The Important Role of Advanced Biofuel in Reducing Greenhouse Gas Emissions in the Transportation Sector

Key summary

• Advanced biofuels will play a crucial role in achieving greenhouse gas reduction targets for heavy-duty vehicles such as trucks and airplanes. Since biofuels have properties similar to fossil fuels, they can be blended without significant infrastructure and engine modifications, making them a vital option for the transition to clean energy.

• Currently, there are concerns about the life-cycle sustainability of biofuels, particularly regarding food security and agricultural issues. Biofuels produced from food crops lead to competition for raw materials between the food consumption and energy sectors, potentially causing shortages and rising food prices. Additionally, increasing yields requires substantial resources, impacting the environment and ecosystems in various ways.

• Advanced biofuels are being developed to ensure sustainability throughout the supply chain by utilizing non-food raw materials, such as agricultural waste and energy crops, and adopting more environmentally friendly cultivation and production processes.

• However, advanced biofuel technology is still in its infancy and lacks technological breakthroughs, making it unable to compete with other fuels due to high costs and properties that do not match fossil fuels. Therefore, investment in research and development is crucial to strengthen and enhance the industry's efficiency.

• Thailand has the opportunity to develop its existing biofuel industry into advanced biofuels by leveraging its raw material advantages and existing knowledge. The Thai agricultural sector has a wealth of agricultural waste with potential for advanced biofuel production, and this opportunity can also add value to waste materials and integrate them into a circular economy.

• Particularly, Sustainable Aviation Fuel (SAF) presents a great opportunity for Thailand to meet the anticipated demand from the global private sector's commitment to achieving net-zero emissions in aviation, leading to a need for SAF refueling in Thailand as well.

• Support from the government and collaborative goals from all stakeholders will be key to developing advanced biofuels. Government policies should be clear and consistent, referencing the potential and efficiency of domestic technology, allowing flexibility to adapt to changes, and creating market mechanisms that promote competition while developing an environment that encourages cooperation across all sectors for effective and sustainable development.

The transportation sector is one of the largest sources of greenhouse gas emissions, accounting for about 17% of global emissions. The primary cause of these emissions is the combustion of fossil fuels in internal combustion engines and jet engines. As governments and private sectors worldwide aim to achieve net-zero emissions, the transportation sector has garnered significant attention for reducing greenhouse gas emissions. Current efforts to reduce emissions in transportation focus on:

1. Increasing public transport usage

2. Improving fuel efficiency of engines

3. Developing zero tailpipe emission technologies, such as battery electric vehicles or hydrogen fuel cell electric vehicles.

4. Developing alternative fuels to replace fossil fuels.

This article will focus on the development of biofuels to reduce greenhouse gas emissions for vehicle groups that are difficult to transition to clean technologies like battery electric and hydrogen fuels, divided as follows:

• The important role of biofuels in reducing greenhouse gas emissions in the transportation sector is significant as they do not require new engine and infrastructure development, making them a key option in the transition to clean energy, especially for heavy-duty vehicles with limitations in developing new clean tech. Furthermore, they can add value to waste materials and be part of the circular economy.

• The challenges of advanced biofuel industry include creating sustainability throughout the supply chain, enhancing competitiveness with other fuel types, and developing drop-in properties that make them comparable to fossil fuels.

• Thailand's opportunity to develop its biofuel industry into advanced biofuels lies in enhancing the existing biofuel industry's potential and leveraging raw material advantages, particularly from Sustainable Aviation Fuel (SAF), which can be initiated immediately due to existing demand and market.

Biofuels will play a crucial role in reducing greenhouse gas emissions in the transportation sector due to three advantages:

- No need to build new infrastructure or develop new engine types, making them a key option in the transition to clean energy.

- Can be used in heavy-duty vehicles that have limitations in developing new technologies like battery electric and hydrogen fuels.

- Can add value to agricultural waste and be part of the circular economy.

Biofuels are key to reducing greenhouse gas emissions in the transportation sector.

In the transition to clean energy, biofuels are an important option for reducing greenhouse gas emissions as they do not require investment in new infrastructure or engine development. Currently, the use of biofuels in various vehicle engines involves blending biofuels like ethanol or biodiesel with fossil fuels, allowing the use of existing infrastructure, from oil transport systems, storage facilities, gas stations, to engines. This means there are no limitations in distributing fuel to users, unlike battery electric and hydrogen technologies that require entirely new infrastructure and supply chains.

In the past, Thailand has continuously expanded the use of biofuels, mandating that all types of gasoline and diesel must contain biofuel blends since 2007, starting with a 10% ethanol blend in gasoline and a 2% biodiesel blend in diesel, gradually increasing the blending ratios. Currently, there are E10, E20, and E85 gasoline products and B7, B10, and B20 diesel products, with ethanol and biodiesel consumption currently at approximately 4.4 and 5.2 million liters per day, respectively, reflecting annual growth rates of 17% CAGR and 32% CAGR.

In the near future, light- and medium-duty vehicles, such as personal cars and pickup trucks, are likely to be replaced by electric vehicle technology. According to the International Energy Agency (IEA), road oil consumption will gradually decline with the rise of personal electric vehicles, which are expected to reach 60 million units by 2026, up from 7.2 million units in 2019. The decline in usage will be concentrated in small and medium vehicles, while other heavy-duty vehicles will continue to rely on internal combustion engines.

