Office Market Q3 2024

Market Overview

The Thai economy grew by 3.0% year-on-year in Q3 2024, marking the fastest growth rate in two years, driven primarily by strong investment, tourism, and exports, according to the National Economic and Social Development Council (NESDC). Most of the growth was supported by the service sector, while the industrial sector slowed down and agricultural output decreased. Despite the positive economic performance, analysts warn of challenges in maintaining growth momentum due to high household debt, sluggish demand from China, and rising borrowing costs.

In response to government pressures, the central bank lowered the policy interest rate to 2.25% last October. Additionally, the government is set to meet on Tuesday to consider further economic stimulus measures, including the second phase of the "Digital Wallet" project.

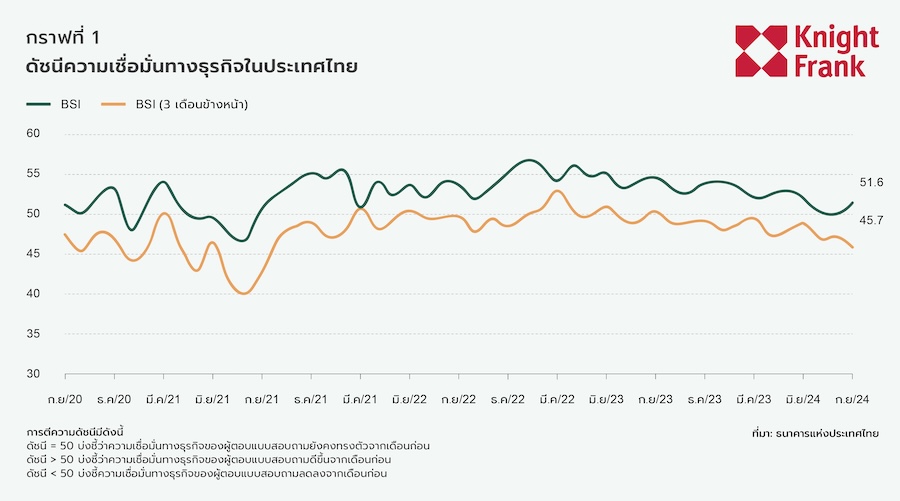

Regarding the Business Sentiment Index (BSI), it continued to decline in September 2024, affected by a slowdown in the manufacturing sector, particularly in electronics and plastics. While the index for the non-manufacturing sector remained stable, confidence in the real estate sector decreased due to economic uncertainties and high household debt, which limited property sales. However, the BSI forecast for the next three months shows slight recovery, driven by improvements in the construction sector and tourism services, benefiting from government projects and the year-end tourism season.

