Housing Market Outlook for 2022-2023: Signs of Recovery Amid Rising Interest Rates and High Development Costs

Key Highlights

- Krungthai COMPASS estimates the value of the housing market in Bangkok and its vicinity for 2022 at 604 billion baht, recovering by 3.3% YoY, with a further acceleration to 4.2% YoY in 2023. This growth is supported by 1) the recovery of the Thai economy, 2) the return of foreign purchasing power, and 3) the government's potential extension of measures to stimulate the real estate sector, including easing LTV regulations and reducing transfer and mortgage fees for another year.

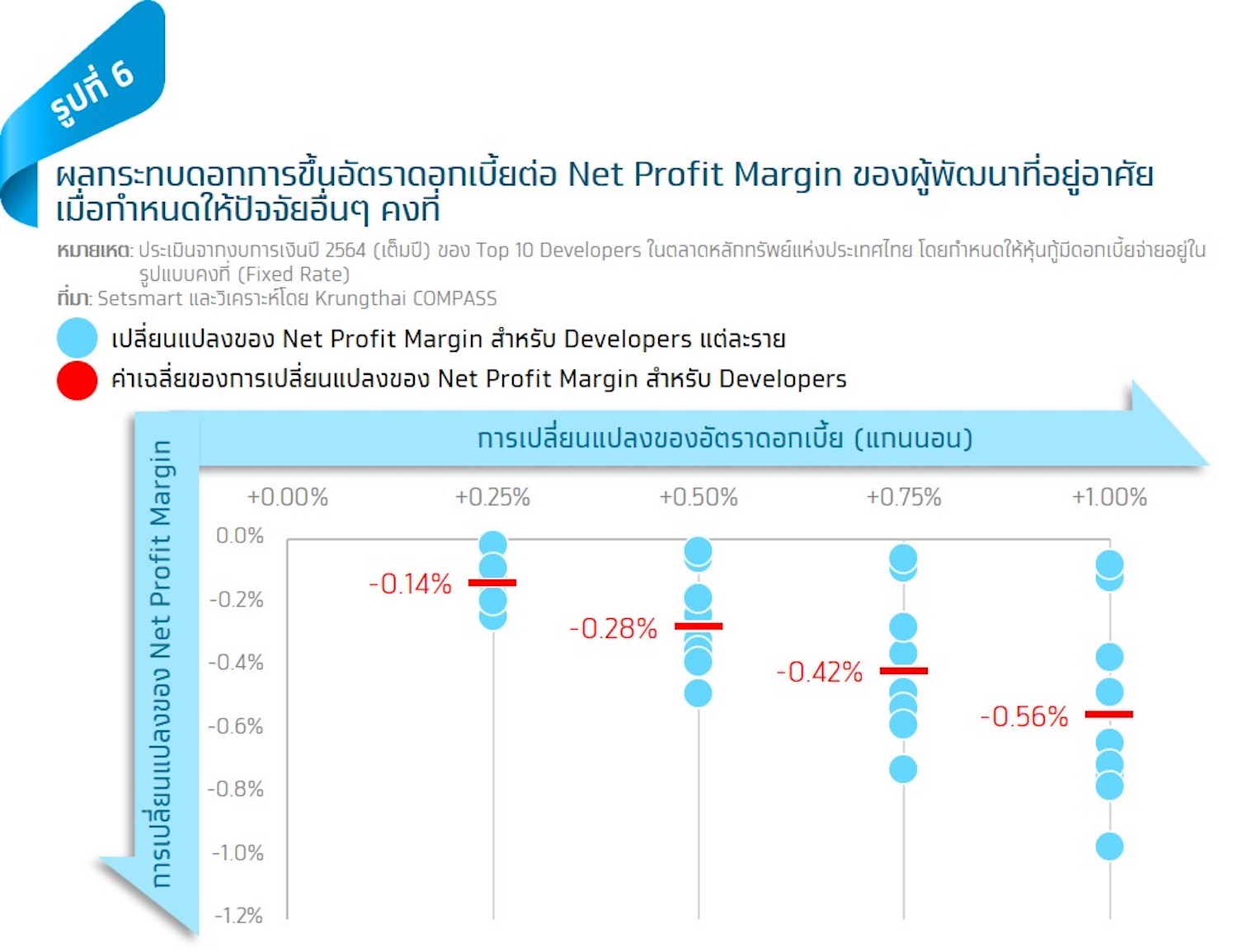

- Rising interest rates will have a direct negative impact on consumers' ability to purchase housing, as each 1% increase in interest rates is expected to reduce the maximum housing value that consumers can afford by approximately 10%. Simultaneously, each 1% increase in interest rates is likely to decrease the Net Profit Margin of housing developers by an average of 0.56% due to higher financial costs.

