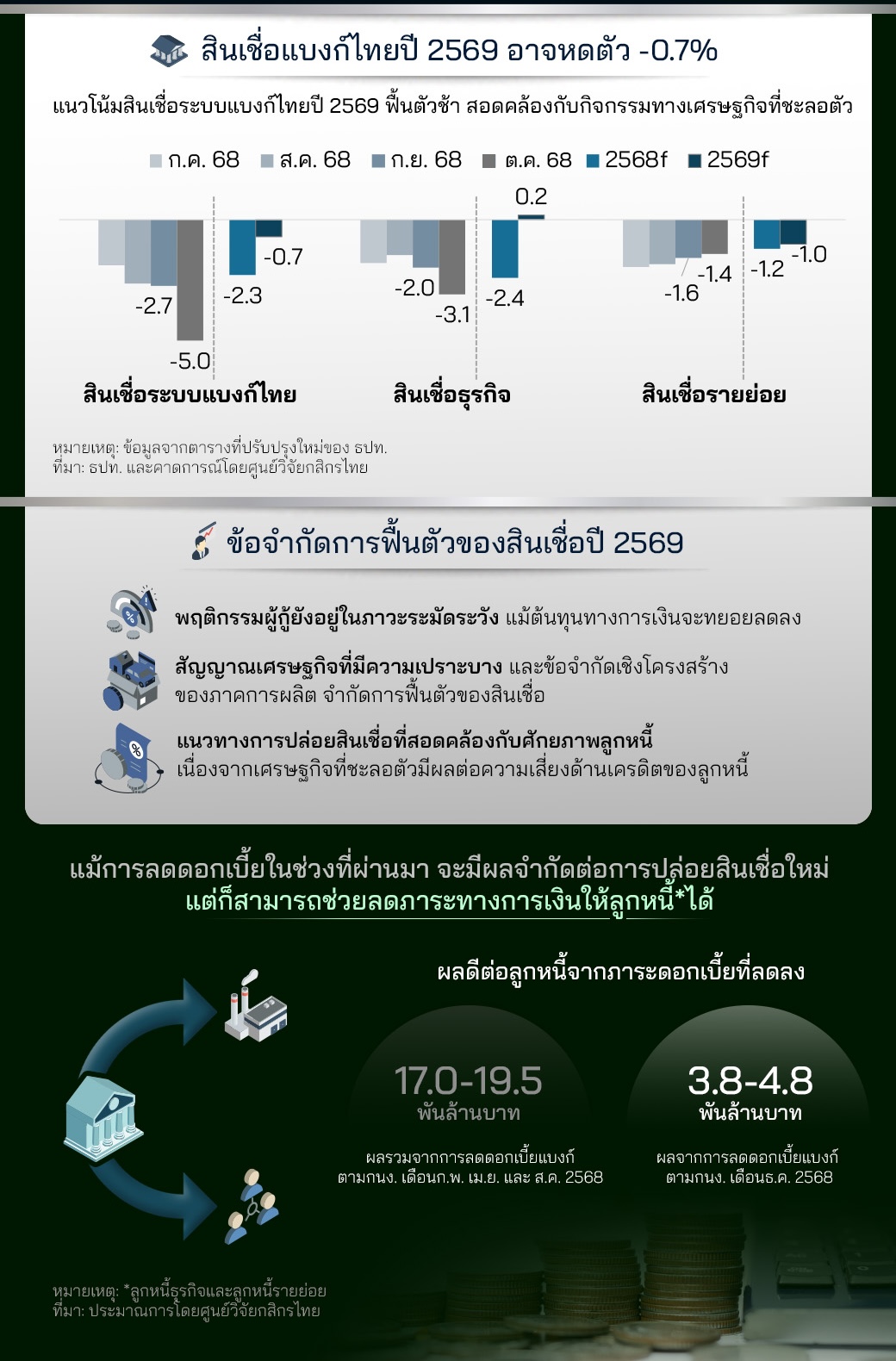

2026 Loans in Negative for the Third Year, Interest Rate Cuts Support Debtors

The overall picture of Thai banking system loans in 2026 continues to face ongoing pressure from a fragile economy. Kasikorn Research Center estimates that total loans are likely to contract by approximately -0.7%, marking a third consecutive year of decline. Although loans for large businesses are beginning to show signs of recovery, loans for SMEs and individuals remain constrained by competitiveness, income, and domestic purchasing power that has not fully returned.

Imbalanced Recovery Structure

The main driving force in 2026 comes from loans to large businesses, while loans to medium and small enterprises, as well as individuals, continue to slow down. This reflects a slow and uneven economic recovery, particularly in the manufacturing sector and among households that are still cautious about taking on new debt.

Interest Rate Cuts Alleviate Burden but Do Not Accelerate Lending

The reduction in loan interest rates at the end of 2025 significantly alleviated the financial burden on debtors.

-

It helped ease the burden on debtors in 2025 by approximately 17.0–19.5 billion baht.

-

It is expected to provide an additional 3.8–4.8 billion baht in the first half of 2026.

However, the interest rate cuts have a more “supportive” effect rather than “stimulating” new lending, as banks continue to assess risks stringently amid economic uncertainties.

Loan Quality Remains Tight

Although lower interest rates increase the chances of debt repayment, loan quality still depends on the overall economic direction. It is expected that the non-performing loan (NPL) ratio in 2026 will remain high at 2.80–2.97% of total loans. Financial institutions will still need to rely on continuous debt restructuring to support both debtors and the stability of the financial system.

Interpretative Perspective

2026 is a year of “stabilization” rather than acceleration. Loans are not yet ready to become the main driving force of the economy, while the reduced interest rates act like a supportive force beneath the vessel, preventing the debtor burden from sinking deeper. However, true recovery still awaits the revival of income, business competitiveness, and broader economic confidence.