The Global Fire Still Burns: Thailand Must Wake Up—On the Day the Global Economy Faces a Tax Storm

The world that once spun to the rhythm of free trade is now shaking with a new chapter in international political games—a game without gunfire, but filled with the thunderous sounds of taxes and economic retaliation measures that each country is wielding to test their power. In 2025, the global economy has reached a critical turning point that cannot be ignored.

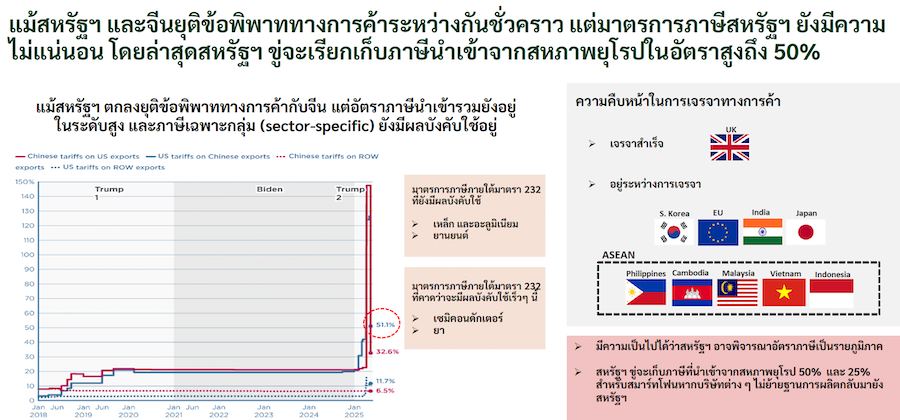

Under the shadow of a temporary ceasefire agreement between the United States and China lies a flickering flame of uncertainty that has yet to be extinguished. Recently, the Washington government announced plans to impose tariffs of up to 50% on imports from the European Union and 25% on smartphones unless manufacturers relocate their production to American soil. This announcement is not merely a political wave; it is a new shockwave that reverberates through global production lines.

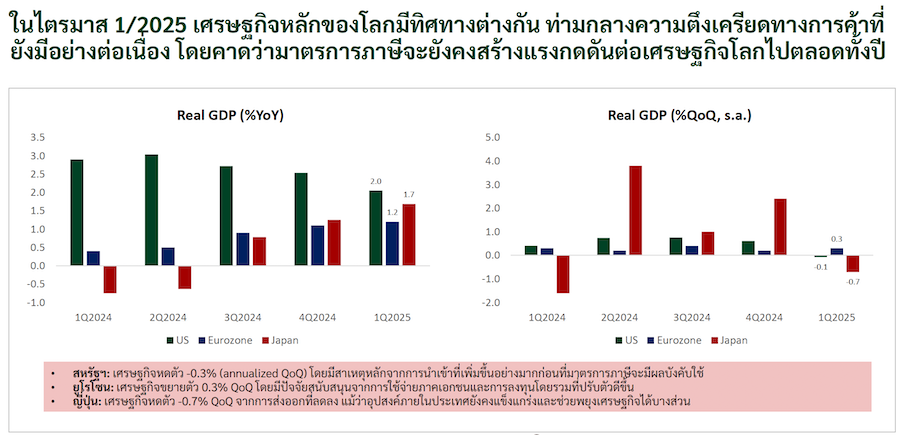

While the U.S. economy is clearly slowing down, with GDP figures dropping by -0.3% per quarter, the strength of the American labor market has not improved consumer confidence. Household spending has contracted, and consumer sentiment has declined. This has led to a shift in signals from the Federal Reserve, which is expected to cut interest rates twice in the latter half of the year to mitigate the impacts of tax pressures and stimulate economic activity.

On the other side of the world, Japan faces similar pressures, with its economy contracting by -0.7% per quarter. The bond market is shaken by yields reaching multi-year highs due to inflation concerns and soaring public debt. Financial instability is heavily weighing down the economic recovery of the Land of the Rising Sun.

As the global economy moves in a rough direction, Thailand cannot escape the ripples. Although the GDP figure for the first quarter of 2025 rose to 3.1%, which seems like a positive initial picture, a deeper analysis reveals that the main driving force came from accelerated exports before the U.S. tax measures took effect, rather than a true recovery of the domestic economy.

The Kasikorn Research Center (KResearch) predicts that Thailand's GDP for the entire year of 2025 may expand by only 1.4%, with a high risk of entering a "technical recession" if the U.S. fully implements a 36% tax measure. The export sector, which grew by 10.2% in April, may merely be an illusion created by preemptive shipments, with trends in May and June expected to slow down.

The trade deficit is beginning to widen due to imports of machinery and electronics from China, reflecting a regional production shift where Thailand has become more of a temporary stop than a long-term manufacturing base. The government is therefore hastening policy adjustments by increasing measures to control the origin of goods and suspending investment promotion in certain high-risk industries.

In contrast, Thailand's competitors in ASEAN, such as Vietnam and Indonesia, continue to show potential for industrial growth, causing Thailand to slowly lose its competitive edge, especially in sectors reliant on global supply chains.

Tourism, once a pillar of economic recovery post-COVID, now faces new headwinds. It is expected that the number of foreign tourists this year will drop to 34.5 million from the original target of 35.9 million, particularly concerning is the decline in tourists from China, which impacts service sector revenues in several provinces.

Overall, in terms of fiscal policy, the Thai government has chosen to shift from injecting money through the Digital Wallet project to investing in infrastructure instead. While this change in strategy appears more sustainable, in terms of short-term economic stimulation, it only contributes a mere 0.1% to GDP, reflecting the ongoing fiscal constraints tightening around the Thai government. The budget for 2026 is expected to grow by only 0.7%, while welfare expenditures remain a significant burden.

As the global economy enters an era of factionalism and tax wars, Thailand's strategy of relying solely on foreign markets is facing a turning point. The country must revitalize its internal economic structure, increase investments in new potential industries, and systematically strengthen the domestic market. Otherwise, this storm may not just pass through but could take root deep within the Thai economy.