Analyzing Business Loan Data from the National Credit Bureau (NCB): How Concerning is Business Debt? (Kasikorn Research Center)

The Kasikorn Research Center has analyzed business loan data from the corporate debtor account database, which is an anonymous statistical database of National Credit Bureau Co., Ltd. (NCB). The average number of accounts is 1.7-1.8 million accounts per quarter. With data up to the second quarter of 2024, five key issues have been identified:

- The quality of Thai business debt has deteriorated since late 2023 after the financial assistance measures during COVID-19 came to an end.

- Smaller businesses are facing more severe bad debt issues.

- Financial institutions of all types are increasingly facing clear impacts.

- When delving into chronic issues, the severity of problems is greater than the overall business loan portfolio, and the debt issues of small and medium enterprises are becoming more concerning.

- Business sectors facing debt quality issues include real estate, accommodation and food services, wholesale and retail trade, and manufacturing, reflecting immediate challenges and structural problems that require collaboration across all sectors to resolve.

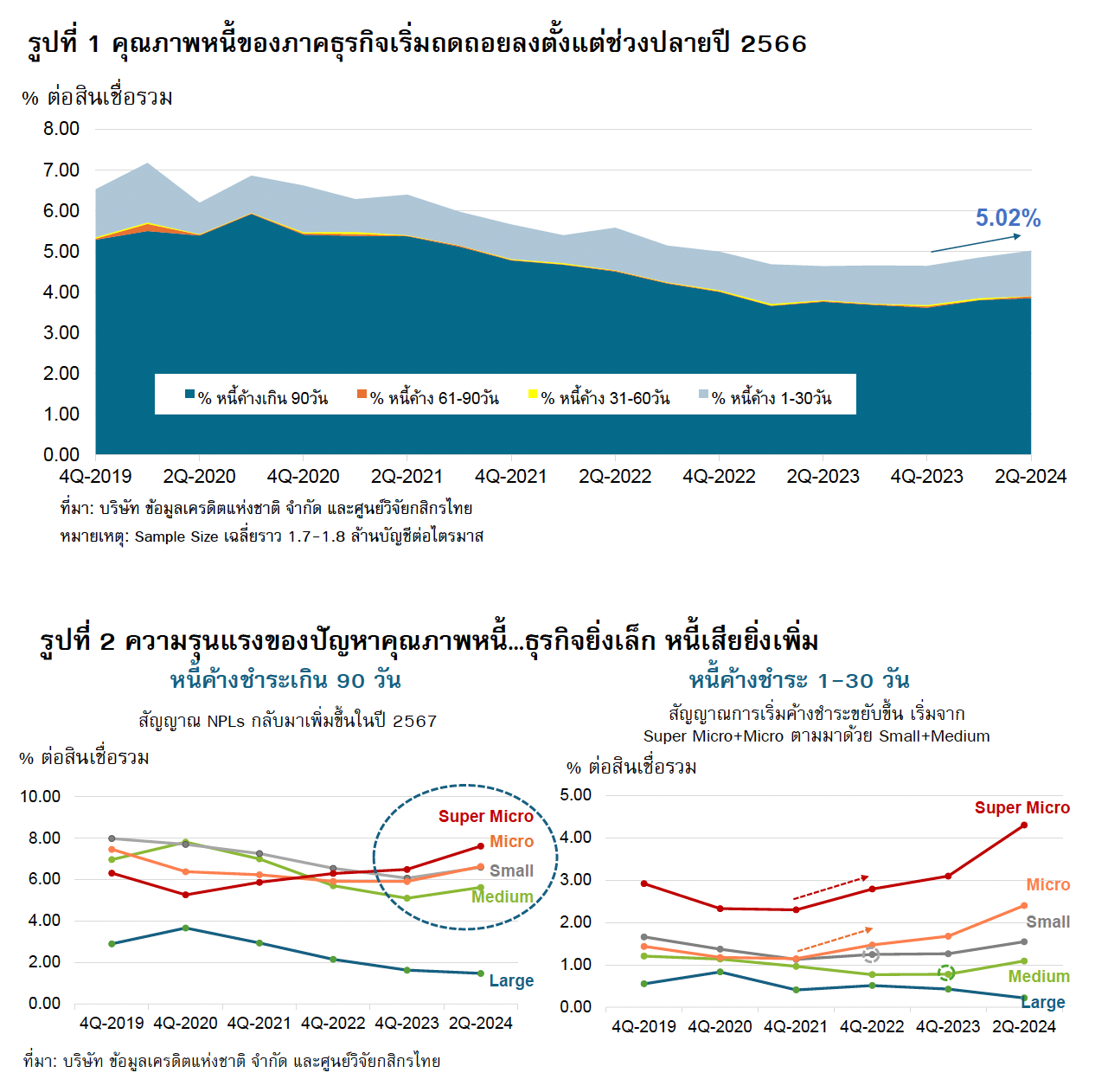

1. The quality of Thai business debt has deteriorated since late 2023 after the financial assistance measures ended.

Overall, the quality of debt for Thai businesses according to NCB data[1] shows that while there was an improvement in debt quality after the COVID-19 crisis, the proportion of overdue debt (1 day or more) decreased from a peak of 7.18% in the first quarter of 2020 to around 4.60-4.70% during 2023, thanks to various relief measures implemented during COVID. However, this proportion began to rise again in early 2024, reaching 5.02% by the end of the second quarter of 2024, as the effects of the measures waned and the economic recovery remained fragile and uneven (Figure 1).

2. Smaller businesses are facing more severe bad debt issues.

When examining the proportion of non-performing loans (NPLs) by business size[2], it is found that overdue debt (1-30 days) and NPLs (overdue for more than 90 days) are most prevalent in Super Micro, Micro, Small, and Medium businesses. This reflects the increasing sensitivity of smaller businesses to environmental factors (Figure 2).