- The cost of developing new projects during 2022-2023 is expected to remain high due to the sustained high prices of various construction materials, along with continuously rising land prices, which will significantly pressure the profitability of housing developers over the next 1-2 years. However, the anticipated increase in the minimum wage is expected to have a minimal impact on the real estate sector, as wages in the residential construction business are already above the minimum wage.

Kanith Amaskul, Krungthai COMPASS

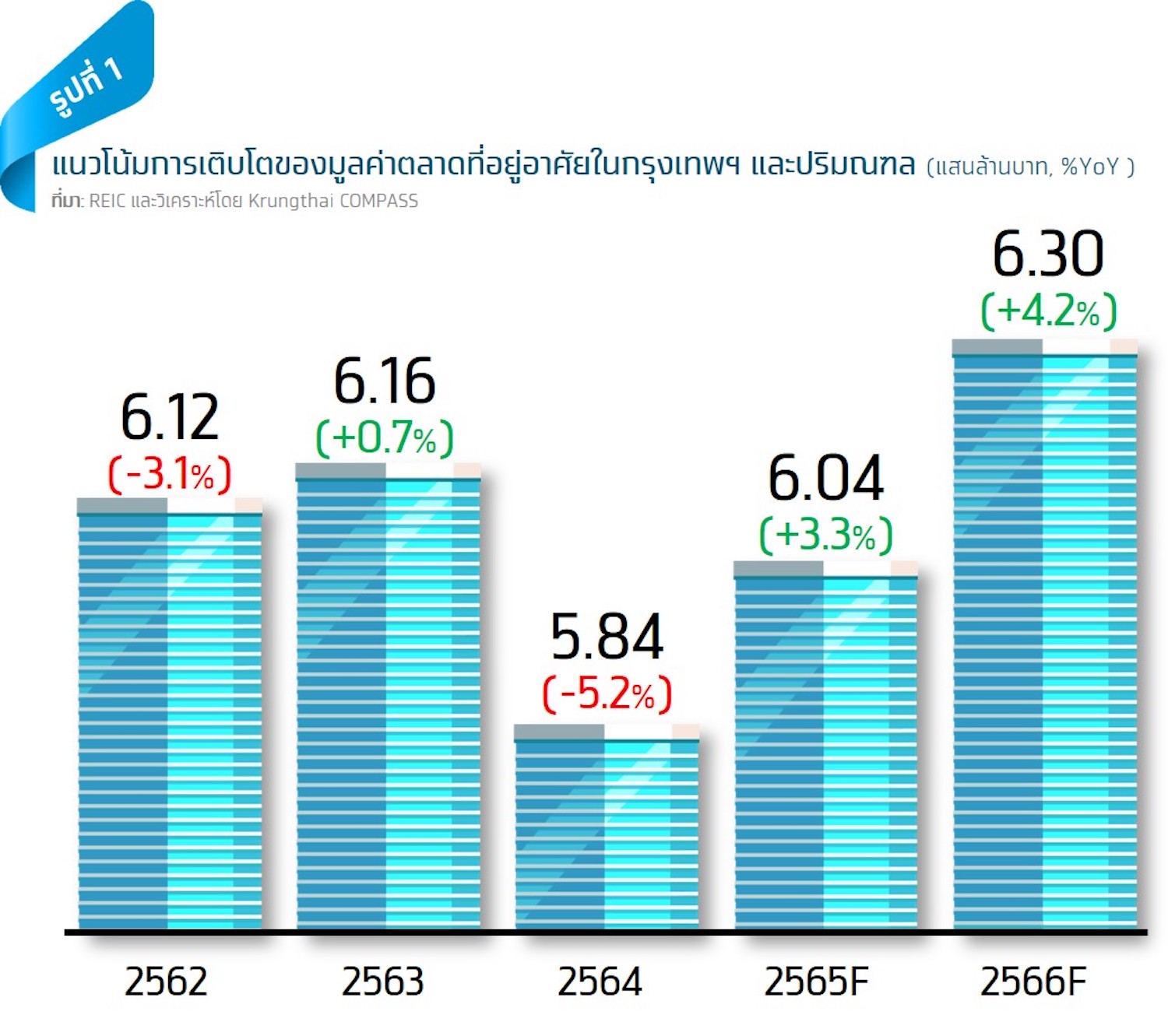

Krungthai COMPASS estimates the value of the housing market in Bangkok and its vicinity for 2022 at 604 billion baht, recovering by 3.3% YoY, with a further acceleration to 4.2% YoY in 2023. The main supporting factors are 1) the recovery of the Thai economy, 2) the return of foreign purchasing power, and 3) the possibility that the government will extend measures to stimulate the real estate sector, including easing LTV regulations and reducing transfer and mortgage fees for another year, originally set to expire at the end of December 2022. However, close attention must be paid to the rising interest rates and high development costs, as both factors will directly affect consumer purchasing and the profitability of housing developers in the next 1-2 years.

Housing Market Value: In 2022, the value of property transfers in Bangkok and its vicinity is expected to recover by 3.3% YoY, amounting to 604 billion baht, supported by 1) the expansion of the Thai economy and 2) measures to stimulate real estate, including easing LTV regulations and reducing transfer and mortgage fees. Residential properties such as single houses, twin houses, and