In 2025, Hotel and Accommodation Revenue Expected to Decline by 4.5% from the Previous Year

- The hotel and accommodation sector faces several negative factors. Kasikorn Research Center predicts that in 2025, revenue from the hotel and accommodation business will shrink by 4.5% compared to 2024, due to a decrease in room revenue following a decline in the number of tourists, lower average room rates, and reduced income from conferences and seminars.

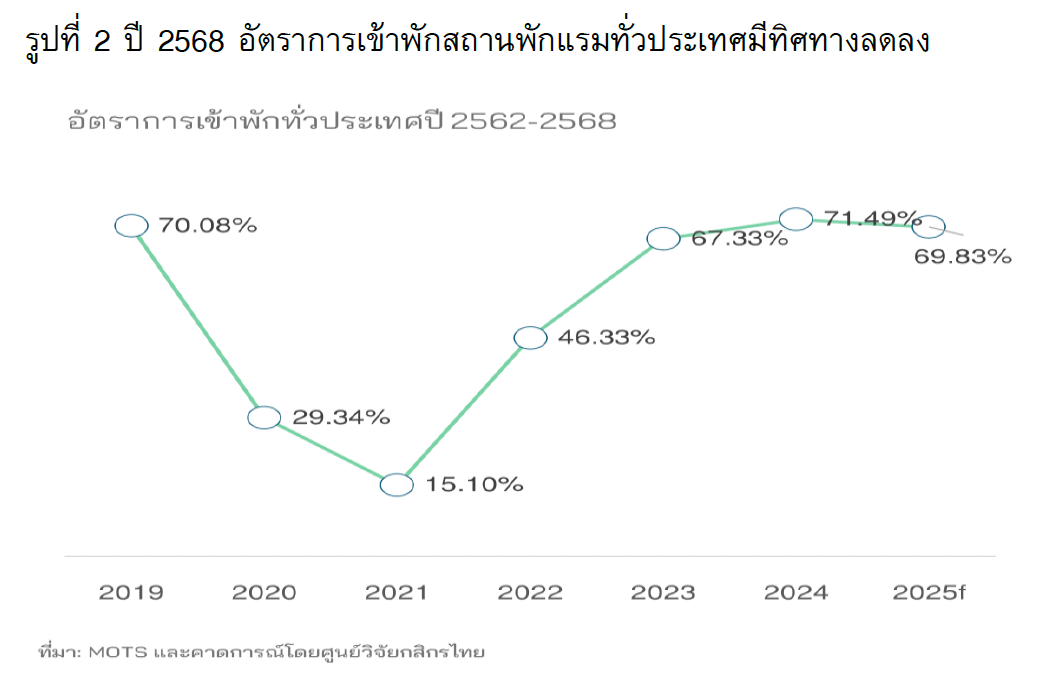

- Kasikorn Research Center estimates that the occupancy rate (Occupancy Rate: OCC) of accommodations nationwide will be around 69.83%, a decrease of 2.3% from 2024. Meanwhile, the average room rate (Average Daily Rate: ADR) is expected to drop by 4% from 2024, as operators continue to use pricing strategies to stimulate the market, impacting revenue from foreign tourists visiting Thailand.

