Bangkok Condominium Market in the First Half of 2026: Limited New Supply While High-End Demand Remains Strong

Savills (Thailand) reports that the overall Bangkok condominium market in the first half of 2026 is still in a phase of market rebalancing. Developers are exercising caution in their investments, resulting in limited new supply concentrated among major developers. Meanwhile, medium and small developers are prioritizing liquidity management and clearing existing inventory over launching new projects.

In terms of demand, the market shows clear differences across segments. Luxury condominiums in the central business district continue to absorb market supply at a satisfactory level, reflecting stable purchasing demand among high-income buyers. In contrast, the middle to lower market segments face pressure from limited purchasing power recovery and strict credit approval processes, leading operators to adopt competitive pricing strategies to boost sales.

Savills (Thailand) anticipates that in the second half of 2026, market recovery will proceed gradually, with growth concentrated in projects with strong location potential, product differentiation, and pricing aligned with purchasing power. This indicates that the ability to develop projects in line with market demand will be a crucial factor determining the success of developers in a challenging market environment.

Savills (Thailand) found that the overall condominium market in Bangkok at the end of Q2 2026 remains cautious, with developers hesitant to launch new projects due to pressures from still-recovering purchasing power, strict housing loan approval conditions, and high development costs. In the past quarter, only 5 new condominium projects were launched, totaling 2,260 units, with a total development value of approximately 15.6 billion baht. All projects were investments from two major publicly listed real estate developers, Sansiri Public Company Limited and AP (Thailand) Public Company Limited, with no new projects launched by medium and small developers during this period. This reflects that smaller developers are still delaying investments and focusing on liquidity management and inventory clearance rather than expanding new projects.

In the first half of 2026, a total of 15 new condominium projects were launched, comprising 12,248 units, representing a 72.52% increase compared to the same period last year (Year-on-Year: YoY). However, this increase was driven by the launch of only a few large projects and does not reflect an overall market recovery, as the number of new entrants remains limited, and new supply is still concentrated among financially strong major developers who can manage cost and liquidity risks better than others.

In terms of demand, Savills (Thailand) found that the Luxury and Super Luxury condominium segments remain the strongest in the past quarter, particularly penthouse units and large apartments in premium projects, which continue to attract high-income buyers, including end-users, long-term investors, and some foreign buyers. This indicates that high-end customers are relatively less affected by the economic situation and prioritize project quality, privacy, design, and location over price factors.

Popular locations include the central Sukhumvit area, Thonglor, and Ekkamai, which remain hubs for high-end living due to their amenities, public transport connectivity, lifestyle sources, and international schools. Additionally, these areas have limited new land supply, allowing projects in these locations to maintain price levels and achieve better sales than the overall market. Conversely, the middle to lower condominium market continues to face pressure from weak domestic purchasing power, high housing loan rejection rates, and intense price competition, leading most operators to focus on rapidly clearing existing stock, especially completed projects with unsold units, through promotional campaigns, price reductions, and additional benefits to stimulate consumer decision-making and accelerate revenue recognition.

Savills (Thailand) predicts that throughout 2026, approximately 16,000 new condominium units will be launched in Bangkok, a decrease of about 6.0% from 2025, which is still below the average launch levels before the COVID-19 pandemic. This reflects that most developers continue to adopt cautious investment strategies and choose to launch only projects with high sales potential. Furthermore, many major developers are beginning to shift their investment focus from Bangkok to tourist destinations and key economic cities such as Phuket and Pattaya, supported by the recovery of the tourism sector, an increase in foreign buyers, and demand for residential properties for investment and leisure, resulting in these provinces having higher growth potential than the Bangkok market in the short to medium term.

Although at the end of Q2, the Cabinet approved an extension of measures to reduce transfer fees and mortgage registration fees for residential properties, lowering the transfer fee from the normal rate of 2% to 0.01% and the mortgage registration fee from 1% to 0.01% until June 30, 2027, to help reduce the cost burden of purchasing housing and stimulate activity in the real estate market, these measures are expected to only partially support the market due to significant current limitations, including sluggish purchasing power, high household debt, and stringent credit assessment criteria from financial institutions.

Given these factors, Savills (Thailand) predicts that the overall Bangkok condominium market for the remainder of 2026 will remain a buyer's market, with competition focusing on clearing existing stock rather than increasing new supply. Developers will continue to prioritize cash flow management, selectively investing in low-risk projects, and developing projects in segments with clear demand support. Many developers agree that the condominium market in 2026 is one of the most challenging periods for the business in decades, due to constraints on purchasing power, development costs, and intense competition, resulting in a gradual overall market recovery with clear differences across price levels and locations.

