DDproperty Predicts Continued Challenges for the Real Estate Market in 2024 - Slow Economic Recovery and High Interest Rates Hinder Thai Homeownership

The real estate market in 2023 has been another year where both consumers and operators face ongoing challenges from the previous year. The main factors include slower-than-expected economic growth and high interest rates, which have led to a decline in consumer purchasing power. DDproperty, Thailand's number one real estate marketplace website, has released the DDproperty Thailand Property Market Outlook 2024 report, which compiles analytical data from various aspects to summarize the overall real estate market in 2023 from both demand and supply perspectives. It also forecasts trends in the real estate market to watch for in 2024, helping buyers, sellers, renters, or investors understand the housing market dynamics and make more confident decisions in real estate.

Summary of the Real Estate Market in 2023: Sluggish Purchase Prices, Strong Rental Market

The overall real estate market in 2023 continued to slow down due to various factors, coupled with a lack of significant measures to stimulate the real estate sector that would attract consumers. This has resulted in a continued decline in purchasing power in line with the economic situation, while housing prices are trending upward due to rising construction costs, leading to a growing trend in residential rentals that remains popular and shows interesting growth.

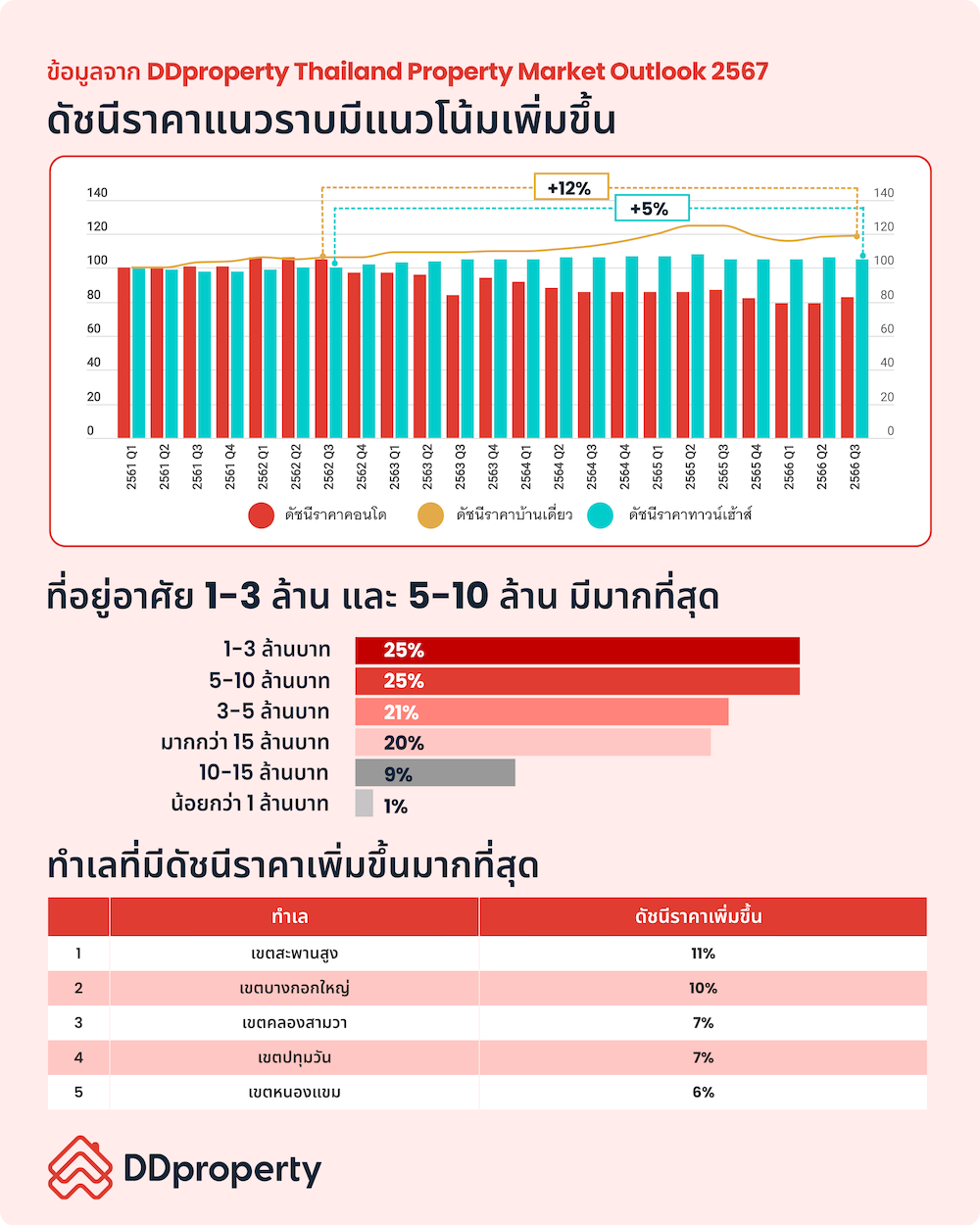

- Real estate price index decreased by 5% over the year, with condominiums seeing the largest drop. According to the latest report from DDproperty Thailand Property Market Outlook 2024, the residential price index in Bangkok increased by 3% in Q3 2023 compared to the previous quarter (QoQ) but decreased by 5% year-on-year (YoY) and dropped by 7% compared to the same period before the COVID-19 pandemic (Q3 2019). However, it is predicted that in 2024, the index for single-family homes is likely to rise again due to construction costs and higher land prices.

When categorized by type of residence, it was found that by the end of 2023, only townhouses maintained stable price indices, while condominiums and single-family homes saw price indices decrease (down 5% YoY and down 4% YoY, respectively). However, when compared to the pre-pandemic period, the price index for horizontal housing has shown interesting growth, with single-family homes increasing by 12% and townhouses by 5%, in contrast to condominiums, which saw a significant decrease of 21%, reflecting the recovery of vertical housing that has not yet returned to its previous state.

