Hotel Business Situation in the First Half of 2025

The Real Estate Information Center (REIC) of the Government Housing Bank (GHB) has prepared an analysis titled "Hotel Business Situation in the First Half of 2025" which reveals the following:

Overall, the demand for hotel services has slowed compared to the same period last year (YoY), attributed to a 4.7% decrease in international tourists arriving in Thailand. However, the average occupancy rate of hotels nationwide has increased to 60.8%, up from 59.1% in the same period last year, reflecting a continuous growth trend in accommodation demand.

In terms of supply, there has also been a slowdown compared to the same period last year (YoY), with the number of new hotel applications and new room counts decreasing by 34.6% and 32.2%, respectively. This has resulted in a 3.7% decrease in the total number of registered hotels nationwide and an 18% decrease in the total number of rooms. Nevertheless, future supply trends show signs of expansion, with permitted hotel construction area increasing by 29.6%, particularly in the Bangkok metropolitan area, where construction permits have surged by 230.7% compared to the same period last year (YoY). This is due to Bangkok and its surrounding areas being a business and tourism hub that continuously attracts tourists and investors. Details are as follows:

1. Supply Situation

1.1 New Hotel Applications Nationwide

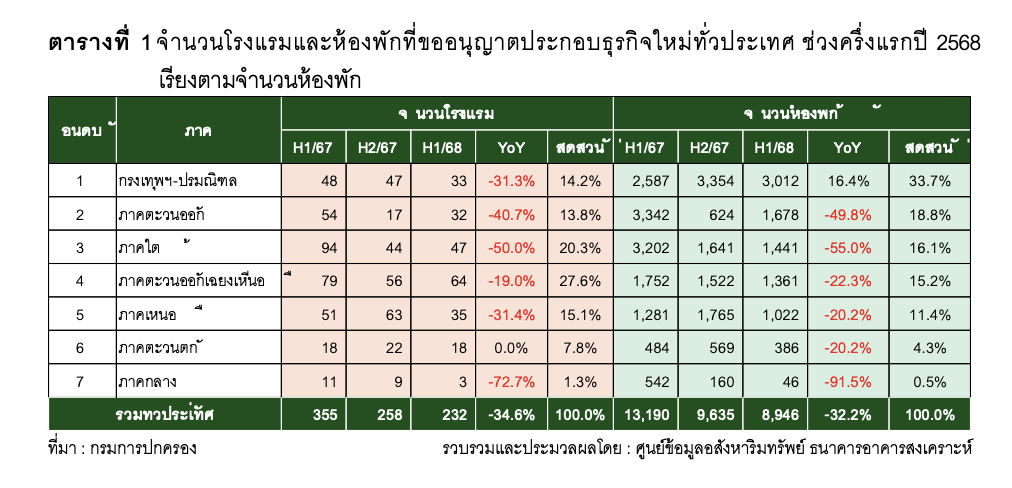

In the first half of 2025 (January - June), there were 232 new hotel applications nationwide, totaling 8,946 rooms, representing a decrease of 34.6% in the number of hotels and 32.2% in the number of rooms compared to the same period last year (YoY), which had 355 hotels and 13,190 rooms. The Bangkok metropolitan area accounted for the highest number of new room applications at 3,012 rooms, making up 33.7% of the total. Consequently, the overall number of new hotel applications decreased across almost all regions, except for the western region, which remained unchanged compared to the same period last year (YoY). The number of new room applications decreased in almost all regions, except for Bangkok and its surrounding areas, which saw an increase of 16.4%, indicating that operators are still delaying new project openings, particularly in the southern and central regions, where the number of new hotel applications has decreased significantly by more than 50% compared to the same period last year (YoY) (details in Table 1).