townhouses that better meet the needs of working from home (WFH) continue to receive positive responses from consumers, as reflected in the transfer volumes in the first half of 2022, which grew by 7.2%. For the measures to stimulate real estate, easing LTV allows all borrowers to borrow up to 100%, and the transfer and mortgage fees are reduced to 0.01% for properties valued up to 3 million baht. The Ministry of Finance and the Bank of Thailand are discussing the possibility of extending both measures for another year, from the original expiration at the end of December 2022 to the end of 2023.

For 2023, the continuous growth of the Thai economy and the return of foreign purchasing power due to the normalization of international travel are expected to accelerate the growth of property transfers in Bangkok and its vicinity at a rate of 4.2% YoY, amounting to 630 billion baht. In addition to the ongoing growth of the Thai economy, which is a positive factor for the purchasing power of Thai consumers, the increase in foreign tourists from 8.9 million in 2022 to 21.3 million will positively impact the demand for housing in Thailand, particularly from Chinese buyers, who represent half of the total foreign purchasing power and continue to show interest in the Thai real estate market, as reflected in data from Juwai.com, China's largest overseas property trading website, indicating that Thai properties remain among the top searches and orders in the first half of 2022. The segments that will benefit most from the return of foreign purchasing power are condominiums of 40-50 square meters priced at 4-5 million baht per unit in popular locations such as Sukhumvit, Sathorn, Asoke, Rama 9, and Ratchada.

