Inflation and Interest Rates: Trends in Mutual Fund and Real Estate Trust Prices

In early 2020, the U.S. Federal Reserve (FED) implemented an accommodative monetary policy by lowering the federal funds rate to a range of 0.00 - 0.25% to manage the economic impact of the COVID-19 pandemic. As the situation improved, the U.S. economy began to recover, but this led to high inflation, with an average rate of 8% in 2022. Consequently, the FED raised interest rates 11 times starting in early 2022, reaching 5.25 - 5.50% by June 2023. The cooling U.S. economy has since reduced inflation to 3.7% as of September 2023. However, the FED is likely to maintain high interest rates (Higher for Longer) to keep inflation below 3%.

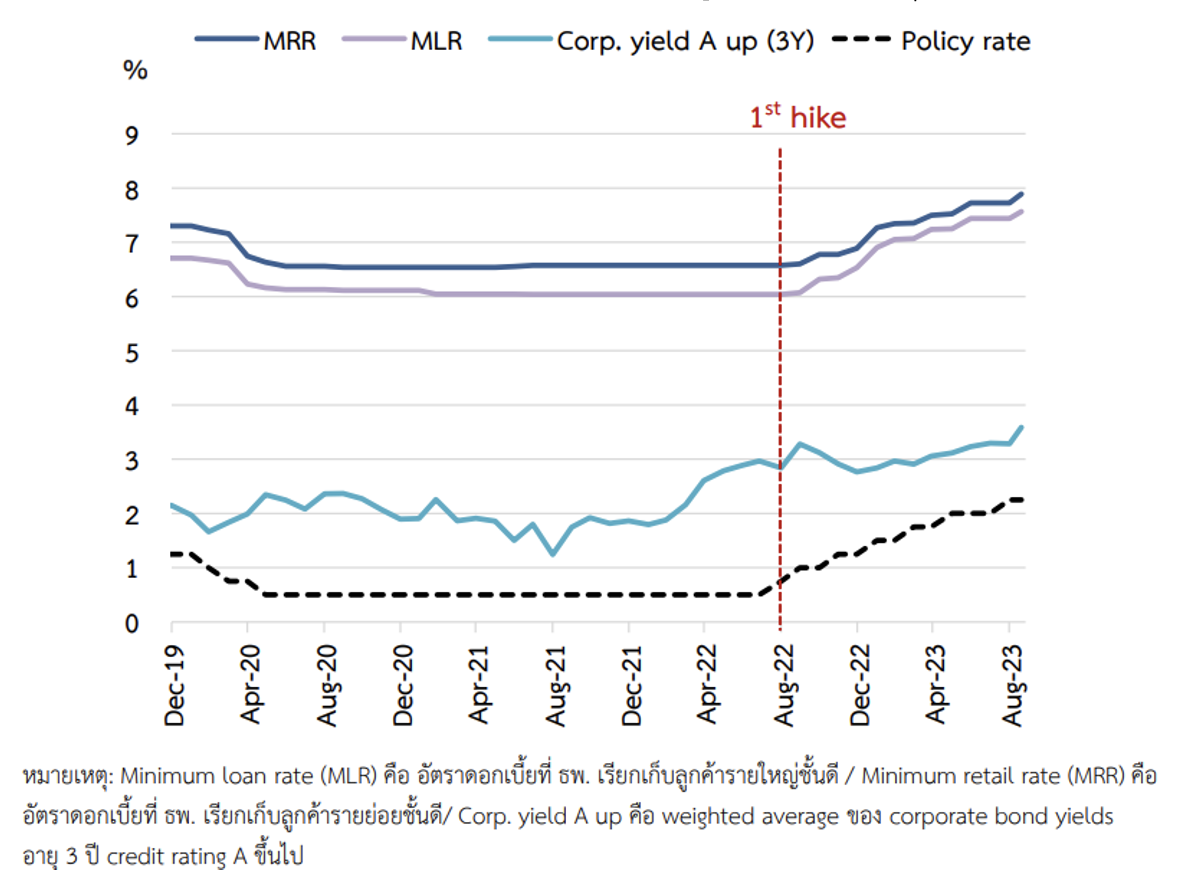

The FED's interest rate hikes to curb inflation have caused capital to flow out of countries with lower interest rates, impacting currency depreciation against the U.S. dollar, including the Thai baht. The Bank of Thailand (BOT) has gradually raised its policy rate since July 2022 from 0.50%, reaching 2.50% by September 2023. Nevertheless, Thailand does not face high inflation, with the BOT forecasting inflation rates of 1.6% and 2.6% for 2023 and 2024, respectively.

