Industrial Market in the Second Half of 2024

Market OverviewThe Thai economy continues to grow in the third quarter of 2024 with the highest growth rate of 3.0% (year-on-year) The key factors are strong exports and accelerated public investment disbursement, which supports the construction sector.

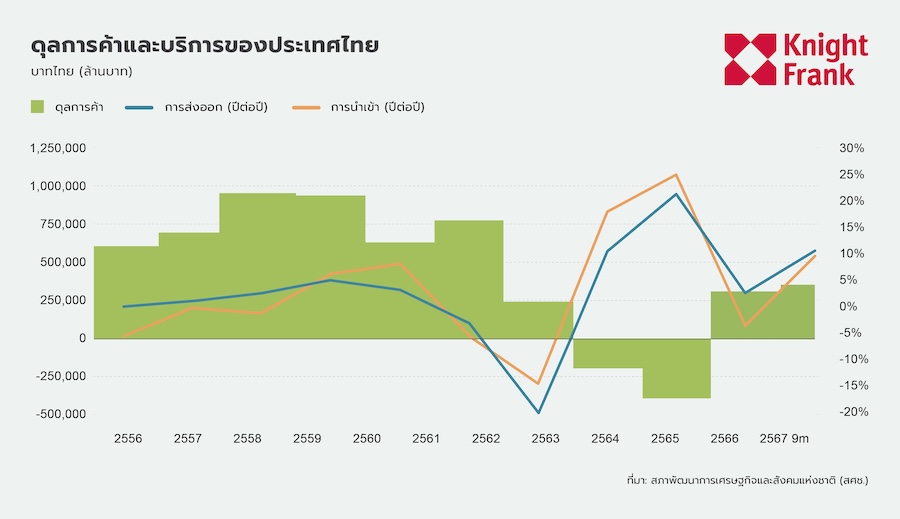

In the first 9 months of 2024, Thailand maintained a trade surplus, with exports of goods and services growing by 10.6% outpacing imports, which grew by 9.8% Meanwhile, private consumption expanded by only 1.7% due to tighter credit conditions, delayed consumer spending decisions, and a decline in durable goods spending, particularly in the automotive sector, which contracted significantly due to price competition from EVs. At the same time, public spending increased by 1.6% due to economic stimulus measures such as the 10,000 baht cash handout program phase 1 and an increase in employee compensation by 1.1% while investment in fixed assets decreased by 1.7% due to reduced investment in the automotive industry and private construction, reflecting credit constraints and weakened business confidence.

Inflationary pressures in Thailand remain low in the second half of 2024 with an average general inflation rate of 0.6% primarily due to lower energy costs, such as electricity and fuel prices, as well as reduced food prices from improved domestic supply conditions. Additionally, government measures to subsidize diesel and electricity prices play a crucial role in maintaining the cost of living for households and businesses. However, core inflation continues to rise slightly due to increasing costs in certain non-food categories, reflecting structural cost pressures. Thailand's inflation rate in the second half of the year is considered the lowest in the region, reflecting the country's stability amid global economic uncertainties.

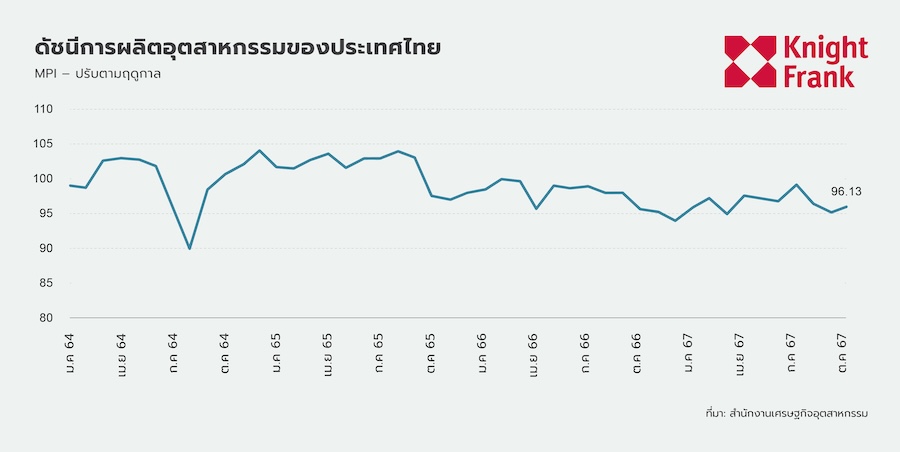

In October 2024, Thailand's seasonally adjusted Manufacturing Production Index (MPI) remained stable at 96% indicating a recovery in the manufacturing sector, although it still faces challenges such as weak domestic purchasing power and increased imports of cheap goods from abroad, which have shifted consumer behavior towards imported products over domestic ones. Furthermore, the tightening of credit approvals has impacted key industries such as automotive, leading to significant contractions in the production of pickup trucks, small cars, and hybrid vehicles.