Supply

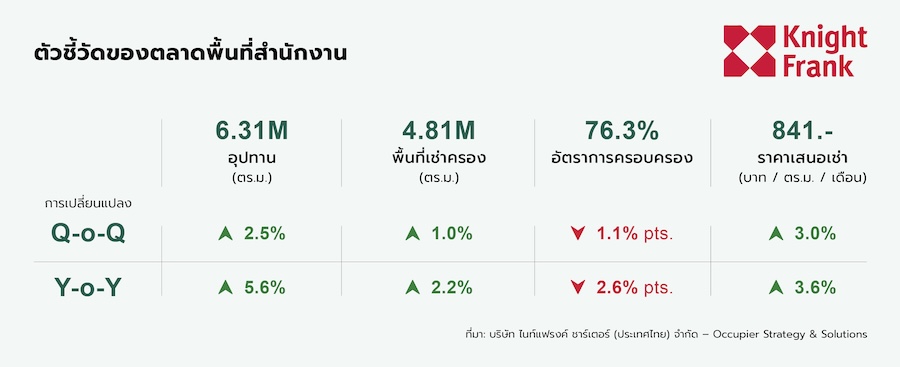

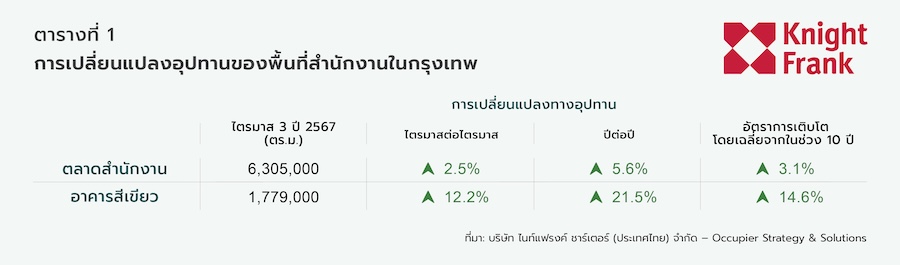

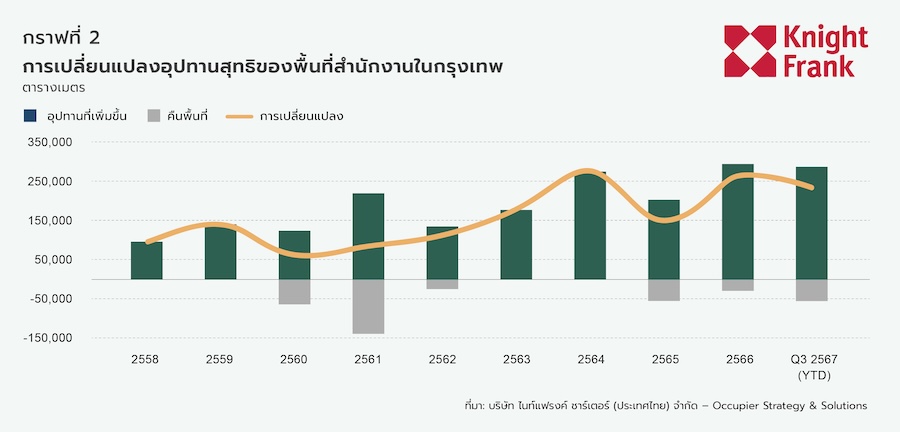

Office space in Bangkok increased by 151,000 square meters this quarter, or 2.5% quarter-on-quarter, bringing the total area to 6.31 million square meters, primarily due to the opening of One Bangkok, Buildings 3 and 4, and Rangsit Business Park.

The proportion of green buildings increased from 26% to 28% of the total supply. However, 54,000 square meters were withdrawn from the market after three buildings were taken out.

Future Supply

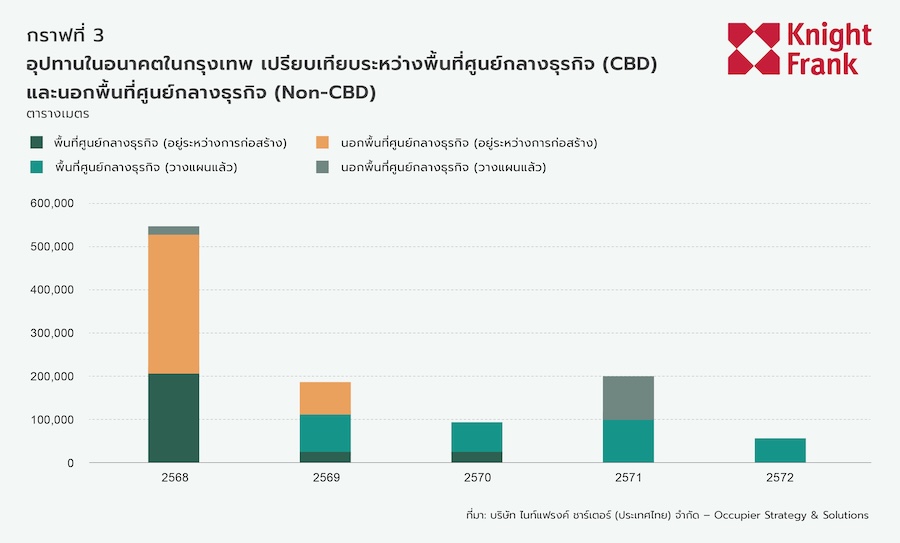

The new office space available for lease has decreased to 1.1 million square meters, reflecting the completion of new buildings and a reduction in future supply. Of this, 640,000 square meters are under construction. Meanwhile, it is forecasted that 2025 will see the highest supply entering the market, expected to increase by up to 550,000 square meters.

