e-Service Tax Impact on Users of Foreign Digital Platforms

Analysis from Kasikorn Research Center

The collection of value-added tax from foreign digital platform providers (VAT for Electronic Service: VES) is one form of taxation in the world of the digital economy (Taxation of the Digital Economy). Many countries have previously enacted laws to collect taxes from foreign digital platform providers in various forms, covering different digital business platforms. This tax collection aims to create fairness between Thai and foreign operators and help the government increase revenue. However, the necessity of relying on foreign digital platforms means that both business operators and consumers will ultimately be affected by cost and price transfers, which will vary according to the environment of each business.

• The e-Service tax collects value-added tax from foreign digital platform businesses providing services in Thailand, effective from September 1, 2021.

As Thailand enters the digital economy era, with technology playing an increasingly significant role in both business and daily life, numerous transactions—whether buying, making business contracts, or conducting financial transactions through digital platforms—are occurring both domestically and internationally. This trend is likely to replace traditional transactions, prompting authorities to find ways to assess taxes and design appropriate tax policies. Thailand has chosen to adopt a consumer tax model, which involves the collection of value-added tax (VAT).

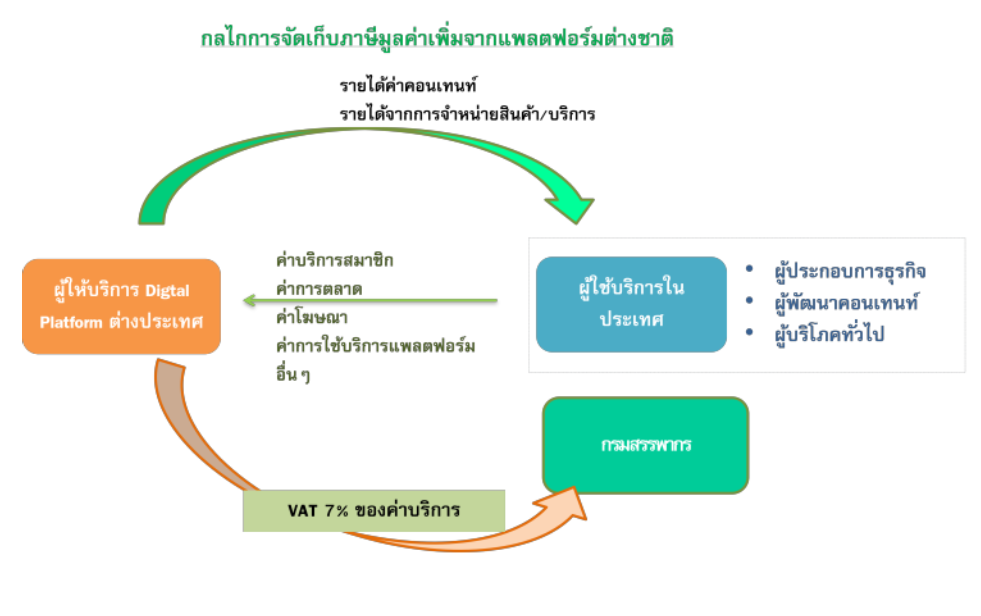

The Amendment to the Revenue Code Act (No. 53) B.E. 2564 (2021) (Collection of Value-Added Tax for Electronic Services from Abroad) came into effect on September 1, 2021. This law collects VAT from foreign digital platform providers offering services in Thailand that were previously not registered as VAT operators, with annual revenues of 1.8 million baht or more, at a VAT rate of 7% of the service price. Government estimates suggest that this tax collection will increase Thailand's revenue by no less than 5 billion baht in the fiscal year 2022, covering various activities, including:

1. Subscription-based platform providers, such as streaming media services (e.g., movies, music, or videos).

2. Online advertising platform providers.

3. Platform providers acting as intermediaries between buyers and sellers without their own applications, and P2P services, such as food delivery, online games, and various applications.

4. E-commerce platform providers, collecting VAT from income generated from using the platform for sales.

5. Agent service platforms, primarily in the tourism sector, where foreign digital platform providers must register for VAT, file monthly VAT returns, and remit VAT under a Pay-Only system (no input tax deduction) without needing to issue tax invoices or tax reports.

• In the next three years, or by 2024, the value of foreign digital platform services used by consumers in Thailand is expected to rise to 100 billion baht.

Currently, the costs associated with using various digital platforms include subscription fees, service fees, advertising costs on platforms, marketing costs, and service fees from product and service sales. These costs must be paid by domestic users to foreign digital platform providers. Kasikorn Research Center estimates that before the COVID-19 pandemic, the value generated from using foreign digital platforms in taxable activities was approximately over 70 billion baht, which foreign providers must assess to remit taxes to the Thai authorities.

