Bangkok and Phuket Hotel Market Outlook for the Second Half of 2024

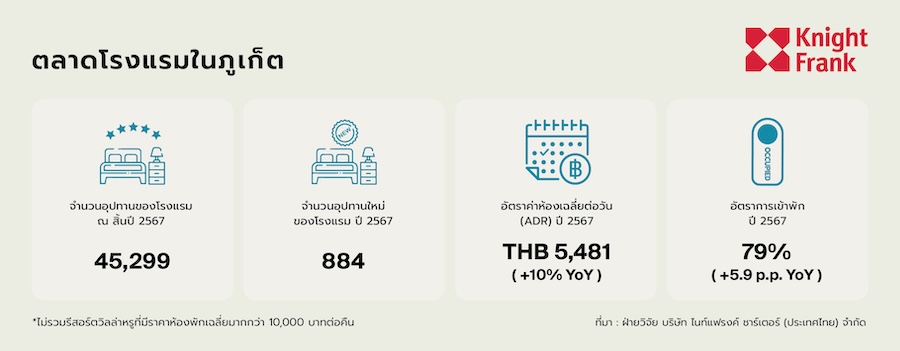

Market Overview The hotel sector in Thailand continues to grow robustly in 2024, with Bangkok and Phuket achieving an average occupancy rate of 79%. The average daily rate (ADR) reached a record high of 4,241 THB in Bangkok (+7.4% YoY) and 5,481 THB in Phuket (+10% YoY), driven by a significant increase in foreign tourists, particularly from China, Russia, and India. Additionally, visa exemption policies and the expansion of international flight routes have stimulated travel demand. Bangkok continues to see growth in the mid to upper-tier hotel segment, while Phuket is evolving into a premium lifestyle market. In 2025, it is expected that the ADR will grow at a slower pace, but occupancy rates will remain strong at around 80%, supported by the recovery of tourism and investor confidence.

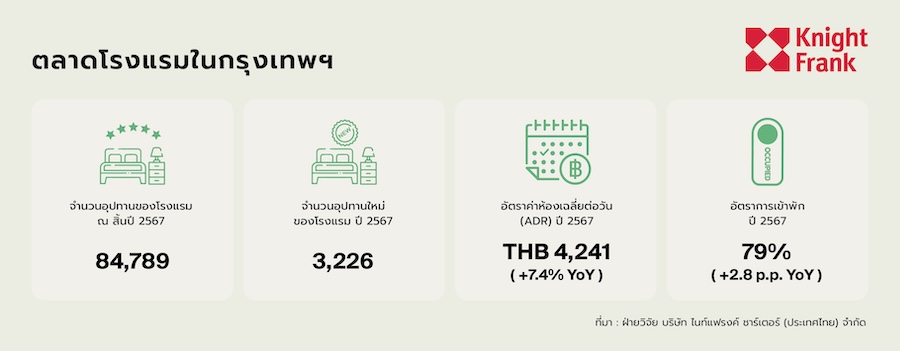

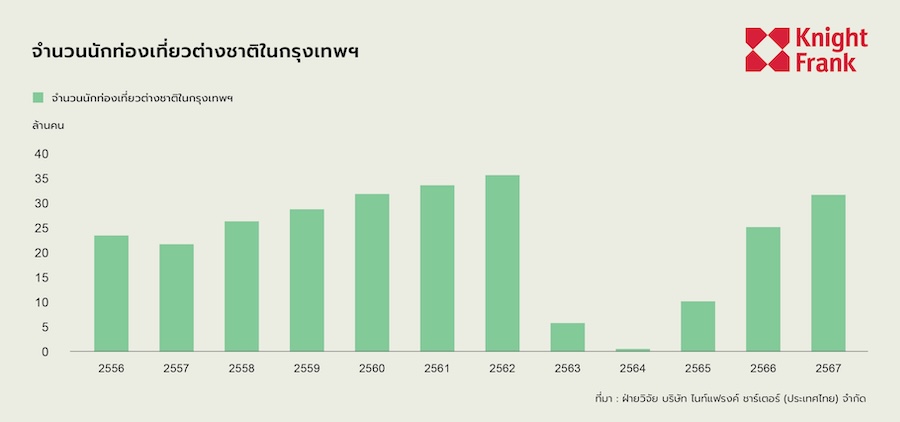

Bangkok Hotel Market Overview In 2024, Bangkok's tourism industry continues to recover strongly, a trend that began in late 2022. The number of foreign tourists grew by 27% YoY, totaling 31.6 million, although still 11% below pre-pandemic levels. Conversely, domestic travel saw only a slight increase of 3% YoY to 14.8 million, which is still 17% below pre-pandemic levels. The increase in foreign tourists has pushed hotel occupancy rates up by 2.8 percentage points, while the average room rate has risen by 7.4% YoY, reaching an all-time high.

