Opportunities and Challenges for ASEAN Amid Supply Chain Changes in the Post-Covid-19 Era

The Covid-19 pandemic has impacted countries that rely on importing intermediate goods from China due to China's production halts and shipping disruptions. Meanwhile, Japan, another key player in the global supply chain, is facing a second wave of outbreaks that poses risks to the production of essential intermediate goods. This situation highlights the vulnerability of relying on concentrated sources of essential goods production. At the same time, the outbreak occurs at a crucial moment when businesses are reassessing their decisions to relocate production bases, amid pressures from an ongoing trade war that could lead to significant shifts in production chains, particularly reducing reliance on imports from China by many countries. The Kasikorn Research Center has compiled issues regarding the dependence on intermediate goods in ASEAN countries, as well as implications from the future adaptation of the supply chain, which are interesting as follows:

Source: UNCOMTRADE, Center for International Development at Harvard University

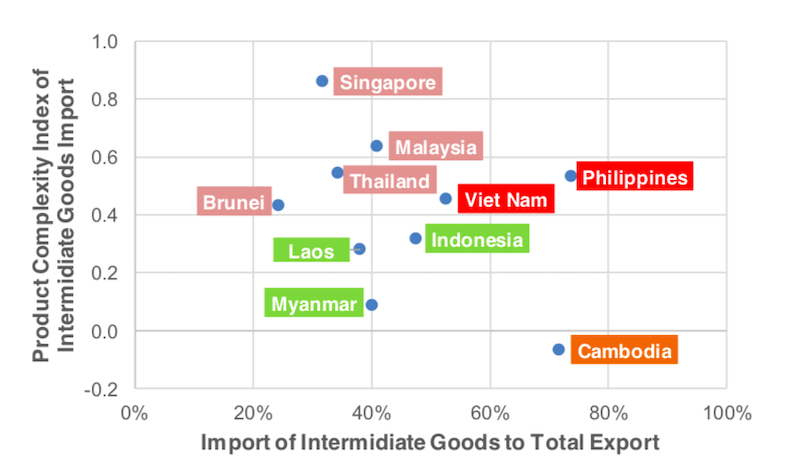

In analyzing the vulnerability of dependence on imported intermediate goods from abroad, in addition to the level of concentration of dependence on these imports, the complexity level of the intermediate goods (Product Complexity Index: PCI[1]) is another factor affecting vulnerability. This is because reliance on intermediate goods with high complexity may indicate difficulties in shifting dependence to other producers. ASEAN countries can be categorized based on the complexity of intermediate goods and the concentration level of imports as follows:

- Countries with low complexity in intermediate goods imports - This category primarily includes raw materials related to textiles, steel, and basic chemicals. Imports in this category are often sourced directly from producing countries, with China being the main source, except for chemicals, which see a mix of imports from China and ASEAN. However, this group can be further divided into two subcategories:

- Countries with low complexity in intermediate goods imports and relatively low dependence on these imports - Countries in this group are generally characterized by relatively closed economies, such as Laos, Myanmar, and Indonesia, focusing on importing intermediate raw materials for domestic consumption. Most imports in this category are related to textiles and steel, except for Indonesia, which imports more industrial goods like chemicals.

- Countries with low complexity in intermediate goods imports but high dependence on these imports - Cambodia is the most at risk of supply chain disruptions due to its export sector.

- It lacks diversification and heavily relies on importing intermediate raw materials for the textile industry from China.

- Countries with high complexity in intermediate goods imports - Most imports in this technology category are electronic goods that often use highly complex intermediate components. Key sources of these imports include South Korea, China, and Japan, with a notable observation that most complex intermediate components come primarily from South Korea, while China produces less complex intermediate goods. In the automotive sector, there is a significant reliance on intermediate goods imports from Japan.

- Countries with high complexity in intermediate goods imports but relatively low dependence on these imports - Malaysia, Singapore, and Thailand fall into this category. The supply chain connections are extended, as less complex intermediate goods are produced through ASEAN and China, which rely on imports from South Korea and Japan, who hold significant technology for producing intermediate goods for export to reduce production costs. However, most complex intermediate goods still depend on East Asian countries, particularly South Korea and Japan.

- Countries with high dependence on intermediate goods exports and high dependence on intermediate goods imports - The Philippines and Vietnam are at high risk of supply chain disruptions due to their reliance on complex intermediate goods imports, especially those from South Korea, which are technology products that may be difficult for other producers to substitute.

Overall, it can be concluded that most ASEAN countries may face vulnerabilities in their supply chains due to reliance on importing intermediate goods from cost-advantaged sources like China, as well as dependence on technology from upstream countries that own advanced technologies, such as South Korea and Japan, indicating risk factors for supply chain disruptions. While ASEAN can produce intermediate goods of medium complexity, it must be acknowledged that the production of these intermediate goods still relies on direct imports from upstream producers who own advanced technologies, meaning that risk diversification in the supply chain from reliance on regional intermediate goods producers may be quite limited.

