Phuket Villa Prices Average 285 Million Baht, Ultra Luxury Market Grows Despite Condo Slowdown

The residential market in Phuket continues to be supported by the recovery of the tourism sector, the growth of long-stay residents, and demand from investors and foreign buyers. However, market trends are starting to diverge clearly between the condominium and villa markets, particularly in the luxury villa segment, which continues to grow despite increased competition in the overall market.

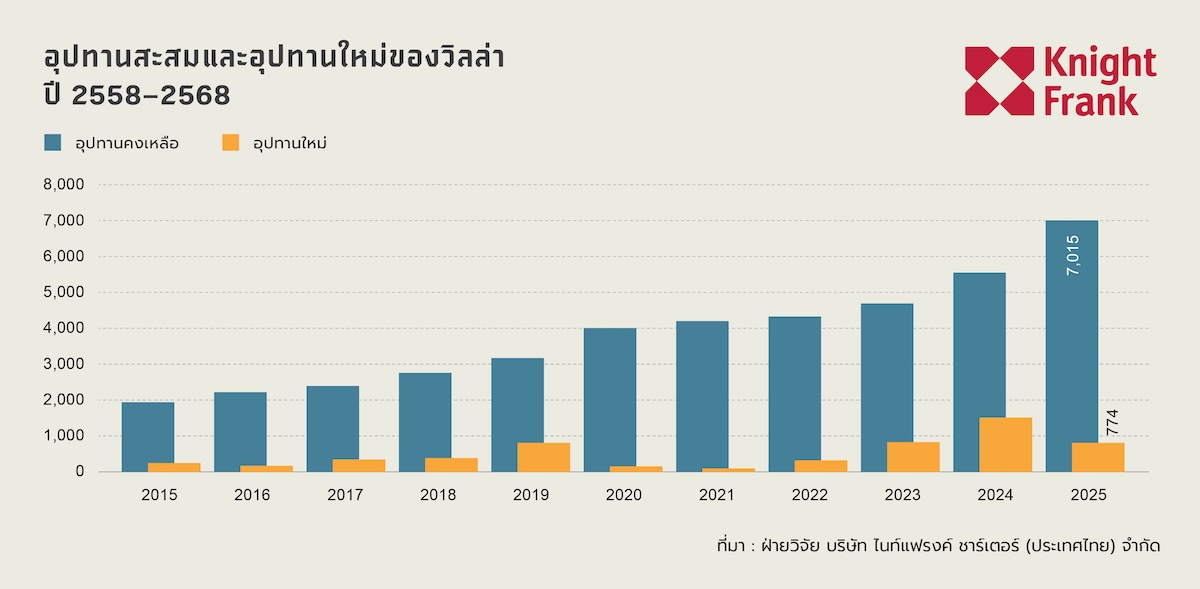

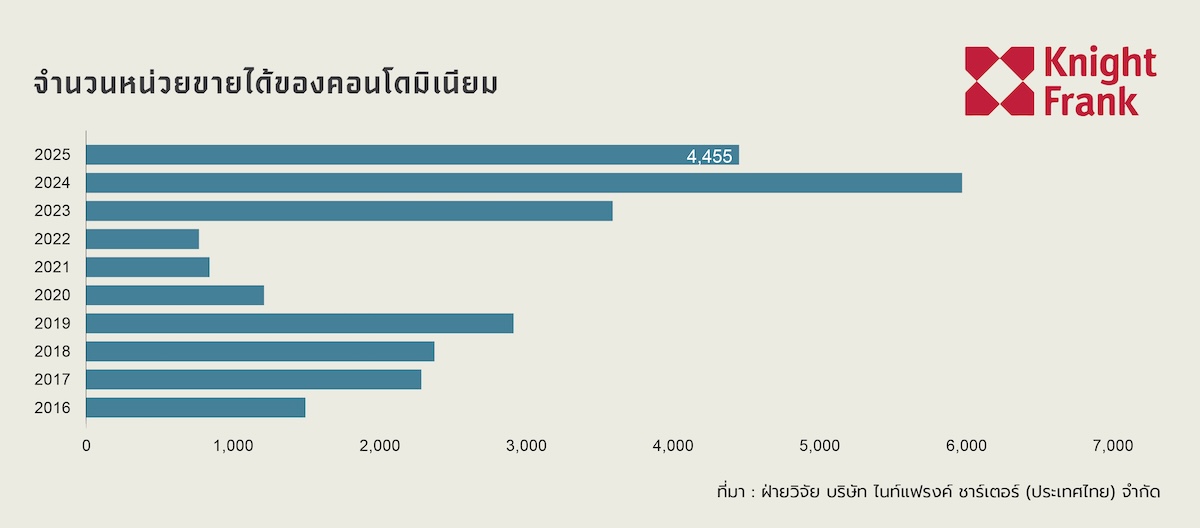

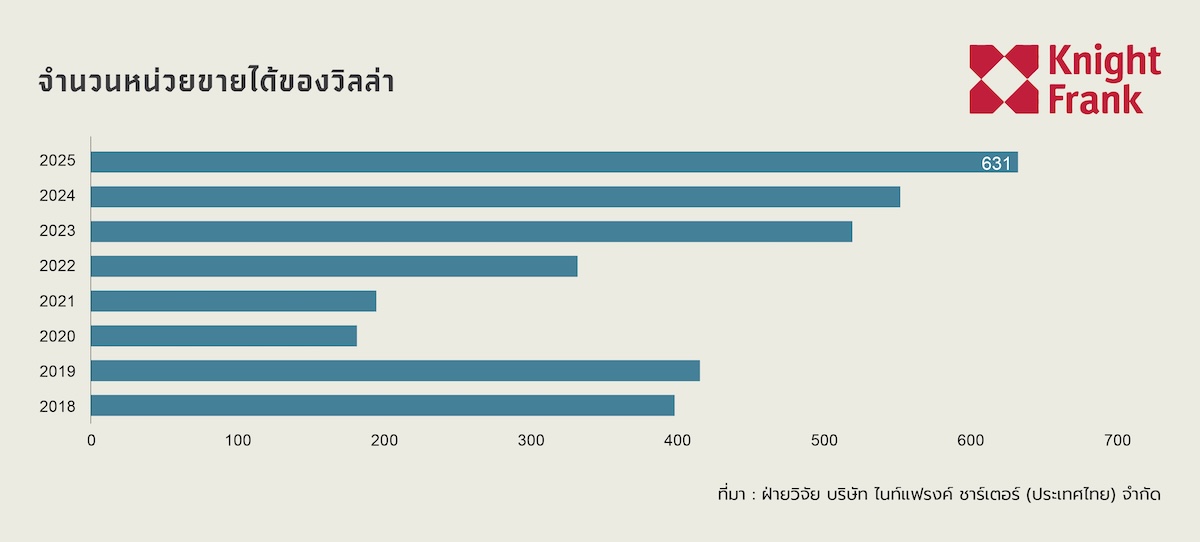

According to data from Knight Frank Thailand, by 2025, the villa market in Phuket has a total supply of 7,789 units, with new sales of 631 units, an increase of 12.9% from the previous year. In contrast, the condominium market, with a total supply of 42,061 units, saw new sales of 4,455 units, a decrease of 24.8% from the previous year. This reflects that demand in the high-end market remains strong, even as overall market buyers are becoming more cautious.

One of the key factors supporting the growth of the villa market is the demand from high-net-worth buyers looking for vacation homes, long-term residences, and investment properties in locations with long-term potential, especially in the western coastal areas of Phuket, which remain the most popular locations for both Thai and foreign buyers.