The primary tourist market remains Asia, accounting for 73% of all foreign tourists. China leads the market with a staggering growth rate of 91% YoY, totaling 6.73 million (19% of all tourists), followed by Malaysia (14%), India (6.0%), and South Korea (5.3%). Europe is the second-largest source of tourists, making up 21% of the total, with Russia being the primary market (4.9%), followed by the UK (2.7%), Germany (2.5%), and France (2.0%). The continued strength of these markets supports the hotel sector in Bangkok, resulting in increased occupancy rates and record-high room rates.

Key supporting factors include government tourism stimulus measures, such as the extension of visa exemptions starting July 2024, allowing citizens from 93 countries to stay in Thailand for up to 60 days. Additionally, the introduction of the new Destination Thailand Visa (DTV), a multi-year (5-year) visa for remote workers and digital nomads, allows stays of up to 180 days at a time.

Demand and Supply The hotel business in Bangkok performed strongly in 2024, with occupancy rates increasing to 79%, up 2.8 percentage points from the previous year. Occupancy rates grew consistently throughout the year, with February and December reaching peaks of 84%, surpassing the figures from 2023 of 74% and 82%, respectively. Even September, typically a low tourist month, improved from 73% in 2023 to 75% in 2024, reflecting the strength of the tourism sector driven by the increase in foreign tourists.

The average daily rate (ADR) also grew significantly, rising from 3,948 THB in 2023 to a record high of 4,241 THB in 2024, leading to a continuous increase in the average revenue per available room (RevPAR) across hotels in Bangkok. Although there was a slight slowdown at the beginning of the year (January), February managed to achieve a record high of 4,567 THB, aligning with the tourist season. The mid-year period, typically a low season, still saw moderate growth, while December marked the highest growth month, increasing by 17% YoY, driven by the tourist season and increased spending by travelers.

In terms of supply, Bangkok saw the addition of 15 new hotels in 2024, contributing 3,226 new rooms, bringing the total number of rooms to 84,789. The new hotels span all price ranges, from budget hotels like Holiday Inn Express Bangkok Central Pier to luxury projects like Dusit Central Park, The Ritz-Carlton, and Grande Centre Point Lumpini. Most new developments focus on the upper-midscale and upscale hotel segments, led by well-known brands such as Moxy, Mercure, Hilton Garden Inn, and The StandardX.

High-growth areas include the Silom-Sathorn district, which remains a business and tourism hub, the expanding Lumpini-Siam area, and the Riverside area, which is popular in the upscale hotel market, with new hotels like Hilton Garden Inn and Glow Bangkok Riverside enhancing the appeal of the riverside location.

International hotel brands such as Marriott, Accor, Hilton, and IHG continue to be major players in the market, while Thai brands like Dusit and Grande Centre Point remain competitive. The development of large projects reflects investor confidence in the Bangkok hotel market, with large new hotels like Moxy Ratchaprasong (532 rooms) and Grande Centre Point Lumpini (512 rooms) showcasing the trend towards higher room counts in potential locations.

Additionally, small boutique hotels like The StandardX (62 rooms) and Lumen Udomsuk (102 rooms) are targeting tourists seeking unique experiences. Another significant trend is investment from Asian operators, particularly from Japan, as seen with the launch of Sotetsu Grand Fresa Bangkok (126 rooms), reflecting Japanese investors' interest in the Bangkok hotel market. Meanwhile, Thai operators like Cross Hotels (Lumen Bangkok Udomsuk Station) and Baiyoke Group (Queensland Hotel Bangkok) continue to expand their businesses, increasing diversity and promoting competition in the mid to upper-midscale market.

Bangkok Hotel Market Trends In 2025, Thailand aims to attract 36-40 million foreign tourists, building on the recovery trend that began in 2022. Key supporting factors include extended visa exemption policies, the recovery of the aviation sector, and the opening of new international flight routes, which will help maintain Bangkok's status as a global tourism hub.

