Q2 GDP Recovers Significantly Due to Low Base Effects and Strong Export Growth

Analysis by Pimchad Ekachai, Krungthai COMPASS

Key Highlights

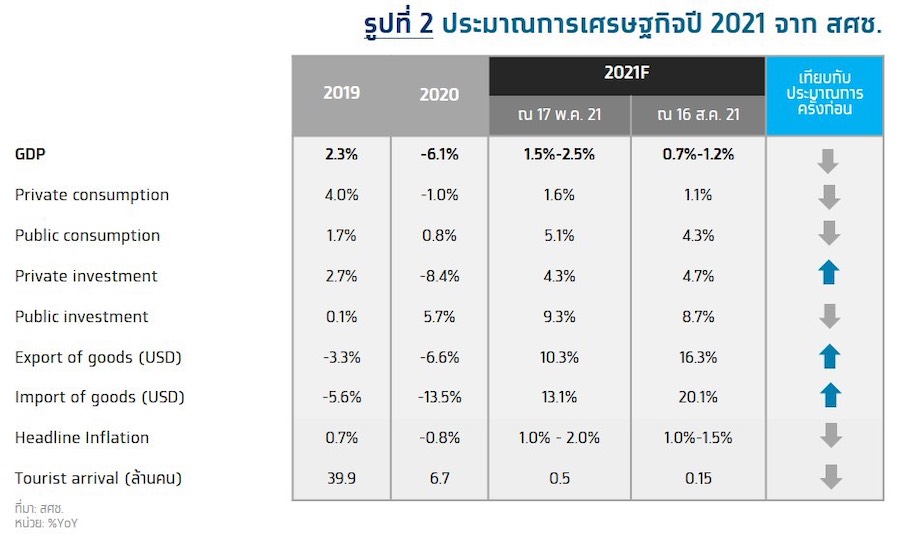

- The economy in Q2/2021 grew by 7.5% YoY or 0.4% QoQ sa, primarily due to the low base effect from the previous year and a strong recovery in exports aligned with global economic trends. However, the prolonged and severe pandemic situation has adversely affected private consumption and delayed the recovery of the tourism sector, leading the NESDC to revise its economic growth forecast for 2021 down to 0.7%-1.2%, from the previous estimate of 1.5%-2.5%.

- Krungthai COMPASS estimates that the Thai economy will grow by 0.5% in 2021, but there are significant downside risks due to semi-lockdown disease control measures that may extend for a longer period. This could lead to a contraction in the Thai economy in the second half of the year. For 2022, the economy is expected to grow by 3.9% as the pandemic situation gradually improves, allowing domestic demand to slowly recover, along with clearer plans for welcoming foreign tourists in the latter half of the year.

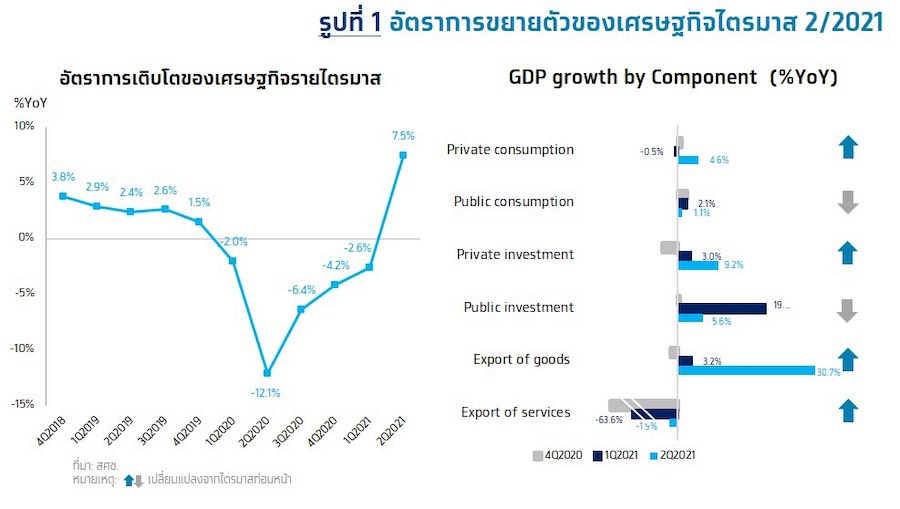

The National Economic and Social Development Council (NESDC) reported that the economic growth in Q2/2021 expanded by 7.5% YoY or 0.4% QoQ sa, with key expenditure components including:

- Private consumption grew by 4.6%, improving from a contraction of 0.3% in the previous quarter. The COVID-19 pandemic continues to significantly impact households, affecting employment and current income, as well as raising concerns about future income. However, there are some supportive factors from government programs aimed at reducing the cost of living and providing relief to those affected. In this quarter, spending on durable goods increased due to higher vehicle purchases, while spending on semi-durable goods continued to decline, and non-durable goods spending saw a slight slowdown in food, although non-food items experienced increased spending.