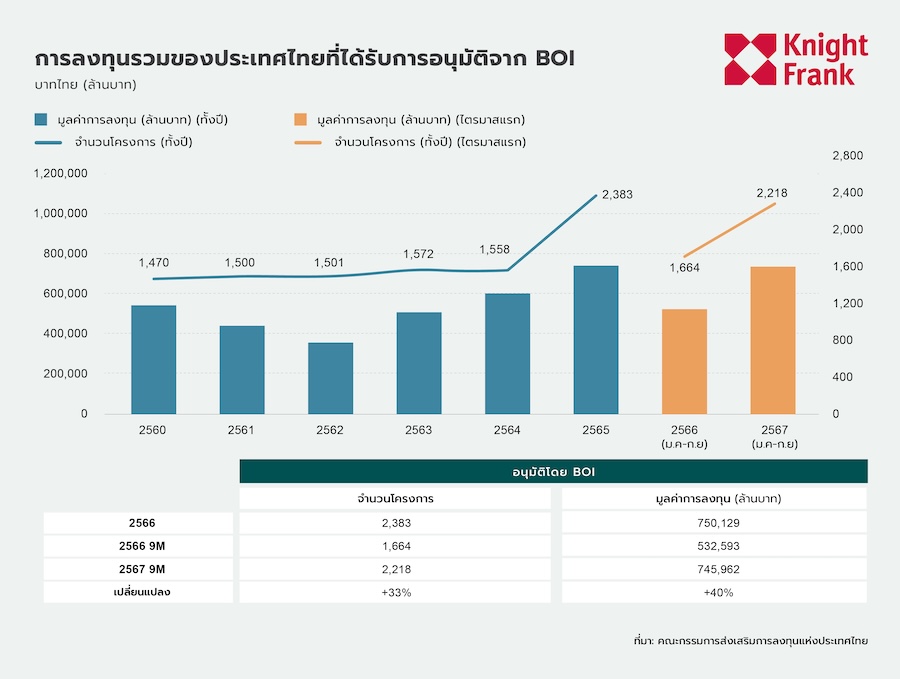

According to a report from the BOI the number of both Thai and foreign investors applying for investment promotion from January to September 2024 increased by 33% with 2,218 approved projects compared to the previous year, and the total investment value increased by 40% to 745,962 million baht, up from 532,593 million baht last year. Foreign direct investment (FDI) is a key driver of this growth, with 1,420 foreign projects valued at 546,680 million baht, with the highest investment sectors being electronics and electrical appliances, accounting for over a quarter of the total approved investment value.