However, the hotel industry faces negative factors in early 2025, such as travel warnings and negative news, for example, Taiwan's high-risk ranking, which may impact the number of tourists from China and neighboring countries. Nevertheless, strong demand is expected to continue supporting hotel occupancy rates at high levels, with expanded flight routes and government policies favoring tourism helping to sustain growth in the tourism sector throughout the year.

The Bangkok hotel market remains on a steady growth trajectory following the recovery from COVID-19. Although the rapid increase in average daily rates (ADR) between 2022-2023 is expected to slow down, it is anticipated that room rates will continue to rise in line with global hotel industry trends. As the number of foreign tourists approaches pre-pandemic levels, competition will intensify with the opening of new hotels. It is expected that Bangkok's ADR will stabilize between 4,250-4,450 THB, with luxury hotels likely to continue growing. Notably, luxury hotel rates in Bangkok have increased by 43% since 2019 but still remain lower than those in Singapore and London, which are 2-3 times higher, indicating significant growth potential for Bangkok in the luxury hotel market.

In 2025, average revenue per available room (RevPAR) will be driven by occupancy rates, particularly from the recovery of foreign tourists, with the Chinese market remaining a key factor. Although the number of travelers from China is still 40% below pre-pandemic levels, the travel behavior of Chinese tourists is changing, with a shift towards smaller, independent travel rather than large group tours, which may impact mid-range hotels that previously relied on traditional tour markets.

Emerging markets such as India and the Middle East are playing an increasingly important role in Bangkok's tourism sector. However, the spending behavior of tourists from these regions varies, necessitating hotel operators to adjust strategies to specifically attract these tourists. Meeting the demands of these high-growth markets will be crucial for maintaining revenue per available room (RevPAR) across all hotel segments.

Overall, occupancy rates are expected to stabilize at around 80%, with peak seasons like February and December potentially exceeding 84%. Meanwhile, mid-year performance will depend on regional travel trends and overall economic conditions. The Chao Phraya riverside area, home to many luxury hotels in Bangkok, is likely to continue experiencing strong demand, supporting overall market stability.

Hotel supply is expected to continue growing, with nearly 4,000 new rooms anticipated to enter the central Bangkok market by 2025, representing a 4.7% increase in total room count. The ongoing increase in supply reflects investor confidence in Bangkok's hotel sector, as well as long-term growth potential.

In the future, strong international travel demand and an increasing number of tourists will continue to drive growth in Bangkok's hotel market. Although the growth of average daily rates (ADR) is beginning to slow, luxury market hotels are still expected to grow. Over the past two years, the gap in room rates between high and low seasons has narrowed as hotels have improved their revenue management strategies. However, this trend may be temporary, and it remains uncertain whether it will persist in the long term.

With various favorable factors such as a tourism-friendly economy, the expansion of international flight routes, and supportive government policies like visa exemptions, Bangkok's hotel business is likely to continue growing and remain strong in 2025 and beyond.

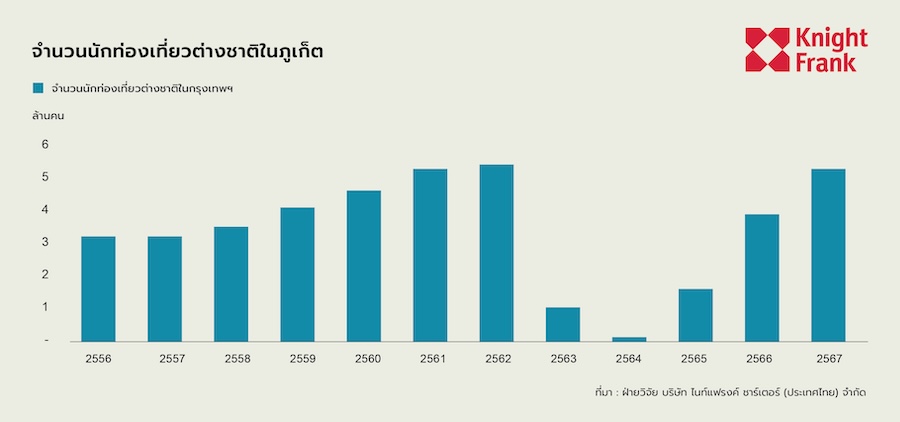

Phuket Hotel Market Overview In 2024, Phuket welcomed 8.6 million foreign tourists, still 4.7% below pre-pandemic levels. However, the recovery pattern varies among tourist groups, with foreign tourists increasing to 5.3 million, a growth of 37% compared to the previous year, bringing this segment back to near pre-COVID-19 levels, reflecting Phuket's appeal as a world-class resort destination that continues to attract foreign travelers strongly. Conversely, the number of Thai tourists totaled 3.3 million, growing only 6% YoY and still 11% below pre-COVID-19 levels.