For locations with the highest price index increases over the past year, most are in the outskirts of Bangkok's business district and outer Bangkok areas, such as the Saphan Sung district, which saw an 11% YoY increase, followed by the Bangkok Yai district with a 10% YoY increase, Khlong Sam Wa district with a 7% YoY increase, Nong Khaem district with a 6% YoY increase, Bang Na district with a 5% YoY increase, and Bang Phlat district with a 4% YoY increase. In the central business district (CBD) of Bangkok, the areas with price index increases include Pathum Wan district with a 7% YoY increase and Wattana district with a 6% YoY increase.

- Rental index surged by 9% over the year, with high-rise residences meeting tenant needs. Due to economic factors affecting consumer purchasing power, the trend of renting residential properties has shown significant growth, with the overall rental index in Bangkok increasing by 9% YoY, indicating that the rental market still has an interesting growth trajectory in the capital, despite a 1% decrease from the pre-pandemic period. This is likely due to price stabilization efforts to encourage rental decisions amid increasing competition.

When categorized by type of residence, high-rise residences such as condominiums and apartments remain popular, with the rental index increasing by 10% YoY but decreasing by 4% from the pre-pandemic period, in contrast to horizontal residences like single-family homes and townhouses, which decreased by 2% YoY but increased by 60% from the pre-pandemic period, reflecting a clear shift in living trends.

For locations with the highest rental index increases over the past year, most are in areas with high demand for rental housing and near public transport lines, such as Pathum Wan district with a 16% YoY increase, followed by Wattana district with a 13% YoY increase, Khlong San district with a 12% YoY increase, Bang Sue district with an 11% YoY increase, Bang Kho Laem district with a 10% YoY increase, Din Daeng district with a 10% YoY increase, Ratchathewi district with a 9% YoY increase, Thon Buri district with a 9% YoY increase, Huai Khwang district with an 8% YoY increase, and Khlong Toei district with an 8% YoY increase.

- Watch for shrinking demand for buying and renting, but still growing compared to pre-COVID levels. Focusing on the index of demand for residential purchases in Bangkok over the past year, the overall index decreased by 31% YoY but increased by 9% compared to the pre-pandemic period. When categorized by type of residence, it was found that the demand index for all types decreased, with single-family homes seeing the largest decline of 34% YoY but increasing by 16% from the pre-pandemic period. Townhouses decreased by 30% YoY but increased by 15% from the pre-pandemic period, while condominiums decreased by 30% YoY but increased by 4% from the pre-pandemic period.