Demand

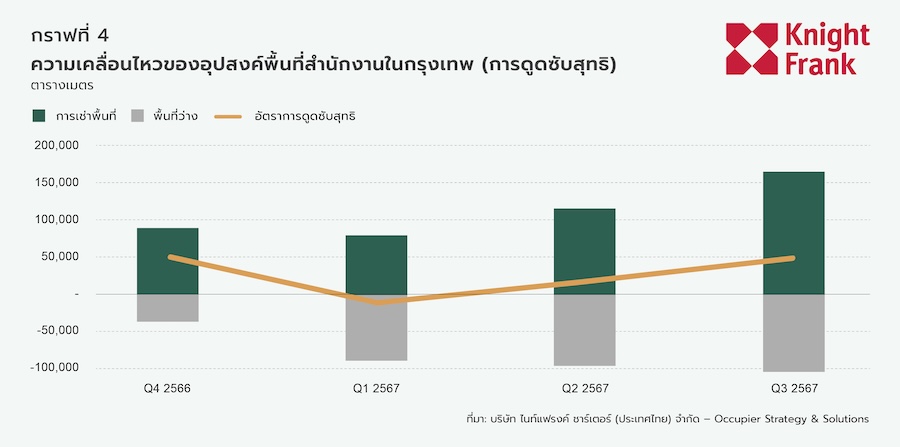

Demand for rental space increased from the previous quarter, with a total of 164,000 square meters leased, while net absorption rose to 50,000 square meters, driven by strong leasing activity in the One Bangkok project, resulting in total usable space increasing by 1% to 4.81 million square meters.

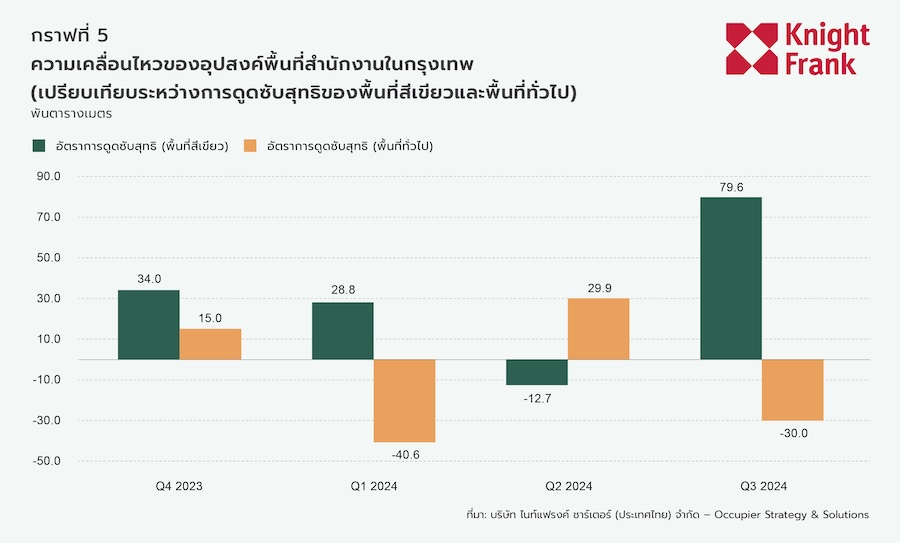

Green buildings played a significant role in meeting the rising demand, with net absorption reaching 80,000 square meters, while non-green buildings saw a net decrease of 30,000 square meters.

The trend for office space leasing remains positive in both the Central Business District (CBD) and Non-CBD areas, with net absorption of 24,000 square meters and 26,000 square meters, respectively.