The use of digital platforms in Thailand is expected to grow. Currently, various businesses must adapt to digital platforms as a means of selling and promoting products both domestically and internationally, especially during the COVID-19 pandemic, where businesses heavily relied on digital platforms. Additionally, consumer behavior has become accustomed to technology and the use of digital platforms, becoming part of the daily lives of certain groups, such as watching movies, listening to music, playing games, and purchasing various products and services, which have seen significant growth.

As the COVID-19 situation improves and economic activities return to normal, the use of services for tourism is expected to drive the value of using foreign digital platforms again after declining during the pandemic. Other activities are likely to continue growing but at a slower rate. Kasikorn Research Center estimates that by 2024, the value of using foreign digital platform services in these activities may reach 100 billion baht, with an average growth rate (CAGR) of about 10-15% per year.

• The complexity of the business context may prevent the automatic transfer of tax burdens from foreign digital platform providers to users.

The collection of VAT from foreign digital platform providers aims to create fairness in competition between Thai and foreign operators. However, from another perspective, tax collection will impact those within the business chain in different dimensions. Although it seems that the effects will primarily impact users more than foreign digital platform providers, as these providers are large global companies with significant market shares and high bargaining power, some providers still face challenges in generating profits. Additionally, the high competition in the technology sector requires providers to invest and develop new products to generate revenue, making it difficult to absorb costs. Therefore, it is possible that foreign digital platform providers may pass on costs to users.

However, Kasikorn Research Center believes that the issue of passing on tax costs to users is more complex than that. It is one option that foreign digital platform providers may consider, but overall, it is unlikely to occur automatically. This tax collection expands the scope to include players in the system that were previously outside the VAT collection mechanism, while the direction and business environment have different details. Therefore, each foreign platform provider in various businesses will need to assess all factors to find the best solution, including their role or bargaining power in the market, the growth rate of their products, how competition and pricing affect their customer base, and their planned business strategies moving forward. All these factors must be evaluated by foreign digital platform providers before making decisions; otherwise, they may lose profitability and competitiveness to other players, especially as technology advances and consumer behavior changes rapidly, which could significantly alter business trends from the present.

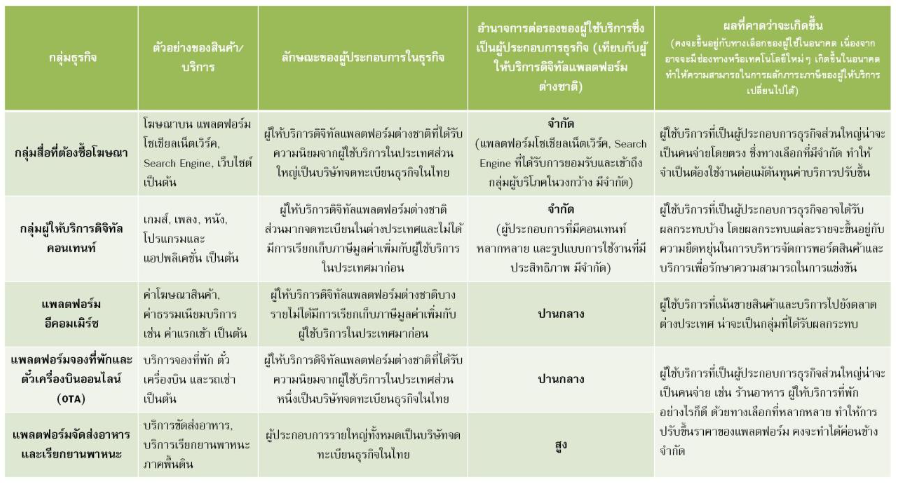

Nevertheless, considering the scope of the types of businesses involved within the current market and technology context, it can be preliminarily assessed that ultimately, users of foreign digital platforms, including business operators and consumers, may be affected both directly and indirectly in various forms. For example:

- Business operators using platforms as sales channels for products or services and promoting goods to target groups both domestically and internationally. Typically, users pay costs in the form of fees or marketing costs. In this case, digital platform providers may pass some burdens onto users through increased fees. Business operators with low margins and in highly competitive sectors may find it challenging to adjust prices and could be significantly affected if tax costs are passed on to users, such as those in the tourism, e-commerce, and entertainment sectors.

- Content developers may experience reduced income. This group includes developers of content such as videos, music, or films, and various applications that are sold or offered for free on platforms, earning revenue from advertising or view counts as determined by each platform. They may also be affected by changes in revenue-sharing rules or potential tax deductions in the future.

Example of e-Service Tax's Initial Impact on Users of Foreign Digital Platforms*

Note: * This is a preliminary assessment based on the current business and technology context. The impacts in various dimensions may change if technological advancements occur in the future, affecting consumer behavior and business operations.