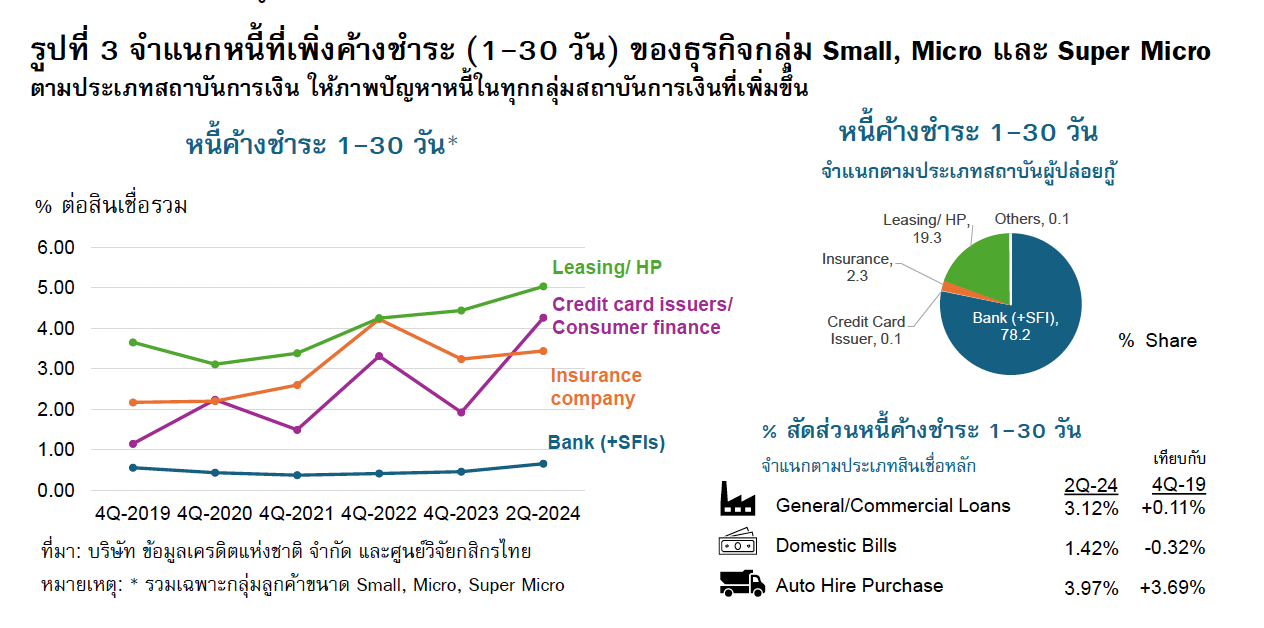

3. All types of financial institutions are facing clearer impacts.

When focusing on debt that has just surpassed the payment deadline of 30 days for Super Micro, Micro, and Small businesses, which are the most severely affected groups, it indicates that all lending institutions (members of NCB) are experiencing a rise in low-quality debt (not limited to commercial banks and specialized