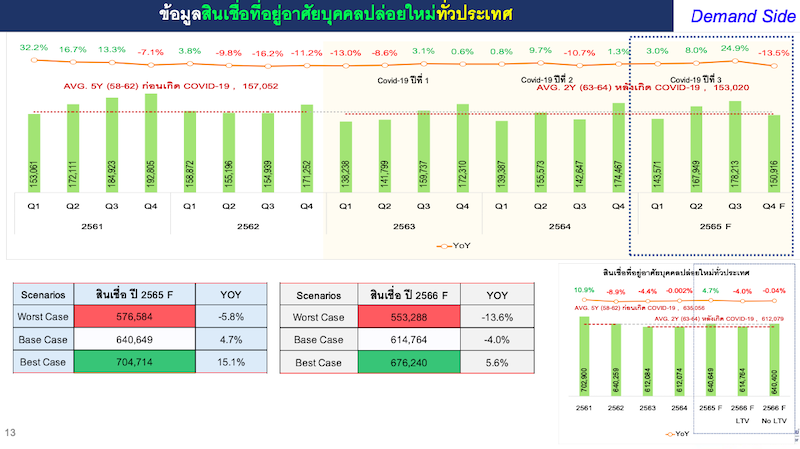

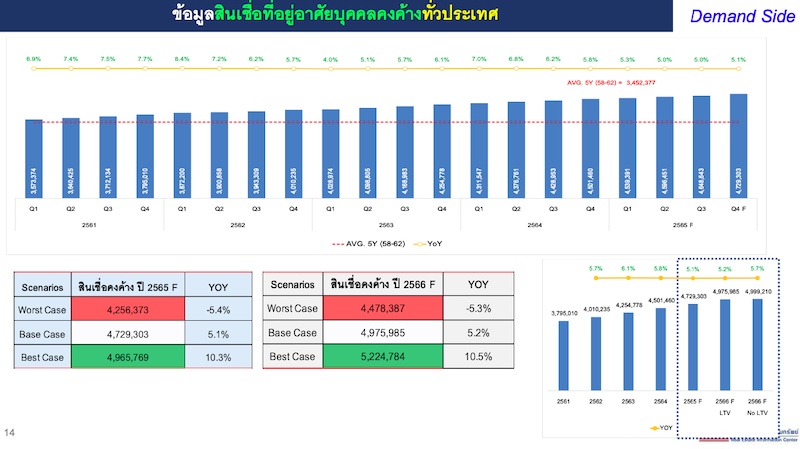

The number of residential ownership transfers nationwide in Q3 2022 totaled 97,228 units, an increase of 28.56%, marking three consecutive quarters of growth. This can be divided into 72,665 units for horizontal housing and 24,563 units for residential condominiums, with the total transfer value also rising to 260,813 million baht, an increase of 22.8%, divided into 194,454 million baht for horizontal housing and 66,349 million baht for condominiums. It was found that the amount of new personal housing loans issued nationwide in Q3 2022 was 178,213 million baht, an increase of 24.93%, aligning with the trend of residential ownership transfers and exceeding the 5-year average of 157,052 million baht, resulting in the total outstanding personal housing loans nationwide rising to 4,648,643 million baht, an increase of 5% from the same period last year.

Field survey data in Bangkok and surrounding areas found that the total number of projects offered for sale in Q3 2022 was 198,024 units, a decrease of -1.0%, while the total project value was 984,904 million baht, an increase of 0.8% compared to the previous quarter. New sales totaled 20,261 units, a decrease of -13.7%, while the value of new sales was 113,399 million baht, a decrease of -2.7%. This slowdown was primarily due to a significant decline in new sales of condominiums, which dropped by -39.0% in unit numbers and -41.9% in value from the previous quarter, while housing projects expanded by over 20% in both units and value, resulting in remaining unsold housing units totaling 177,763 units, with a total value of 871,505 million baht, reflecting increases of 0.7% and 1.3%, respectively, compared to the previous quarter.