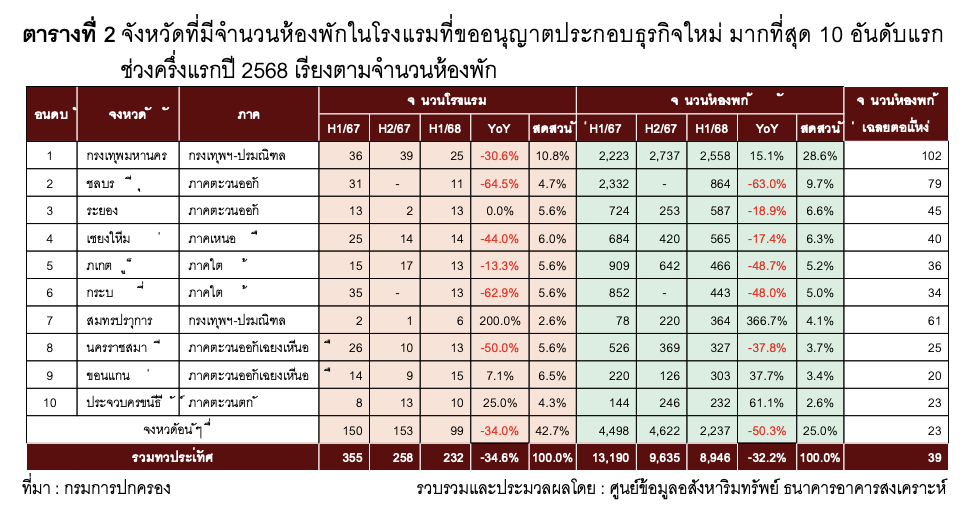

The top 10 provinces with the highest number of new hotel room applications in the first half of 2025 accounted for 75.0% of the total new hotel room applications nationwide, including Bangkok, Chonburi, Rayong, Chiang Mai, Phuket, Krabi, Samut Prakan, Nakhon Ratchasima, Khon Kaen, and Prachuap Khiri Khan, respectively. Among these, Samut Prakan saw the highest increase at 366.7%, followed by Prachuap Khiri Khan, Khon Kaen, and Bangkok, which also saw increases compared to the same period last year (YoY). In contrast, Chonburi experienced the largest decrease at 63.0%, followed by Phuket, Krabi, Nakhon Ratchasima, Rayong, and Chiang Mai, which all saw decreases compared to the same period last year (YoY). Other provinces saw a decrease of 50.3% compared to the same period last year (YoY) (details in Table 2).

1.2 Cumulative Hotel Applications Nationwide

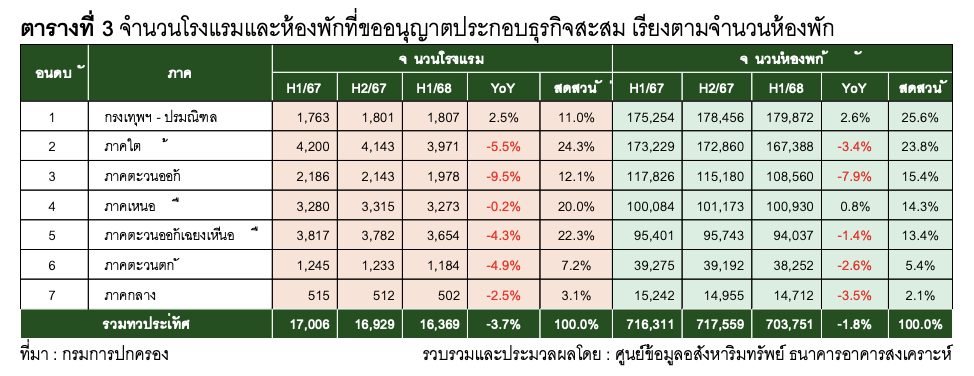

The cumulative number of registered hotels nationwide (excluding guesthouses, resorts, or unregistered hotels) as of the first half of 2025 was 16,369, with 703,751 rooms available, representing a decrease of 3.7% in the number of hotels and 1.8% in the number of rooms compared to the same period last year (YoY), which had 17,006 hotels and 716,311 rooms. When considering the cumulative number of available rooms in the first half of 2025 compared to the same period last year (YoY) by region, Bangkok and its surrounding areas had the highest number of available rooms at 179,872, an increase of 2.6%, accounting for 25.6%. The southern region had 167,388 rooms, a decrease of 3.4%, accounting for 23.8%, while the eastern region had 108,560 rooms, a decrease of 7.9%, accounting for 15.4% of the total rooms (details in Table 3).

