Carbon Credit Prices and the Challenges of Developing the Carbon Market in Thailand (Kasikorn Research Center)

- The carbon market in Thailand operates on a voluntary basis, which results in a lack of motivation for buyers to purchase carbon credits. Consequently, the demand for carbon credits in significant quantities that would drive prices up is minimal.

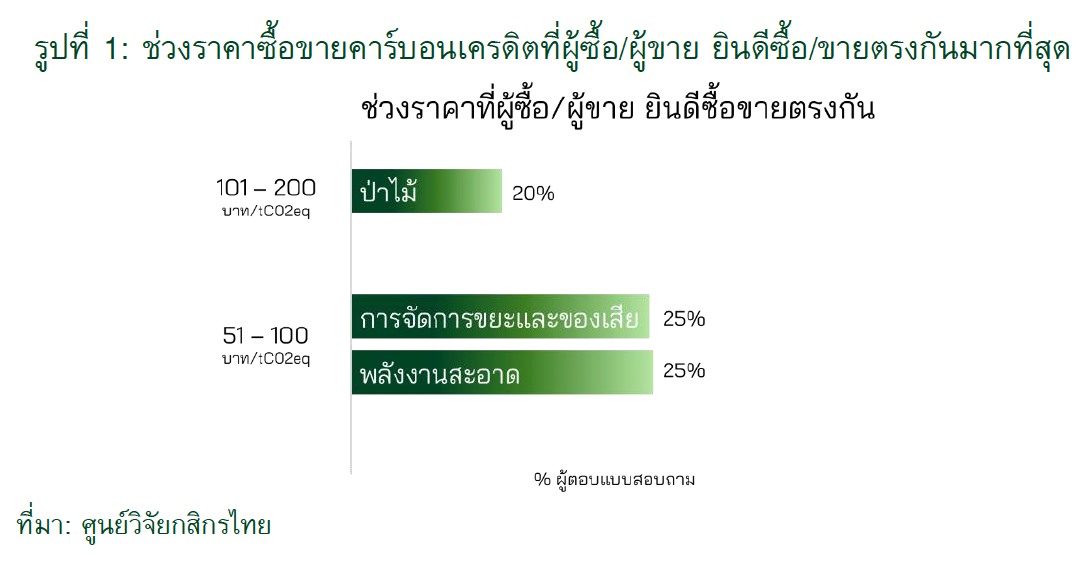

- Surveys indicate that only 20-25% of buyers and sellers can agree on a price that they are willing to buy and sell at, which ranges between 51 – 200 Baht per ton of carbon dioxide equivalent (tCO2eq). This is considered relatively low compared to mandatory markets abroad.

- However, several projects can sell at prices close to international markets because they create added value, such as co-benefits for the community or directly addressing buyers' needs, which are factors that developers must consider.

Current issues regarding the pricing of carbon credit transactions show a low alignment between the prices buyers are willing to pay and those sellers are willing to accept, with only 20 – 25% of buyers wanting to purchase carbon credits at prices that match sellers' expectations (Price Equilibrium) (Figure 1).