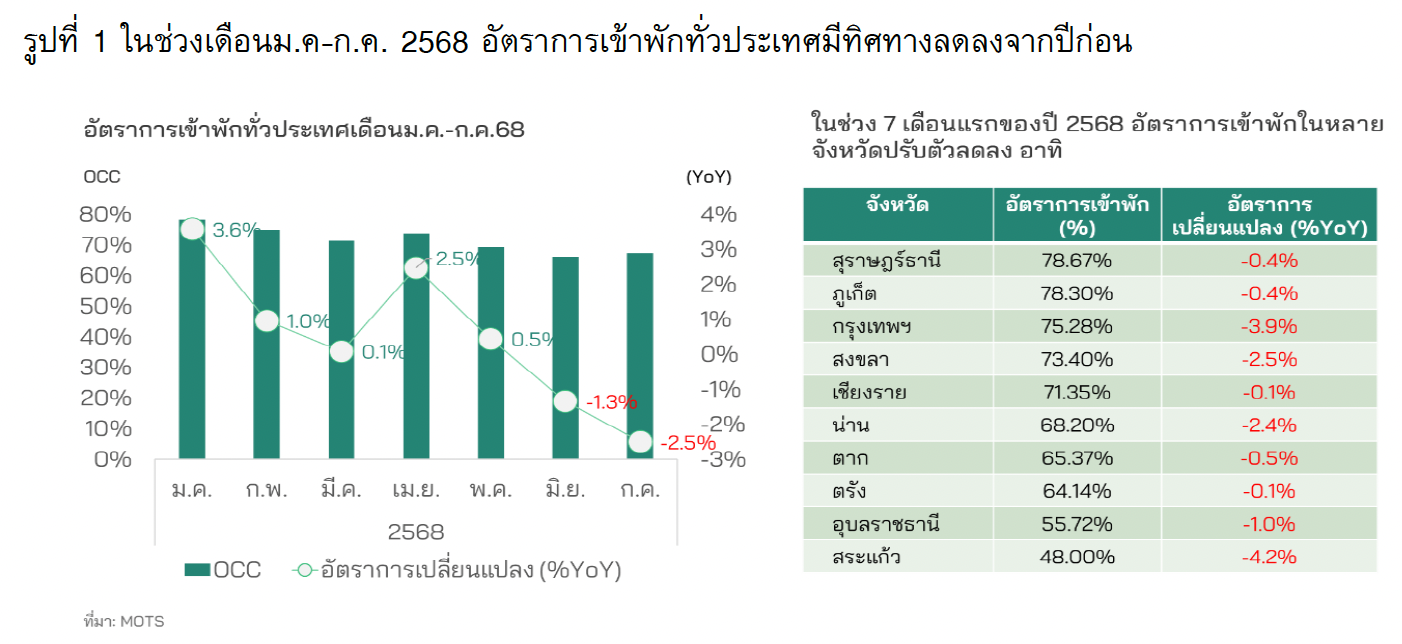

In the first 7 months of 2025, the hotel and accommodation business indicators reflect a downward trend. According to data from the Ministry of Tourism and Sports, the occupancy rate of accommodations nationwide from January to July 2025 was 71.66%, a decrease of 0.2% (YoY) (Figure 1).

The hotel and accommodation sector is facing several negative factors, such as a decline in the number of foreign tourists visiting Thailand, slower domestic travel growth among Thai citizens, flooding in the northern provinces, and the situation between Thailand and Cambodia.

In the remaining months of the year, although the sector may benefit from the "Half Price Thailand Travel" project, due to increasing negative factors in the hotel business, Kasikorn Research Center believes that in 2025, the revenue of the hotel and accommodation sector will decrease for the first time in 5 years, due to reduced revenue from occupancy rates and declining room rates, as well as decreased income from conferences and seminars.

- The occupancy rate of accommodations nationwide is expected to be around 69.83%, a decrease of 2.3% from 2024 (Figure 2). The main reason is that the number of foreign tourists visiting Thailand is expected to decline by 9% from the previous year, totaling 32.2 million people, along with a reduction in the average stay duration of foreign tourists.

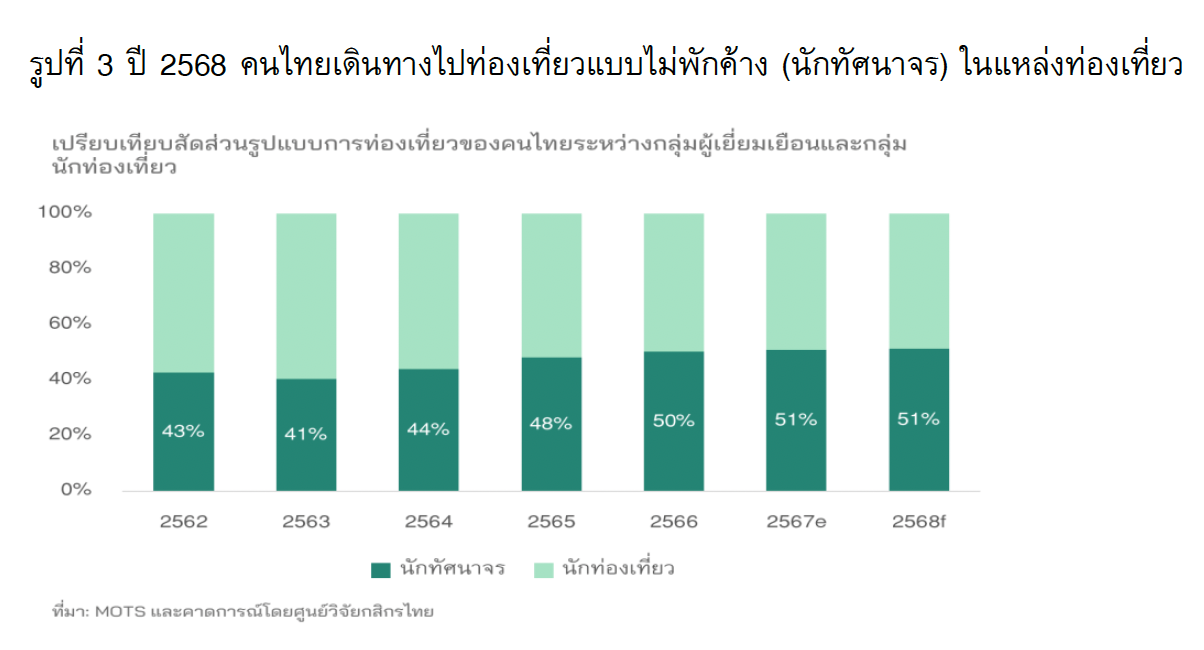

Although tourism is supported by an increase in domestic travel among Thai citizens, when considering travel patterns, it is found that more than half of Thai travelers are day-trippers or excursionists, a proportion that continues to increase (Figure 3).