- Total investment grew by 8.1%, improving from 7.3% in the previous quarter, driven by a 9.2% increase in private sector investment due to the low base effect from the previous year, alongside investments in machinery, industry, and automotive sectors, as well as increased imports of capital goods. Meanwhile, public investment grew by 5.6%, slowing from the previous quarter due to a deceleration in public and state enterprise investments in construction and machinery, as well as a slowdown in investments in office equipment and computers due to reduced domestic sales.

- Exports of goods grew by 30.7%, improving from 3.2% in the previous quarter, driven by a strong recovery in the global economy and the low base effect from the previous year. This growth was primarily due to industrial exports, including vehicles, electronics, electrical appliances, metals, machinery, chemicals, petrochemical products, and petroleum products. Agricultural exports continued to grow, led by rubber and fruits, in response to rising global demand, while rice exports significantly declined compared to the previous quarter. Imports of goods grew by 32.2%, improving from 6.4% in the previous quarter, with all categories of imports expanding significantly, particularly private sector investments in machinery and tools, as well as raw materials driven by fuel imports.

- Service exports contracted by 1.9%, an improvement from a contraction of 63.6% in the previous quarter, due to increased revenues from freight services in line with a surge in international trade volumes, along with good growth in other business service revenues. However, revenues from tourism and passenger transport remained significantly low due to the limited number of foreign tourists allowed to enter the country.

For the entire year of 2021, the NESDC expects economic growth to be in the range of 0.7%-1.2%, down from the previous estimate of 1.5%-2.5%, due to the ongoing severity and prolonged nature of the pandemic affecting private consumption, particularly in the second and third quarters of the year, along with a slower-than-expected recovery in the tourism sector due to the persistent pandemic situation both domestically and in many countries, especially the risks posed by virus mutations.

Krungthai COMPASS estimates that the Thai economy will grow by 0.5% in 2021 amidst significant downside risks, while for 2022, it is expected to grow by 3.9%.

Krungthai COMPASS observes that private consumption weakened significantly in the second quarter and is likely to remain fragile in the future. Private consumption in Q2/2021 grew by 4.6% compared to the same period last year but contracted by 2.5% compared to the previous quarter. Despite ongoing and intensified support measures for living costs, such as the 'We Win' program and the 'M.33 We Love Each Other' initiative, which helped sustain some household purchasing power, it reflects that the prolonged pandemic since the beginning of Q2 has severely impacted the financial health of businesses and households, leading to higher debt levels and declining purchasing power due to concerns about future income, along with a highly vulnerable labor market, especially in the service sector.