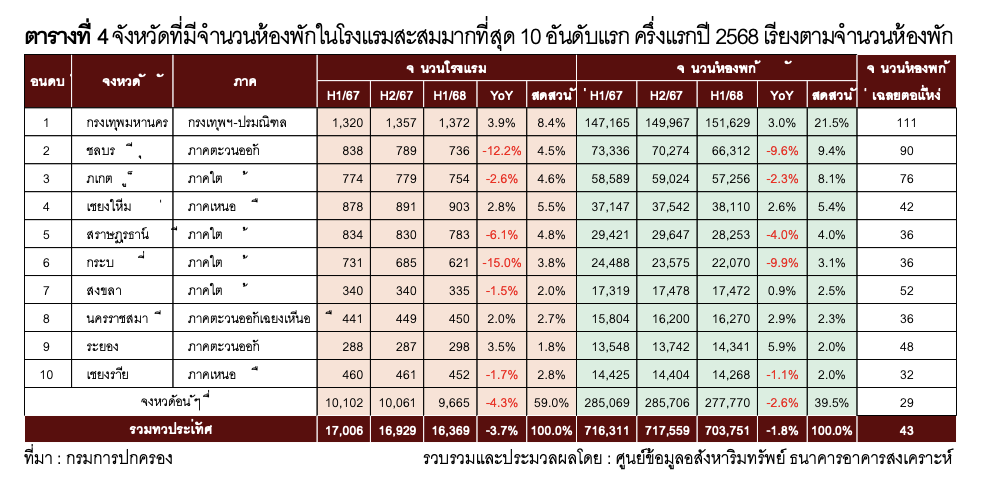

When considering the cumulative number of available hotel rooms by province, the top 10 provinces with the most rooms as of the first half of 2025 accounted for 60.5% of the total available rooms, including Bangkok, Chonburi, Phuket, Chiang Mai, Surat Thani, Krabi, Songkhla, Nakhon Ratchasima, Rayong, and Chiang Rai. Among these, Rayong saw the highest increase at 5.9%, while Krabi experienced the largest decrease at 9.9%. Other provinces saw a decrease of 2.6% compared to the same period last year (YoY) (details in Table 4).

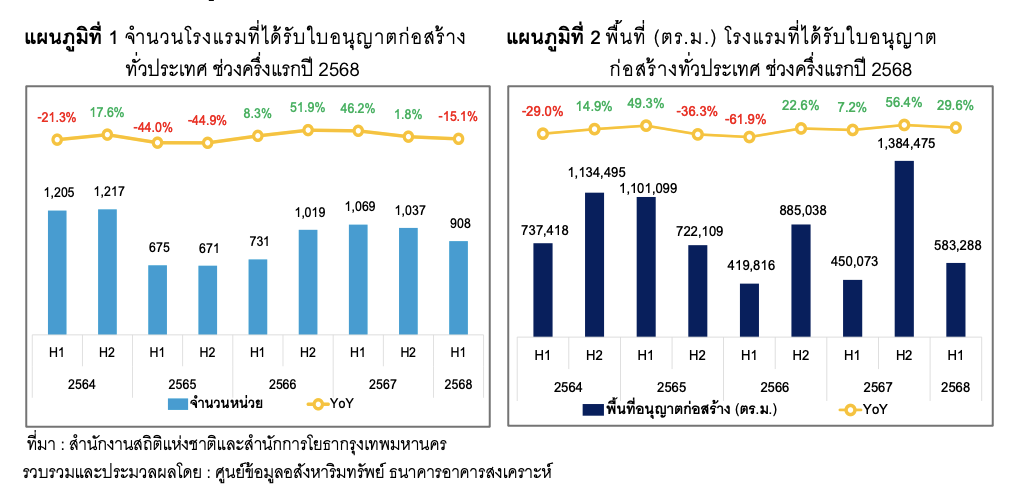

1.3 Hotel Construction Permits

In the first half of 2025, 908 hotel construction permits were issued, a decrease of 15.1% compared to the same period last year (YoY), which had 1,069 permits. However, the total permitted construction area increased to 583,288 square meters, up 29.6% compared to the same period last year (YoY), which had 450,073 square meters (details in Charts 1 and 2).

