Thai Economic Outlook for 2026: Projected Growth Slows to 1.6% Due to External Risks and Domestic Politics

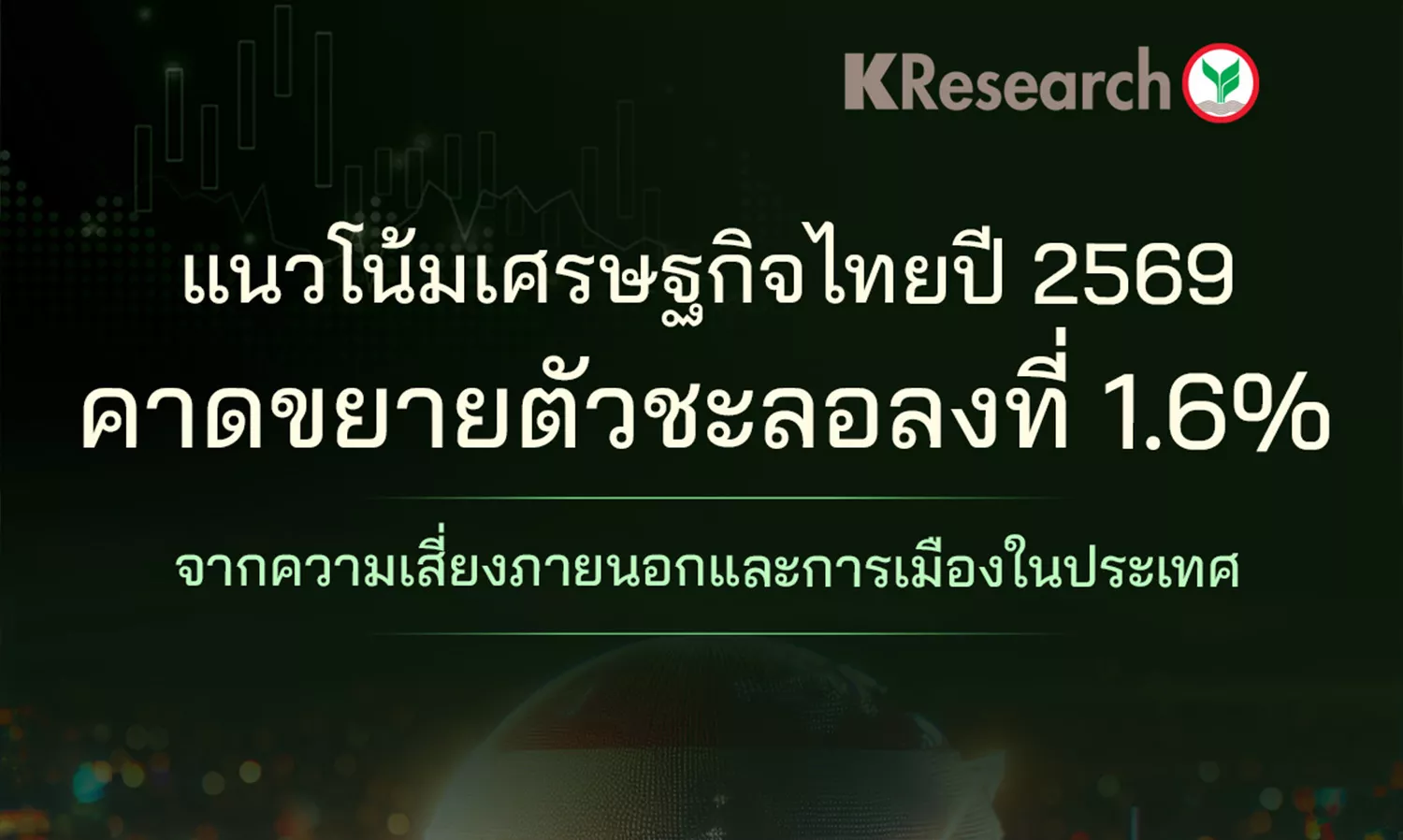

The Thai economy is expected to grow at a slower rate of 1.6% in 2026, down from an estimated 2.0% in 2025, amid high external risks, particularly geopolitical tensions and U.S. trade policies.