Although battery electric and hydrogen technologies have garnered significant attention as technologies to reduce greenhouse gas emissions in the transportation sector, only electric vehicles show potential for increased usage in the near future, limited to small and medium vehicles.

Thus, fossil fuels and internal combustion engines will remain the primary energy sources and engines for heavy-duty vehicles and long-distance travel in the near future, accounting for about 50% of greenhouse gas emissions in the transportation sector. Therefore, biofuels that can be blended immediately meet the demand for reducing greenhouse gas emissions and will be a crucial technology in achieving net-zero emissions goals.

Transportation sectors that are difficult to transition to clean technologies like battery electric and hydrogen fuels in the short to medium term include:

- Large trucks and long-haul trucks, which primarily use diesel engines, can utilize biodiesel as biofuel. Currently, blending rates vary according to each country's policies, such as 7%, 10%, 20%, or 30%. Biofuels will serve as transition fuels while waiting for clean technologies like battery electric and hydrogen to become widely available in the long term.

- Airplanes face significant limitations in modifying engines and airframes. Although battery electric or hydrogen airplanes may be feasible for long-term use (post-2050), industry experts believe they will be limited to small and short-haul aircraft. Long-haul aircraft will require jet engines and will continue to rely on fuels with properties similar to aviation fuel.

Sustainable Aviation Fuels (SAF) will thus be the primary transition fuel for airplanes. Aviation biofuels blended with aviation fuel can be produced from the same raw materials used for ethanol and biodiesel production. Since aviation fuel properties lie between gasoline and diesel, SAF production depends on the chosen technology pathway and raw materials. Currently, the global share of aviation biofuels remains below 1% of total aviation fuel usage, as production technology is still in development and testing phases.

- Ships have more flexible internal combustion engines than those in cars and jet engines, allowing them to accommodate a wider variety of fuels. Thus, ship engines do not require fuels with specific properties like those of cars and airplanes. Additionally, the shipping sector is beginning to research and develop engine technologies to support a wider range of fuel types (multi-fuel engines).

Biodiesel that can be used in ship engines has properties similar to bunker fuel and diesel for ships. However, biofuels are currently more expensive than the bunker fuel or diesel used by ships, and there is competition for biofuel supply from the automotive and aviation sectors, making biofuels less likely to be a viable option for reducing greenhouse gas emissions in the shipping sector in the near future.

Three challenges facing the biofuel industry include:

- Ensuring sustainability throughout the biofuel production supply chain.

- Making biofuel prices competitive with other fuel types in the market.

- Developing drop-in biofuels that have properties similar to fossil fuels.

Sustainability concerns

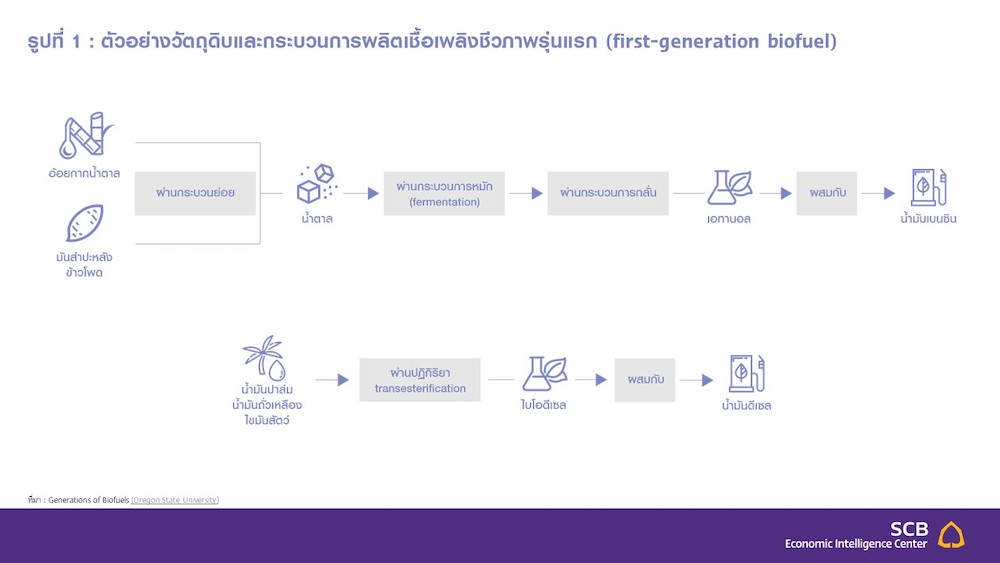

Although biofuels reduce greenhouse gas emissions from burning oil in engines more than fossil fuels, there are still concerns about life-cycle sustainability of biofuels, particularly regarding food security and agricultural land issues. Most current biofuels or first-generation biofuels are produced from crops that can be used for human and animal food, such as cassava, sugarcane, palm oil, corn, and soybeans, leading to competition for food crops between the food consumption and energy sectors. This may result in food shortages and drive up food prices. For instance, in 2021, U.S. refineries increased demand for biofuels due to clean fuel support measures, causing vegetable oil prices to rise more than threefold.