financial institutions). This is particularly true for leasing companies and consumer finance, followed by credit card companies, with overdue debt (1-30 days) increasing to 5.04%, 4.27%, and 3.44%, respectively (Figure 3).

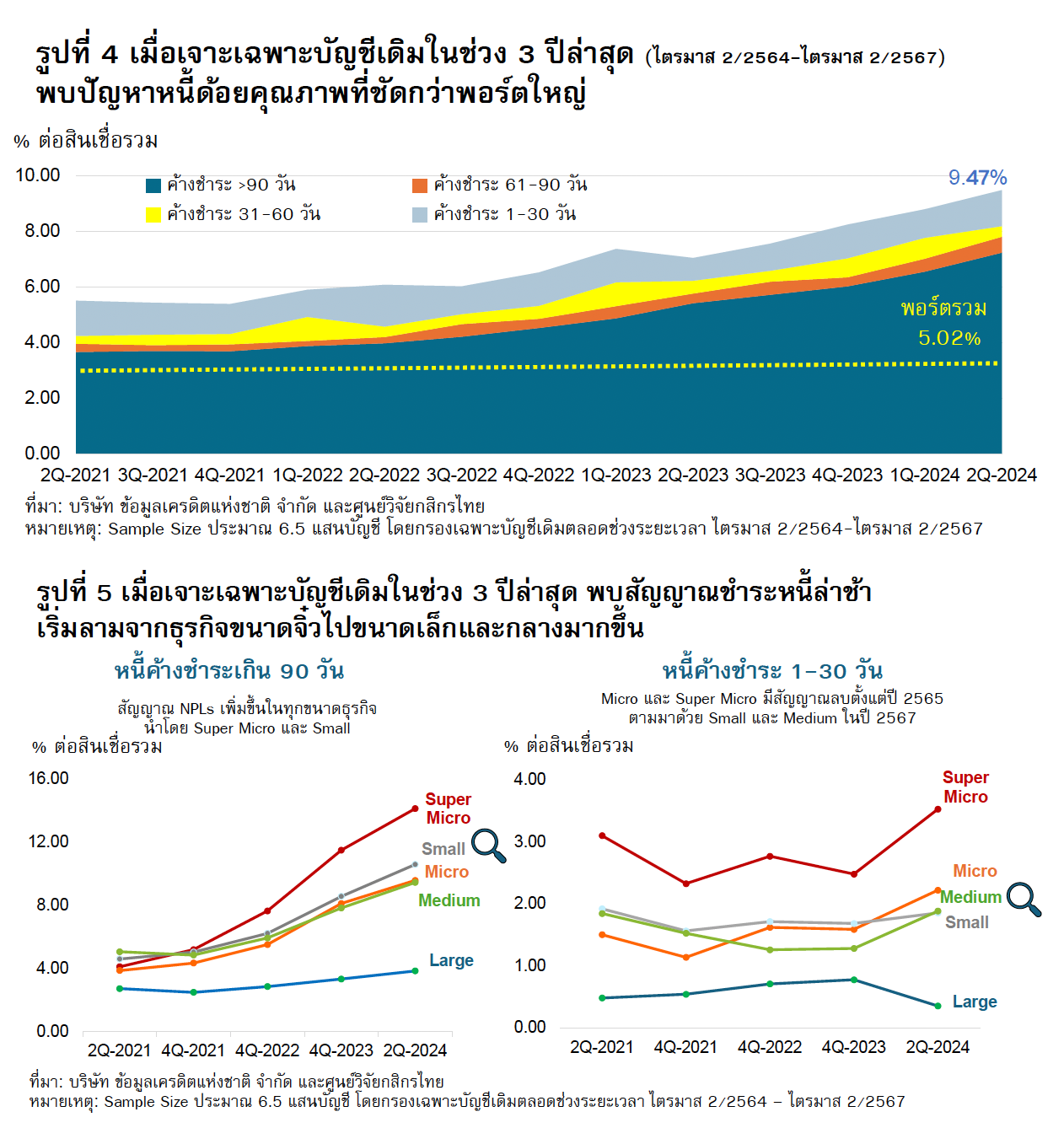

4. Focusing on chronic issues reveals problems more severe than the overall portfolio, with small and medium businesses becoming increasingly concerning.