Exports, which were a key driver of the Thai economy in 2025, face a contraction risk of -1.2% with the following details:

- The main pressure comes from U.S. tax measures, which are expected to have clearer impacts after a surge in exports in 2025. Exports of goods subject to tariffs under Section 232 and Reciprocal tariffs are likely to slow down. Additionally, there is a risk that the U.S. will expand the range of products subject to increased import tariffs under Section 232, particularly in ICs and semiconductor products.

- Global trade is expected to slow down and face increased competition, further pressuring Thai exports. The World Trade Organization (WTO) forecasts that global trade will grow by only 0.5%, down from 2.4% the previous year, while China continues to face excess supply issues despite implementing anti-involution measures to reduce overproduction to address pricing problems, such as setting quotas for production and supporting inefficient mergers. However, inventory levels remain high, causing Thai exports to face competition from Chinese imports in both domestic and other export markets.

- Thai exports in 2026 to major markets such as the U.S., ASEAN, and Japan are expected to contract, while exports to China and the Eurozone are projected to still grow positively but at a slower pace, supported by electronics and agricultural products.

- U.S.: Exports are expected to contract by -5.8% from a high base in the previous period, which saw a surge in exports before the U.S. import tariffs took effect, coupled with slowing demand in the U.S., particularly for electronics, which is expected to shrink by -10.5% (contribution to growth -6.0%), led by products at risk of additional tariffs under Section 232, such as integrated circuits, diodes, and transistors in the semiconductor category. However, if these products are not subject to Section 232 tariffs, Thai exports to the U.S. would contract less severely to -4.2%, helping to limit the overall contraction of Thai exports in 2026 to only -0.8%. Products expected to still grow include Hard Disk Drives and electronic components related to Data Centers, such as communication devices and storage equipment, although growth rates will slow compared to the previous year.

- ASEAN: Exports are expected to contract by -3.5%, led by energy and fuel exports projected to shrink by -17.9% (contribution to growth -1.6%) and a decline in gold exports, along with a slowdown in electronics exports due to supply chains linked to the U.S. market. Additionally, the closure of the Thai-Cambodian border has resulted in nearly a 100% drop in Thai exports to Cambodia through the border (accounting for about 6% of Thai exports to ASEAN).

- Japan: Exports are expected to slightly contract by -0.4% due to a slowdown in automotive and parts exports projected to decrease by -3.4% (contribution to growth -0.3%). Although Japan can maintain domestic production capacity, it faces increased competition from Chinese manufacturers, as well as in chemicals and plastic pellets. Furthermore, the Japanese market is not benefiting from AI and data center trends compared to other countries, leading to a lack of support for electronics.

- China: Exports are expected to still grow at 1.2%, supported by a 5.5% growth in electronics exports (contribution to growth 1.3%) driven by domestic demand for AI-related and data center products, as well as agricultural products such as wheat products, seasonings, canned fruits, and sugar, which are expected to return to positive growth from a low base.

- European Union: Exports are expected to grow by 0.9%, supported by electronics that can still grow at 1.7% (contribution to growth 0.7%), along with agricultural products expected to continue growing due to food security issues.

In 2026, although the Carbon Border Adjustment Mechanism (CBAM) will be implemented, the impact on exports to the European Union is expected to be minimal, as exports of steel and aluminum, the first products subject to CBAM taxes, account for only 2.3% of the value of Thai exports to the EU.

- The upward cycle of electronics continues to support Thai exports, but at a slowing pace, driven by the expansion of AI technology and investment in data centers, which support the export of Thai electronics such as HDDs, PCBs, and computers. However, the export direction of these products in 2026 is expected to slow compared to the previous year, as some orders have already surged in the past, resulting in a high growth base, coupled with global demand returning to normal after the IT equipment upgrade cycle has passed, and pressures from a slowing global economy, a strengthening baht, and uncertainties in trade policies and geopolitics.