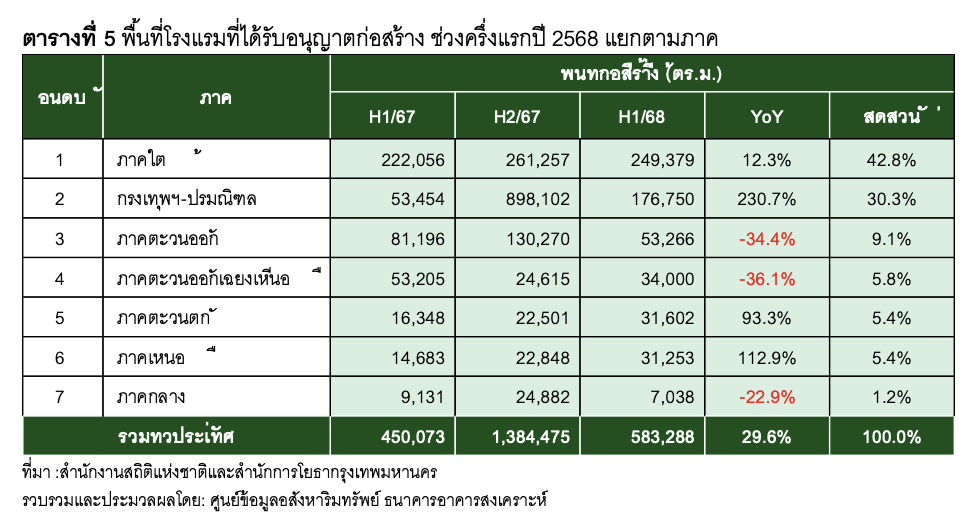

When analyzing hotel construction permits by region in the first half of 2025, the southern region had the largest permitted construction area at 249,379 square meters, accounting for 42.8% of the total permitted construction area. Regions that saw growth in hotel construction area compared to the same period last year (YoY) included Bangkok and its surrounding areas, which increased by 230.7%, followed by the northern region at 112.9%, the western region at 93.3%, and the southern region at 12.3% (details in Table 5).

