Why Should the 'Central Bank' 'Lower Interest Rates' Again?

The Thai economy is still facing three factors: the second wave of the outbreak, another economic slowdown due to weak demand, and domestic political factors affecting investment confidence. The decision now lies with the central bank on whether to lower the policy interest rate.

The recently announced GDP growth figures for Thailand in the second quarter were quite in line with many predictions. It was reported that the Thai economy experienced a negative GDP growth of 12.2% in the last quarter, with exports also down by 10%, leading to a significant contraction in GDP. Total investment in the previous quarter decreased by 8%, and private consumption fell by 6.6%.

For the first half of the year, the Thai economy showed a negative growth of 6.9%, with total consumption down by 7.2% and total investment down by 10.2%. Meanwhile, public investment increased by 1.2%, and exports in the first half decreased by 17.8%.

Additionally, the National Economic and Social Development Board has revised its economic forecast for this year downwards, expecting a contraction of between 7.8% and -7.3%, with a median estimate of 7.5%. Consumption is expected to decrease by 3.1%, and investment is projected to drop by 2.1%, while exports are anticipated to decline by 20%. This overall picture is quite similar to what I had previously estimated during a seminar held by the Association of Investment Analysts/The Stock Exchange of Thailand nearly four months ago.

Looking ahead to the second half of this year, I see three key factors affecting the Thai economy: first, the second wave of COVID-19; second, another economic slowdown due to weak demand, as government relief measures for COVID-19 are nearing their end while unemployment continues to rise; and third, domestic political factors that will impact confidence and slow down investment.

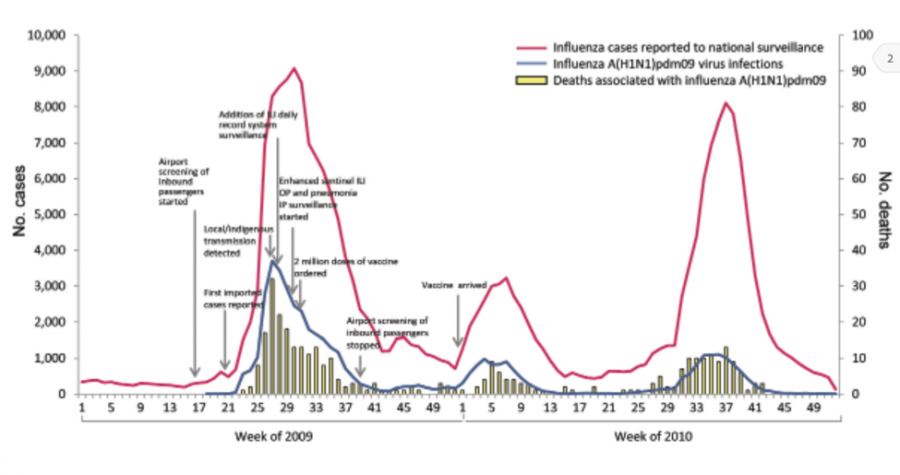

Figure 1: Number of infections and deaths in Thailand during the Swine Flu outbreak in 2009

Starting with the factor of the second wave of COVID-19, although our country has been free of domestic infections for over a month now, if we consider the Swine Flu outbreak in 2009, we find that the interval between the first and second waves was about 30 weeks, as shown in Figure 1, with the severity of the second wave being about half that of the first.

Moreover, New Zealand, known for its effective COVID-19 management, has recently reported double-digit COVID-19 cases after over a hundred days without any infections. Thus, we cannot rule out the possibility of a second wave of COVID-19 occurring in our country, especially considering the potential for outbreaks in neighboring countries that could further reduce cross-border trade.

Second, there is the risk of another economic slowdown due to weak demand, as government relief measures for COVID-19 are nearing their end while unemployment continues to rise. The private sector, particularly in the service sector that relies on foreign customers, is still unable to operate fully, leading to what is referred to as a Greater Recession.

This issue is relatively new in the field of economics, as past crises in our generation have never seen such a phenomenon, making it difficult to assess the extent of the decline in demand affecting GDP. However, it is anticipated that the decline will not be less than 1-1.5% of GDP.

Lastly, the protests by the younger generation calling for democracy, which is a trend seen in various countries worldwide, also impact confidence and slow down investment. This social phenomenon is new in our country, and while I believe it may not be as severe as the situation in Hong Kong last year, it still affects the investment atmosphere and confidence, particularly regarding long-term political stability, which will gradually impact the economy if the parties involved do not engage in constructive dialogue soon.