- The U.S. Supreme Court may issue a ruling to suspend and cancel the collection of import tariffs under the IEEPA law, which would affect Thailand through the 19% Reciprocal tariff. This could lead to another surge in exports, but the boost is expected to be limited due to the high base in the previous year and slowing demand in the U.S., while other U.S. trading partners will also benefit, particularly China, where the tariff rate will drop from 47.6% to 27.6%, resulting in some Thai products that previously benefited from lower IEEPA tariff rates, such as air conditioners, potentially losing that advantage. Additionally, the U.S. still has other trade tools to impose additional import tariffs, including:

- Section 232, which grants authority to impose tariffs on imports citing national security reasons.

- Section 301, used to retaliate against countries with unfair trade practices.

- Section 122, which grants authority to impose temporary measures for no more than 150 days.

- Section 201 (safeguard), which grants authority to impose tariffs or set temporary quotas to assist domestic industries affected by rapidly increasing imports.

Therefore, risks from U.S. trade policies remain a pressure on global trade overall.

Imports are expected to slow down in line with exports, particularly in intermediate and capital goods, such as electronic components and electrical machinery, which saw high growth in the previous year. Additionally, crude oil imports may decrease in line with global oil prices. However, imports of consumer goods, especially from China, are expected to continue to grow positively, as the De Minimis measure that imposes import tariffs and VAT on goods valued under 1,500 baht is unlikely to affect the volume of consumer goods imported from China, resulting in Thailand's trade balance in 2026 remaining in surplus but lower than in 2025.

The number of foreign tourists in 2026 is expected to increase to 34.1 million from 32.97 million the previous year, while revenue from foreign tourists is expected to rise by 4.5% to 1.61 trillion baht (contribution to GDP growth 0.3%). However, the Thai tourism sector still faces competition from regional countries, coupled with a strong baht. Additionally, safety issues continue to pressure tourist confidence.

The baht is expected to strengthen in the short term, supported by rising gold prices. However, by the end of 2026, the baht may weaken to 32.8 baht per U.S. dollar due to domestic factors, including slowing economic growth, political uncertainties, and impacts from U.S. trade policies.

Domestic demand is slowing down, while the manufacturing sector continues to contract for the fourth consecutive year amid uncertainties in government formation and the direction of the new government's policies.

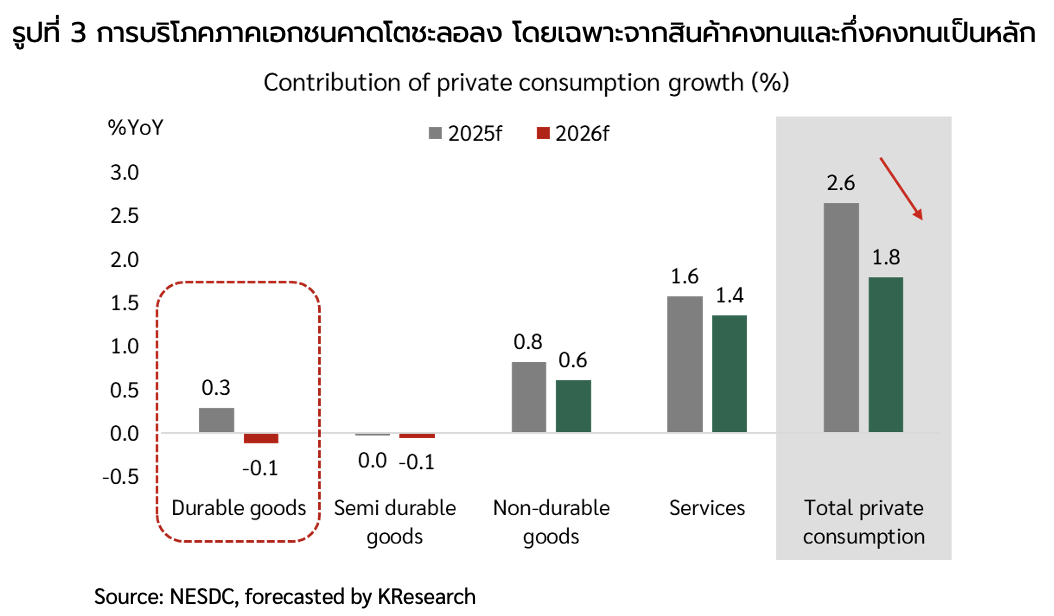

Private consumption is expected to remain the main driver of the Thai economy but is projected to grow at a slower rate of 1.8% down from 2.6% the previous year, reflecting weakened domestic demand, high household debt burdens, and tight credit conditions.