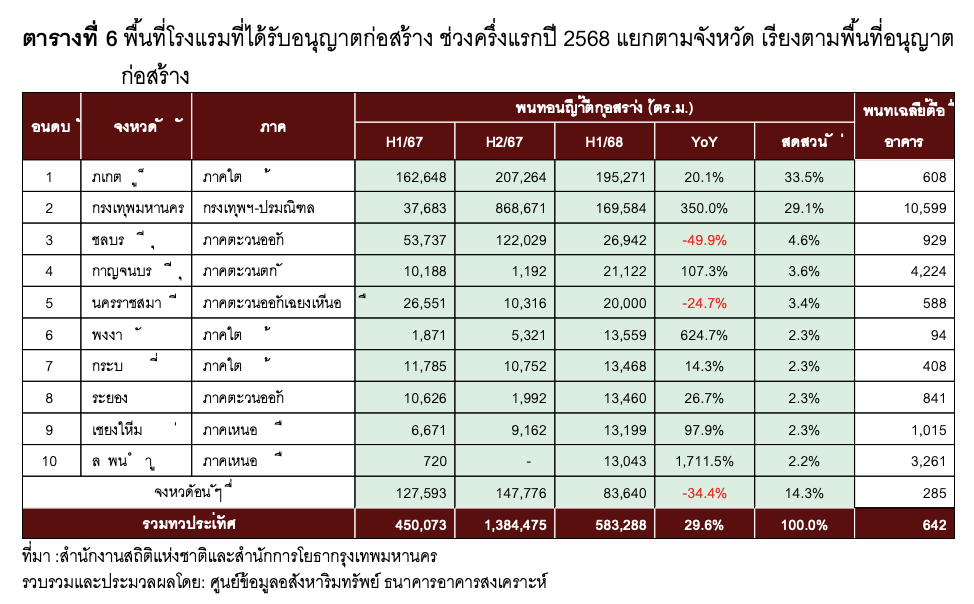

For the top 10 provinces with the most hotel construction permits in the first half of 2025, they collectively accounted for 85.7% of the total, with Phuket having the largest permitted construction area at 195,271 square meters, accounting for 33.5% of the total permitted construction area, an increase of 20.1% compared to the same period last year (YoY). Following Phuket were Bangkok, Chonburi, Kanchanaburi, Nakhon Ratchasima, Phang Nga, Krabi, Rayong, Chiang Mai, and Lamphun. In these 10 provinces, almost all saw an increase in permitted construction area, with only Chonburi and Nakhon Ratchasima experiencing decreases of 49.9% and 24.7%, respectively, compared to the same period last year (YoY) (details in Table 6).

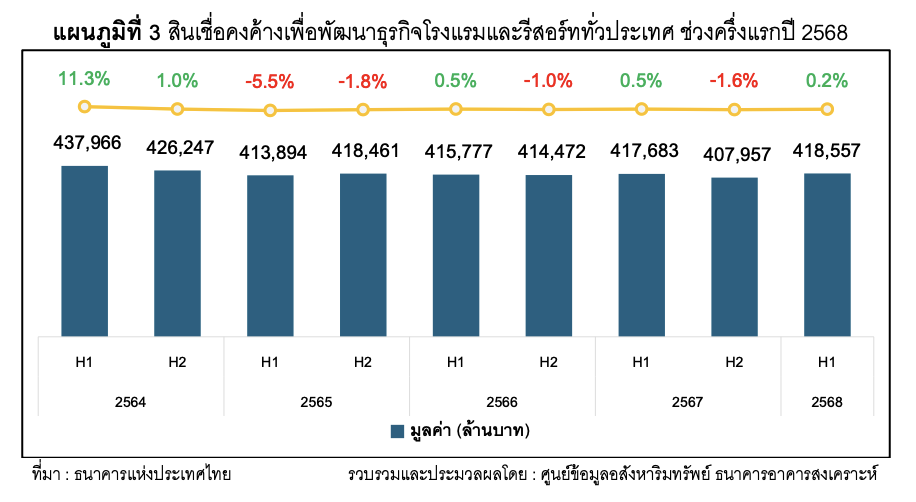

1.4 Outstanding Loans for Hotel and Resort Development

As of the first half of 2025, outstanding loans for hotel and resort development nationwide amounted to 418,557 million baht, a slight increase of 0.2% compared to the same period last year (YoY), which had a value of 417,683 million baht (details in Chart 3).