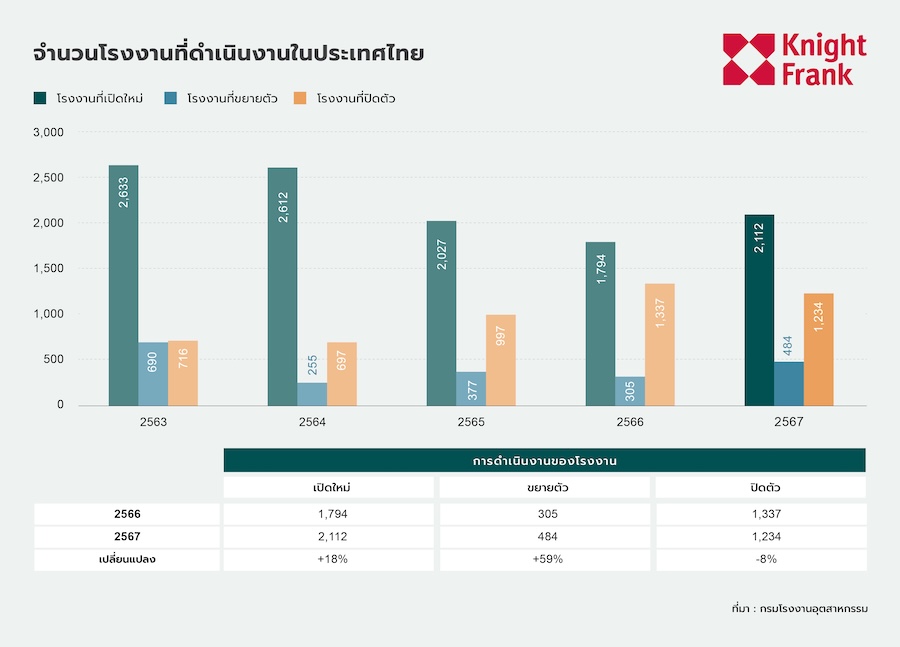

The operational sector of factories in Thailand shows clear signs of recovery in 2024 compared to 2023 with a significant increase of 59% in the number of factories expanding operations to 484 projects, reflecting increased confidence in Thailand's industrial sector, while new factory startups also continued to grow, increasing by 18% compared to the previous year to 2,112 locations, while the number of factory closures decreased by 8% to 1,234 locations. Although the industrial sector is still in recovery and has not returned to pre-COVID-19 levels, the significant increase in factory expansion projects indicates a strong recovery in industrial investment and a positive trend in Thailand's manufacturing sector.

Serviced Industrial Land

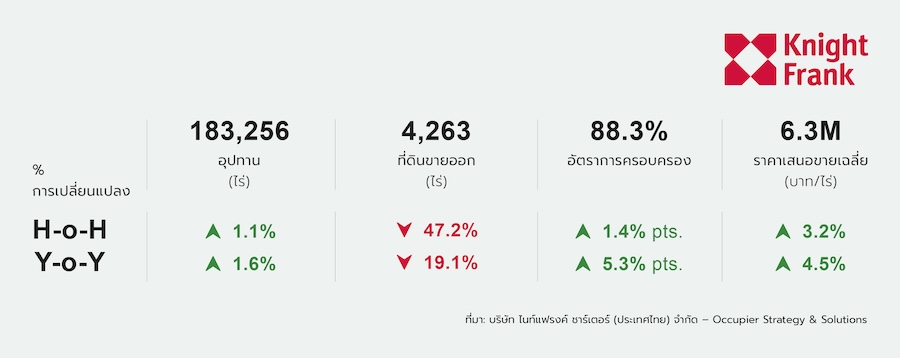

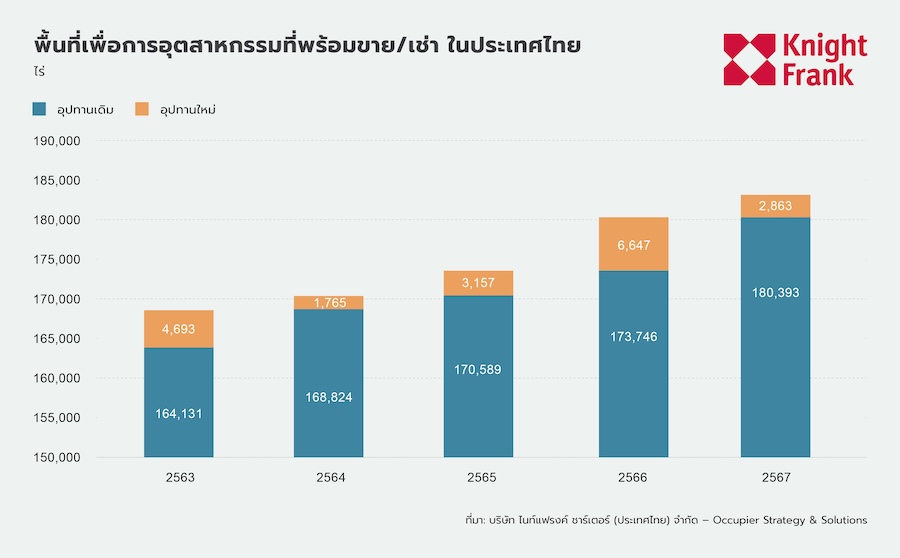

SupplyIn the second half of 2024, the amount of serviced industrial land plots (SILP) available for sale or lease in industrial estates, industrial zones, and industrial parks increased by 1.6% compared to the previous half-year, or an increase of 2,863 rai, totaling 183,256 rai. This increase was driven by the launch of the Amata Chonburi 2 project, which helped expand supply in the market. Over the past 5 years, the supply of SILP has averaged a growth rate of 1-4% per year.