- Spending on durable goods is expected to slow down the most, in line with projected car sales to contract by -1.7% after growing approximately 4.8% in 2025 due to a surge in BEV car sales driven by price wars and the expiration of the EV 3.0 measures at the end of 2025, while spending in the service sector remains a key support for private consumption.

- In the first quarter of 2026, support from economic stimulus measures will significantly decrease after the conclusion of the Half-Half program, and there will be no tax relief measures (Easy E-Receipt) like in the first quarter of 2025, coupled with the remaining mid-year budget of only about 50 billion baht, resulting in limited space for economic stimulus measures this year.

- At the same time, during the election period, there is expected to be a flow of funds into the economy, which will have a short-term positive effect on the service sector, particularly in food and accommodation businesses, transportation and logistics, as well as retail.

Private investment is expected to slow down, particularly in the manufacturing and construction sectors, as the real estate sector continues to face ongoing pressures. Investment in housing is likely to stagnate due to slow recovery in demand, high household debt burdens, and strict lending conditions from financial institutions.

However, private investment is supported by foreign investment inflows in data center industries, driven by the expansion of the digital economy and AI technology, as well as the government's "Fast Pass" project aimed at facilitating and expediting the investment process, which is expected to partially support private investment, particularly in machinery, equipment, and development in industrial estate areas.

However, these positive effects are expected to gradually materialize, as most investments are large-scale projects that require several years of continuous implementation.

Public investment spending is expected to slow down in line with anticipated lower disbursement of investment budgets during the election period and waiting for the new government to be formed, coupled with the budget framework for public investment (including state enterprises) in 2026 not increasing significantly.