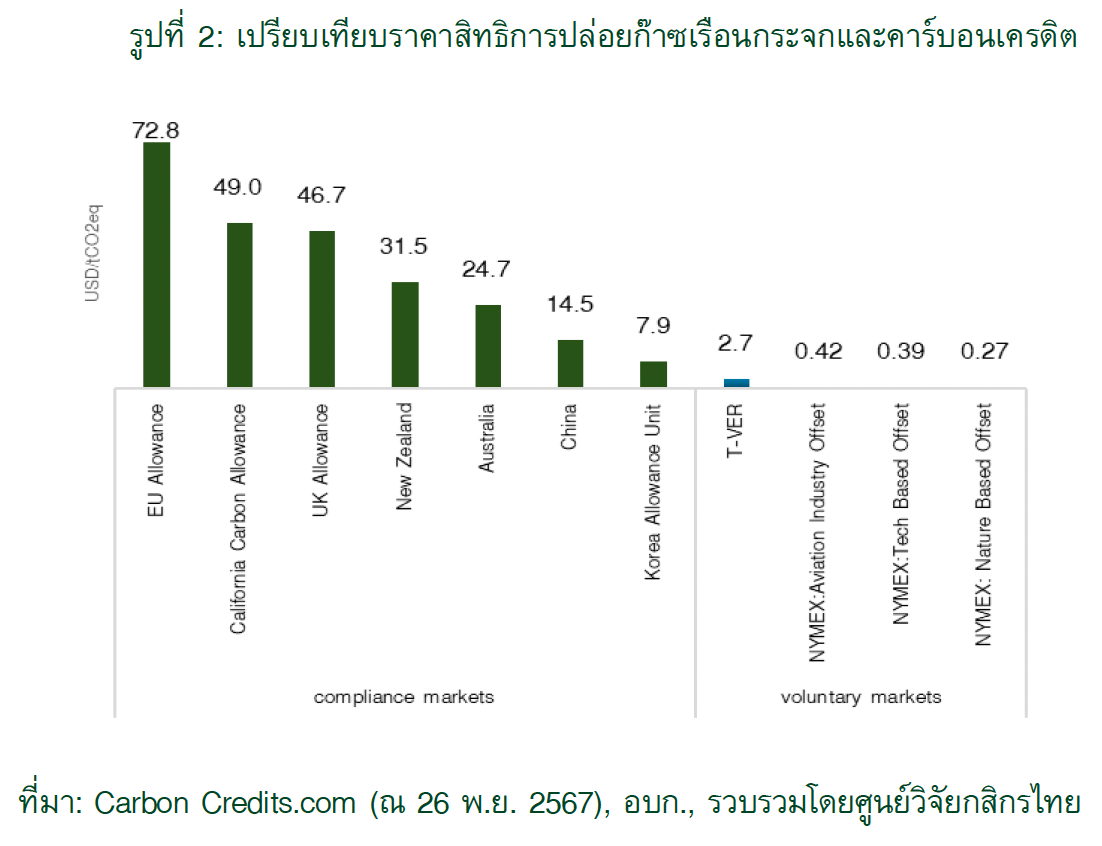

The reasons for the price discrepancies stem from the voluntary nature of Thailand's carbon market, which leads buyers to have lower purchasing motivations, primarily for CSR purposes or internal policies. As a result, the prices of traded carbon credits are relatively low compared to compliance markets (Figure 2).

-

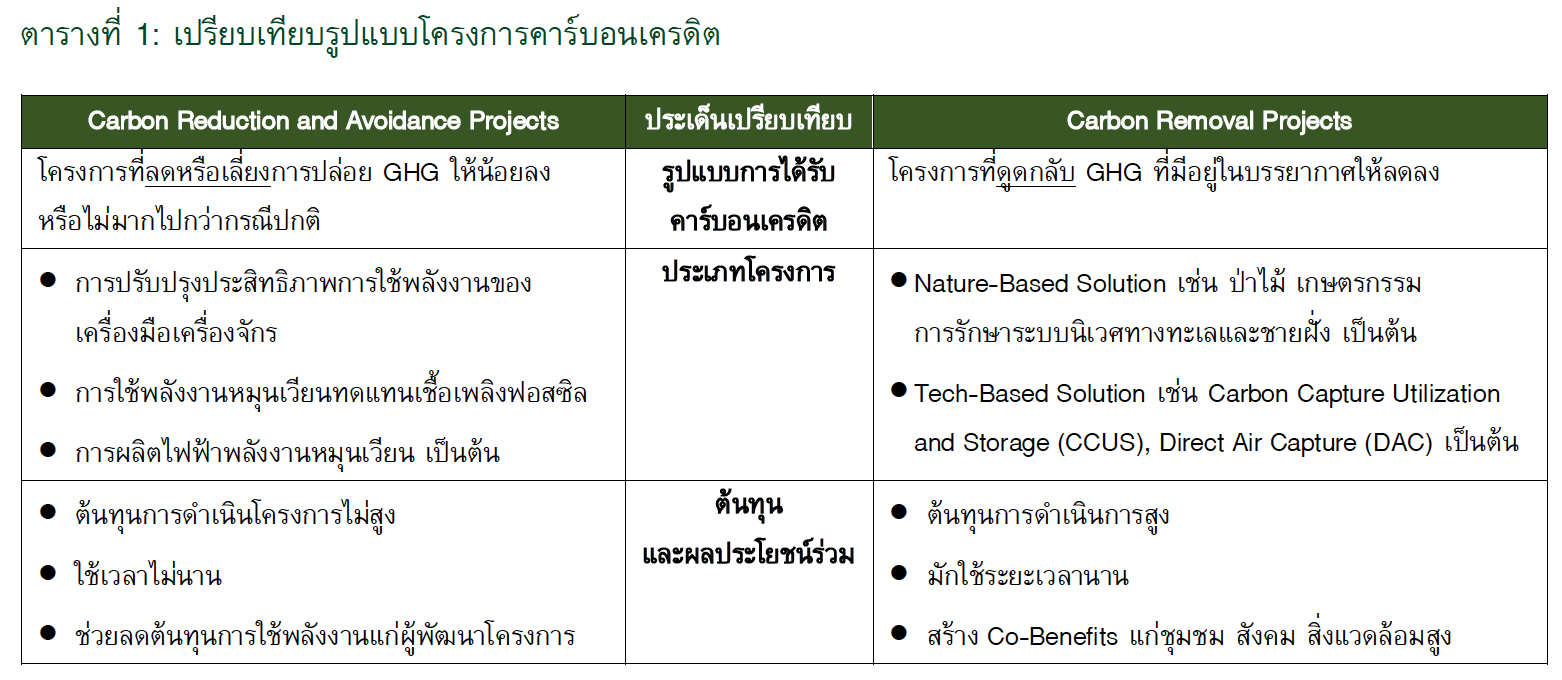

Project Types

Carbon credits derived from GHG sequestration projects tend to be priced higher, especially those that provide co-benefits to society, such as forestry and waste management. Buyers may assign value to these projects, allowing sellers to create added value from carbon credits. To sell carbon credits at higher prices, sellers cannot rely solely on high demand to push prices up, as the current carbon credit purchases for offsetting greenhouse gas emissions in Thailand are voluntary.