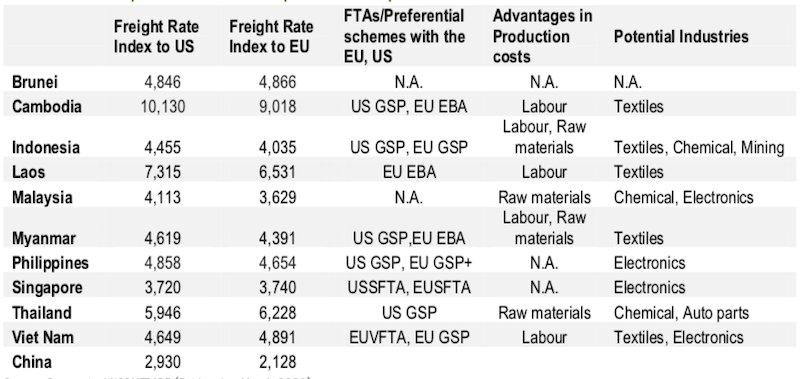

Looking ahead, the Covid-19 outbreak has severely impacted large countries that are end markets for industrial goods, reinforcing the vulnerability of supply chains that depend on concentrated sources of intermediate goods production. Coupled with pressures from U.S. trade tariffs, this may accelerate considerations to shift important production bases away from China. When comparing ASEAN and China, ASEAN's advantages lie in the trade privileges many countries receive from both the U.S. and the European Union, as well as lower labor costs in several countries compared to China, which could help mitigate some disadvantages related to transportation costs. The Kasikorn Research Center has compiled interesting points regarding the shift of the supply chain from China to ASEAN as follows:

- Protected goods (Safeguard) and labor-intensive production may be worthwhile for relocating production bases away from China. Cambodia, Myanmar, and Laos may benefit from attracting investments in these goods due to lower labor costs than China, as well as trade privileges that can offset potentially higher transportation costs from relocating production bases. For example, in this group, the textile and garment industry has seen production shifts away from China while still relying on the advantages of nearby production sources (Nearshoring) since the production of these goods still requires upstream raw materials from China, which retains production advantages.

- Final goods from China that have profit potential and do not rely on labor-intensive production may see limited relocation as China still holds advantages in production costs and transportation costs. Goods in this category are primarily capital-intensive, such as the steel industry, where China maintains production advantages.

- For goods that impact supply chain security or high-tech products with intellectual property risks, relocation is likely to be a reshoring back to destination countries that own the technology to diversify risks, especially for products that can utilize robots and machinery for production, as well as products sensitive to disruptions in the supply chain of critical goods. Products likely to be brought back for production in destination countries that own technology include upstream goods in the electronics industry that use advanced technology, such as semiconductors, as well as industrial products that utilize advanced technology in production, such as alloys and composite materials.

- For goods that do not require high levels of production technology, ASEAN may benefit from partial relocation of production. It must be acknowledged that the production capabilities of ASEAN countries are somewhat limited by the knowledge required to produce complex goods and still rely on production technology, as well as intermediate goods from abroad, making it possible to replace Chinese goods only in certain parts of the supply chain, particularly in the production of final goods. The forms of relocating production from China can be divided into two subtypes:

- Relocating production from China to market in ASEAN - This shift may come from Chinese companies seeking production sources with lower production costs than in China, as well as seeking new markets to replace those affected by the trade war. Examples of goods in this category may include electrical appliances that do not rely on high-level production technology, low-complexity automotive parts, and utilizing local raw material sources to reduce production costs, such as tires. Additionally, production relocation may stem from factors related to the destination country's industrial protection policies, such as the steel industry, where Chinese steel producers have distributed production bases to Indonesia to expand production and take advantage of lower energy and mineral resource costs than in China.

- Relocating production from China to produce goods for export to major markets outside ASEAN - In this case, companies relocating production will consider the benefits from trade agreements that grant tax privileges to production sources in ASEAN, in addition to production cost factors, or as a means of diversifying production bases to reduce reliance on a single production base in China. The level of technology and complexity of products in this group will be higher than those in the first group and may rely on technology or imports of intermediate goods from upstream producers. Relocation in this group may involve expanding the existing production bases of multinational companies that have investments in both ASEAN and China to avoid the impacts of trade tariffs, seeking supply chain security, and finding production sources with lower costs to gain advantages over products where Chinese companies are competitors. Examples of such products may include the production of final electronic goods, such as electrical appliances and portable electronic devices, medium-complexity automotive parts, and the production of relatively simple medical devices.

Comparing logistics costs and strengths of production costs for export between ASEAN and China

Source: Cargorouter, UNCOMTRADE (Retrieved on May 4, 2020)

In summary, while ASEAN, as one of the important production sources in the world, has the potential to attract the relocation of production bases from China, the changes in the supply chain involve many factors, including considerations for reshoring to reduce risks from supply chain disruptions, production cost factors, and access to end markets, which continue to weigh on decisions to shift production chains away from China. When considering the production potential of ASEAN countries, it is evident that ASEAN can produce a variety of final goods to replace those from China, relying on imports of intermediate goods from China or countries that own technology, while the production of intermediate goods that depend on upstream goods from the region may only be feasible for certain categories of goods, indicating that the dependence on intermediate goods may not change significantly.