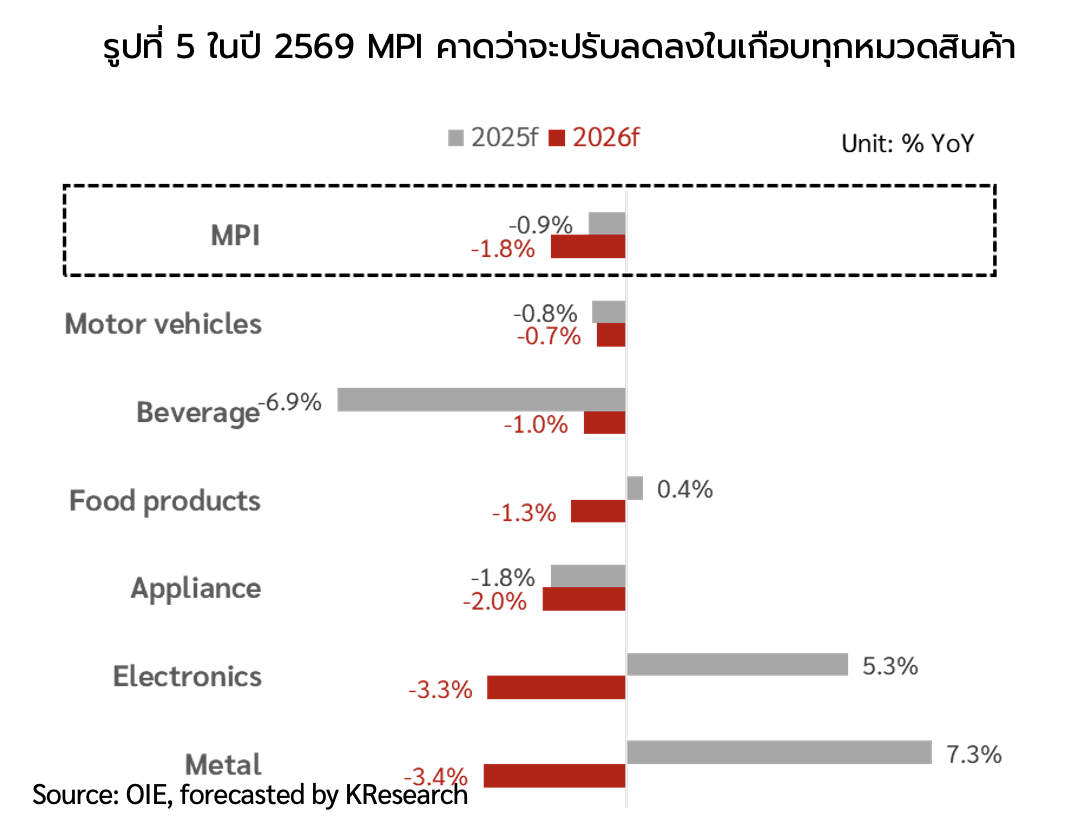

The Thai production sector is expected to remain sluggish, with the Manufacturing Production Index (MPI) projected to contract for the fourth consecutive year due to weakened orders both domestically and internationally, coupled with facing high competition from imports, which pressures production in almost all major categories, such as automotive, electronics, electrical appliances, and food and beverages, to continue to contract.

Meanwhile, agricultural production may decrease from the previous year due to lower water availability for cultivation, as climate conditions are expected to normalize (neutral) starting in the second quarter of 2026.

Additionally, farmers' incomes are expected to contract as they continue to face competition in the global market, particularly for rice products, as India, a major exporter in the global market, continues to increase its exports.

Domestic political factors remain an uncertainty for the Thai economy, particularly regarding the formation of a new government. If a government can be formed quickly, there is a chance that the budget for 2027 will be expedited for use by the end of 2026. However, if the government formation is delayed, it will impact the continuity of policies, delays in preparing the 2027 budget, budget disbursement, and investor confidence.