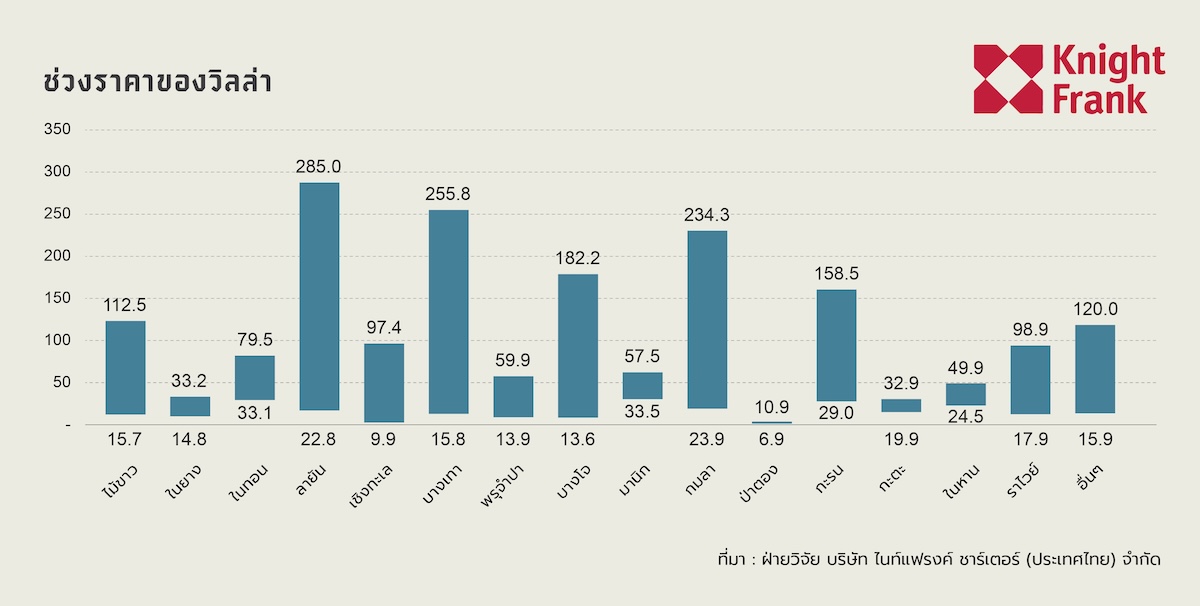

In terms of pricing, the high-end villa market in Phuket has clearly entered the Ultra Luxury segment, with Layan having the highest average selling price at approximately 285 million baht per unit, followed by Bang Tao at 255.8 million baht per unit, and Kamala at 234.3 million baht per unit. These price levels are comparable to those in high-end vacation home markets in leading global destinations.

These figures indicate that the 200–300 million baht villa market is no longer a niche market but is becoming one of the key segments of the Phuket residential market, supported by high-net-worth individuals, foreign investors, and buyers seeking high-quality properties for long-term holding.

