Stakeholders in Thailand's Voluntary Carbon Market: Challenges and Support Strategies

Who are the stakeholders in Thailand's voluntary carbon market? To continuously develop the voluntary carbon market in Thailand, it is essential to understand who the current stakeholders are and their characteristics. This knowledge will help in identifying tools or mechanisms to support these groups or attract additional stakeholders into the market. The Kasikorn Research Center and the Office of Natural Resources and Environmental Policy and Planning (ONEP) have prepared a report on the situation and trends of Thailand's voluntary carbon market for 2024, outlining the characteristics of stakeholders in the carbon market, summarized as follows:

-

Supply Side

Approximately 27% of all stakeholders belong to this group, which plays a role in developing and implementing carbon credit projects. Analyzing the supply of carbon credits, specifically the amount certified under the TVERs standard, reveals a total of 20.5 million tCO2eq certified from 173 projects. The most popular projects developed are in the renewable energy sector, which have received certification for a total of 11.6 million tCO2eq (56.5%) from 84 projects.

Next are projects focused on energy efficiency at 15.4%, while forestry and agriculture projects have the least number of certified carbon credit projects, accounting for only 2.7% of the total greenhouse gas emissions certified.

Another role of supply-side stakeholders is selling the carbon credits obtained from their projects, with only 3.48 million tCO2eq or 17.0% of the total certified carbon credits having been traded.

[1] This is due to developers or project owners having the discretion to decide how much of the certified carbon credits to sell, when to sell them, or whether to retain them for their own greenhouse gas offsetting purposes.

Data on carbon credit trading (Figure 1) shows that the majority of trades occur in renewable energy projects (78%), followed by waste management (12%) and forestry (10%).

However, the lower trading volume of carbon credits compared to the certified amount reflects two possible scenarios from the stakeholders in the carbon market:

(1) Sellers are not bringing their certified carbon credits to the market because they intend to use them for their own purposes.

(2) Buyers have limited demand for carbon credits, making the selling price unattractive enough for developers or project owners to agree to sell.

- Demand Side

- Increase avenues for using carbon credits to offset greenhouse gas emissions domestically through mandatory policies by establishing tools such as a carbon tax that allows partial use of carbon credits for offsets or setting a time frame.

- Develop registration, measurement, and certification standards for projects to be applicable at an international level to expand the market and increase demand for the use of carbon credits more broadly, such as carbon offsetting and reduction projects for international aviation (CORSIA), International Maritime Organization (IMO), or the ability to convert across standards.

- Financial support through tax incentives for expenses incurred in assessing and certifying carbon credits, as well as providing low-interest loans related to carbon credit project development to help reduce costs for project developers.

- Establish guidelines and promote greenhouse gas reduction for the public and businesses (Best Practice) to create awareness about implementing carbon credit projects, including the use of carbon credits, especially at the community level, which may lack knowledge but have the potential to implement carbon credit projects to attract new organizations or agencies into Thailand's voluntary carbon credit market.

- Size and Type of Organization

- Involvement in the Carbon Market

Various organizations, both domestic and international, have a demand for TVERs carbon credits to offset greenhouse gas emissions resulting from their operations, accounting for about 13% of all stakeholders.

The amount of carbon credits used to offset greenhouse gas emissions from organizations, products, events, and personal offsets using TVERs standards totals 1.88 million tCO2eq.

[2] (As of September 2, 2024) This represents an average offset of 455,000 tCO2eq per year over the last three years, while CO2 emissions are approximately 270 million tons per year.

[3] This reflects the potential for a significant amount of greenhouse gas offsetting through carbon credits to meet the carbon neutrality goals of organizations.

[1] The trading volume and total certified greenhouse gas emissions as of August 31, 2024, source: ONEP.

[2] Data as of September 2, 2024, source: ONEP, compiled and calculated by the Kasikorn Research Center.

[3] CO2 emissions in the industrial sector and from fossil fuel combustion in 2022, excluding land use such as deforestation and agriculture, source: OurWorldinData.