Market Dynamics by Segment

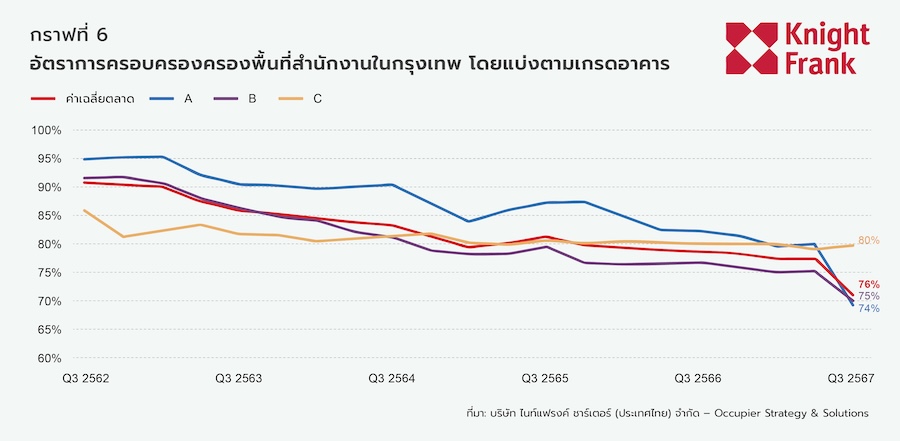

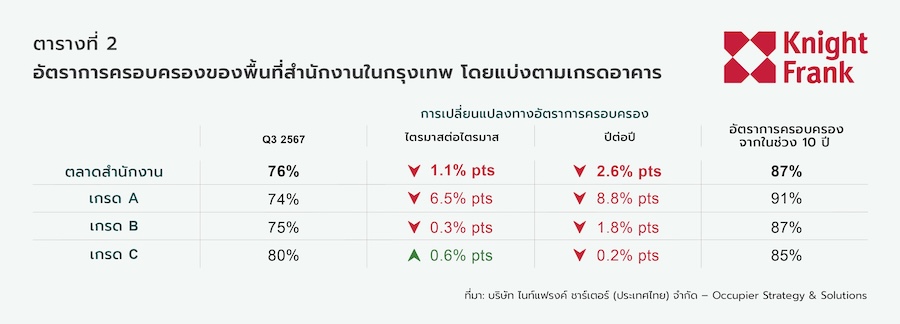

The overall office rental rate remained stable at 76%, slightly down from the previous quarter. The rental rate for Grade A office space significantly dropped from 80% to 74% due to increased supply and heightened competition, while Grade B buildings remained stable at 75%, continuing to be the lowest-performing segment. Conversely, the rental rate for Grade C offices was the only segment to improve, rising from 79% to 80%.

The supply of Grade C buildings remained relatively stable, as they often undergo property upgrades or are withdrawn from the market in response to challenging market conditions. Additionally, Grade C buildings continue to attract demand from cost-conscious tenants.

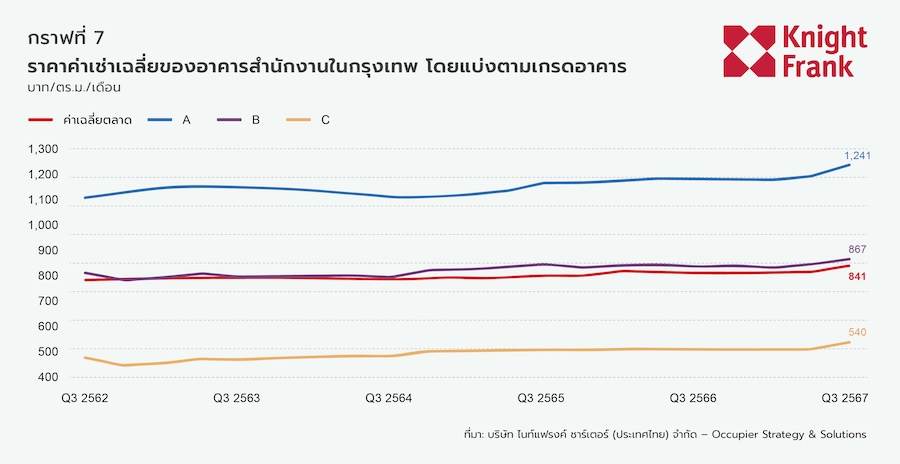

In Q3 2024, the average rent was 841 baht per square meter per month, an increase of 3.0% quarter-on-quarter and 3.6% year-on-year, surpassing the average growth of 3.1% over the past decade. Average rents increased across all grades, with Grade A at 1,241 baht per square meter per month, up 4.0% from the previous quarter. Grade B averaged 867 baht per square meter per month, up 2.6% quarter-on-quarter, while Grade C saw the highest growth, increasing by 5.7% quarter-on-quarter to 540 baht per square meter per month, driven by a reduction in low-performing supply in this segment rather than rental increases in existing properties.