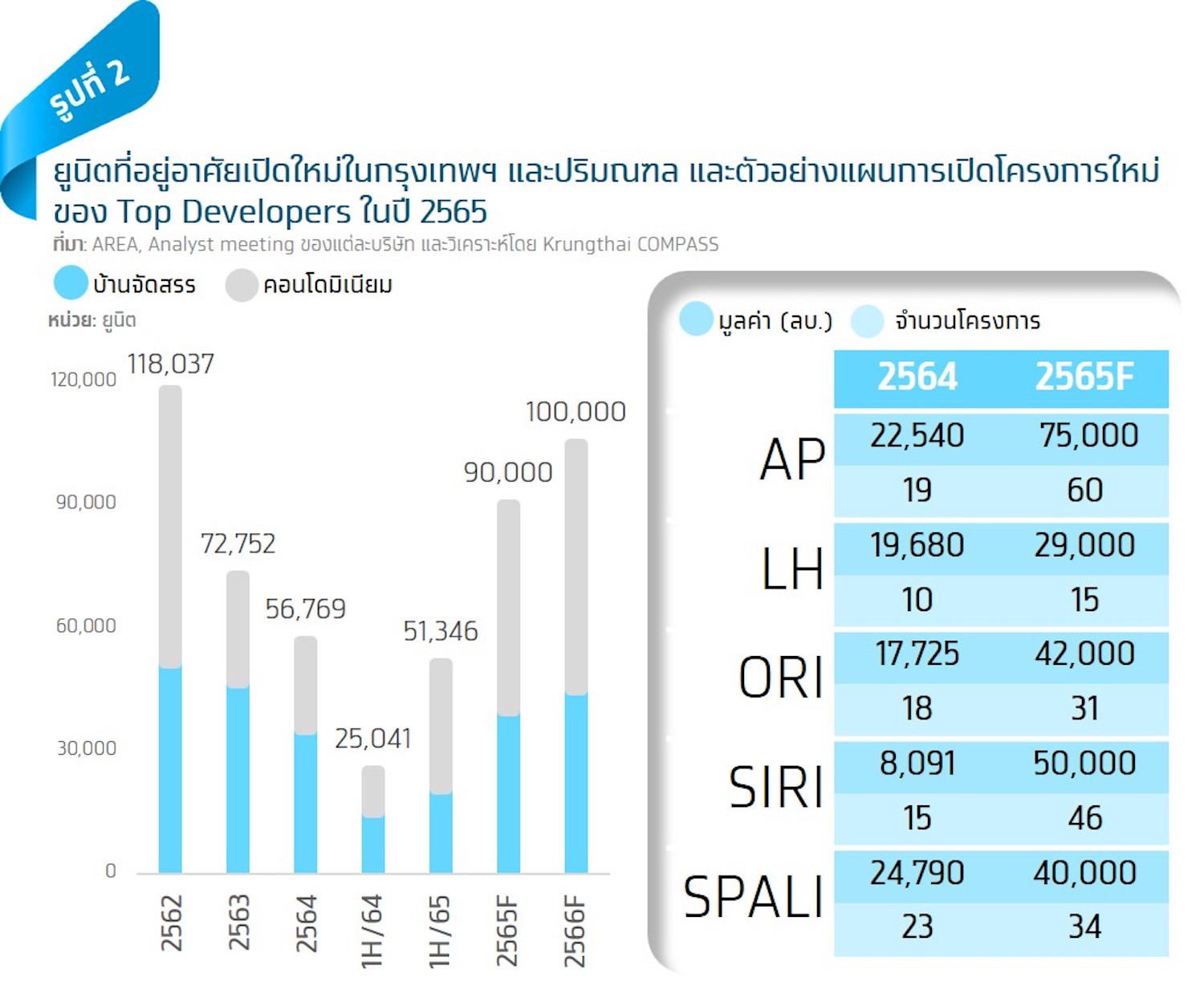

New Projects: In the first half of 2022, the housing market in Bangkok and its vicinity saw approximately 51,500 new units launched, more than double compared to the previous year, comprising 21,500 single houses and 30,500 condominiums. The segments of residential properties that received positive responses from consumers, as reflected in high pre-sale levels, include 1) single houses priced over 20 million baht with a pre-sale rate of 18.9%, 2) twin houses priced at 5-10 million baht with a pre-sale rate of 23.4%, 3) townhouses priced at 5-10 million baht with a pre-sale rate of 57.8%, while 4) the most popular condominium segment is priced at no more than 3 million baht, focusing on providing value to consumers, with a pre-sale rate of 37.4%.

For the entire year of 2022-2023, Krungthai COMPASS expects the number of new units to increase from 56,800 units in 2021 to 90,000-100,000 units per year, comprising 40,000-45,000 single houses and 50,000-55,000 condominiums, as housing developers need to stock up on backlogs. After the COVID-19 outbreak in 2020-2021, most housing developers decided to maintain liquidity by focusing on selling completed stock and delaying the launch of new projects until the situation improved, resulting in low new unit launches of only 65,000 units per year during that period. The upward trend in new unit launches in 2022-2023 aligns with the plans of top developers, nearly all of whom plan to launch new projects in 2022 at higher levels than the previous year, such as AP, which plans to launch 60 projects worth 75 billion baht, up from 19 projects worth 22.54 billion baht in 2021, and SIRI, which aims to launch 46 projects worth 50 billion baht, an increase from 15 projects worth nearly 8.1 billion baht in the previous year. The increase in new units in the single house segment, which generally has a relatively quick construction period of 6-12 months, is another supporting factor for the growth of the housing market value in 2023.