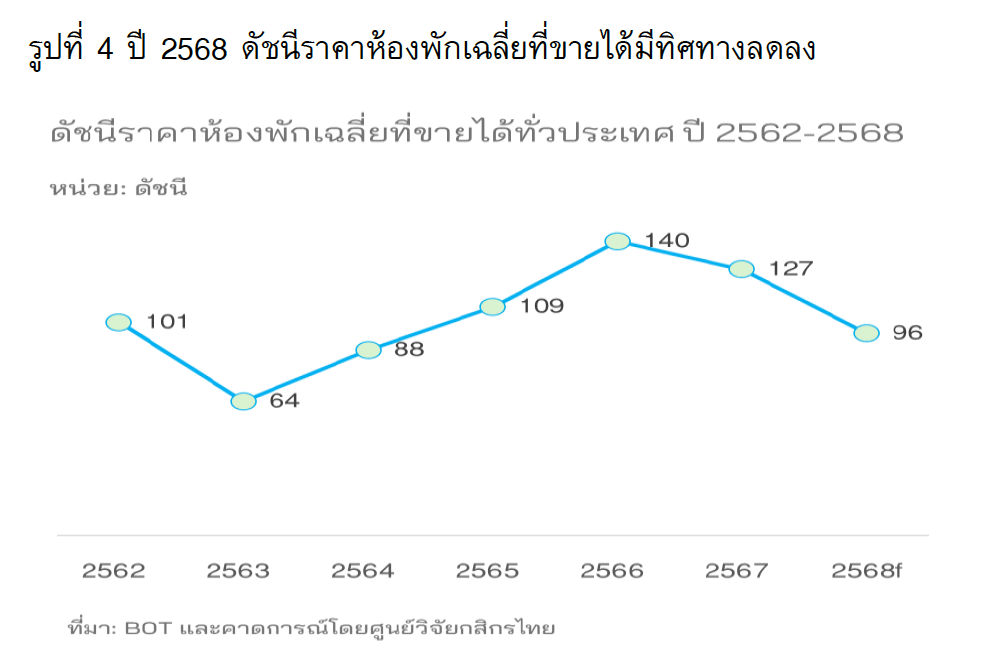

- The average room rate for the entire year of 2025 is expected to decrease by 4% from the previous year (Figure 4). In the first 7 months of 2025, the average room rate index decreased by 5%, as operators need to implement pricing strategies to attract customers due to decreased travel demand, while competition in the hotel and accommodation sector is high due to a large number of available rooms in the market. Most tourists prefer to stay in the midscale category, with an average room rate of 1,850 baht per night.

- Other revenues, such as organizing conferences/seminars for public and private organizations both domestically and internationally, have decreased. Additionally, the number of international events and concerts featuring world-class artists has also decreased compared to the previous year. According to TCEB data, in the first half of 2025, the number of conferences/seminars organized both domestically and internationally decreased by 13% (YoY).