In terms of the foreign tourist market, Russia is the leading market with the highest number of tourists at 1.1 million, an increase of 26% YoY, followed by China with 1.0 million (growing 76% YoY), India with 0.5 million (growing 58% YoY), Australia with 0.3 million (down 4% YoY), and the UK with 0.3 million (growing 37% YoY).

Phuket's tourism market in 2024 continues to move towards full recovery, supported by the growth of Russian, Chinese, and Indian tourists, who together account for 45% of all foreign tourists. The Thai government plays a crucial role in stimulating the market with visa exemption measures that began in late 2023. However, China, which was once Phuket's largest foreign market, still only saw 1.0 million tourists in 2024, far from the peak of 3.0 million before the pandemic.

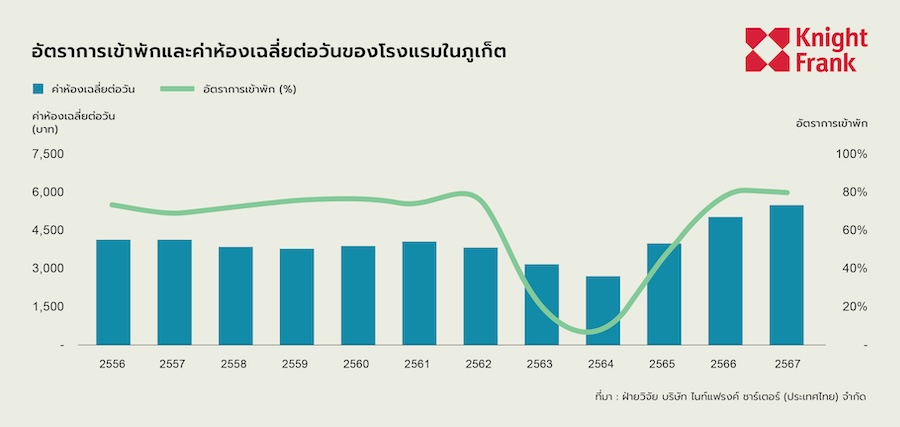

Demand and Supply The hotel market in Phuket rebounded strongly in 2024, with average occupancy rates increasing to 79% from 73% in 2023. During the high season (January-April), occupancy peaked at 84%, while November and December also performed strongly at 81% and 91%, respectively. Even during the low season (July-September), occupancy remained strong above 75%.

The average room rate (ARR) reached a record high of 5,481 THB, up 10% YoY, primarily driven by the luxury and upscale hotel segments that can still command high prices, while mid-range and budget hotels experienced slower growth, reflecting a clearer market segmentation.

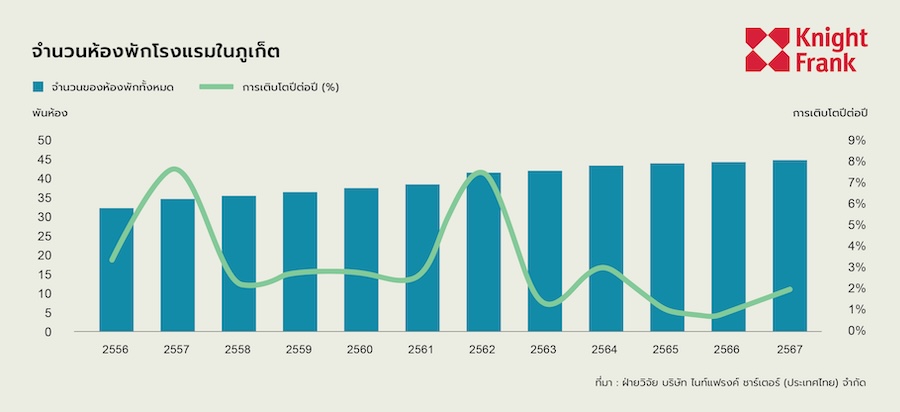

In 2024, the supply of new hotels remained limited, with only three new hotels opening: Radisson Red Phuket Patong Beach (390 rooms, upscale), Homa Phuket Cherngtalay (423 rooms, midscale), and Blue Monkey Hub (71 rooms, midscale), adding only 884 new rooms, bringing the total number of rooms in Phuket to 45,299.