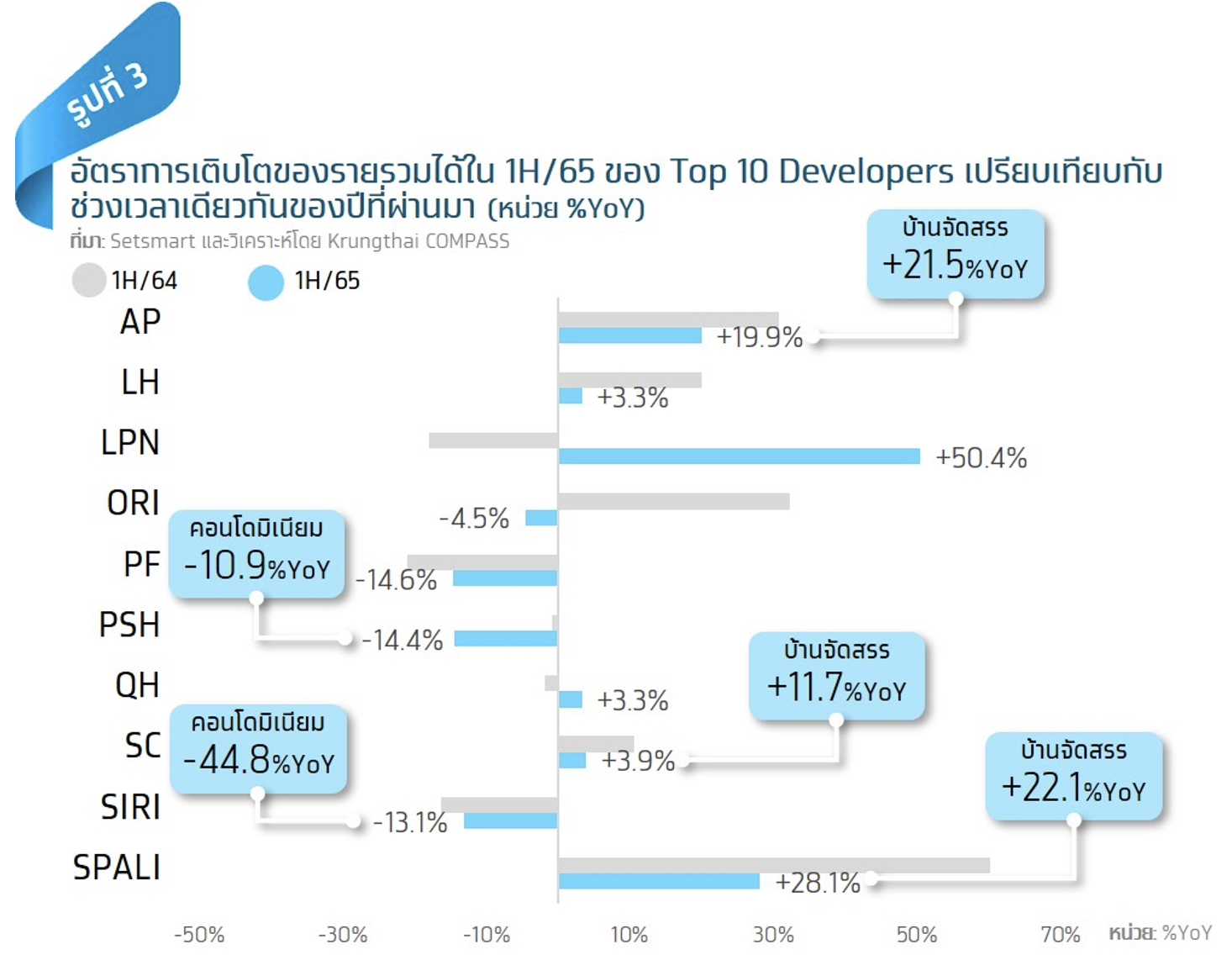

Performance of Operators in the First Half of 2022: The top 10 developers in the Stock Exchange of Thailand reported total revenue of 105.617 billion baht in the first half of 2022, growing by 3.9% YoY, which is higher than the pre-COVID level of 103.128 billion baht in the first half of 2020 by 2.4%. The increase in revenue is mainly due to housing in the single house segment, such as single houses, twin houses, and townhouses, as they continue to meet the needs of consumers working from home better than condominiums. This is reflected in the strong revenue growth in the single house segment among housing developers in the first half of 2022, such as AP, which grew by 21.5% YoY, as well as SC and SPALI, which grew by 11.7% YoY and 22.1% YoY, respectively. However, some housing developers reported a decline in revenue in the first half of 2022 compared to the previous year.

Regarding profitability, the top 10 developers have seen an average net profit margin increase from 12.5% in the first half of 2021 to 12.9%, as competition in marketing promotions has gradually eased. However, compared to the average net profit margin of 15.5% in the first half of 2020, the average profitability remains significantly lower than pre-COVID levels.