Despite the increase in foreign direct investment (FDI) the availability of large land for production or development into industrial estates has been continuously decreasing, resulting in constraints for investors looking to expand their businesses. The shortage of large industrial land in strategic locations is a significant challenge and may hinder the growth of industries that rely on large-scale operations.

Supply Distribution

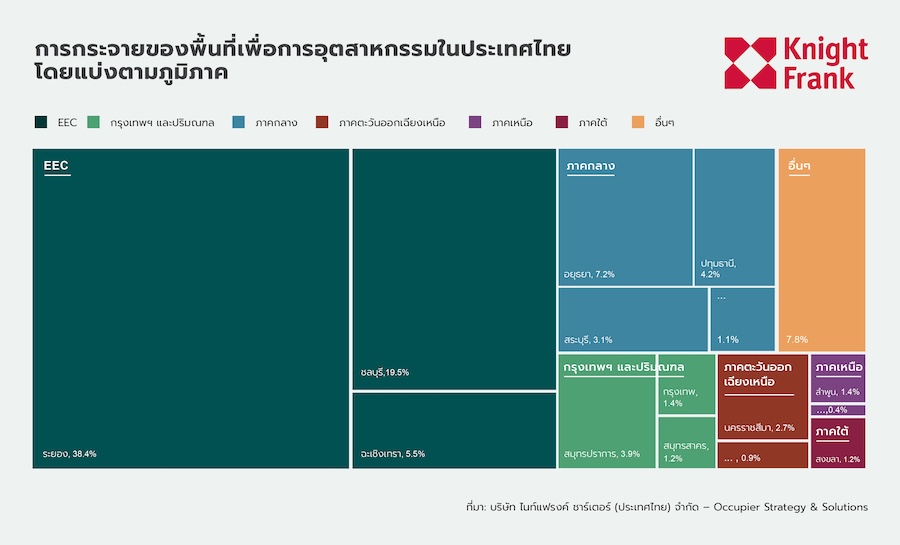

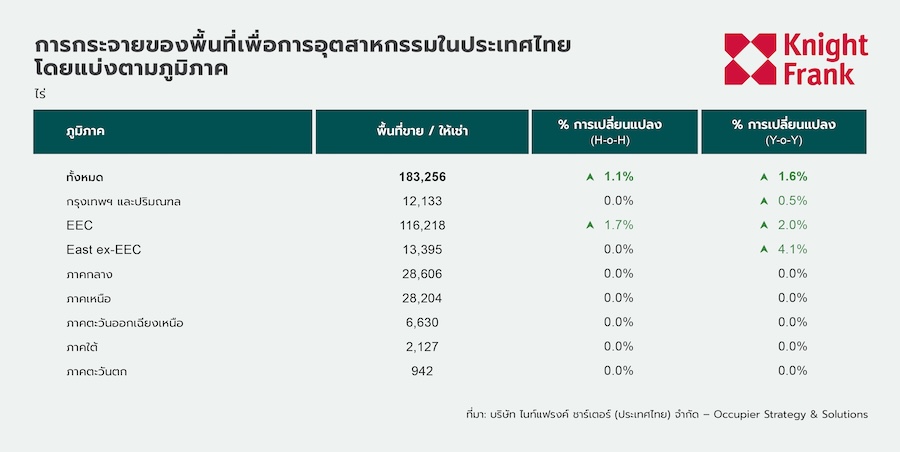

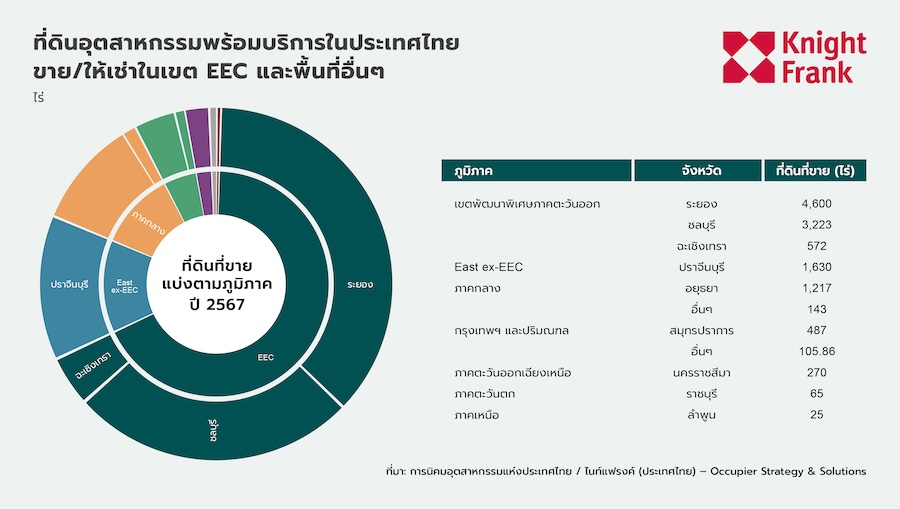

Serviced industrial land (SILP) in Thailand remains concentrated in the Eastern Economic Corridor (EEC) accounting for 64% of the total market share. Within the EEC, Rayong province has the largest share at 38.4% of the total SILP supply, followed by Chonburi at 19.5% and Chachoengsao at 5.5%, which are key centers for major industries such as automotive, electronics, and petrochemicals. Additionally, the proximity to Laem Chabang Port provides the EEC with strong infrastructure, which is a crucial factor driving Thailand's export-oriented economy. In the second half of 2024, land supply in the EEC increased by 1.7% compared to the first half, totaling 116,218 rai, supported by the official launch of the Amata City 2 industrial estate in Chonburi.

Meanwhile, the Central region, which includes Phra Nakhon Si Ayutthaya, Pathum Thani, and Saraburi, accounts for 15% of the total SILP supply, with Ayutthaya having the largest share at 7.2%, followed by Pathum Thani at 4.2% and Saraburi at 3.1%. This region remains an attractive destination for industrial investment due to accessibility and ongoing infrastructure development. The Bangkok Metropolitan Region ranks third with a land supply share of 6% with Samut Prakan at 3.9% and Bangkok at 1.4%, showing no change in supply during the second half of the year.