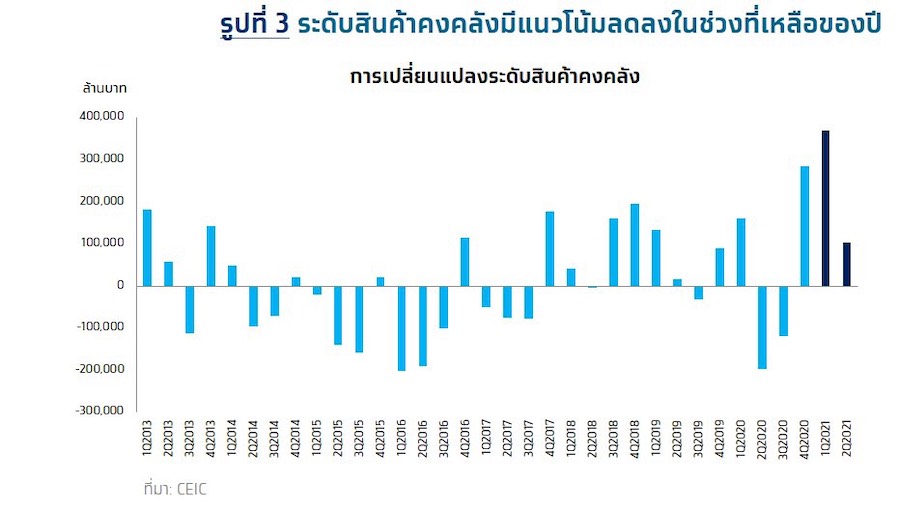

Inventory levels are expected to slow down as economic growth in this quarter is partly supported by an increase in inventory change of 103 billion baht compared to an increase of 369 billion baht in the previous quarter, driven by accumulation in industrial goods such as jewelry, gemstones, plastics, synthetic rubber, computers and peripherals, and vehicles. Currently, high inventory levels are expected to decrease in the second half of the year according to business cycles, while some production capacity is beginning to be affected by outbreaks in factory clusters, and the continued fragility of the Thai economy will also impact production support factors for the remainder of the year.

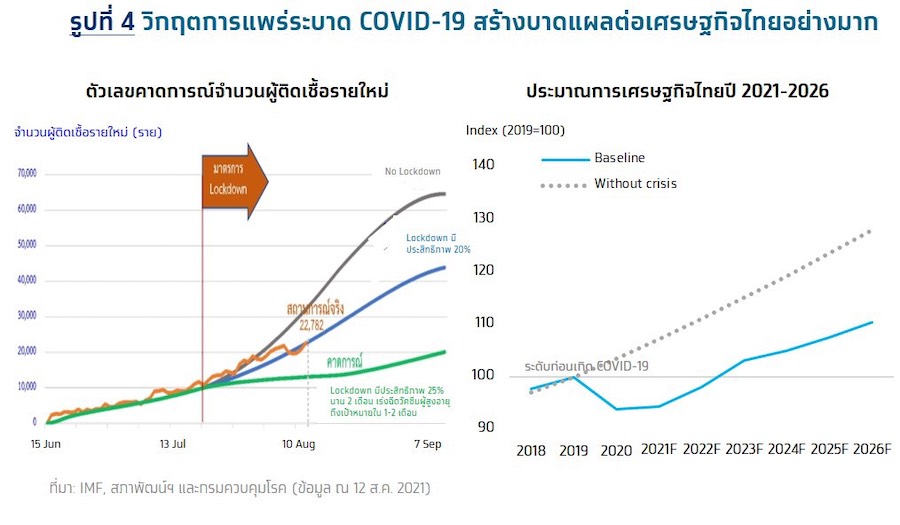

Krungthai COMPASS estimates that the Thai economy will grow by 0.5% in 2021, anticipating that semi-lockdown disease control measures may extend for at least two months (or until the end of September). The number of infections is expected to remain high throughout the rest of the year according to forecasts from the Disease Control Department (Figure 4: left), leading to risks of contraction in the Thai economy in the second half of the year. The Thai economy this year still faces significant downside risks due to the outbreak of the Delta variant, which spreads more rapidly than the original virus strain.

In contrast to the delayed implementation of disease control measures, the vaccination rate among the population remains very low, and there are limitations regarding the effectiveness of vaccines against variants, along with limited disease screening capabilities, leading to risks that the economy may face additional impacts from heightened disease control measures in terms of intensity, scope, and duration of enforcement.

The likelihood of the Bank of Thailand reducing the policy interest rate has increased, alongside additional measures to assist those affected, as the economy in the remainder of the year still faces significant downside risks.

For 2022, we expect the economy to grow by 3.9% as the pandemic situation is expected to improve in Q2/2022, amidst progress in accelerating vaccine distribution. Domestic demand is expected to gradually recover slowly, along with clearer plans for welcoming foreign tourists in the latter half of the year.