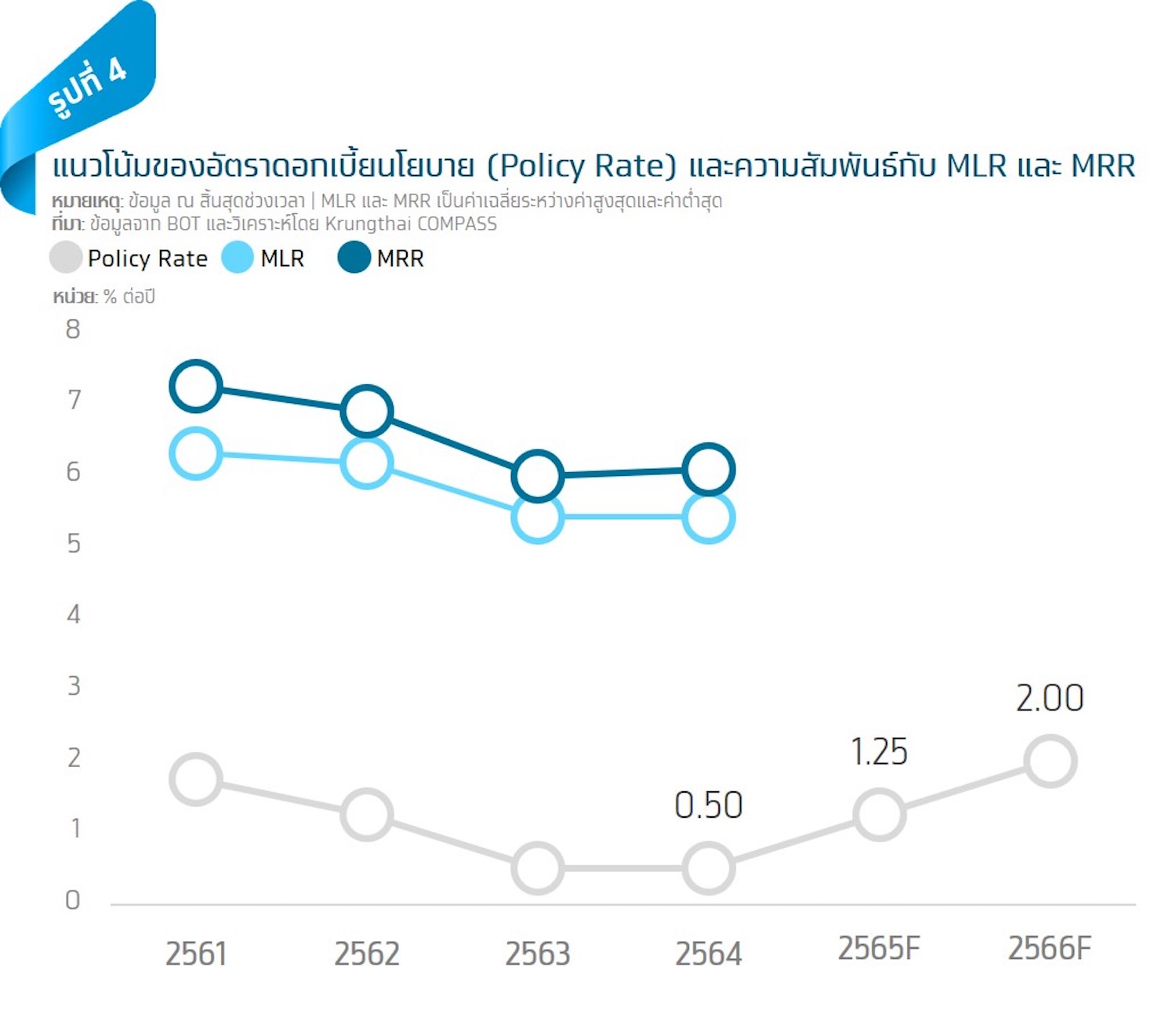

Key Trends to Watch in 2023: The "rising interest rate trend" and "high project development costs" are significant negative factors for the operating costs of housing developers. Rising Interest Rates: Krungthai COMPASS predicts that interest rates will continue to rise from the remaining period of 2022 into 2023, primarily driven by 1) the Bank of Thailand's likely increase in the policy interest rate by another two times from the current 0.75% to 1.25% in 2022, followed by three more increases to 2% in 2023, and 2) the increase in fees for contributions to the FIDF fund, which will revert to the previous rate of 0.46% from the current rate of 0.23% on January 1, 2023. This will impact both consumers and housing developers through rising borrowing costs, as both the Minimum Retail Rate (MRR) and Minimum Loan Rate (MLR) are expected to increase.

- Impact on Consumers: This can be divided into two groups: 1) those currently repaying their housing loans, and 2) those interested in applying for housing loans in the next 1-2 years. For those currently repaying their loans, although their monthly payments remain unchanged, these payments will go towards higher interest, leaving less to reduce the principal. This means that the impact on this group of consumers will manifest as a longer repayment period if interest rates continue to rise.

As for the impact on those interested in applying for housing loans in the next 1-2 years, it is the decrease in the maximum housing value they can afford. We estimate that each 1% increase in interest rates will likely reduce the maximum housing value that consumers can afford by about 10%. For example, at an average interest rate of 5%, a consumer with a repayment capacity of 6,000 baht/month can afford a housing loan of about 1 million baht. However, if the average interest rate rises to 6%, the consumer will need to have a repayment capacity of 6,700 baht/month to afford the same housing price. Therefore, if the consumer maintains the same repayment capacity of 6,000 baht/month, they will need to purchase a property priced lower at 900,000 baht instead.