Market Dynamics by Area

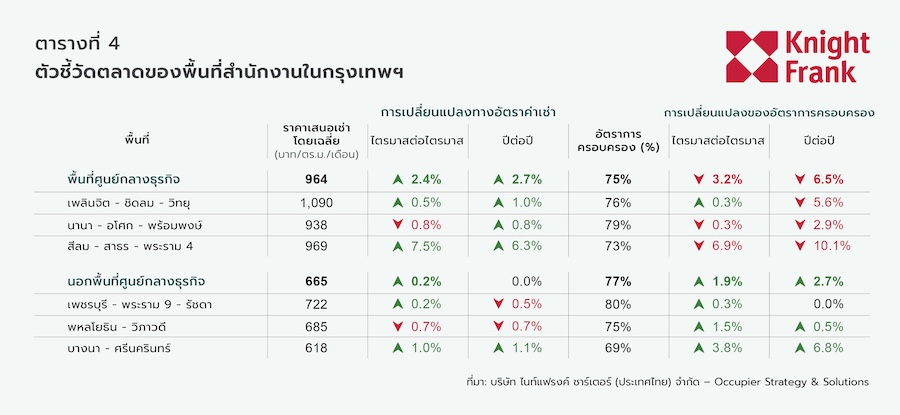

Central Business District (CBD) average rent increased by 2.4% quarter-on-quarter to 964 baht per square meter per month, while the rental rate decreased to 75%, down 3.2% quarter-on-quarter.

- Silom-Sathorn-Rama 4 experienced the highest rental growth in the CBD, increasing by 7.5% quarter-on-quarter to 969 baht per square meter, driven by the One Bangkok project, which added nearly 200,000 square meters of rental space at approximately 1,500 baht per square meter. However, this location also faced the highest decline in rental rates in the CBD, dropping by 6.9% quarter-on-quarter to 73%.

- Conversely, the Ploenchit-Chidlom-Witthayu area showed relatively stable performance, with a slight rental rate increase of 0.3% quarter-on-quarter to 76%, and rent rising by 0.5% quarter-on-quarter to 1,090 baht per square meter.

- Nana-Asoke-Phrom Phong saw a slight rental decrease of 0.8% quarter-on-quarter to 938 baht per square meter, with a minor rental rate decline of 0.3% quarter-on-quarter to 79%.

Non-CBD Areas saw relatively stable average rent, with a slight increase of 0.2% quarter-on-quarter to 665 baht per square meter per month. The average rental rate improved, rising by 1.9% quarter-on-quarter to 77%.

- Bangna-Srinakarin performed the best in the Non-CBD area, with rent increasing by 1.0% quarter-on-quarter to 618 baht per square meter and the rental rate soaring by 3.8% quarter-on-quarter to 69%.

- The Phetchaburi-Rama 9-Ratchada area saw slight rental growth of 0.2% quarter-on-quarter to 722 baht per square meter, with a minor rental rate increase of 0.3% quarter-on-quarter to 80%, the highest rental rate in the Non-CBD market.

- Meanwhile, the Phahonyothin-Vibhavadi area experienced a rental decrease of 0.7% quarter-on-quarter to 685 baht per square meter, but the rental rate increased slightly by 1.5% quarter-on-quarter to 75%.

Mr. Panya Jenkijwatanalert, Executive Director and Head of Office Space Division stated, “In Q3 2024, the office market in Bangkok demonstrated strong momentum, driven by increased supply and heightened leasing activity. The completion of major projects like One Bangkok has expanded the city’s total office space to 6.31 million square meters, reflecting the growing prominence of large mixed-use developments that are transforming the cityscape.” He added that environmentally certified buildings are playing an increasingly important role, now accounting for 28% of the total supply. In terms of demand, leasing activity has seen significant growth, nearly doubling compared to the previous quarter, with many tenants transitioning back to full office work.

Looking ahead, the office market in Bangkok will face challenges in balancing the large supply with the changing demands of tenants. With an additional 1.1 million square meters expected to come online in the next few years, competition among building owners is anticipated to remain fierce, potentially leading to innovations in building design, services, and pricing strategies. Grade A buildings with high rents will need to differentiate themselves with outstanding offerings such as state-of-the-art amenities, health-focused designs, and convenient access. Furthermore, buildings certified by WiredScore and SmartScore are becoming increasingly significant, reflecting the growing importance of digital infrastructure and smart building technologies. These certifications, which assess and highlight the connectivity and intelligence capabilities of buildings, have become key factors in differentiating building owners looking to attract technology-savvy and innovation-driven tenants.

“Next year will be a crucial time, with approximately 550,000 square meters of new supply expected to enter the market. As these dynamics unfold, space owners will need to focus on tenant retention and building competitiveness in a market with diverse tenant demands,” Mr. Panya concluded.