Implication:

Krungthai COMPASS estimates that the Thai economy may take at least another 2 years (by 2023) to return to pre-crisis levels. The Thai economy has been growing at a low rate since the global financial crisis in 2008, with an average growth of 4.8% before the crisis (1998-2008) before gradually slowing to an average of only 3.3% in the following 10 years (2008-2018). The COVID-19 crisis that the world is currently facing has caused the Thai economy to contract by 6.1% in 2020, and there is a risk that the Thai economy may continue to decline for a second consecutive year, leaving economic scars and impacting Thailand's productivity in the long term through three main issues:

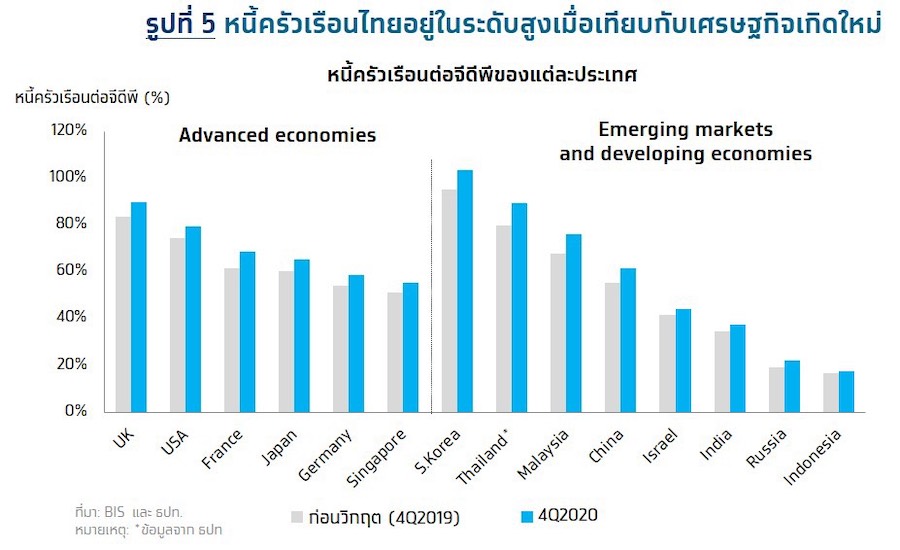

(1) High household debt pressures future spending and borrowing capacity. Thailand has faced household debt to GDP ratios exceeding 60% since 2011. According to a BIS study (2017), an increase of 1 percentage point in the household debt to GDP ratio results in a long-term economic growth reduction of 0.1 percentage points. If the household debt to GDP ratio exceeds 60%, it will increasingly negatively impact consumption. The COVID-19 crisis has contributed to an increase in household debt in Q1/2021 to 14.1 trillion baht, growing by 0.6% from the previous quarter, resulting in a household debt to GDP ratio rising to 90.5%, up from 89.4% in the previous quarter. This sustained high ratio will affect households' spending and borrowing capacity, increasing the risk of bad debts that could impact financial system stability and negatively affect the economy.