- Impact on Housing Developers: The increase in interest rates will lead to higher financial costs for housing developers. Assuming other factors remain constant, Krungthai COMPASS estimates that each 1% increase in interest rates will result in an average decrease of 0.56% in the Net Profit Margin of housing developers. The rising interest rate trend in the next 1-2 years will thus pressure the profitability of housing developers. However, the impact of rising interest rates on the Net Profit Margin of each housing developer will depend on various factors, such as the proportion of reliance on funding sources from loans and bonds relative to equity, the proportion of loans and bonds that incur interest at variable rates, and the maturity of bonds. If any housing developer relies heavily on floating rate loans and bonds or needs to roll over bonds to repay existing bonds, they may be more adversely affected by rising interest rates than other developers.

Development Costs Remain High: The prices of various construction materials have risen significantly in the first half of 2022, particularly steel and cement, as well as land prices, which continue to grow even amid the COVID-19 pandemic and in a slow-growing economy. In the first half of 2022, the overall construction material prices increased by 5.8% from 2021, accelerating compared to the average 5-year growth rate of 1.9%. Steel prices increased the most at 10.3%, followed by cement at 5.3%, wood and wood products at 4.2%, tiles at 4%, and electrical and plumbing equipment at 3.8%. For key construction materials like steel, despite the situation in China's real estate sector reducing demand for steel, leading to a potential decline in steel prices in the second half of 2022, the average steel price in 2022-2023 is expected to remain high at 23,500-24,000 baht/ton compared to the average of 20,800 baht/ton over the past 5 years. Similarly, other construction material prices are expected to remain high over the next 1-2 years due to sustained high energy and raw material costs. Regarding land prices, they continue to rise, with the land price index in Bangkok and its vicinity increasing by 2.6% in the first half of 2022 compared to the average in 2021, resulting in higher costs for developing new projects.