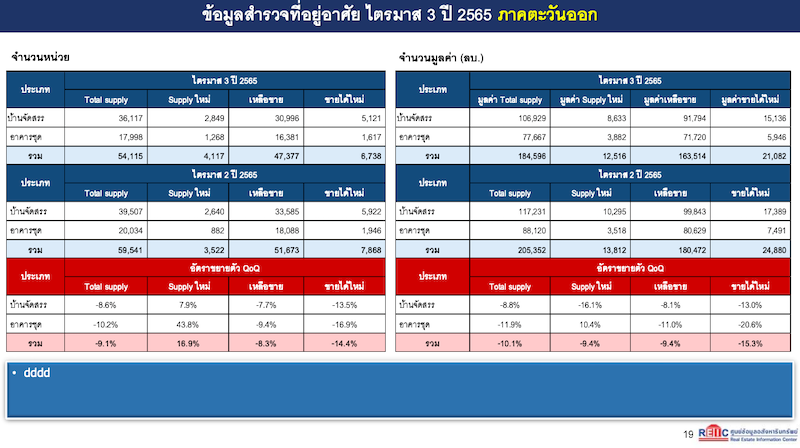

Meanwhile, the EEC area comprising three provinces exhibited a market situation similar to that of Bangkok and surrounding areas, but with a greater decline in the number of units and value of new sales, affecting both housing projects and condominiums, while the overall remaining unsold units decreased more significantly.

The overall market in both areas reflects that the housing market in this quarter has clearly begun to cool down, as evidenced by the decline in new sales compared to the previous quarter, particularly in the condominium category, which saw a significant drop in sales compared to the previous quarter, where many low-priced condominiums were launched and sales were strong in the first two quarters.

• Forecast for Supply and Demand in Housing for 2022

REIC forecasts that the supply and demand for housing in 2022 will see approximately 77,221 land allocation permits issued, an increase of 12.7%, and around 96,803 new housing units launched specifically in the Bangkok and surrounding areas, valued at 508,264 million baht, representing increases of 87.9% and 132.1%, respectively, from the previous year. This includes 49,492 units of horizontal housing valued at 336,008 million baht and 47,311 units of condominiums valued at 172,256 million baht, with approximately 310,976 construction permits expected to be issued, divided into 264,031 units for horizontal housing and 46,945 units for residential condominiums.

As for housing demand in 2022, it is expected that there will be approximately 373,253 residential ownership transfers nationwide, valued at 997,471 million baht, reflecting increases of 8.59% and 5.61% from the previous year, divided into 279,447 units for horizontal housing and 93,806 units for residential condominiums.

Dr. Vichai Wiratthakhan summarized the overall housing market for 2022, stating, "Supply movements have been continuously expanding since Q1 2022, with new projects launched in the Bangkok and surrounding areas, while the issuance of land allocation permits nationwide has significantly increased in Q3, reaching the highest number in 10 quarters. Meanwhile, the issuance of building permits remains stable. On the demand side, ownership transfers for residential properties nationwide have consistently increased in both unit numbers and transfer values, as well as personal housing loans since Q1."

• Housing Market Trends for 2023 under LTV Framework

REIC predicts that in 2023, the real estate market (residential category) will face pressure from the non-renewal of the relaxed minimum down payment measures for housing loans or the "LTV (Loan to Value) measures" from the Bank of Thailand (BOT), which will take effect from January 1, 2023. REIC forecasts that the overall real estate market index (residential category) for 2023 may decrease to 89.5 points, a decline of -1.1% from 2022, with a lower bound of 80.6 points (Worst Case) or a decrease of -11.0%, and an upper bound of 98.5 points (Best Case) or an increase of 8.8%.

The non-renewal of LTV relaxation may lead developers to delay launching new projects, with an expected 98,581 new housing units to be launched in the Bangkok and surrounding areas in 2023, valued at 513,982 million baht, reflecting only a 1.8% and 1.1% increase, respectively, from 2022, comprising approximately 58,312 units of horizontal housing valued at 367,363 million baht and approximately 40,270 units of condominiums valued at 146,619 million baht.

Meanwhile, the issuance of land allocation permits nationwide is expected to be around 79,909 units, an increase of 3.5% from the previous year, with approximately 294,019 building permits expected to be issued, a decrease of -5.5% compared to 2022, and approximately 91,615 completed residential registrations expected, a decrease of -0.1% compared to 2022.

On the demand side, it is projected that there will be approximately 320,227 residential ownership transfers nationwide in 2023, valued at 953,404 million baht, reflecting decreases of -14.2% and -4.4%, respectively, and approximately 614,764 million baht in new loans expected to be issued, a decrease of -4.0% compared to 2022.

"The market situation in 2023 under the control of financial system risks through LTV measures signals a reduction in the intensity of investment expansion in the new housing market, which will also impact the second-hand housing market. Coupled with rising interest rates and gradually recovering purchasing power, it is highly likely that in 2023, the market for properties priced below 5 million baht will see increased demand," Dr. Vichai Wiratthakhan concluded.