Therefore, if project developers want to sell carbon credits at higher prices, they may consider these factors to enhance value, which can be summarized as follows:

- Co-Benefit

Project developers may choose to develop projects that attract buyer interest and create added value for communities, such as forestry, composting, and waste-to-fuel projects, which currently have higher trading prices.

- Carbon Credit Crediting Period

Currently, carbon credits have no expiration, leading to market distortions due to two scenarios: (1) buyers tend to stockpile only cheap credits, and (2) sellers are reluctant to sell their credits, hoping for higher prices, which can lead to oversupply in the market.

However, future regulations may require the use of only new generation carbon credits for certain measures, such as CORSIA. Therefore, stockpiling or holding carbon credits for future offsets or sales will become challenging, which will help stimulate the trading of current credits.

- In-Demand Project Types

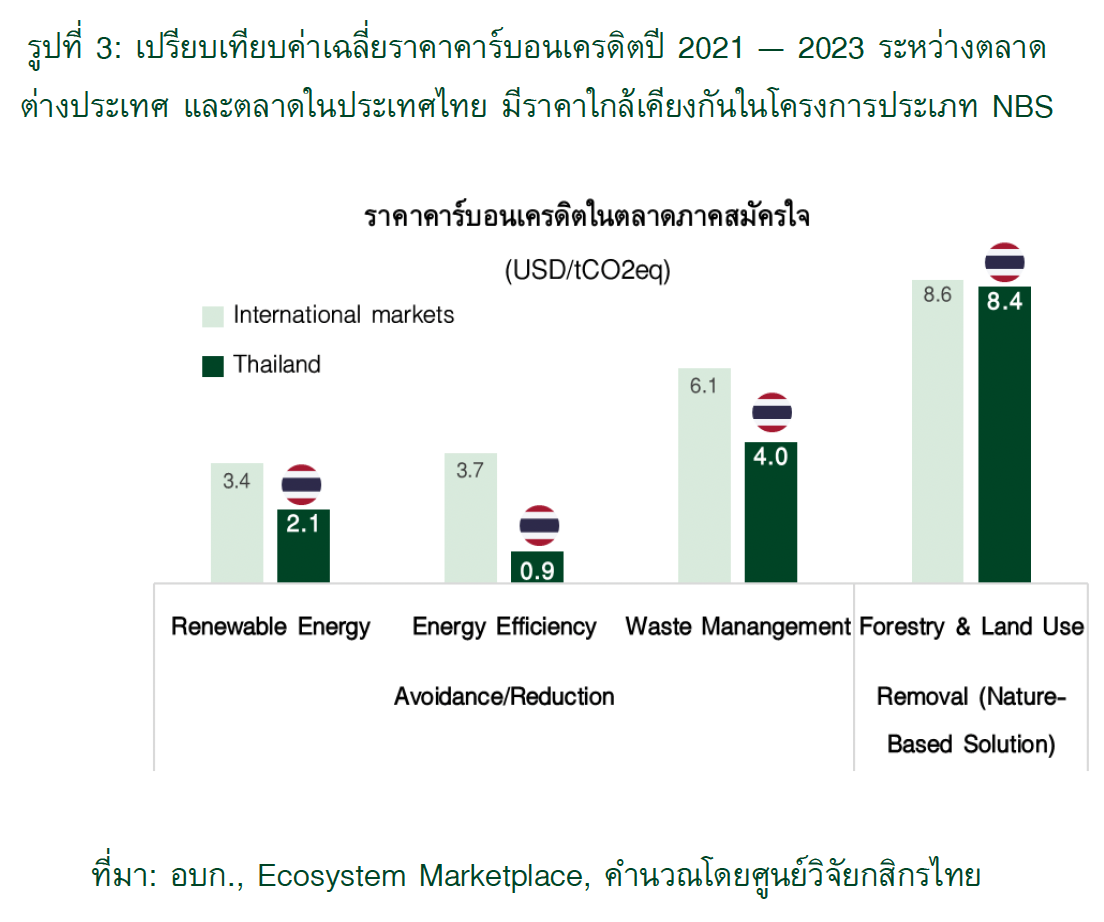

Developing projects in scarce categories can lead to higher trading prices based on the principles of demand and supply, such as projects that capture or sequester greenhouse gases using technologies like Carbon Capture Utilization and Storage (CCUS) and Direct Air Capture (DAC), which are priced competitively with other global standards (Figure 3) according to the demands of organizations aiming for Net Zero but unable to reduce GHG usage themselves.

Finally, beyond the actions of project developers, the government and supporting agencies will play a crucial role in helping to drive carbon credit prices higher.

They may consider implementing mandatory greenhouse gas reduction mechanisms, such as carbon taxes, in a way that allows for the use of carbon credits for offsets during the initial transition phase, which will help stimulate the carbon credit market and push domestic carbon prices higher.