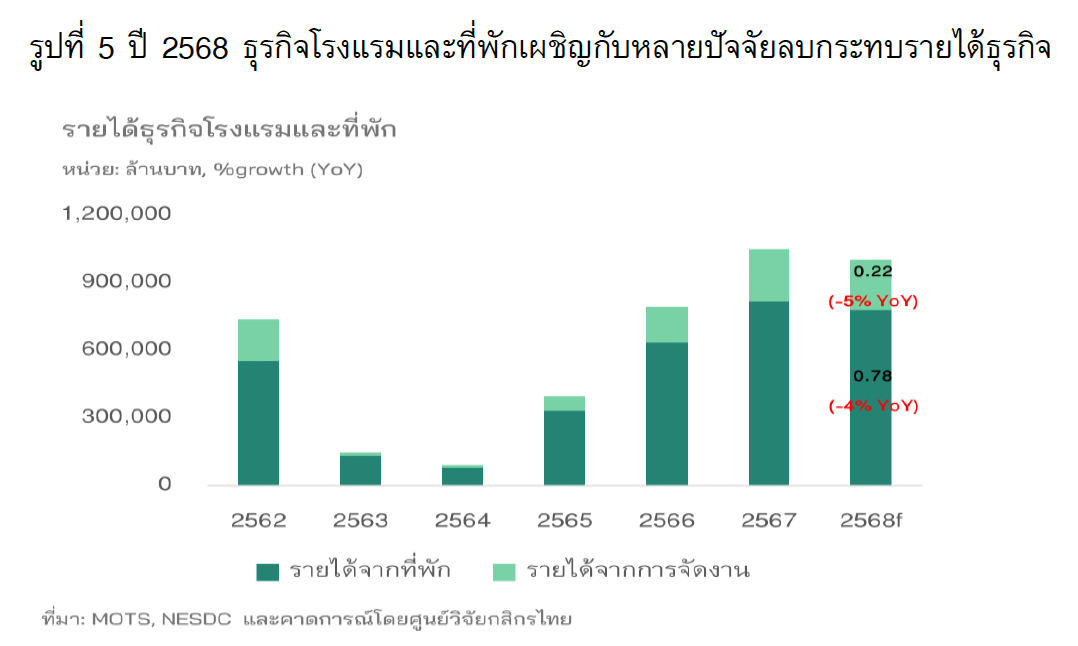

Given these factors, Kasikorn Research Center estimates that in 2025, the revenue of the hotel and accommodation sector will likely shrink by 4.5% from 2024, amounting to approximately 1 trillion baht, with declines in both accommodation revenue and other revenues (Figure 5). In the first 6 months of 2025, the overall revenue of the hotel and accommodation sector is expected to decrease by about 2.8%, and in the second half of the year, a continued downward trend is anticipated. The impact on operators will vary depending on location, accommodation type, competition, pricing strategies, and marketing strategies that meet customer needs.

For the remainder of this year, hotel and accommodation groups that need to be cautious include:

- Hotels and accommodations that heavily rely on foreign tourists, especially those from East Asia, which are mainly located in key tourist provinces such as Bangkok, Chonburi, Songkhla, and Chiang Mai. Additionally, these provinces have a high number of available rooms, leading to increased competition in these areas.

- Hotels and accommodations located near the Thailand-Cambodia border, such as Sa Kaeo and Ubon Ratchathani. However, for Trat province, which is a popular destination for foreign tourists in the last quarter, if the border situation remains stable, an increase in occupancy rates is expected.

However, provinces expected to continue seeing growth are mostly those that are popular domestic tourist destinations, such as Kanchanaburi, Phang Nga, Nakhon Si Thammarat, Nakhon Ratchasima, and Nakhon Phanom.

Kasikorn Research Center believes that moving forward, the hotel and accommodation sector will face high uncertainty, which will impact revenue and profits for operators, especially for medium and small-sized operators, as more than half of these operators have a debt-to-revenue ratio higher than the market average. (The average debt-to-revenue ratio in the market is approximately 3.5 times.) Meanwhile, revenue has not fully recovered.

- The risk of the number of foreign and Thai tourists may be lower than estimated, as the market still has risk factors to monitor, including the economic slowdown both domestically and internationally, geopolitical issues, and the border situation between Thailand and Cambodia, which may affect travel plans for both Thai and foreign tourists.

- High competition in the hotel business across all segments, especially in key tourist provinces with a high number of available rooms, such as Bangkok, Phuket, and Chonburi, which account for 40% of the total number of rooms nationwide. In 2025, the number of completed rooms in these provinces continues to increase, such as in Bangkok, where the number of rooms increased by approximately 3,000 rooms or 2% from the previous year, and in Phuket, where the number of rooms increased by approximately 1,500 rooms or 3% from the previous year. Particularly, upscale hotels will face greater challenges, as most newly completed hotels are in the upscale category, limiting pricing flexibility.

- Challenges in managing costs due to rising operational costs, such as increased labor costs, [1]. Currently, the tourism situation has not fully recovered, and intense competition limits the ability to pass costs onto customers, as labor costs in the hotel and accommodation sector average around 25%-30% of total costs (depending on the size and structure of the business).

The impact on hotels in different areas varies. The groups most affected are mainly in secondary tourist provinces, as the rate of increase in labor costs is expected to rise significantly more than in other provinces, averaging an increase of 14%-19% compared to wage rates in January 2025.

- The shift towards sustainable hotels is becoming increasingly necessary for the business, due to regulations and measures from authorities, customer demands, and competitors adapting to reduce environmental impacts and greenhouse gas emissions.

[1] On July 1, 2025, the government raised the minimum wage in the hotel and accommodation sector to 400 baht nationwide for hotels classified as 2 stars and above (2-star hotels are those that provide more than fifty rooms or hotels that provide rooms and dining services or facilities for food preparation. 3-star hotels provide rooms, dining services, or facilities for food preparation and meeting rooms. 4-star hotels provide rooms, dining services, or facilities for food preparation and meeting rooms.)