When categorized by price level, it was found that the price levels of 1-3 million baht and 5-10 million baht accounted for the largest share over the past year, each making up 25% of the total residential properties in Bangkok. The next largest share was the 3-5 million baht level (21%). However, when separated by type of residence, it was found that for the 1-3 million baht price level, townhouses had the largest share at 39%, while condominiums had a share of 26%, reflecting that the purchasing power of middle to lower-income consumers has not yet returned, resulting in the largest share of properties at this price level remaining stagnant. Meanwhile, single-family homes priced over 15 million baht had the largest share (44%), due to developers choosing to launch projects at higher prices to target the higher purchasing power market. At the same time, upper-income consumers, who are the limited group of actual homebuyers, continue to delay home purchases and turn to other types of investments instead. The rental demand index for residential properties in Bangkok over the past year, although it decreased by 21% YoY, has increased by as much as 147% compared to the pre-pandemic period, with all types of residences showing an increase, especially condominiums, where rental demand increased by 185% from the pre-pandemic period, reflecting that the rental trend still meets the needs of consumers who do not want long-term financial commitments and want to avoid financial impacts from interest rates. This is followed by single-family homes increasing by 38% and townhouses increasing by 11%.

For the rental levels with the highest volume of properties in the market, the rental level of 10,000-30,000 baht/month meets the needs and aligns with the rental capabilities of most consumers. When separated by type of residence, it was found that condominiums at the rental level of 10,000-30,000 baht/month accounted for as much as 50% of the total rental levels, while townhouses at this rental level accounted for 35%. In contrast, single-family homes at rental levels above 100,000 baht/month accounted for as much as 50%.

Examining the Driving Factors for the Real Estate Market in 2024: Opportunities or Challenges Not to Be Overlooked?

The DDproperty Thailand Property Market Outlook 2024 report predicts that the overall real estate market in 2024 will continue to face ongoing challenges from the previous year, including an economic recovery that is not as robust as expected. High household debt and interest rates directly impact consumer purchasing power, leading developers to focus on projects targeting middle to upper-income consumers, who are more prepared to purchase homes than lower-income consumers who are more sensitive to economic changes and are the group most often denied credit.

However, it cannot be denied that the growth of the real estate sector requires simultaneous driving forces from the government, operators, and consumers. If the economic situation continues to show signs of recovery and the government implements additional concrete measures to stimulate the real estate sector, it is expected that the overall real estate market in 2024 will grow by about 5-10% from the previous year, with key factors influencing the growth of the real estate market to watch for, including:

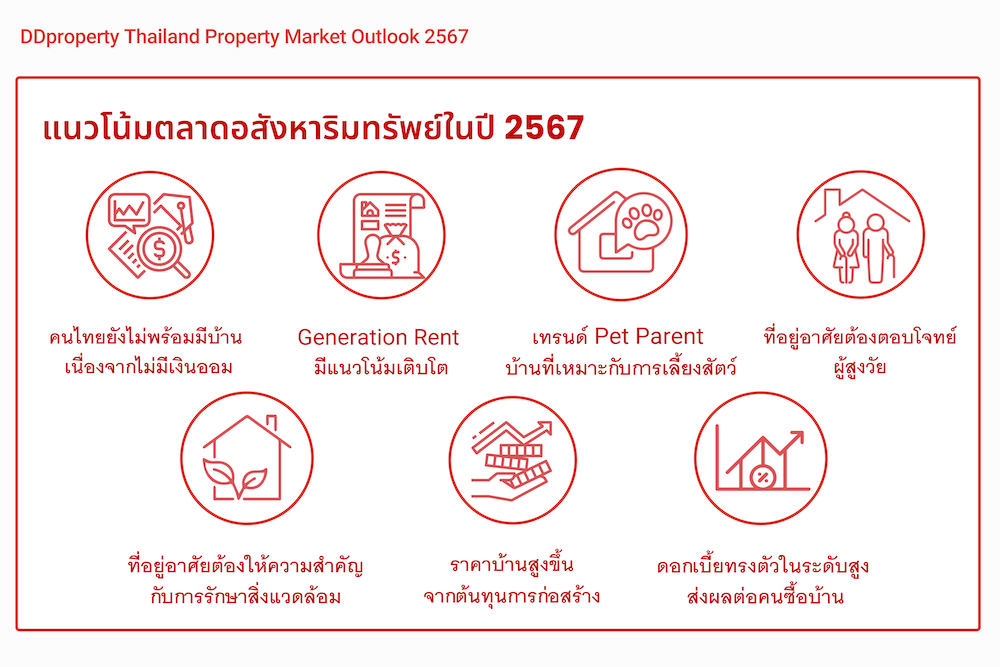

- Lack of financial liquidity hinders homeownership readiness. According to the latest consumer sentiment survey regarding the housing market, the challenges of economic conditions and rising interest rates have directly impacted consumers' financial liquidity, reducing their ability to purchase homes to 63% (down from 65% in the previous round). When considering financial readiness, which is a crucial factor when thinking about buying a home, only 24% have sufficient savings to buy their own home at this time, while the majority of consumers (54%) have saved only halfway, and 21% have not started any savings plans.

At the same time, financial factors remain a major challenge when applying for home loans, especially among actual homebuyers (Real Demand), who are mostly middle and lower-income consumers. More than half (56%) reported that unstable income and employment are significant barriers to obtaining home loans, followed by 32% citing poor financial history and 29% having an unfavorable debt-to-income ratio (Debt Service Ratio: DSR). Additionally, most consumers feel that government policies are not conducive enough to homeownership, with only 15% believing that the government is making sufficient efforts to help them buy their own homes, down from 19% in the previous round due to the lack of new measures to stimulate the real estate sector in the past year.

- Generation Rent is thriving; younger generations prefer renting over buying. The trend of Generation Rent continues to gain popularity as the perspective on homeownership among younger generations has changed. Although working-age consumers are the primary target group in the real estate market, amid such uncertain economic conditions, consumers do not want to increase expenses from purchasing homes/condominiums that would become long-term commitments. Renting offers flexibility and mobility for future relocations and helps save expenses, leading to a significant increase in rental demand, contrasting with the decreasing demand for purchases. The main factors driving consumers to choose renting instead are that nearly 2 in 3 (64%) of renters report insufficient savings to buy a home, while 41% believe that housing prices are too high, and 30% do not see an urgent need to buy at this time, reflecting that financial challenges remain a crucial factor and a turning point for consumers to choose renting instead.

- The Pet Parent trend: Pets are important family members. The Pet Parent trend, or Pet Humanization, involves treating pets as children and caring for them as family members. This aligns with the current lifestyle trend where more Thais are choosing to remain single or marry without children, leading them to seek pets for companionship. This has resulted in a growing interest in housing projects that cater to this lifestyle.

Therefore, current and future housing must pay more attention to this trend, not only allowing pets but also providing amenities and facilities that support the lifestyle of pets comprehensively, including living space suitable for pets, scratch-resistant materials or furniture, balcony designs that prevent falls, or ventilation systems within projects, as well as common areas that accommodate play or recreation for pets. Additionally, it is essential to clearly delineate between common areas for pet-loving residents and those without pets or those allergic to pet hair, allowing them to coexist harmoniously and hygienically.

- Universal Design meets the needs of the elderly, covering everyone in the family. Thailand has fully entered an aging society since 2022, and data from the Ministry of Commerce's Policy and Strategy Office predicts that by 2040, there will be 20.4 million elderly people, accounting for 31.3% of the country's population. Meanwhile, data from the DDproperty Thailand Consumer Sentiment Study shows that the majority of consumers (63%) have started planning for retirement, especially among middle-income groups.

The rapid growth of the elderly population necessitates the real estate sector to adapt to meet the changing needs of home seekers, from project design that prioritizes the living conditions of the elderly through the concept of Universal Design, which allows all groups to live conveniently and safely, covering both external and internal areas of homes.