To accurately assess the causes and trends of debt quality in the business sector, the Kasikorn Research Center filtered business loan accounts with historical data for three years (excluding newly established businesses and those that disappeared for various reasons), resulting in a sample of approximately 650,000 accounts. This study found that the proportion of overdue debt at all stages for this group of loans is around 9.47% in the second quarter of 2024, a significant increase from 5.50% in the second quarter of 2022, primarily due to the rise in NPLs (Figure 4).

The proportion of debt that has just started to become overdue is significantly higher than the overall business loan portfolio, which stands at 5.02%, emphasizing that this group of debtors has not benefited from the recovery of economic activities and/or the government's and financial institutions' debt relief measures as much as they should have. Furthermore, when categorized by business size, it is evident that Medium and Small businesses are experiencing a more pronounced decline in debt quality compared to the overall portfolio (Figure 5), indicating that issues are spreading from micro businesses to small and medium enterprises.

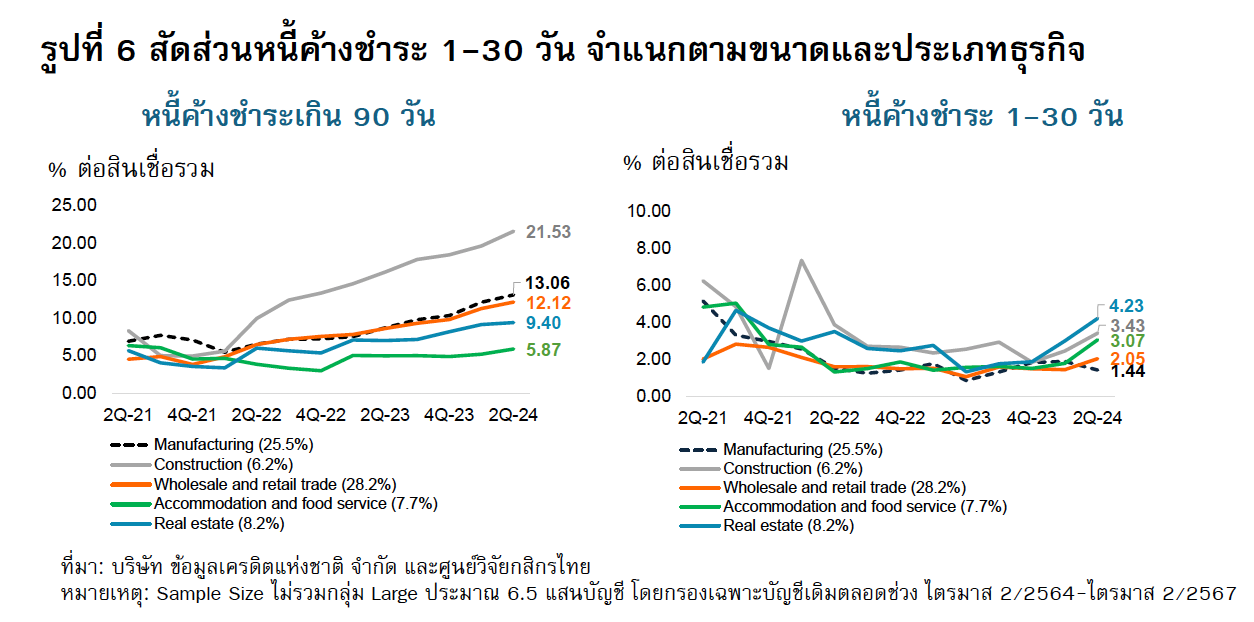

5. Business types with concentrated problems include construction, real estate, accommodation and food services, wholesale and retail trade, and manufacturing, reflecting immediate challenges and structural issues.