Figure 1: Examples of raw materials and production processes for first-generation biofuels

Moreover, cultivation requires large areas to increase yields to meet high demand from the transportation sector. In some areas, this may lead to encroachment into forest areas, reducing forests that absorb carbon and are vital to ecosystems. Ultimately, the net greenhouse gas emissions from the entire process, from cultivation to engine use, may not decrease or may even exceed those from fossil fuel use when considering deforestation and emissions from agriculture. This concern has led some countries to announce reductions in first-generation biofuel use. For example, the European Union has implemented measures to limit and set long-term goals to phase out biodiesel produced from palm oil from Indonesia and Malaysia, citing deforestation issues.

Additionally, increasing yields requires significant resources and impacts the environment and ecosystems in various ways, such as increased water resource usage, fertilizer and chemical use that may degrade soil quality and contaminate water sources, and monoculture practices that may harm biodiversity. Thus, first-generation biofuels produced from food-based raw materials are considered unsustainable and not environmentally friendly enough.

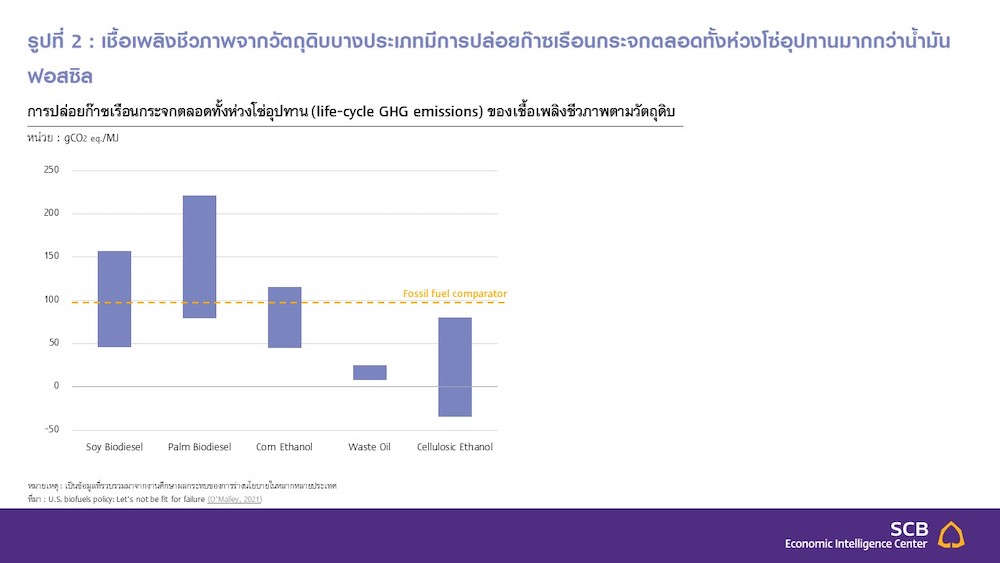

Figure 2: Some types of biofuels release more greenhouse gases throughout the supply chain than fossil fuels

Life-cycle GHG emissions of biofuels by raw material

Note: Data compiled from impact studies of policy drafting in various countries

Source: U.S. biofuels policy: Let’s not be fit for failure (O’Malley, 2021)

‘Advanced Biofuel’ for sustainability throughout the supply chain

To ensure that biofuel use is environmentally sustainable from production to end-use, advanced biofuels are being developed from non-food raw materials. The development and design of new biofuels aim to achieve environmental sustainability objectives, such as reducing life-cycle GHG emissions from raw material cultivation, transportation, refining, and end-use, managing water resources efficiently, avoiding competition for food raw materials, preventing deforestation, and maintaining ecosystem balance.

Thus, the definition of advanced biofuels (advanced biofuels) is set for biofuels that use raw materials not directly in the food production chain and are more sustainable and environmentally friendly. Currently, advanced biofuels being developed include:

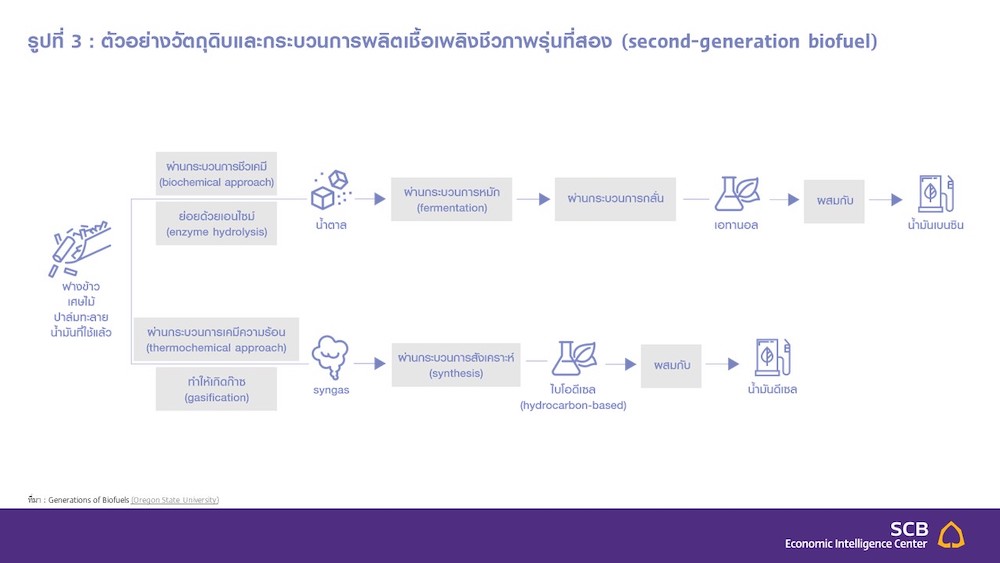

- Second-generation biofuels that use raw materials that cannot be used for human food and are waste materials like lignocellulosic biomass, such as corn stover, rice straw, palm fronds, wood scraps, etc., including other types of waste. These raw materials are already waste, making them low-cost and abundant compared to food crops that can be directly consumed, thus reducing resource competition between the energy and food consumption sectors.