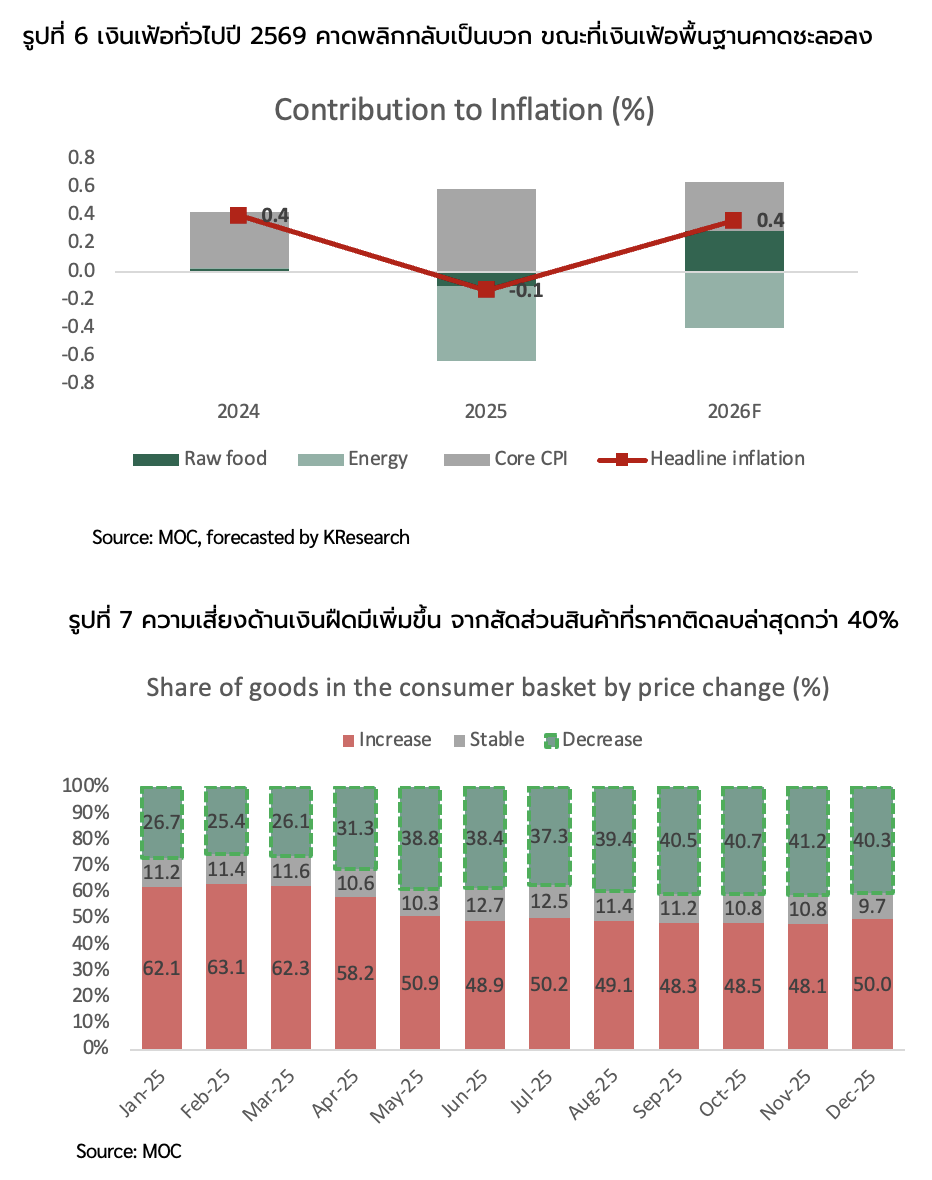

Thailand continues to face deflation risks, with general inflation in 2026 expected to grow positively at 0.4% due to easing supply pressures, particularly for fresh food prices recovering from a low base in the previous year, while global energy prices decrease.

- The average price of Dubai crude oil in 2026 is expected to be around $62 per barrel, slightly down from $68.3 per barrel in 2025.

- The latest retail price of diesel has been reduced by 50 satang to 29.94 baht per liter as of January 9, 2026, and is expected to decrease further in the remaining year, in line with global oil price trends and the status of the fuel fund expected to return to positive by the end of January 2026.

- Most political party policies focus on reducing the burden of living costs in the short term, such as lowering electricity and public transport fares, which will continue to pressure inflation in the future.

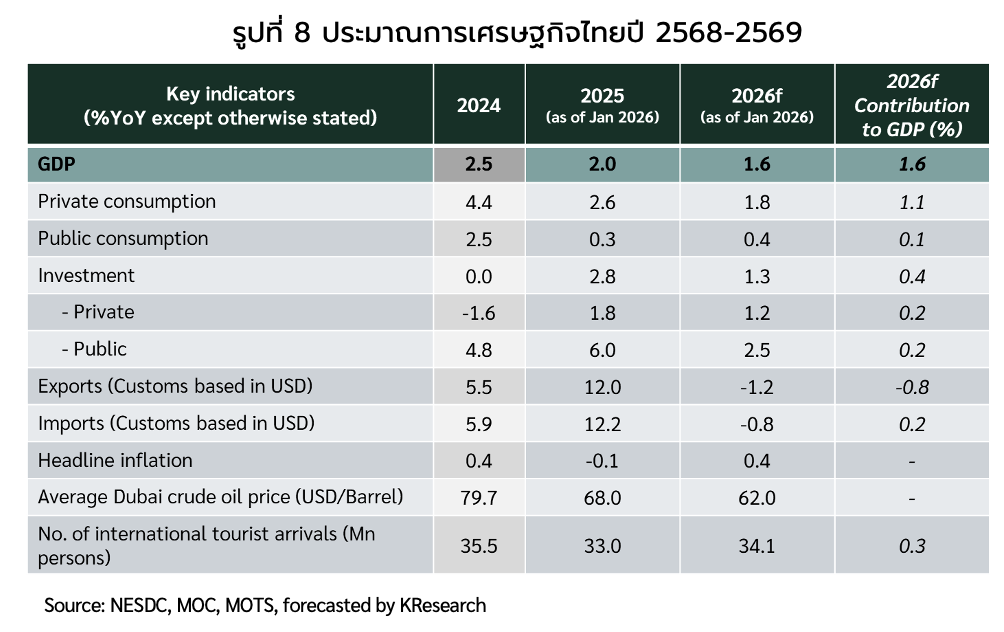

- Core inflation is expected to continue to grow but at a slowing rate of 0.5% in line with domestic purchasing power. However, deflation risks remain, reflected in the increasing proportion of falling prices of goods and services in the inflation basket.