One Year After COVID-19 Eases... Which Types of Mutual Funds and Real Estate Trusts Are Worth Considering?

One year ago, the Ministry of Public Health announced that COVID-19 would transition from a dangerous communicable disease to a monitored communicable disease, effective from October 1, 2022. This led to the cancellation of travel restrictions for foreigners entering Thailand. Activities and daily life, such as dining out, traveling, and shopping, have returned to pre-pandemic levels. However, not all types of real estate are experiencing a recovery similar to that before the COVID-19 outbreak. Here’s an overview of the various types of real estate that mutual funds and real estate trusts are investing in:

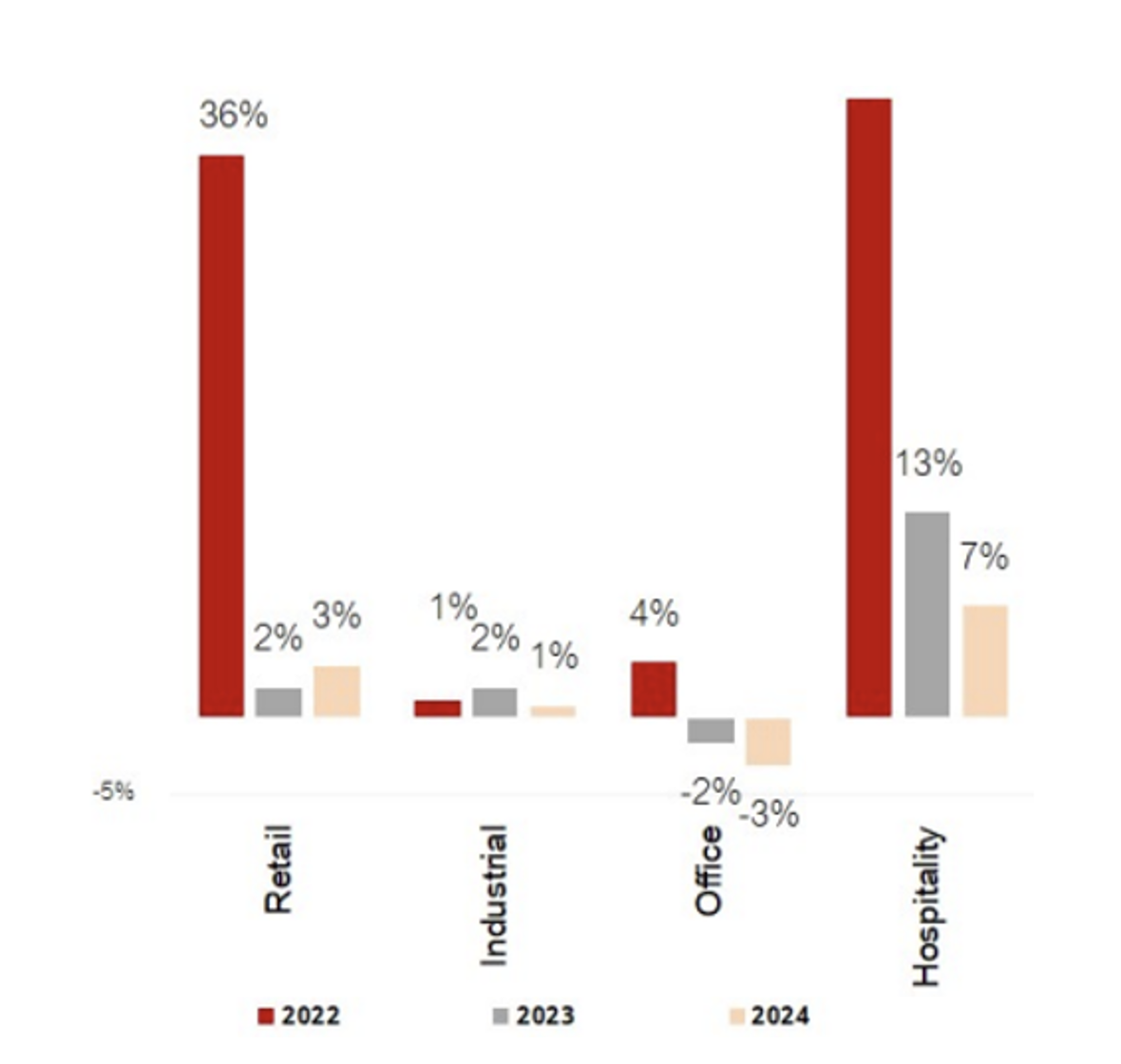

Retail Sector

- Current Situation: Although the COVID-19 pandemic reduced foot traffic in retail spaces, both malls and community centers, retail space management has offered rental discounts based on the impact on individual tenants. They have also restructured lease agreements to include variable rent based on sales, allowing tenants to remain and preventing vacancies. As a result, the overall rental rate in Bangkok remained above 95% by the end of 2022. With the easing of COVID-19 restrictions, Thai consumers have returned to shopping, and the number of foreign visitors has gradually increased, bringing foot traffic in retail spaces back to pre-COVID levels. The level of new demand in the market aligns with the need for rental space.

- Outlook: As foot traffic in retail spaces approaches pre-COVID levels, rental discounts are decreasing, and some landlords can increase rents for tenants who are no longer affected, such as restaurants. However, rising electricity costs, labor costs, and property taxes are also impacting the profitability of retail spaces. Therefore, mutual funds and real estate trusts in the retail sector are likely to maintain or slightly increase their dividend per unit (DPU) over the next year.

Industrial Sector

- Current Situation: During the COVID-19 pandemic, while most types of real estate were affected, the industrial sector, particularly warehouses, saw sustained demand due to the growth of logistics and e-commerce. The relocation of foreign businesses from China due to geopolitical issues, China's reopening, and government incentives for major companies to invest in Thailand have all contributed to increased demand for industrial space. However, the supply of industrial space continues to rise.

- Outlook: Despite positive factors driving demand for industrial space, the supply in the market remains high. The development of rental factories and warehouses is quicker than other types of real estate, allowing operators to introduce new supply rapidly if demand increases. This creates limitations on rent increases. Overall rental rates in the market are expected to remain stable, leading mutual funds and real estate trusts in the industrial sector to maintain or slightly increase their DPU over the next year.

