Borrowing Money for Real Estate Development Investment

When it comes to borrowing money, many people may feel a sense of financial risk, uncertainty, interest payments, and the potential for trouble. If the purpose of borrowing is for daily living expenses, these concerns are valid. However, if the borrowing is intended for investment, whether for real estate development or other business ventures, it may be necessary to consider borrowing from a different perspective.

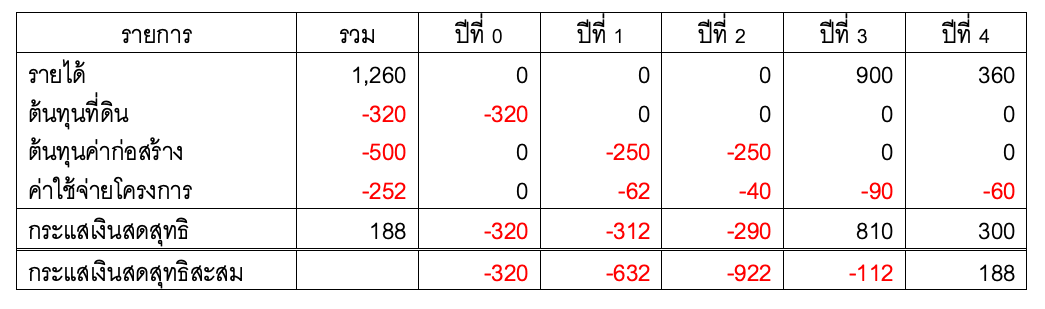

For instance, if Innovative Real Estate Development Co., Ltd. intends to invest in developing a residential condominium for sale, the main investment costs would include land costs, construction costs, design fees, and project expenses, which consist of marketing costs, sales expenses, costs for transferring units to customers, as well as various taxes, as shown in Table 1.

Table 1: Estimated Cash Flow of the Project Without Borrowing (Unit: Million Baht)

From the table, it can be seen that the company uses a maximum investment of approximately 922 million baht, resulting in a profit of about 188 million baht at the end of the project, which translates to an ROE (Return on Equity) of approximately 20.39%.

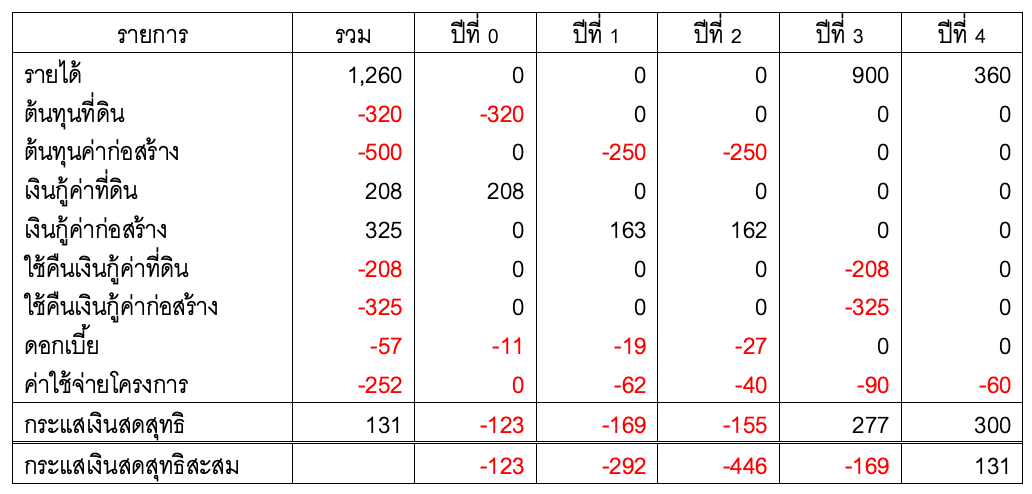

Furthermore, considering the scenario where the company also uses borrowed funds for operations, with the initial borrowing assumption being 65% of the land and construction costs at an interest rate of 5% per year, this would affect the estimated cash flow of the project. The profit at the end of the project would decrease to about 131 million baht due to an additional interest payment of 57 million baht. However, it can be observed that the company would only need a maximum investment of approximately 446 million baht (as seen from the accumulated net cash flow), which, when calculating ROE (Return on Equity), would increase to approximately 29.37%, as shown in Table 2.

Table 2: Estimated Cash Flow of the Project With Borrowing (Unit: Million Baht)

In addition to the increased ROE, it can be seen that borrowing according to the above assumptions would reduce the maximum investment by more than half compared to the scenario without borrowing. In other words, the company could undertake two projects simultaneously while using a maximum investment close to that of operating a single project without borrowing. If we take the figures from Table 2 and calculate, we find that when operating two projects simultaneously, the maximum investment would be approximately 892 million baht, resulting in a profit of 262 million baht after project completion, which is greater than the profit from operating a single project without borrowing, which is approximately 188 million baht, while using a similar amount of owner’s equity.

Various financial indicators that would improve as a result of borrowing include IRR (Internal Rate of Return) and NPV (Net Present Value), among others, due to the slower cash outflow from the business. However, for more in-depth details, interested parties can further study general finance textbooks or in the course on the feasibility study of real estate projects in the Master of Science in Real Estate Development Innovation program at the Faculty of Architecture and Planning, Thammasat University, which also discusses these details.