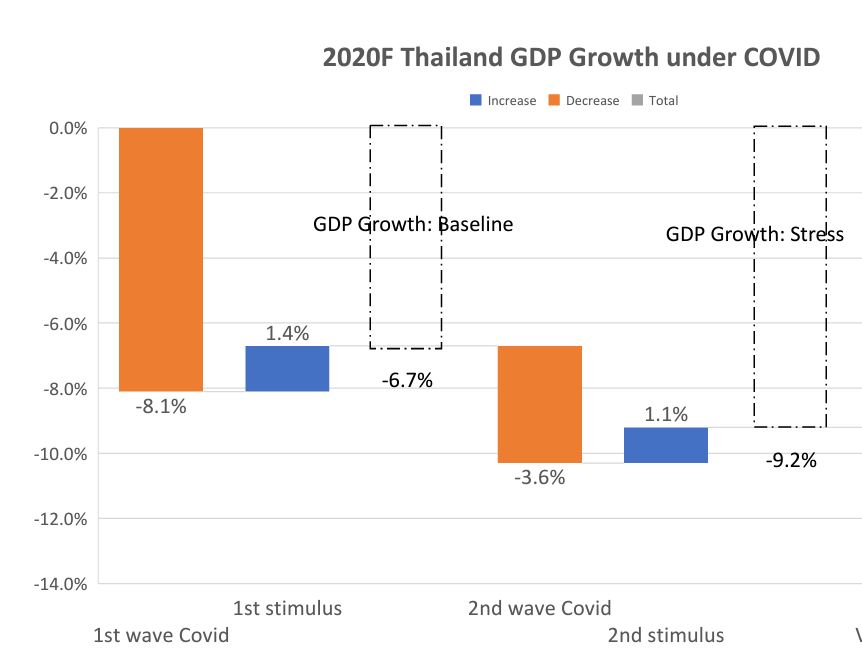

Figure 2: Projected GDP growth rate for Thailand if the policy interest rate does not decrease from now

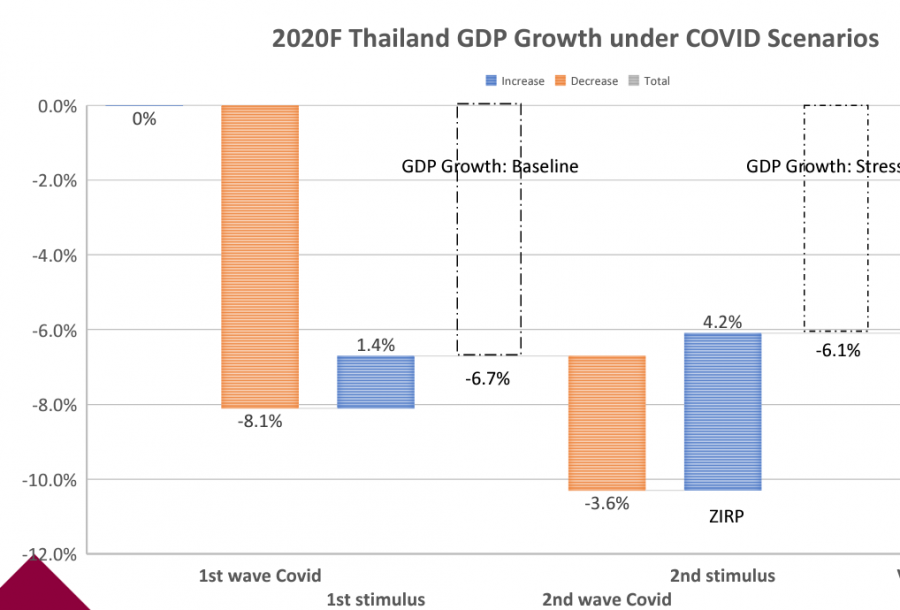

Figure 3: Projected GDP growth rate for Thailand if the policy interest rate is lowered 1-2 times from now

This leads me to believe that the three risk factors mentioned above for the Thai economy in the second half of this year represent another significant hurdle that will lead to further economic contraction in Thailand. From Figures 2 and 3, it can be seen that the GDP growth rate for Thailand could drop to -9.2%, which is close to the National Economic and Social Development Board's forecast of -7%. The decision now rests with the Bank of Thailand on whether to lower the policy interest rate to between 0-0.25%.

The reason is that studies on fiscal policy have found that the fiscal multiplier under a zero lower bound interest rate environment is four times larger than in an environment where the interest rate is above zero.

As shown in Figures 2 and 3, if the government implements an economic stimulus package that is half the size of the first stimulus package, it is projected that if the central bank maintains the current interest rate, Thailand's GDP will grow at -9.2%, while if the policy interest rate is lowered, GDP growth is expected to be -6.1%.

This is because if interest rates are lowered, the public will perceive that the government's debt burden from borrowing or issuing bonds will significantly decrease, eliminating the need to raise taxes in the future. This will encourage consumers to spend more, positively impacting the growth of the Thai economy.

Of course, lowering the policy interest rate to near zero will reduce returns for retirees' savings and pose additional risks to financial stability due to the search for yield phenomenon. However, the uncertainty of the economic risk factors today may outweigh the benefits of maintaining interest rates to avoid the negative impacts of a zero interest rate policy.

SOURCE: www.bangkokbiznews.com