Office Sector

- Current Situation: Demand for office space is recovering slowly, partly because some tenants have adopted work-from-home or hybrid models, leading to reduced space requirements or no expansion. The influx of new office supply in the market is affecting the ability to attract new tenants to increase occupancy rates for the office buildings that mutual funds and real estate trusts invest in. Rent increases will be limited in a tenant market, as new office buildings will offer incentives to attract tenants.

- Outlook: The difficulty in increasing office rents and attracting new tenants will continue to pose challenges. Additionally, if funds plan to renovate office buildings, this will incur additional capital expenditures, leading mutual funds and real estate trusts in the office sector to likely maintain or decrease their DPU over the next year.

Hospitality Sector

- Current Situation: The Thai tourism sector and hotel industry are showing clear signs of recovery, with a continuous increase in foreign visitors to Thailand in 2023. In the first eight months, approximately 17.8 million visitors were recorded, surpassing the total of about 11.2 million in 2022. The Bank of Thailand predicts that tourist numbers will reach 28 million in 2023 and 35.5 million in 2024. The government has implemented free visa policies and supported an increase in flight numbers, along with plans to expand airports to accommodate future flight increases. Recently, Suvarnabhumi Airport opened a new passenger terminal, SAT-1.

- Outlook: With the increasing demand for hotel stays following the easing of COVID-19, there is an opportunity to raise average room rates (ARR) in line with this demand. Provided that incidents like the shooting at Paragon and the Israel-Hamas conflict do not have a significant impact, hotel revenues are expected to grow. High occupancy rates will help manage rising costs, such as electricity and labor, while maintaining a high net profit margin. Therefore, mutual funds and real estate trusts in the hospitality sector are likely to increase their DPU over the next year.

Forecast of Dividend Growth (DPU Growth) for Each Type of Mutual Fund and Real Estate Trust:

Source: SET, DBSVTH (Data as of September 4, 2023)

The information above considers the overall market situation for each type of real estate investment. However, the performance of mutual funds and real estate trusts in the market may vary due to specific factors affecting each fund, such as the expiration of lease rights for investment assets, loan repayment obligations, and investments in additional assets or conversions from mutual funds to real estate trusts.