Figure 3: Examples of raw materials and production processes for second-generation biofuels

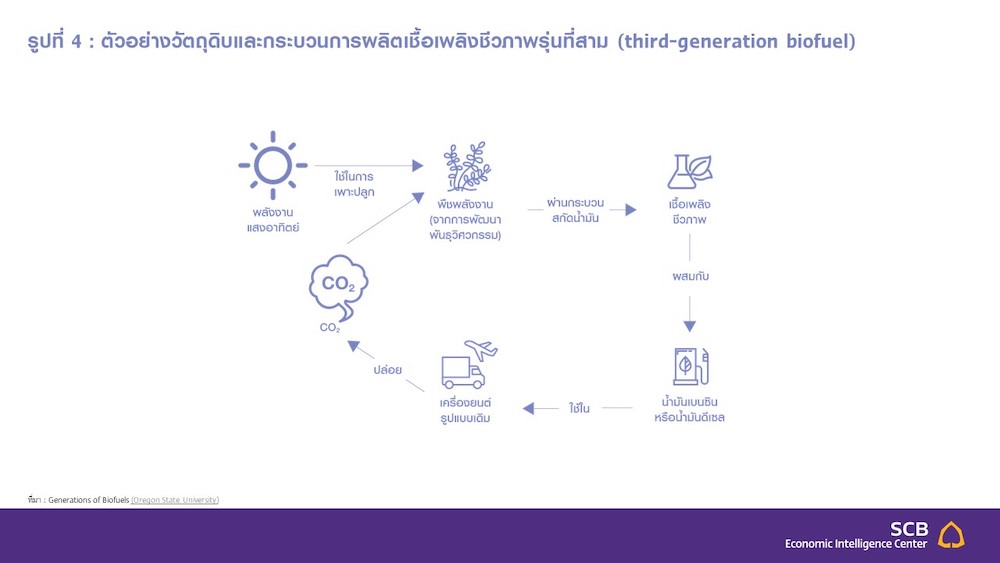

- Third-generation biofuels arise from concerns about land use and resource competition in the cultivation of second-generation biofuels, as they still involve waste materials from food or energy crops. This has led to the development of new energy crop raw materials like algae, which can be cultivated on less fertile land unsuitable for traditional crops, requiring less water and potentially using non-potable water such as saline or even industrial wastewater. Furthermore, algae cultivation can absorb carbon from the atmosphere. These raw materials rely on photosynthesis, ultimately yielding fats or oils that can be extracted and processed into biofuels. However, the development of raw materials for third-generation biofuels is still in experimental cultivation stages.

Figure 4: Examples of raw materials and production processes for third-generation biofuels

Source: Generations of Biofuels (Oregon State University)

Obstacles to price competitiveness

The price of advanced biofuels is one of the main challenges for the industry, as it remains high and cannot compete with other fuels. The industry is still in its early stages and has not achieved commercial maturity, for example, the price of SAF is 3-5 times higher than fossil aviation fuel, with fuel costs accounting for 20-30% of airline operating costs, making advanced biofuels uncompetitive. The price of biofuels results from high production costs, which affect the return on investment for advanced biofuel refineries and are a major limitation to industry development.

Drop-in properties are essential for Advanced Biofuels

Another challenge is developing biofuels with drop-in properties, making them comparable to fossil fuels to allow for higher blending ratios. Since conventional biofuels have different chemical compositions and physical properties from fossil fuels, such as higher viscosity and specific gravity and lower volatility, the combustion process in engines and ignition in combustion chambers may be incomplete, affecting performance and safety. This also limits the blending ratios of biofuels with fossil fuels, with maximum blending ratios for ethanol and biodiesel in existing infrastructure and engines being only 15% and 20%, respectively.

Therefore, to reduce the need for new infrastructure investment for biofuels, the biofuel industry focuses on developing drop-in properties that make biofuels comparable to fossil fuels and can be fully utilized in existing engines and infrastructure. This is evident in the aviation sector, which mandates that SAF must have drop-in properties equivalent to fossil aviation fuel in both chemical and physical terms, allowing for higher blending ratios without the need for new infrastructure and modifications to jet engines, which have strict performance and safety requirements.

Developing biofuels with drop-in properties presents several technical challenges. The first is reducing the oxygen content in biofuels, which can be as high as 10-45% depending on the raw material type, compared to crude oil, which has an oxygen content of less than 2%. The process of reducing oxygen in biofuels (deoxygenation) is still under development. The second challenge is the hydrogen-to-carbon ratio (effective hydrogen to carbon: H/C ratio), which is a key indicator of energy density. Biofuels typically have a lower H/C ratio than fossil fuels, necessitating the addition of hydrogen to achieve drop-in properties. The processes of deoxygenation and increasing the H/C ratio require hydrogen, which will increase the demand for hydrogen.