- Eco-friendly housing: A sustainable trend for the future. As the world enters an era of global warming, many parties are becoming increasingly aware of climate change and environmental issues. This is evident as real estate developers begin to continuously develop projects that promote the use of clean energy and pay attention to environmental issues from the construction stage, such as using non-toxic materials or reducing carbon dioxide emissions in the production process, as well as supporting the use of clean energy, such as installing solar systems in projects or EV charging points in homes.

Similarly, consumers are equally concerned about environmental issues. Data from the latest DDproperty Thailand Consumer Sentiment Study shows that the majority of consumers (91%) are willing to pay more for environmentally friendly and health-conscious housing. Additionally, 71% of consumers want spaces for air-purifying plants and plan to avoid purchasing homes in areas prone to PM 2.5 dust problems.

- Home prices in 2024 will rise in line with construction costs. Housing prices in 2024 are expected to increase due to the continuous rise in construction costs since the previous year, including raw material prices and operational costs, as well as higher energy prices affecting transportation costs. According to the Real Estate Information Center of the Government Housing Bank (REIC), the standard home construction cost index in Q3 2023 increased by 0.1% QoQ and 1.5% YoY.

Moreover, the increase in the minimum wage in 2024, new land appraisal prices, and rising land prices in Bangkok and surrounding areas are all unavoidable construction cost increases, which are expected to lead to a necessary increase in housing prices in 2024 by 5-10% from the previous year, impacting consumers' decisions to own homes as well.

- High interest rates deter home purchases. Interest rates in Thailand are expected to continue rising. Although the latest meeting of the Monetary Policy Committee (MPC) decided to maintain the policy interest rate at 2.50% per annum, it remains at a high level, the highest in 10 years. The continuous increase in the policy interest rate allows financial institutions to raise loan interest rates accordingly, directly affecting real estate developers who must bear increased financial costs, while homebuyers must also pay higher mortgage interest.

It is expected that in 2024, financial institutions will remain strict in approving home loans to control the ratio of non-performing loans (NPL). According to a report from the National Credit Bureau, the special mention loan group (SM) or home loans that are overdue by 1-3 months in Q3 2023 increased by 37.2% YoY, mostly for homes priced below 3 million baht.

This reflects that lower-income consumers continue to be affected by the previous pandemic, combined with rising living costs, leading to a lack of financial liquidity, causing financial institutions to deny home loans for properties priced below 3 million baht to prevent potential bad debts. The rejection rate for loans in this group is expected to remain high.

- The real estate market recovers slowly in line with the economic situation. The overall Thai economy is growing slowly. Although the tourism sector is recovering and private spending is increasing, the growth of gross domestic product (GDP) is still affected by reduced private sector investment and low public spending, resulting in slower-than-expected economic growth. Coupled with high interest rates, this directly impacts the growth of the real estate market, leading to a decrease in property transfer transactions in Q3 2023.

However, although the demand index for purchases is trending downward, it is expected to increase in 2024. Data collected continuously since 2018 shows that the trend of the demand index for residential purchases tends to rise in the first quarter of each year. Interestingly, in the past year, selling prices have tended to increase since the beginning of the year, amid high interest rates, which has led buyers to delay their home purchase plans. At the same time, rising costs are pushing developers to set higher selling prices as well, creating tension between buyers and sellers, which is likely to continue in 2024, similar to other markets in Southeast Asia, unless unexpected events occur that necessitate a price adjustment.

Note: The DDproperty Thailand Property Market Outlook is a comprehensive report analyzing and forecasting the direction of the real estate market based on the compilation of price index data and demand index of various types of residences in both the buying-selling and rental markets, as well as consumer confidence over the past 12 months. This analysis aims to help buyers, sellers, renters, or investors understand the dynamics of the real estate market and enable them to plan or make confident buying-selling-renting decisions.

Read and study the full overview of the real estate market in 2024 from the DDproperty Thailand Property Market Outlook 2024 report.

For more details, visit PropertyGuruGroup.com; PropertyGuru Group on LinkedIn.

1 Data reference from SimilarWeb between April - September 2023.

2 Data reference from Google Analytics between April - September 2023.

3 Data from July - September 2023.

4 Data from April - September 2023.