Looking ahead, the Phuket hotel market is expected to continue growing, with 18 new hotels set to open in the next two years, adding over 4,100 rooms, representing a 9.1% growth in supply, reflecting investor confidence in Phuket's long-term potential. The launch of new projects, particularly in the luxury and upper-upscale segments, is expected to elevate service standards in Phuket's hotel industry and meet the increasing demand from foreign tourists.

Phuket Hotel Market Trends

Phuket's tourism sector is on a strong recovery path, with international flight volumes increasing by 33% YoY, although still 12% below pre-pandemic levels. This recovery is expected to accelerate in 2025, driven by the expansion of international flight routes, visa exemption measures for key markets like China, Russia, and India, as well as the opening of new flight routes, which will stimulate the influx of foreign tourists and strengthen Phuket's status as a global destination.

Phuket is transforming its image from a traditional luxury destination to a more diverse premium lifestyle market, with areas like Bang Tao and Kamala becoming the center of this transformation, featuring high-end development projects that enhance Phuket's appeal to high-spending tourists and long-term investors.

Despite the positive trends, challenges remain, particularly negative news and travel warnings, such as Taiwan's high-risk classification for Thailand, which impacts the country's image in some Asian markets and may slow travel from Chinese and neighboring tourists in early 2025. However, overall demand remains strong, and occupancy rates are expected to stay high, especially during the high season.

After high growth rates over the past two years, the increase in average room rates (ARR) is expected to slow as inflation stabilizes. In 2025, revenue per available room (RevPAR) is likely to be driven by increased occupancy rates rather than significant price hikes, aligning with global trends toward revenue stabilization following the pandemic recovery.

One significant change in the Phuket hotel market is the lifting of the 80-meter height restriction for buildings, which will open opportunities for luxury hotel and residential developments in higher locations. In the next two years, over 4,100 new rooms are expected to enter the market in the luxury and upper-upscale hotel segments, reflecting strong investor confidence in Phuket's long-term potential.

Leading global hotel brands such as JW Marriott, Ritz-Carlton, Wyndham Grand, and Riu Palace are enhancing Phuket's high-end service capabilities. At the same time, international hotel chains like Marriott, Accor, Radisson, and Wyndham are expanding their investments, while Thai operators like Chatrium and Centara are increasing their roles in the upscale market.

The landscape of the Phuket hotel market is changing from the dynamics of sub-markets developing in new directions, with the southeastern region of Phuket, particularly Chalong Bay and Maikhao Bay, becoming a luxury tourism destination attracting high-end travelers, while Mai Khao and Bang Tao are popular among large all-inclusive resorts due to their proximity to the airport and beautiful beaches. Patong and Rawai are gaining attention from lifestyle development projects, featuring brands focused on design and targeting younger travelers, such as Tribe and W Hotels.

At the same time, the demand for quality mid-range accommodations at accessible prices is increasing, leading to the expansion of midscale brands like ibis Styles, Tribe, and Courtyard by Marriott. Additionally, European operators such as Riu, Meliá, Mövenpick, and ibis Styles are increasing their investments in Phuket, reflecting ongoing confidence in the long-term potential of the market.

Looking ahead, the Phuket hotel market is well-positioned for continued growth, driven by increasing demand from a more diverse foreign market, the expansion of premium lifestyle and luxury segments, and supportive government policies through visa exemptions and infrastructure development. However, the full recovery of Chinese tourist numbers remains a key factor to watch, depending on geopolitical developments and economic conditions in the region. If trends remain positive, occupancy rates are expected to stabilize at around 80%, potentially exceeding 85% during peak seasons.

In summary, the Phuket hotel sector is expected to grow steadily in 2025, driven by the development of high-end projects, the increase in international flights, and changing traveler demands. These factors are positive signs for Phuket's long-term potential, which will continue to be a strong-growing global destination.