Development Strategies for the Carbon Market Addressing Stakeholder Issues

The voluntary carbon market in Thailand is still a new market with significant potential for further development, as the volume of greenhouse gas offsets remains very low compared to total emissions (0.17%). With cooperation from all sectors, including government, private sector, academic institutions, and international organizations, the voluntary carbon market in Thailand can be elevated to greater popularity.

In this regard, the Kasikorn Research Center suggests the following development strategies focusing on supporting both supply and demand stakeholders:

Appendix

This article follows the Carbon Credit Vol. 1 article by the Kasikorn Research Center published in early 2024.

[1] which summarized details on trading, project development guidelines, pricing, considerations, and approaches to using carbon credit mechanisms to address various issues such as reducing PM2.5.

In Vol. 2, various aspects of Thailand's voluntary carbon market will be presented, including survey data and empirical data in the carbon market. This article will discuss the characteristics of stakeholders in the carbon credit market on both the demand and supply sides to propose targeted development strategies for Thailand's voluntary carbon market.

Size, Type of Organization, and Involvement in the Carbon Market in Thailand

Survey results indicate that stakeholders in the market are predominantly large businesses, accounting for 54%, followed by SMEs at 39%, and government agencies/independent organizations at 7%. When classified by industry, the largest sectors are manufacturing (32%), agriculture, hunting, and forestry (13%), and consulting firms (10%).

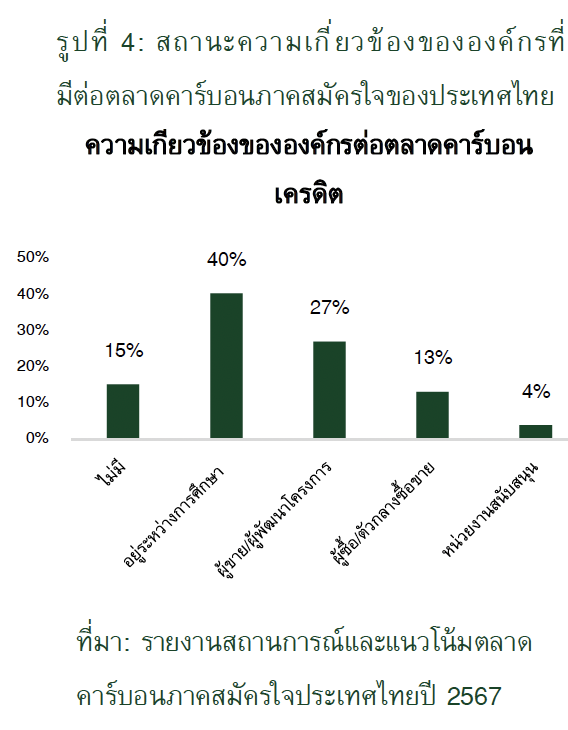

Most organizations (85%)[1] are involved or are preparing to engage as stakeholders in the carbon credit market. Among the stakeholders in the carbon market, 27% are sellers/project developers who create the supply of carbon credits, 13% are buyers/intermediaries representing the demand for carbon credits, and 4% are supporting agencies.

Additionally, regarding greenhouse gas reduction efforts, it was found that one-third of stakeholders in the carbon credit market have already undertaken such actions, which the Kasikorn Research Center refers to as the “Climate Action” group.

This group has initiated T-VER carbon credit projects, process modifications, carbon credit offsets, and self-declaration or achieved Carbon Neutrality/Net Zero goals, reflecting the adaptation of companies/agencies in Thailand to reduce greenhouse gas emissions.

However, the reasons for the participation of Climate Action organizations in the carbon market, particularly as sellers/project developers and buyers/intermediaries, are largely due to these businesses being large organizations with knowledge and financial readiness, allowing them to implement these actions in a tangible way that benefits the organization.

[1] Organizations that are members of various greenhouse gas reduction networks, such as the Thailand Carbon Neutral Network (TCNN), Carbon Markets Club, Thai Renewable Energy Association (RE 100), and members of the Federation of Thai Industries, etc.