2. Demand Situation

2.1 Number of International Tourists Arriving in the Country

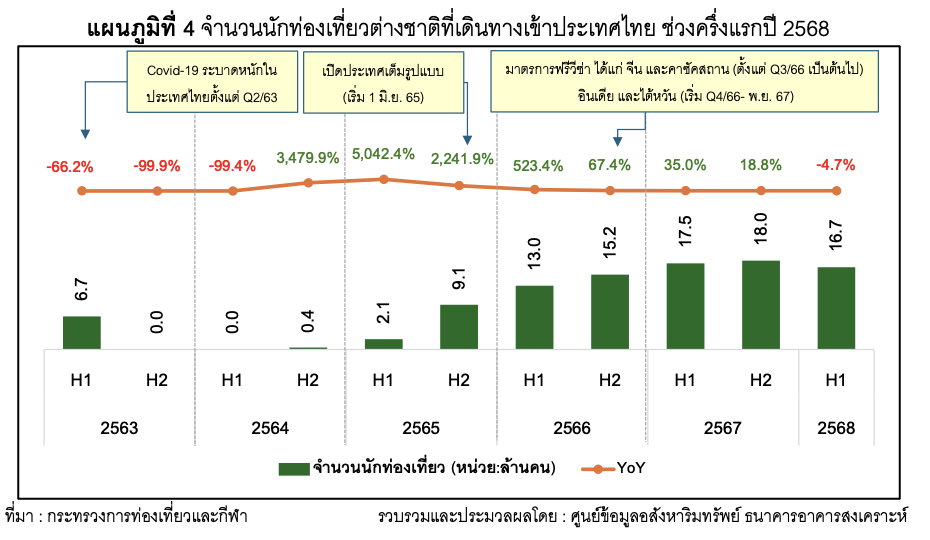

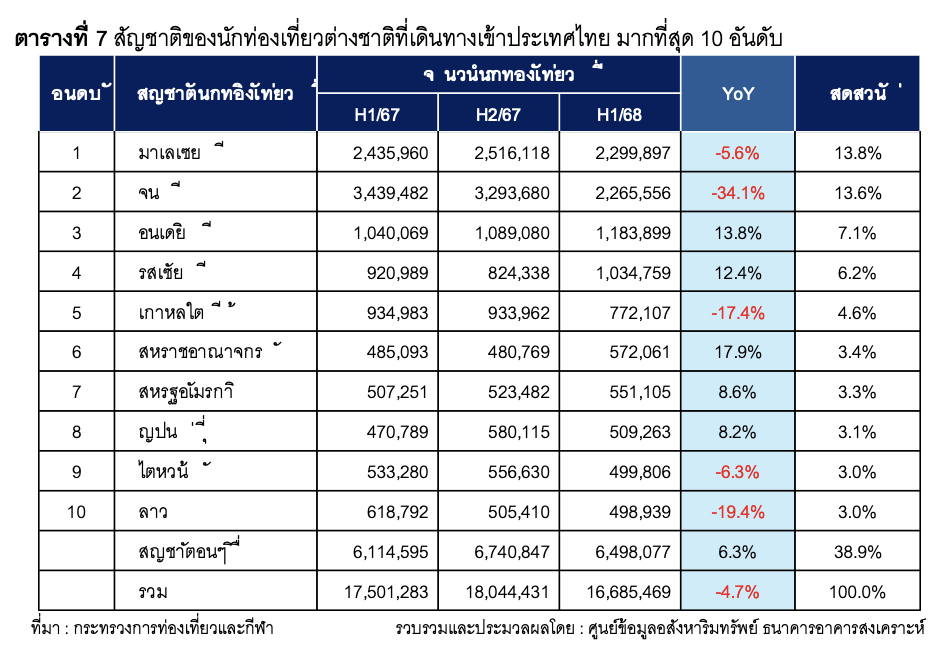

In the first half of 2025, the number of international tourists arriving in Thailand for various purposes other than work or study was 16,685,469, a decrease of 4.7% compared to the same period last year (YoY), which had 17,501,283 tourists. This decrease marks the first decline since the second half of 2021, primarily due to a significant 34.1% drop in Chinese tourists, who were previously the largest market for Thailand, resulting in China falling to second place behind Malaysia. Additionally, the number of tourists from Malaysia also decreased by 5.6%. The simultaneous decline of the two largest tourist groups has been a significant factor in the overall decrease in tourist numbers. However, there were some nationalities that saw an increase of over 10%, such as India (up 13.8%), Russia (up 12.4%), and the UK (up 17.9%), which may present opportunities and help the tourism and hotel sectors continue to grow. The top 10 nationalities of international tourists arriving in the first half of 2025 included Malaysia, China, India, Russia, South Korea, the UK, the USA, Japan, Taiwan, and Laos, collectively accounting for 61.1% (details in Chart 4 and Table 7).