Demand According to reports from the Industrial Estate Authority of Thailand (IEAT) and Knight Frank's research, the demand for serviced industrial land (SILP) in the second half of 2024 slightly decreased compared to the first half, with a total area sold or leased of 4,263 rai, resulting in an annual total of 12,340 rai in 2024, an increase of 39% compared to 2023, reflecting continued interest in Thailand's industrial land market, driven by key industries such as automotive, electronics, and data centers.

The EEC remains the sub-market with the highest demand, accounting for 64% of all transactions in 2024, with Rayong province having the highest sales at 4,600 rai, followed by Chonburi at 3,223 rai and Chachoengsao at 572 rai, supported by strong infrastructure and proximity to major ports. Notably, there have been large land purchase contracts with Google, which plans to establish a data center and cloud region in Chonburi. Outside the EEC, land transactions totaled 3,944 rai, with Prachinburi, Phra Nakhon Si Ayutthaya, and Samut Prakan being the most active areas.

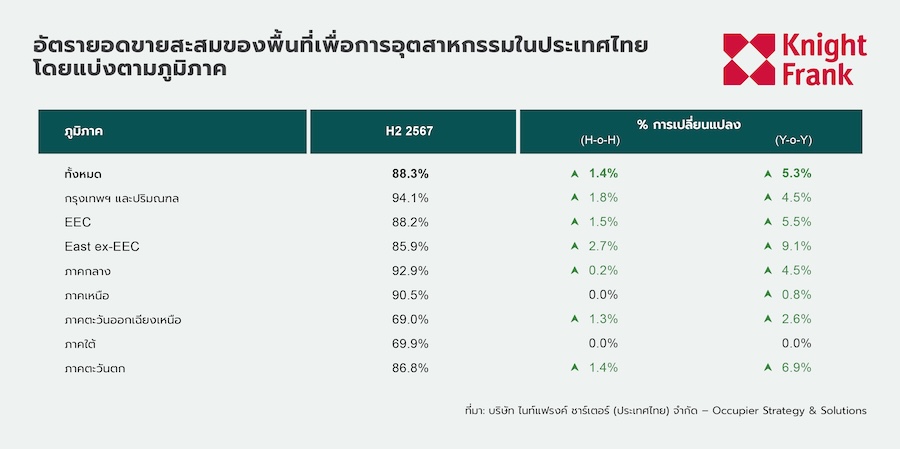

The cumulative sales rate of the market shows improved growth of 1.4% compared to the first half, resulting in a cumulative sales rate of 88.3% in the second half of 2024, with the Bangkok Metropolitan Region having the highest sales rate at 94.1%, followed by the Central region at 92.9% and the Northern region at 90.5%. Meanwhile, the Eastern region outside the EEC experienced the most growth, increasing by 2.7% to 85.9%, while the Northeastern region, despite having the lowest sales rate at 69.0%, still shows a continuous growth trend, increasing by 1.3% compared to the first half.