However, the current supply of hydrogen is limited due to primary demand for hydrogen in the refining industry, which produces hydrogen from fossil fuels for its own oil refining processes, and in the fertilizer industry, which uses hydrogen to produce ammonia. Therefore, a significant challenge for producing drop-in biofuels also includes the supply of hydrogen produced from clean energy (green hydrogen) that is low-cost and sufficient for biofuel production.

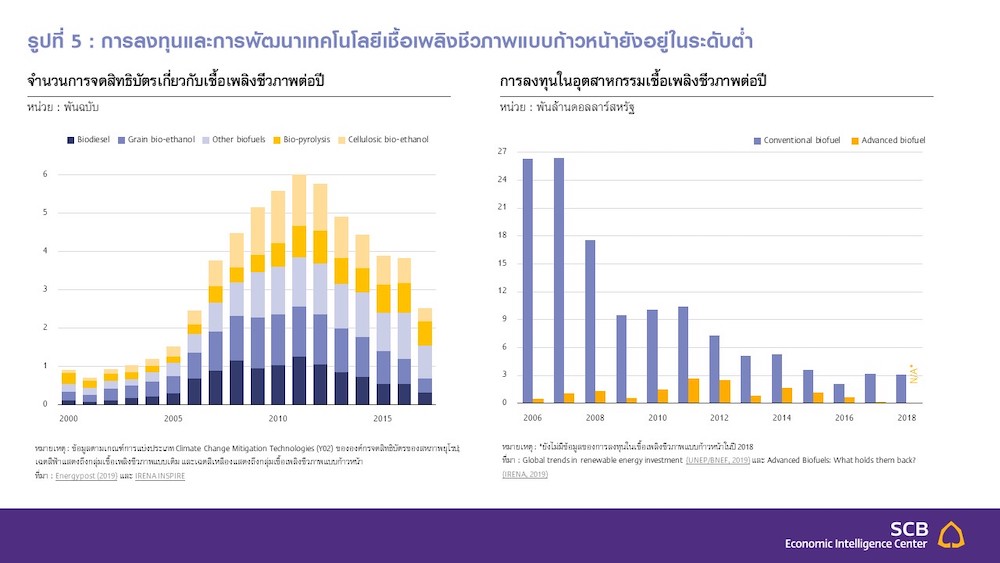

Thus, investment in the development of advanced biofuel technology is crucial, as the production process for advanced biofuels is a new technology still in its early stages and has not yet achieved technological breakthroughs, resulting in fuel quality and production costs that cannot replace fossil fuel use. However, the development of biofuel technology remains low compared to other clean technologies.

The number of patents related to biofuel technology has significantly decreased since 2011, during the oil price crisis, and the trend of newly filed patents aligns with the trend of investment in the biofuel industry, as the industry is perceived to be stagnant, especially compared to investments in other clean technologies such as solar, wind, and lithium-ion batteries.

Figure 5: Investment and technology development in advanced biofuels remains low

Nonetheless, the development of advanced biofuels is regaining attention due to their potential role and market demand, particularly in achieving net-zero goals, making it a significant opportunity for investment in research and development to advance biofuel technology, which will help strengthen and enhance the industry.

Opportunities for industry development in Thailand

Thailand has the opportunity to develop its biofuel industry into advanced biofuels by enhancing the existing biofuel industry's potential and fully leveraging raw material advantages. As mentioned, biofuels play a crucial role in reducing greenhouse gas emissions in the transportation sector, serving as transition fuels to clean energy and as options for vehicle groups that are challenging to reduce emissions, such as heavy-duty trucks and airplanes. This presents a great opportunity for Thailand to develop biofuels to meet the anticipated demand for global net-zero emissions targets.

The Thai agricultural sector has a wealth of diverse waste materials that can be used to produce advanced biofuels, particularly from key economic crops and those currently used as raw materials for ethanol and biodiesel production. There are abundant waste materials such as bagasse, cassava pulp, and palm fronds, which have insufficient market support, making it a good starting point for experimental production. Looking ahead, waste materials from other economic crops, such as corn stover or fruit scraps from processing plants, may also have potential for developing advanced biofuels. Additionally, producing advanced biofuels from various raw materials will help diversify risks and reduce over-reliance on any single raw material.

Furthermore, the demand for reducing greenhouse gas emissions and using advanced biofuels will provide an opportunity for Thailand to add value to the agricultural industry and integrate into a circular economy, strengthening and enhancing the efficiency of the supply chain for these key economic crops from cultivation, production, usage, to waste management.

The role of the government in promoting the development of Advanced Biofuels

The development of advanced biofuels requires government driving forces, which can help promote Thailand's knowledge and resources to become a leader in advanced biofuels by:

1. Establishing clear and consistent usage policies to create a market for advanced biofuels.

2. Creating pricing and market mechanisms that promote lower production costs for advanced biofuels to compete with fossil fuels.

3. Supporting an ecosystem that ensures sustainability throughout the value chain.

Blending Mandate

In the past, blending mandates have been a crucial factor in driving the market for advanced biofuels in the country. In the future, mandating blending ratios will help stimulate investment in technology and production capacity. The market and demand for advanced biofuels will be difficult to establish if the demand is uncertain, leading the private sector to hesitate to invest. Therefore, the blending mandate for advanced biofuels should align with technology development and industry readiness, considering the potential and efficiency of domestic technology in increasing production capacity and the amount of raw materials needed. Gradually increasing the blending mandate will create certainty in both demand and supply in the market.