2.2 Average Hotel Occupancy Rate

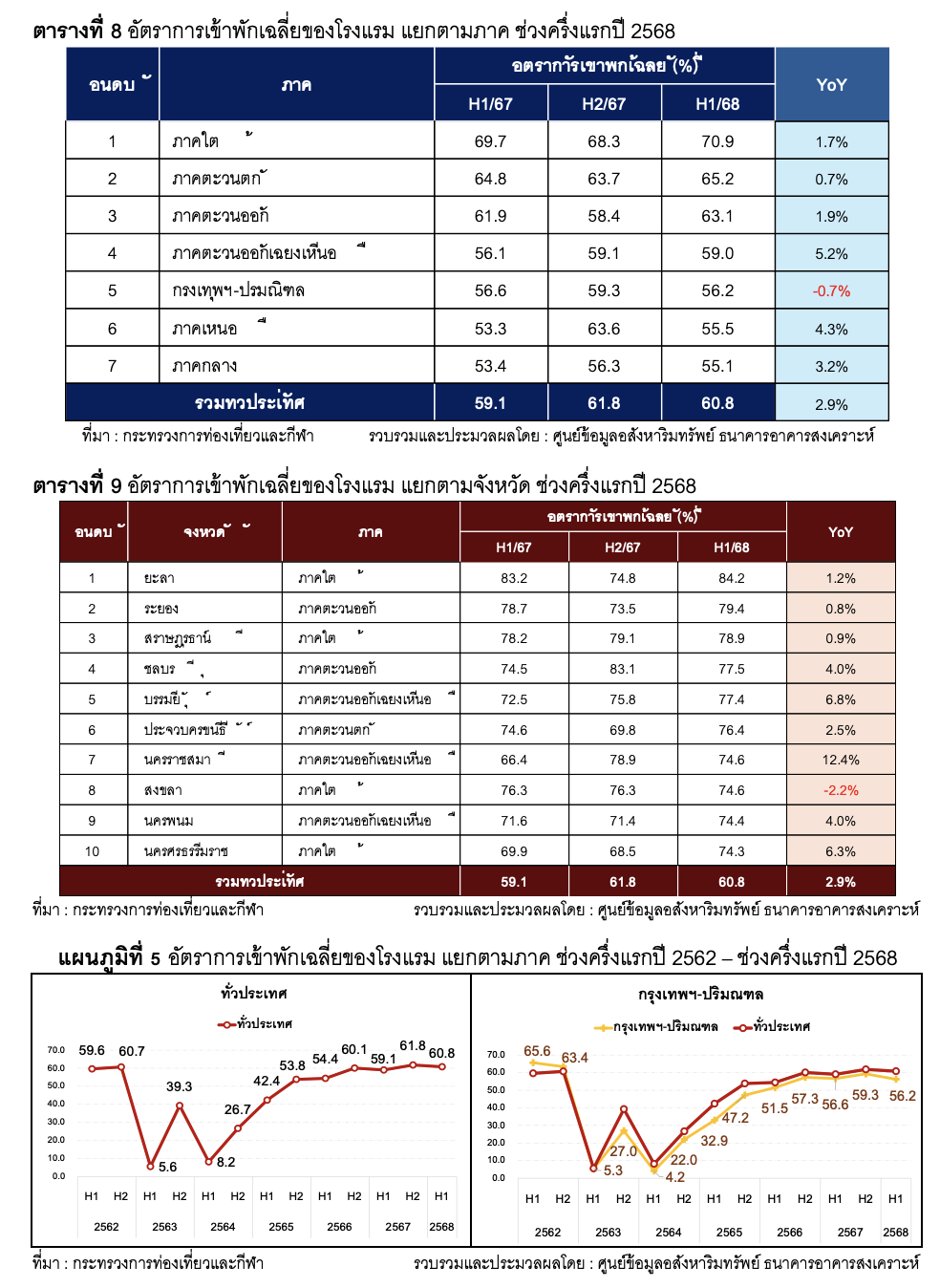

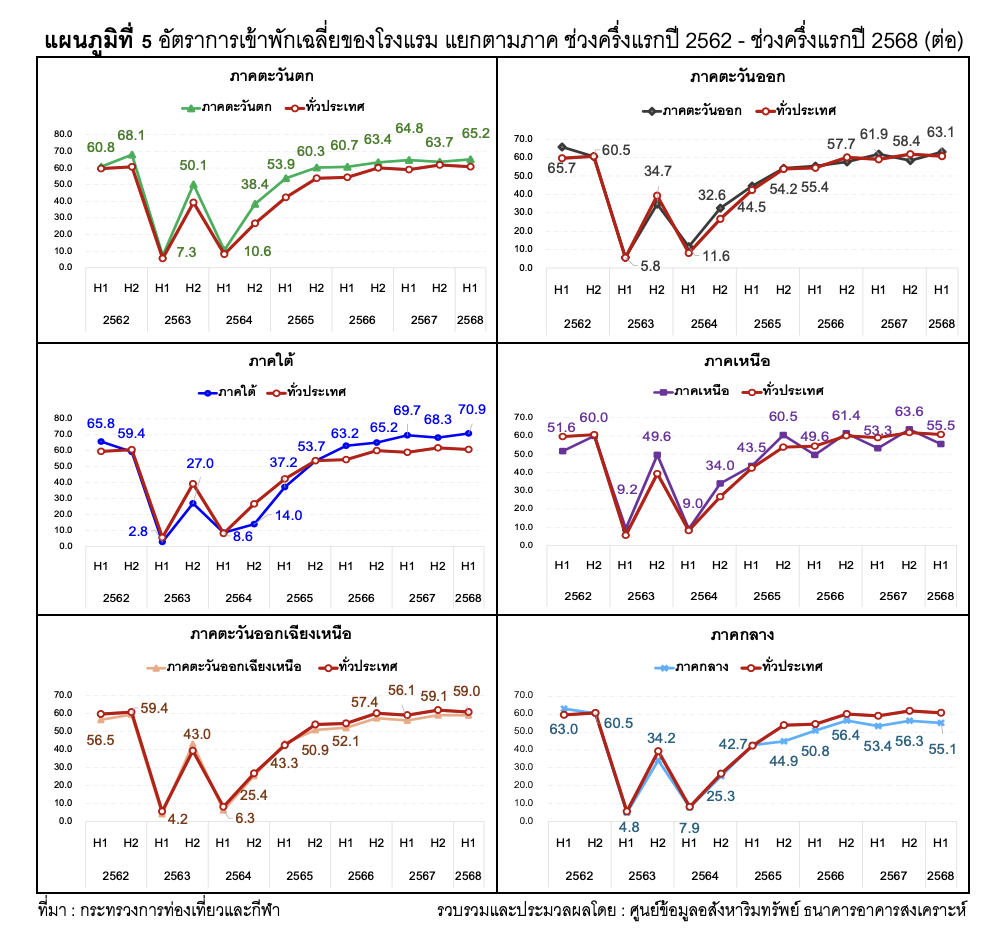

As of the first half of 2025, the average hotel occupancy rate nationwide was 60.8%, an increase compared to 59.1% in the same period last year (YoY). When analyzed by region, the southern region had the highest average occupancy rate at 70.9%, followed by the western region at 65.2%, the eastern region at 63.1%, the northeastern region at 59.0%, Bangkok and its surrounding areas at 56.2%, the northern region at 55.5%, and the central region at 55.1%. Almost all regions saw an increase in average occupancy rates; however, only Bangkok and its surrounding areas experienced a decrease of 0.7%, indicating that demand or the number of guests has decreased in contrast to the increasing number of available rooms in Bangkok and its surrounding areas, leading to heightened competition in the accommodation market and presenting a challenge for operators to plan and adjust strategies to cope with the risks of oversupply (details in Chart 5 and Tables 8 to 9).

Copyright Notice

The use or publication of any information contained in this report, whether in part or in whole, should reference the "Real Estate Information Center" as the source of the information.

Disclaimer

The statistical data and any writings in this report have been obtained from reliable sources or processed from reliable data. The Real Estate Information Center has verified the information to a certain extent but cannot guarantee its accuracy or truthfulness and cannot be held liable for any damages arising from the use of this information. Users of this information should exercise discretion and verify as appropriate.

For more information, please contact: Public Relations and Information Services, Real Estate Information Center

18th Floor, Building 2, Government Housing Bank Headquarters, 63 Rama 9 Road, Huai Khwang, Bangkok 10310

Phone: 0–2645–9675–6 Fax: 0–2643–1252