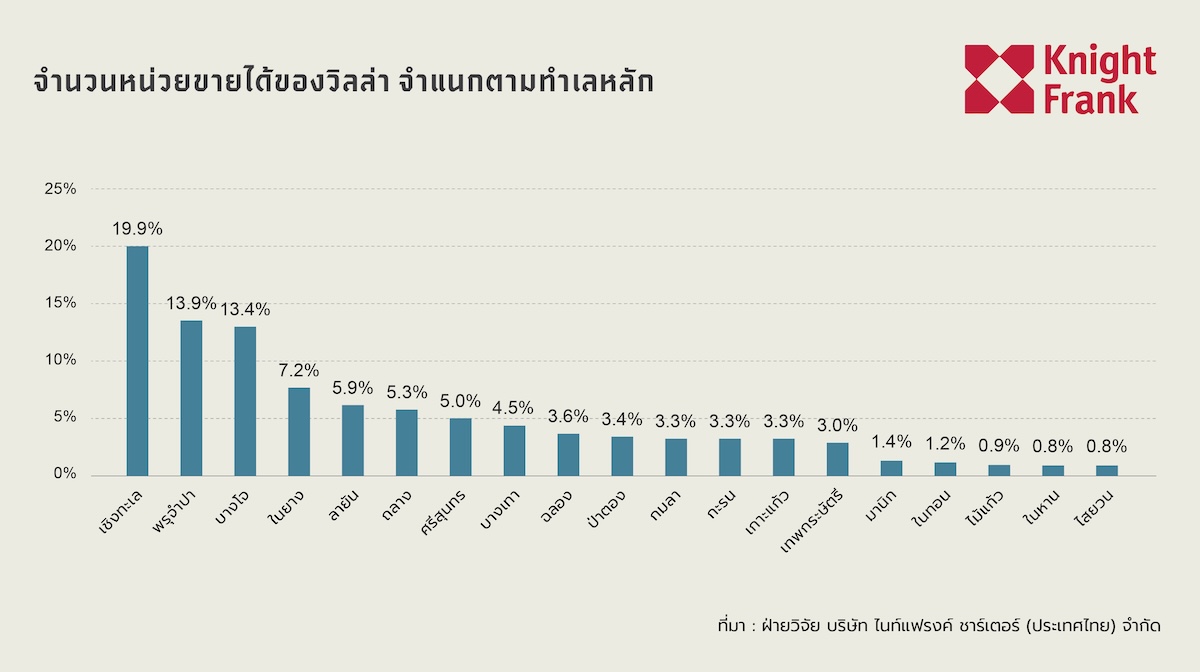

In terms of location, Cherng Talay remains the area with the highest villa sales in 2025, accounting for 19.9% of total sales, followed by Paklok at 13.9% and Bang Jo at 13.4%. This reflects that buying demand continues to concentrate in areas close to the beach and major lifestyle hubs of the province.

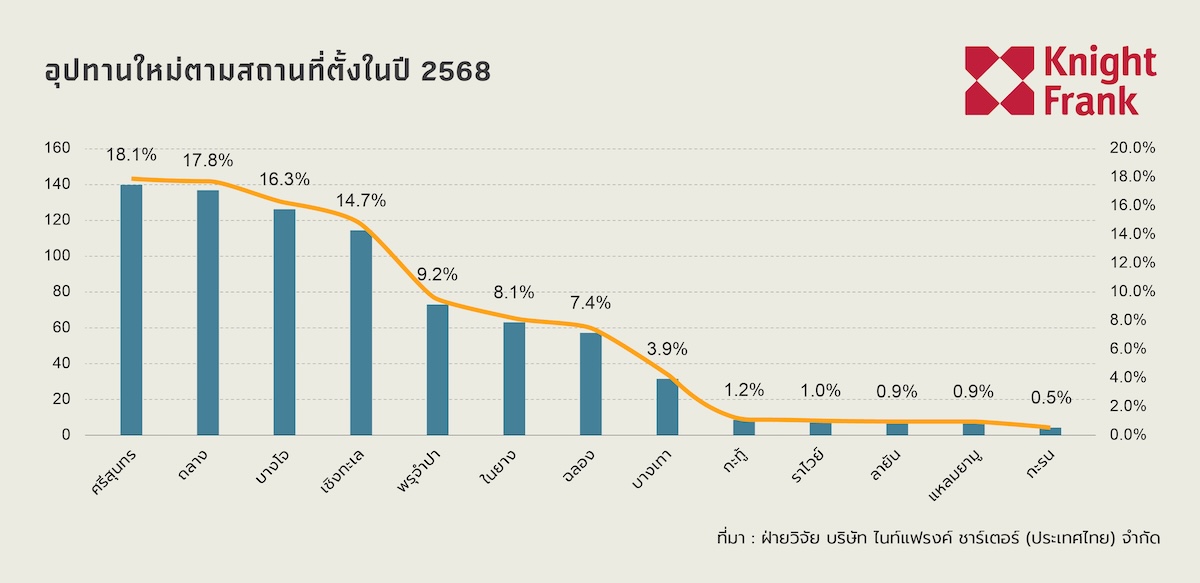

Meanwhile, new project developments are starting to expand into areas like Si Sunthorn and Thalang, with Si Sunthorn having the highest proportion of new supply at 18.1%, followed by Thalang at 17.8% and Bang Jo at 16.3%. This reflects land limitations and rising development costs in Phuket's main coastal areas, pushing developers to seek new locations to accommodate future growth.

Mr. Nattha Khahapana, Partner – Managing Director of Knight Frank Thailand stated, "One of the interesting signals in the current Phuket market is the strength of the high-end villa market. Although the overall market is becoming more competitive, demand from high-net-worth buyers continues to be strong, especially in locations that can meet the needs for living, relaxation, and long-term property value retention."

"Currently, Phuket is not only competing with domestic destinations but is also competing with high-end resort and vacation home markets in the region and globally. Many buyers see Phuket as more than just a tourist destination; it is a place for living, investing, and long-term wealth allocation."

Knight Frank Thailand believes that the luxury villa market will continue to grow in the future, supported by the recovery of the tourism sector, the expansion of long-stay residents, and ongoing demand from foreign buyers looking for high-quality assets in one of the most important lifestyle destinations in the Asia-Pacific region.