When examining the dimensions of SME business types with chronic debt, it is found that overdue debt (1-30 days) is concentrated in real estate and construction, accommodation and food services, wholesale and retail trade, and manufacturing (which together account for 75.8% of total SME loans). This reflects immediate challenges such as weak purchasing power and increased competition from cheaper foreign goods, which pressure sales and orders, exacerbating the ability to repay debts (Figure 6). Additionally, it is noteworthy that the accommodation and food services sector has begun to worsen in the first half of 2024, coinciding with the uneven recovery of tourism, which also affects the accommodation and restaurant sectors.

As for the structural problems leading to the continuous rise in NPLs (overdue for more than 90 days) in the aforementioned core businesses, they are largely due to household debt issues that pressure purchasing power, rising costs, competition with foreign capital, changing consumer behaviors, trade wars affecting supply chain adjustments, and increased trade regulations. These factors inevitably lead to an influx of cheap foreign goods into the Thai market (e.g., electronics, textiles, and electrical appliances after exports to the U.S. have decreased), forcing the manufacturing sector to reduce production capacity for many products. Thus, all these factors are putting pressure on the income and competitiveness of Thai SMEs, making it increasingly difficult for them to survive in a rapidly changing global trade environment.

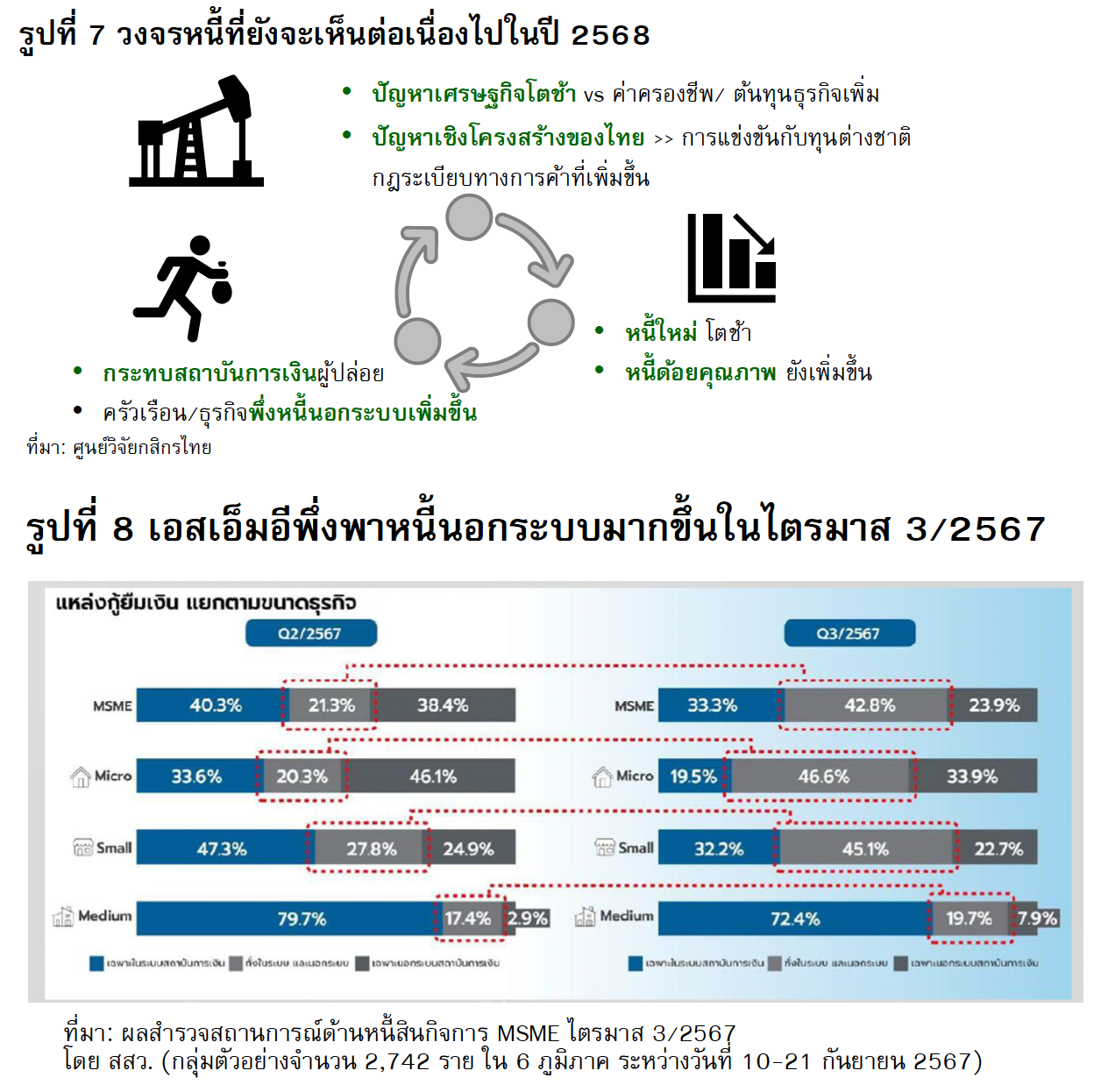

If the root causes of the problems are not concretely addressed, 2025 will be another year of facing the same cycle of issues.

The increasing problem of low-quality debt, although a lagging indicator, still shows no improvement, reiterating the impact of accumulated issues mentioned above, which ultimately ties back to the root cause of the problem: the economic situation and structural issues that require sustained government efforts to 'restructure the economy' to create new growth engines beyond enhancing the capabilities of entrepreneurs and debt restructuring measures from the financial sector to manage immediate debt issues, as the Bank of Thailand and commercial banks have already implemented and may continue to do so in the future, such as extending the debt restructuring period for troubled groups alongside measures to assist financial institutions in helping debtors over a longer timeframe.

As long as the root causes of the problems remain unaddressed, 2025 will be another year where we face new loans growing slowly amidst a borrower market with limited repayment capacity and increasing low-quality debt, which will continuously impact lenders' burdens in managing high levels of bad debt, affecting profitability (Figure 7). Meanwhile, entrepreneurs and households facing chronic issues may have to increasingly rely on informal debt, as a survey by the Office of Small and Medium Enterprises Promotion in the third quarter of 2024 indicates that SMEs are increasingly depending on informal debt compared to the previous quarter (Figure 8).