For example, France has mandated that all flights departing from France must use at least 1% SAF of the total fuel used in aircraft by 2022, increasing to 2%, 5%, and 50% by 2025, 2030, and 2050, respectively. This has led Air France-KLM to collaborate with Total, ADP Group, and Airbus to research and develop SAF technology to meet government regulations.

Additionally, the government should continuously assess the impact of blending ratio adjustments on all sectors within the advanced biofuel ecosystem, studying problems and obstacles that arise and adjusting support policies to adapt to changes in the industry ecosystem and technology in the future.

BOX: Goals for Advanced Biofuel Usage Abroad

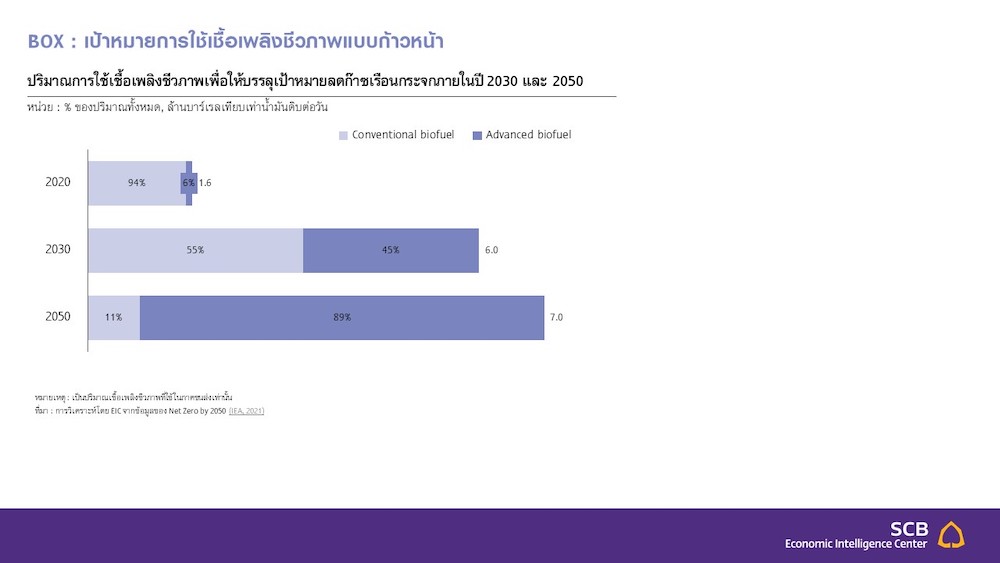

Countries worldwide aim to increase the use of sustainable biofuels, supporting technology development and stimulating biofuel use in various vehicles. The latest IEA report (2021) on net-zero greenhouse gas reduction goals by 2050 emphasizes that globally, the share of advanced biofuels in transportation must increase from about 6% of total biofuel use today to around 45% and 90% by 2030 and 2050, respectively, to achieve the set net-zero emissions targets during that period.

Volume of biofuel usage to achieve greenhouse gas reduction targets by 2030 and 2050

Unit: % of total volume, million barrels equivalent to crude oil per day

Note: This is the volume of biofuel used only in the transportation sector

Source: Analysis by EIC from data of Net Zero by 2050 (IEA, 2021)

Regionally, there have been goals to limit the use of conventional biofuels and increase the share of advanced biofuels, particularly through the latest Renewable Energy Directive (RED) II of the European Union, which limits the share of conventional biofuels for land transport to 7% and mandates the use of advanced biofuels at least 0.2%, 1%, and 3.5% in 2022, 2025, and 2030, respectively, of the total final fuel consumption in the transportation sector. In 2021, the European Union is also considering the draft ReFuel Aviation Initiative, mandating that all airlines from EU countries must use at least 2% SAF starting in 2025, increasing to a minimum of 5%, 32%, and 63% in 2030, 2040, and 2050, respectively.

At the national level, for example, France has capped the share of biofuels produced from food crops at a maximum of 7% of total oil consumption and has set blending ratios for advanced biofuels in gasoline and diesel at 3.8% and 2.8%, respectively, starting from 2028. The business sector has also set goals and plans for development, such as Shell's decision to invest in the advanced biofuel refinery project in the Netherlands, which will use agricultural waste, used vegetable oils, and animal fats, with sustainability certifications for cultivation and distribution, expected to be completed by 2024.

Creating market mechanisms that promote competition for Advanced Biofuels

The government should have mechanisms that reflect the environmental costs of various fuels to increase incentives for cleaner energy use. Currently, the prices of advanced biofuels remain higher than fossil fuel prices. However, the environmental costs of using fossil fuels have not been reflected in fuel prices.

Therefore, the government should create mechanisms that reflect the environmental costs of various fuels in line with global climate change policy directions, allowing fuel users to recognize price signals regarding the increased costs from environmental impacts caused by high-impact fuels compared to other options. This will encourage behavioral changes towards cleaner fuels. This can be achieved through increasing environmental taxes such as carbon taxes and gradually reducing subsidies for all types of fossil fuels.