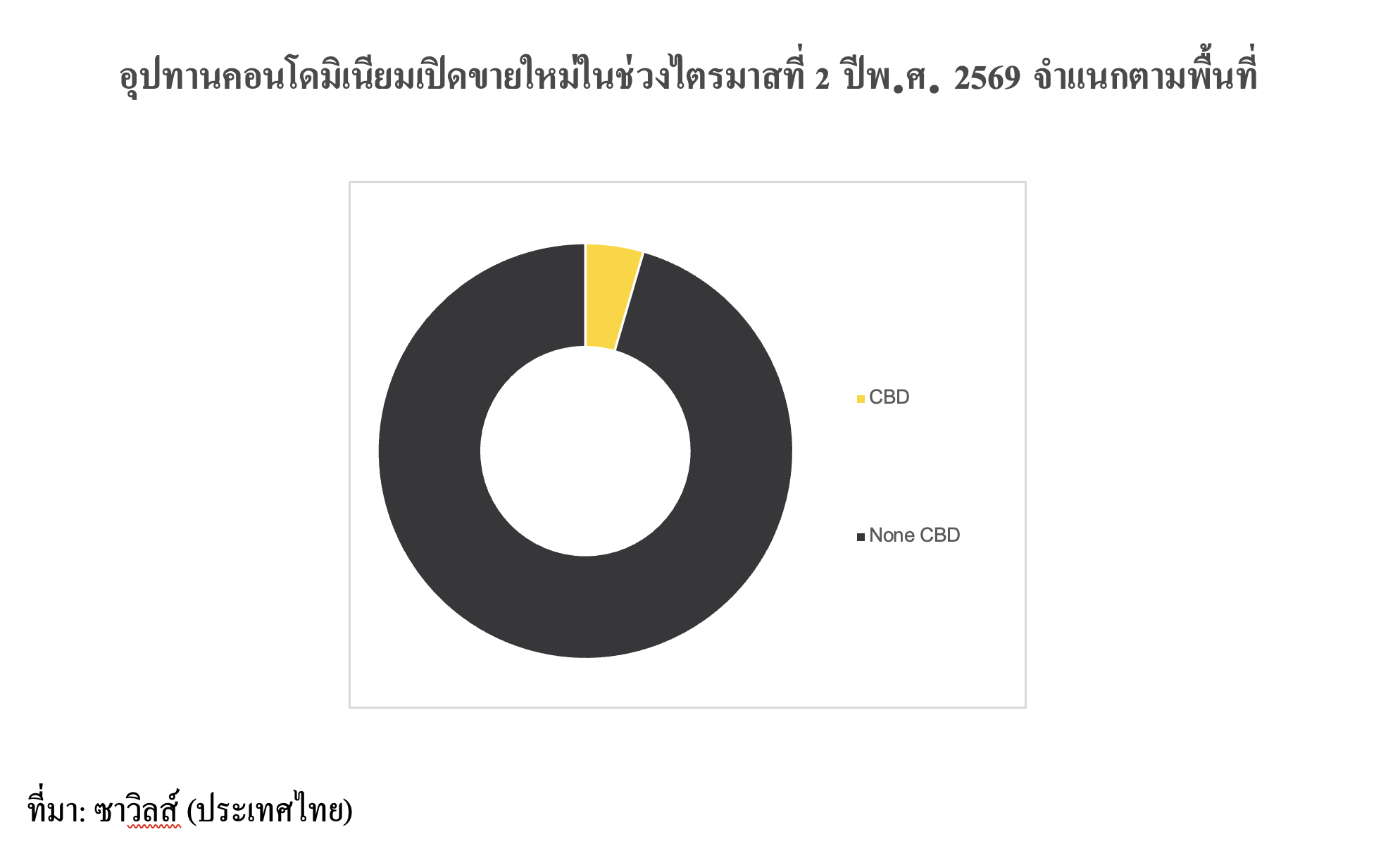

Savills (Thailand) found that of the total new supply of 5 projects comprising 2,260 units in Q2 2026, only 2 projects totaling 102 units, or 4.51% of the total new supply, are located in the Central Business District (CBD), with an average asking price of approximately 237,080 baht per square meter. Meanwhile, the majority of the supply, 87.92%, is located in the eastern suburban areas, with an average asking price of approximately 134,086 baht per square meter, and another 7.57% is located in the northern suburban areas, with an average asking price of approximately 86,500 baht per square meter.

The distribution of this supply reflects that developers continue to prioritize development in suburban areas over the city center due to continuously rising land cost constraints in the CBD and the necessity to develop projects at price levels that can meet market purchasing power. However, despite the relatively low proportion of new supply in the central business district, it remains a segment of high interest among buyers, especially projects with outstanding locations, development concepts, product quality, and limited unit numbers.

In the past quarter, the market also witnessed a phenomenon where interested buyers queued to reserve rights for certain projects in the city center even before the official sales launch, a sight not seen for some time. This reflects that the Luxury and Super Luxury condominium market, characterized by uniqueness and scarcity, continues to generate ongoing purchasing demand, even as the overall housing market remains sluggish. Savills (Thailand) believes that the success of projects in this segment is not solely due to location but also stems from appropriate pricing, product differentiation, long-term value creation, and the potential for investment returns, both in terms of capital appreciation and rental yield, which remain key factors attracting both end-users and investors.

Sales data for the first half of 2026 clearly indicates that Luxury condominiums in central areas such as Sukhumvit, Chidlom, Phloen Chit, and Lumpini continue to have strong acceptance rates and can maintain sales levels better than other market segments, reflecting the purchasing power of high-income groups that remain relatively less affected by the economic situation, in contrast to the middle and lower condominium markets that continue to face pressure from domestic purchasing power and limitations on access to housing credit.

However, in the suburban condominium market, Savills (Thailand) found that several projects also achieved satisfactory sales levels, but the key factors supporting these sales did not solely arise from demand growth; rather, they resulted from competitively set opening prices, with many developers choosing to launch projects at significantly lower prices than the average market rates in the same locations to enhance accessibility for buyers and accelerate purchasing decisions. This situation reflects intensified price competition, and in some areas, the new asking price levels are approaching those seen in the market over a decade ago after adjustments through pricing strategies and various promotions.

For the second half of 2026, Savills (Thailand) predicts that the Luxury condominium market will continue to be the segment with the most outstanding performance, particularly Branded Residence projects in central areas, which will still be supported by demand from high-income groups and foreign buyers. At the same time, developers will continue to emphasize launching projects with appropriately set prices that can create competitive advantages from the day of sale.

Additionally, Savills (Thailand) expects that riverside condominiums and Campus Condominium projects located near leading universities and large medical centers will continue to attract developers' interest, as they have clear demand bases from end-users, investors, and parents looking to purchase housing for their children. This suggests that both market segments still have potential for new project development in the future, even as the overall Bangkok condominium market remains in a gradual recovery phase.