ASEAN+China 2025: Navigating Economic Strategies Amidst Global Tariff Storms

1. A Changing World with the Return of Trump 2.0 and Its Impact on ASEAN

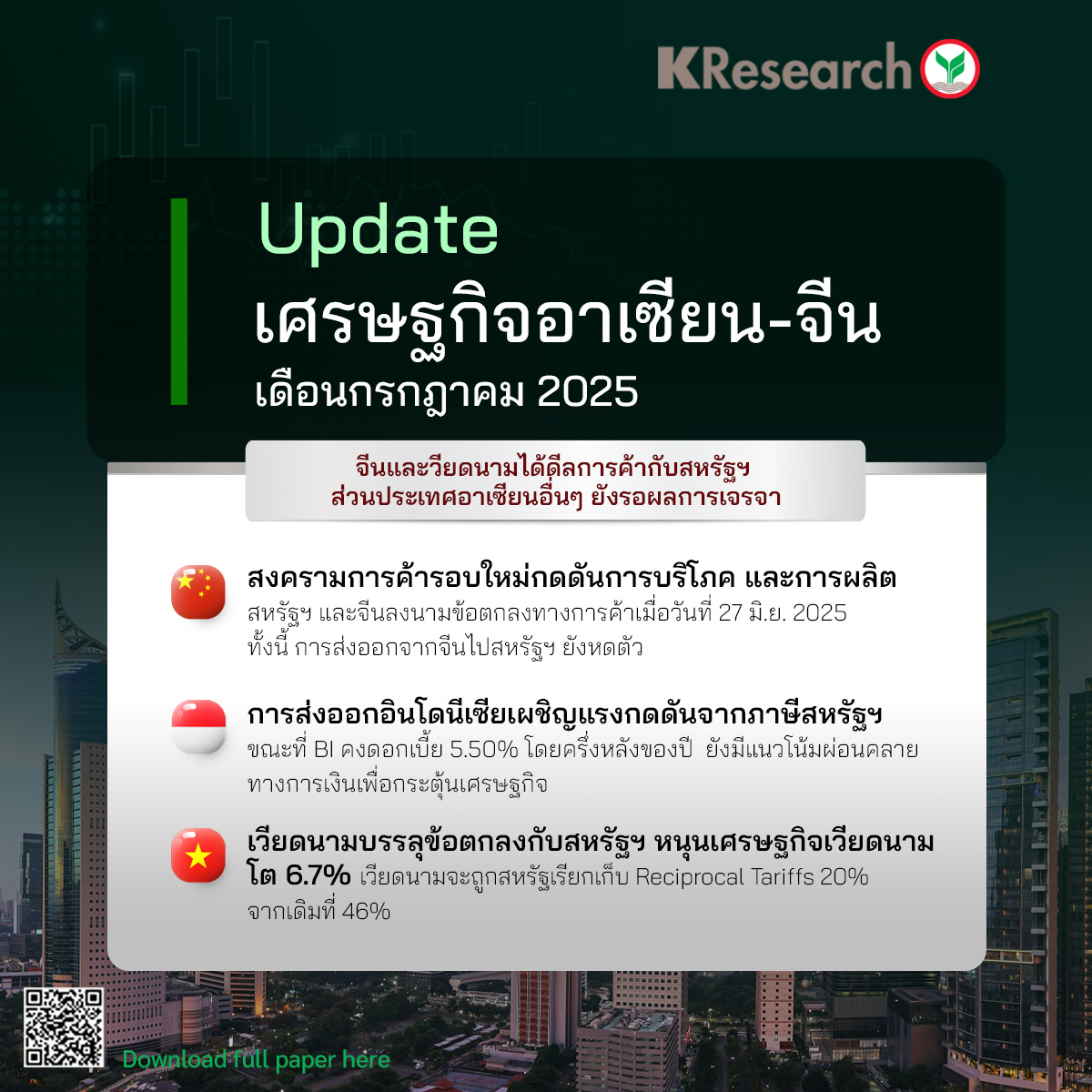

2025 marks a year of upheaval in global trade under the "Reciprocal Tariffs" policy of the U.S. government, which has expanded during the era of "Trump 2.0." This policy directly affects the Southeast Asian region, particularly ASEAN countries that have closely linked supply chains with China. ASEAN nations must expedite trade negotiations with the U.S. to mitigate the impact of tariffs. Vietnam, Indonesia, Malaysia, and Cambodia each have different stances in their negotiations. Vietnam has emerged as the first country to reach an agreement with the U.S., reducing the tariff rate from 46% to 20% and opening its market to the U.S. without imposing import duties.

Conversely, Thailand is still in negotiations, hoping to extend customs duty exemptions or negotiate new agreements to avoid significant damage to exports, which could substantially impact GDP.

2. Vietnam, Indonesia, Malaysia – The Three Pillars of ASEAN

Despite external pressures, some ASEAN countries have managed to turn challenges into opportunities.

Vietnam has not only reached an agreement with the U.S. but is also accelerating reforms in its public sector, aiming to develop an “International Financial Center” in both Ho Chi Minh City and Da Nang to attract investment through income tax and profit tax exemptions until 2030.

Indonesia has adopted a “second-best proposal” approach, offering to increase market access for U.S. energy products by up to $10 billion while expediting an agreement with the EU through the FTA (IEU-CEPA), which is expected to boost exports to Europe by over 50% within 3-4 years. Additionally, it has begun taxing e-commerce traders to balance the budget.

Malaysia is moving forward to protect its domestic industries through anti-dumping tariffs, particularly on steel and iron from China, Japan, India, and South Korea. Meanwhile, its relationship with the U.S. focuses on reducing tariffs and strategic negotiations to maintain its position in the global semiconductor supply chain.

3. Uncertainty in China and Its Ripple Effects on the Global Economy

Even though China and the U.S. signed a trade agreement at the end of June 2025, exports from China, particularly rare earths, shrank by 90%, reflecting pressures from a renewed trade war. Meanwhile, the domestic economy faces deflation, EV car prices are decreasing, and the real estate sector continues to contract.

Domestic consumption in China is still constrained by government spending cuts, impacting luxury goods businesses and the stock market. Although the “trade-in program” has helped boost sales of electrical appliances, it is insufficient to clearly revive the economy.

Conclusion: ASEAN at a Crossroads of Economic Change

In the latter half of 2025, the ASEAN region remains vulnerable to global trade shocks. The accelerated adaptation of AEC Plus countries, whether through FTA negotiations, domestic reforms, or seeking new economic partnerships, will be crucial in shaping the future direction.

ASEAN is transitioning from being a “low-cost producer” to a “strategic partner” in the new global era. Countries that dare to make decisive moves and act swiftly will have the opportunity to lead, while those that hesitate may miss the upcoming recovery wave.