For example, Sweden has a bioenergy share of about 20% of total fuel use in the transportation sector, which is higher than the European average, resulting from tax exemptions for bioenergy use and increased carbon and energy taxes on fossil fuels. Recently, the European Union is drafting the Energy Taxation Directive, considering the removal of tax exemptions for fossil fuels, particularly in aviation and shipping, to increase incentives for cleaner fuel use and is considering increasing tax rates on these greenhouse gas-emitting fuels.

Additionally, the pricing structure for advanced biofuels should be designed to incentivize producers to continuously improve production efficiency and reduce costs. In the early stages of promoting the industry and market for advanced biofuels, the government may help set the pricing structure to encourage investment. However, in the future, the pricing structure should be adjusted according to industry development and push producers to continuously reduce costs.

As the advanced biofuel industry begins to achieve commercial maturity, the government should allow prices to be determined by market mechanisms to promote competition with other fuels, which will encourage producers to accelerate their competitiveness in technology development and production processes to reduce production costs, improve fuel quality, and reduce greenhouse gas emissions (to lower environmental costs) to create a fully competitive market.

Accelerating the creation of a sustainable ecosystem throughout the value chain

The government should create an environment conducive to investment in the sustainable development and production of advanced biofuels. Sustainability should not only arise from production and use but must occur throughout the ecosystem. Thus, designing a roadmap to support advanced biofuels must consider and develop all related sectors simultaneously, from raw material sourcing, agriculture, biofuel production, transportation, automotive, waste management, to consumers, as all parties are interconnected. Policies in each sector within this ecosystem must also consider the impacts on the advanced biofuel policy plan and other related sectors.

Moreover, investing in new technologies carries high risks and requires significant capital investment, especially in technologies that efficiently convert raw materials into fuels and develop drop-in properties for advanced biofuels, which are still in early stages. Therefore, private sector investment is challenging. The government should help absorb risks and support investments to nurture this industry, creating an environment and support requirements conducive to trial and error to encourage attempts to innovate and ultimately lead to breakthrough innovations and new technologies.

Thailand has the potential to be a testing and development area for advanced biofuel production technology because it has agricultural advantages with suitable yields for large-scale biofuel production and a diverse range of agricultural products that can be further experimented with. Additionally, there is already a developing biofuel industry, along with market and infrastructure support for biofuel testing. Therefore, a clear policy direction and supportive ecosystem will attract both Thai and foreign investors to develop technology in Thailand, positioning Thailand as a potential regional hub for biofuel research and development.

Sustainable Aviation Fuel (SAF) presents an immediate opportunity through private sector collaboration.

In addition to government push, the commitment of private sector groups can also create a market. For instance, advanced aviation biofuels or SAF are viable options for the aviation sector, which has faced heavy criticism regarding greenhouse gas emissions, leading related businesses to have a shared goal of firmly reducing emissions, with SAF being the most feasible option for the aviation sector now and in the future.

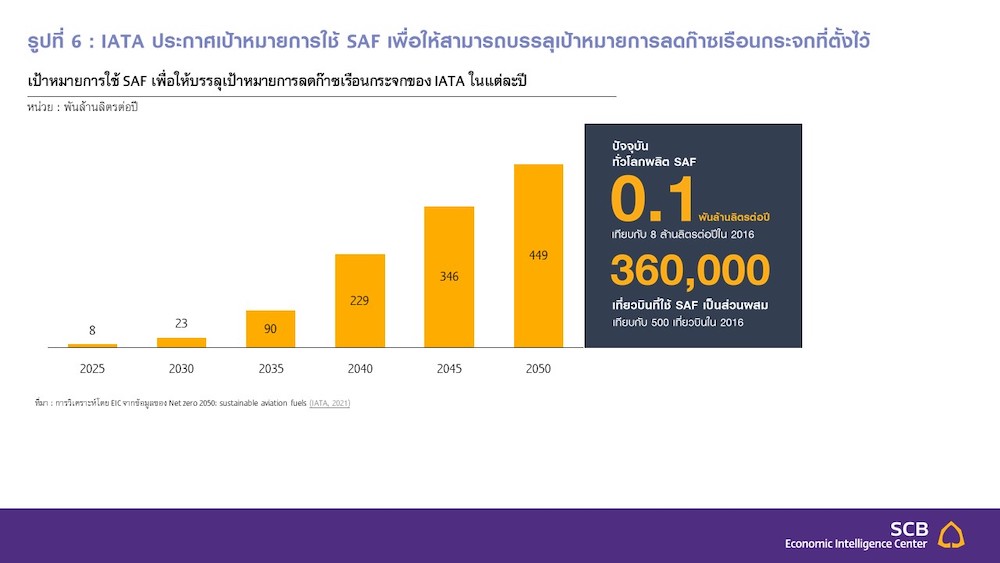

In October 2021, the International Air Transport Association (IATA) announced a goal to reduce greenhouse gas emissions by 2050, focusing primarily on using SAF. Currently, SAF production is only 100 million liters per year. To accelerate production and usage, IATA aims to increase SAF usage to 8 billion liters per year by 2025 and further to 230 billion and 450 billion liters per year by 2040 and 2050, respectively.

Figure 6: IATA announces SAF usage goals to achieve set greenhouse gas reduction targets

SAF usage goals to achieve IATA's greenhouse gas reduction targets each year, unit: billion liters per year

Source: Analysis by EIC from data of Net zero 2050: sustainable aviation fuels (IATA, 2021)

Using SAF may increase costs compared to fossil aviation fuel, but airlines can pass these costs onto consumers due to relatively inelastic demand for air travel compared to other travel types.

