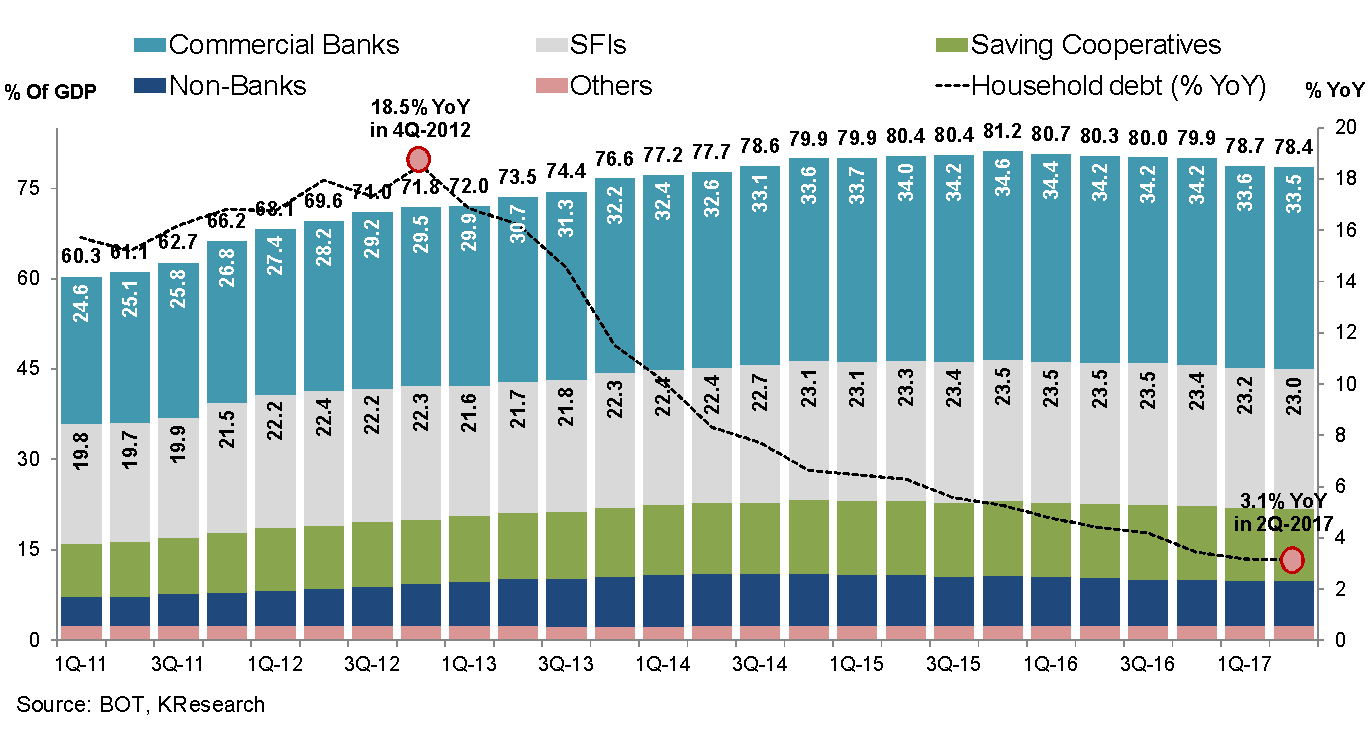

Thai Household Debt Slows to 78.4% of GDP in Q2/2017 Reflecting Caution from Both Financial Institutions and Consumers

According to the latest household loan figures from the Bank of Thailand, the ratio of household debt to GDP continues to show a downward trend over the past six quarters, standing at 78.4% in Q2/2017, down from 78.7% in Q1/2017. Although the outstanding household debt in Q2/2017 increased to 11.603 trillion baht, reflecting a 3.1% YoY rise compared to the same period last year, this growth rate has slowed from 3.2% YoY in the previous quarter. The Kasikorn Research Center has compiled interesting points from the latest household debt data as follows:

- The outstanding household debt in Q2/2017 increased by approximately 106.788 billion baht from the previous quarter, reaching 11.603 trillion baht, up from 11.496 trillion baht in Q1/2017. This increase is partly due to seasonal factors, as household debt typically rises in Q2 more than in Q1, when repayments are more common, resulting in less significant increases in household debt. Additionally, it is noteworthy that the increase in household debt is primarily attributed to housing and car loans (from both commercial banks and specialized financial institutions), which likely belong to households with purchasing power. This aligns with the high growth in property transfers in Bangkok and its vicinity, as well as domestic car sales.

- Despite the high and continuously increasing household debt situation, the growth rate has been consistently slowing down. The outstanding household liabilities increased by 3.1% YoY in Q2/2017, down from 3.2% YoY in Q1/2017, and lower than the average quarterly growth of about 4% YoY in 2016.

Upon closer examination, it is found that the burden of debt for consumption, as reflected through credit card loans and personal loans, expanded at a slowing rate of 6.1% YoY and 4.1% YoY in Q2/2017 (down from 8.9% YoY and 4.4% YoY in Q1/2017, respectively). Similarly, housing loans also slowed down due to the high comparative base from the same period last year, which was influenced by market stimulus measures. Meanwhile, the increase in car leasing loans (especially from commercial banks) corresponds with the recovery period of the domestic car market.

In summary, the Kasikorn Research Center views the continuously slowing growth of household debt as a reflection of caution from both sides. On the financial institution side, both commercial banks and non-bank financial institutions remain cautious in extending retail loans, including housing loans, credit card loans, and personal loans, to manage credit quality issues. On the household side, there is likely a slowdown in debt accumulation due to already high debt burdens.

Furthermore, the increase in household debt at a rate lower than GDP has led to a continuous decline in the household debt-to-GDP ratio in Thailand, which now stands at 78.4% in Q2/2017 (the lowest in three years). Meanwhile, the ongoing signals of economic expansion in the near future suggest that the Kasikorn Research Center estimates that household debt in Thailand in 2017 may slow down to near the lower end of the projected range of 78.0-79.0% of GDP. However, it must be acknowledged that while the household debt-to-GDP ratio in 2017 may decrease from 2016, the debt burden relative to income remains high, indicating that purchasing power and the atmosphere for private sector spending may have limited recovery potential. Additionally, maintaining discipline in debt accumulation remains crucial for reducing financial vulnerability for households and the overall Thai economy.

Household Debt and Household Debt-to-GDP Ratio

Thank you for the information from www.kasikornresearch.com