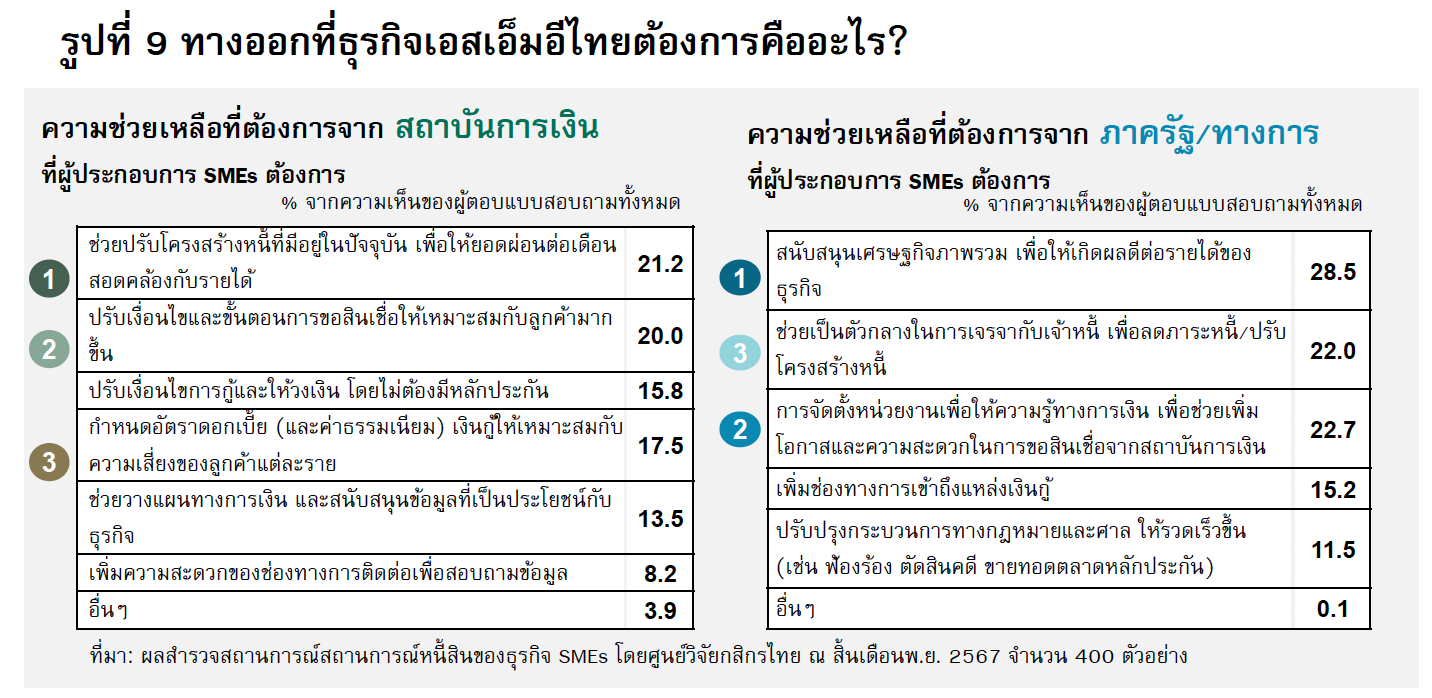

A survey of SME entrepreneurs by the Kasikorn Research Center of 400 samples at the end of November 2024 (Figure 9) indicates the need for sustainable solutions from the government, namely: First, support for the overall economy to positively impact business income (28.5%); Second, establishing agencies to provide financial education to enhance opportunities and ease of access to loans from financial institutions (22.7%), reflecting the need to increase the financial literacy of business clients; Third, assistance in mediating negotiations with creditors to reduce debt burdens/restructure debt (22.0%), which are measures to support and sustain immediate survival.

On the side of SME entrepreneurs' demands from financial institutions, the focus will be on three areas: restructuring debt to align monthly payments with income, adjusting loan application conditions and procedures, and setting fees and interest rates appropriate to the risk of each customer. The latter refers to Risk-Based Pricing, where customers with low risk should receive lower interest rates, while those with high risk should be charged higher rates.

Disclaimers:

This article, analysis, or research is prepared by Kasikorn Research Center Co., Ltd. and National Credit Bureau Co., Ltd. for the benefit of public dissemination. The information contained in this report is based on statistical economic and financial data from reliable sources. However, Kasikorn Research Center Co., Ltd. and National Credit Bureau Co., Ltd. do not guarantee the completeness or accuracy of the information and are not responsible for any use of the information, text, opinions, or conclusions presented in this report under any circumstances. Kasikorn Research Center Co., Ltd. and National Credit Bureau Co., Ltd. hold exclusive rights to the intellectual property of this report and reserve all rights to the information contained in this document. No one may use, reproduce, modify, display, or publish this information, in whole or in part, for commercial purposes without prior written permission from Kasikorn Research Center Co., Ltd. and National Credit Bureau Co., Ltd. Furthermore, any citation or reference to parts of this report in articles, analyses, research, documents, or other communications must be done correctly and not misleading or damaging to Kasikorn Research Center Co., Ltd. and National Credit Bureau Co., Ltd., and must acknowledge the copyright ownership of the information of Kasikorn Research Center Co., Ltd. and National Credit Bureau Co., Ltd., and must explicitly reference the edition and date of this document from Kasikorn Research Center Co., Ltd. and National Credit Bureau Co., Ltd.

[1] The NCB database differs from the Bank of Thailand's database as it covers debts of member institutions beyond commercial banks, including all types of debt obligations of debtors, not just principal amounts, and includes debts that financial institutions have written off but are still in the legal process and have not been closed, resulting in different and higher proportions compared to the Bank of Thailand's statistics, which primarily report on commercial banking system data.

[2] Large refers to businesses with outstanding loans greater than 500 million baht.

Medium refers to businesses with outstanding loans greater than 100-500 million baht.

Small refers to businesses with outstanding loans greater than 20-100 million baht.

Micro refers to businesses with outstanding loans greater than 5-20 million baht.

Super Micro refers to businesses with outstanding loans less than or equal to 5 million baht.