The anticipated increase in minimum wage is expected to impact the real estate sector somewhat, but likely not significantly, as most wages in the residential construction sector are already above the minimum wage. Additionally, the current trend of using precast construction technology is helping to reduce labor requirements to some extent.

Summary: Krungthai COMPASS views the housing market for 2022-2023 as expanding, driven by increased purchasing demand from economic growth and the return of foreign purchasing power, along with housing developers planning to launch new projects at a level of 90,000-100,000 units per year to compensate for the low number of new projects launched in the past 1-2 years. Furthermore, the housing market has upside potential from government support measures, including easing LTV regulations and reducing transfer and mortgage fees, which may be extended for another year from their original expiration at the end of 2022, as the Ministry of Finance is currently discussing this with the Bank of Thailand. However, attention must also be paid to the downside risks in the housing market, including 1) rising interest rates, which we estimate will reduce the maximum housing value that consumers can afford by about 10% for each 1% increase in interest rates, and will decrease the net profit of housing developers by 0.56% due to higher financial costs, and 2) high development costs from sustained high construction material prices and continuously rising land prices.

[1] Reference Finance Ministry Meets with BOT to Discuss Extending Real Estate Stimulus Measures for Another Year

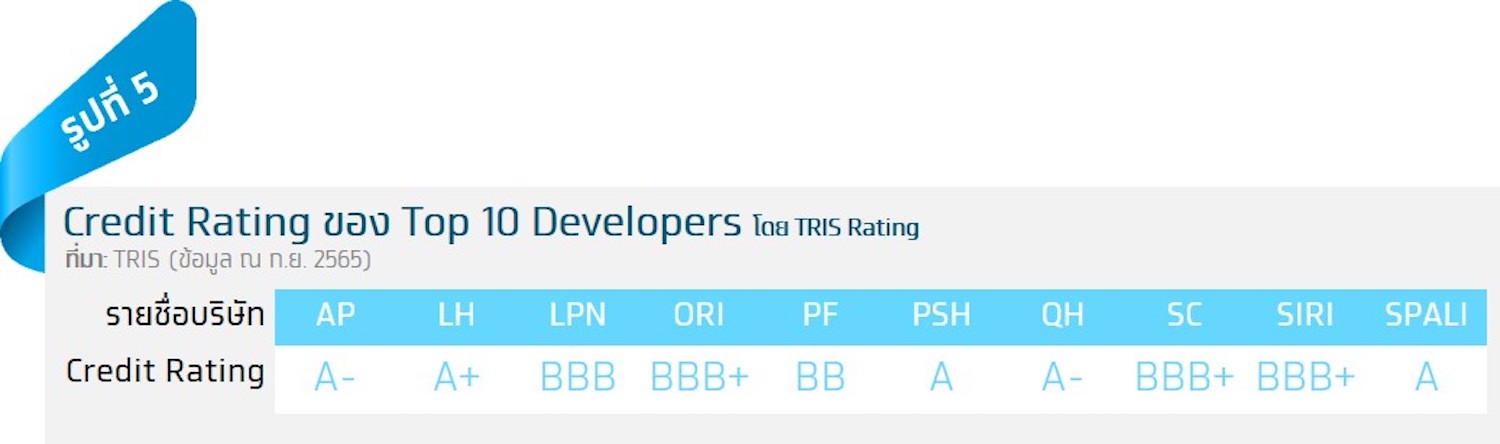

[3] Includes AP, LH, LPN, ORI, PF, PSH, QH, SC, SIRI, and SPALI

[4] In 2020, the reduction of the FIDF fee from 0.46% to 0.23% immediately resulted in a reduction of MLR, MOR, and MRR loan interest rates by 0.40%.

[5] This impact also includes those currently repaying fixed-rate loans in the first 3 years, as the interest rate will change to variable in the fourth year.

[6] Estimated based on a 30-year housing loan repayment, assuming a fixed average interest rate throughout the contract.

[7] Includes electrical and telephone conduit pipes, electrical wires, water gates, PVC pipes, faucets, and filter screens, etc.