Asking Prices In the second half of 2024, the average land price in Thailand increased by 3.2% compared to the first half, standing at 6.34 million baht per rai. The Bangkok Metropolitan Region remains the area with the highest prices at 11.1 million baht per rai, while the EEC has an average price of 6.9 million baht per rai. The Central region has an average price of 6.4 million baht per rai, and the Eastern region outside the EEC saw the highest price adjustment at 8.0% compared to the first half, while the EEC continues to see price increases of 2.9%. In the EEC, land prices vary from 3.6 to 12.0 million baht per rai, with industrial estates near Laem Chabang and Map Ta Phut ports having the highest prices, while areas with the lowest prices (below 3 million baht per rai) are in the Northeastern region, reflecting lower demand compared to major industrial areas.

Market Review & Outlook

In the second half of 2024, Thailand's industrial real estate market continues to grow, driven by ongoing interest from foreign investors, with industrial land sales and leases reaching a record high of 12,340 rai, marking the second consecutive year of record highs, reflecting the sustained high demand for land in industrial estates. According to data from the Board of Investment (BOI), the number of investment promotion applications in the first 9 months of 2024 increased by 40% compared to the previous year, with key promoted industries including electronics manufacturing and producers in the electric vehicle (EV) supply chain. However, the increase in the supply of serviced industrial land (SILP) has only been 1%, raising concerns about future land supply as rising costs may deter foreign investors from establishing or expanding operations in Thailand.

Additionally, Google's investment announcement in Thailand underscores the country's potential and readiness in the digital industry, particularly in the data center and cloud service sectors. This investment reflects the strength of Thailand's digital infrastructure, such as high-speed internet, stable energy systems, and a skilled workforce. Recently, the approval of 46 investment promotion projects has a total investment value of over 160,000 million baht, which not only enhances the country's digital infrastructure but also increases the demand for industrial land, especially in areas with advanced logistics networks like the Eastern Economic Corridor (EEC).

Conversely, Thailand's automotive industry faces significant challenges in 2024 with total car sales dropping by 33% to approximately 518,000 units, due to a sluggish economy, high household debt, and strict lending measures that have reduced consumer purchasing power, particularly in the pickup truck market, which is the main segment of the domestic market, facing the most severe impacts, with sales from major manufacturers such as Isuzu and Ford dropping by 43.7% and 42.7% respectively. Even the electric vehicle (EV) market, which previously showed strong growth trends, is also beginning to slow down, with the number of registered electric vehicles decreasing from 76,314 units in 2023 to about 70,000 units in 2024. Consequently, the slowdown in automotive production has led manufacturers to lower production targets and delay expansion plans. Additionally, projects related to EVs, which have been a significant driver of industrial land demand in the past, have already been partially completed, resulting in industrial estate developers facing a period of adjustment as the growth of land sales in the automotive sector slows. To address this challenge, industrial estate developers need to diversify their target customer groups, focusing on sectors with high growth rates such as electronics, renewable energy, and the digital industry to maintain long-term land demand.

For the outlook of the Thai economy in 2025, it is expected to grow between 2.3% and 3.3% supported by increased public spending and investment, a continuous recovery in the tourism sector, and ongoing growth in the export sector. The industrial real estate market will continue to benefit from stable demand, although the expansion of production bases by foreign investors may slow slightly. Key driving industries will continue to include producers in the global supply chain, particularly in the electronics sector, which will continue to seek industrial land in strategic locations to support production and exports.

Mr. Marcus Berthenshaw, Partner - Head of Logistics and Industrial Advisory stated, “The industrial market in Thailand continues to demonstrate strength and ongoing attractiveness, with industrial land sales reaching record highs and foreign direct investment (FDI) surging by 40%. However, changing international trade policies, particularly the countervailing tax system proposed by the U.S., may impact supply chains and key export industries such as automotive and electronics. At the same time, Thailand continues to benefit from the diversification of production bases away from China, which enhances the country's role as a regional manufacturing hub. To maintain competitiveness, Thailand needs to focus on expanding free trade zones, improving logistics efficiency, and investing in smart warehouses and multimodal transport systems. Strengthening trade infrastructure and supply chain adaptability will enable Thailand to sustain industrial growth and elevate its position as a leading logistics and manufacturing hub in the region sustainably.”