Thus, the aviation sector has the motivation to start using SAF and has begun to announce clear usage goals to increase the volume used, leading to reduced production costs and prices for SAF, resulting in increased private sector investment.

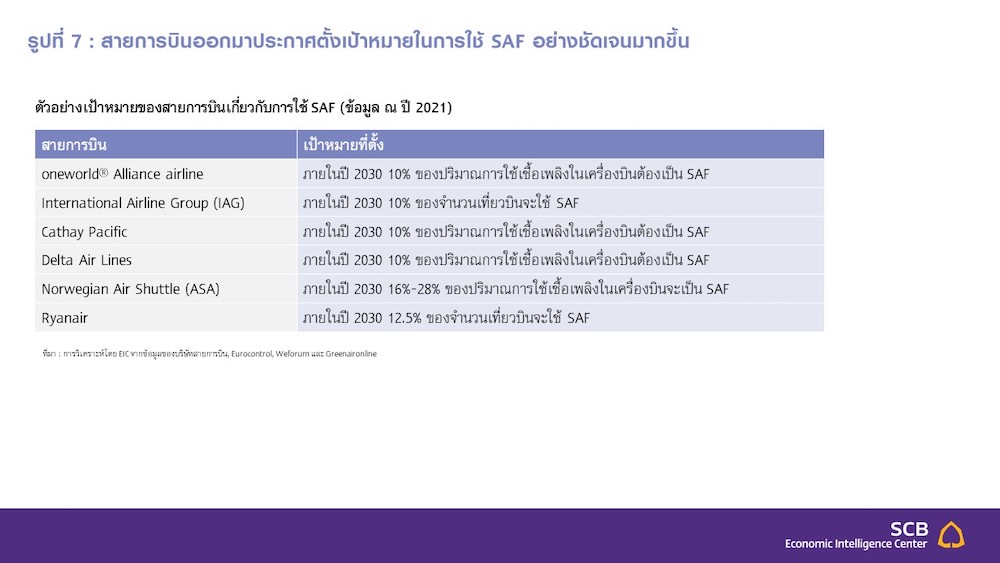

Figure 7: Airlines are increasingly announcing clear SAF usage goals

Examples of airlines' SAF usage goals (as of 2021)

For example, the International Airlines Group (IAG) aims to use SAF for 10% of its aircraft fuel by 2030 and plans to invest $400 million in SAF production development, intending to purchase at least 1.25 billion liters of SAF per year. The Airlines for America (A4A) group is collaborating to produce 13.6 billion liters of SAF by 2030, and All Nippon Airways (ANA) is jointly investing in SAF production technology development and providing funding to the New Energy and Industrial Technology Development Organization (NEDO), which successfully conducted the first domestic flight test using SAF blended with fossil aviation fuel in June 2021.

Additionally, businesses within the aviation ecosystem, such as Boeing, have announced plans to develop and produce aircraft capable of fully utilizing SAF by 2030. Airports are also responding to airlines' goals by starting to stock SAF, such as Heathrow Airport in the UK, which began testing SAF deliveries to airlines last June.

Moreover, other businesses involved in air transport, such as the Clean Skies for Tomorrow coalition, which includes various aviation-related businesses and others, are pushing for and supporting funding to develop technology to achieve SAF usage at 10% of global aviation fuel consumption by 2030.

Combined with mandatory measures from governments in some countries, this will create a more tangible SAF market and generate global demand, as airplanes need to refuel at airports other than their departure airports. Thailand has many international flights, with Suvarnabhumi Airport ranking as the 9th busiest airport in the world in 2019. If Thailand produces SAF, even without government measures, flights from airlines with set goals will create demand for SAF in Thailand as well. This demand is expected to grow alongside the aviation sector's desire to reduce greenhouse gas emissions.

Therefore, Thailand should fully leverage its existing opportunities and potential to produce SAF to meet the anticipated demand in the near future, whether in terms of agricultural waste raw materials, existing knowledge and technology regarding biofuels, or infrastructure such as oil refineries, storage facilities, and gas stations at airports. If Thailand can develop quickly and efficiently, it has the potential to become a leader in SAF technology and production in the region.

Advanced Biofuels will play a significant role in achieving greenhouse gas reduction targets in the transportation sector, particularly for heavy-duty trucks and airplanes, as they do not require new infrastructure and engine development, making them a crucial option for the transition to clean energy. However, the development of these fuels must ensure sustainability and environmental friendliness throughout the supply chain, from raw materials to production and use. For Thailand, accelerating the development of advanced biofuels presents a great opportunity, as there is already supporting infrastructure and a wealth of diverse raw materials for production, particularly agricultural waste, which can help enhance the existing biofuel industry and integrate into the circular economy. However, promoting the development of advanced biofuel industries faces technological challenges and requires significant investment. Collaborative goals from all stakeholders and government policy direction are key to industry development. Therefore, cooperation from all sectors should occur to ensure alignment and effective, sustainable development.

Analysis by… https://www.scbeic.com/th/detail/product/7989

Author of the analysis: Puthita Yamchinda ([email protected]), Analyst

Economic Intelligence Center (EIC)

Siam Commercial Bank Public Company Limited

EIC Online: www.scbeic.com

Line: @scbeic