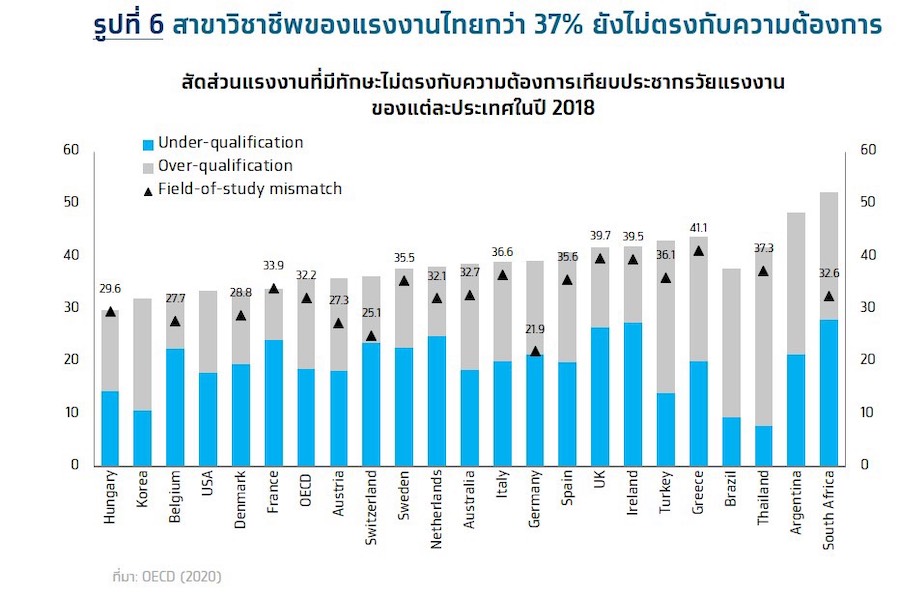

(2) The labor market has become increasingly vulnerable, as reflected in Q2/2021 data showing the first increase in the number of virtual unemployed in a year, along with a surge in long-term unemployment. A significant weakness in the Thai labor market is the "skill mismatch," particularly in fields that do not meet demand, with 37% compared to an OECD average of 32% (OECD, 2020). This will inevitably affect the readiness of the workforce to adapt to Thailand's 4.0 era. Additionally, the Thai labor market faces structural challenges, including one of the fastest declining working-age populations in the world and low labor productivity growth. A World Bank study (2021) indicates that the pandemic crisis has led to an average decline in labor productivity of 6% over a 5-year period. Therefore, COVID-19 is likely to worsen Thailand's productivity since the Asian financial crisis and contribute to potential output loss in the long term.

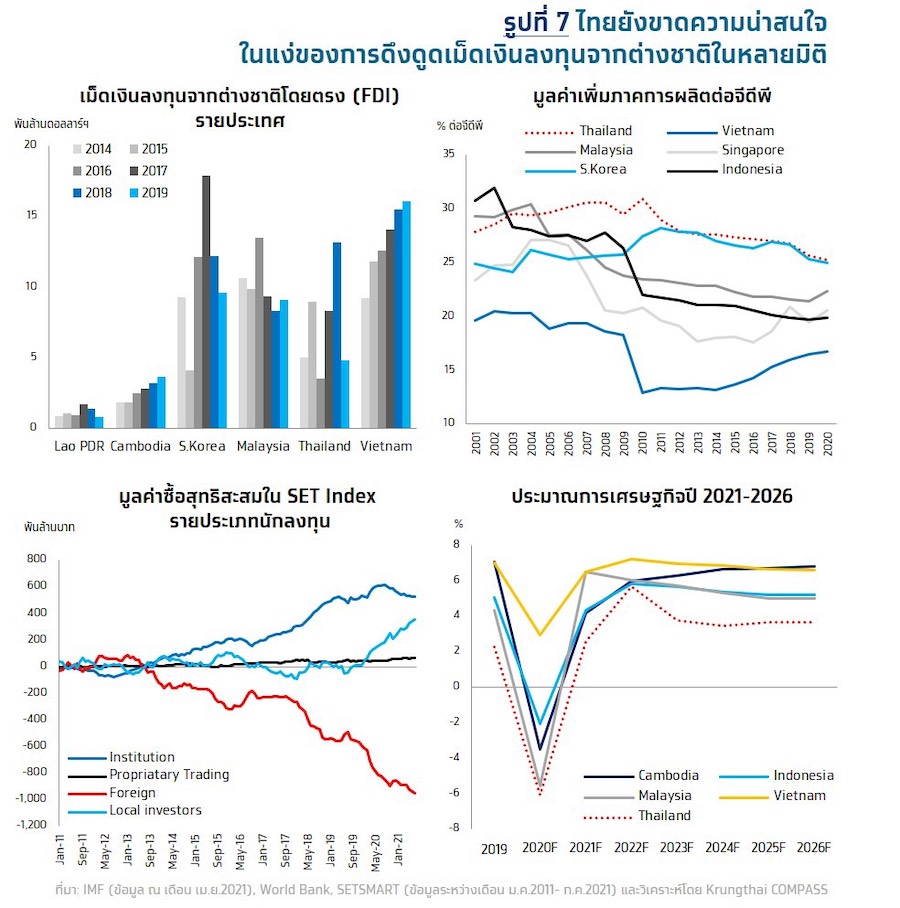

(3) Confidence and attractiveness for foreign investment remain critical issues. Although this year, the Thai economy has received support from a well-performing export sector, structural production factors mean that Thailand primarily serves as an OEM, with most products being mid-level technology items such as electrical appliances and automotive parts benefiting from Japanese investment.

This has led to a continuous decline in value-added production to GDP since 2010, in contrast to competitors that have improved. While Thailand is a major global Hard Disk Drive production base, it faces high risks of being replaced by new technologies such as Solid State Drives, with some production bases relocating to Malaysia, and semiconductors that are in high demand globally, primarily produced in Taiwan. Furthermore, although Thailand has recently focused on promoting investment in key industries that create added value for the economy, such as S-curve and New S-curve industries, the incentive of reducing income tax rates for foreign investors is a measure that all ASEAN competitor countries employ, making Thailand's long-term attractiveness to foreign investors a topic for consideration.