Table 1: Policy Rates and Various Loan Interest Rates

Source: Bank of Thailand

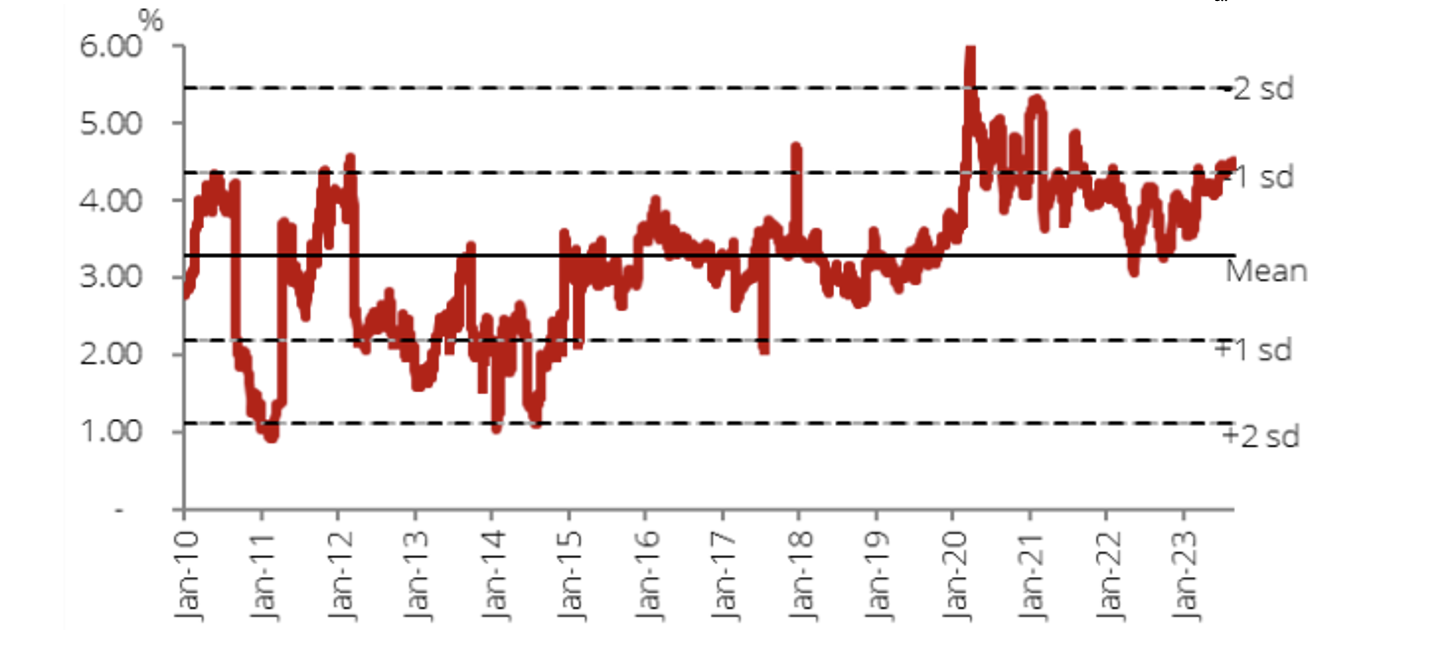

Given the factors and circumstances mentioned above, it seems that U.S. policy rates are nearing their peak, while Thailand's policy rates are likely at their peak as well, with low inflation forecasts suggesting that further increases in the policy rate will be limited. Therefore, mutual funds and real estate trusts ("real estate funds"), which focus on dividend returns, are expected to gain more interest. Investors often compare interest from deposits with dividend yields. Additionally, if interest rates decrease in the future, it will further enhance the attractiveness of investing in real estate funds. Currently, the yield spread between real estate funds and 10-year government bond yields stands at 4.2%, compared to a historical average of 3.3%.

Table 2: Spread Between Real Estate Fund Yields and 10-Year Government Bond Interest Rates

Source: Bloomberg, DBSVTH

The current high yield spread reflects several factors, including:

- The performance of real estate funds is not on par with historical levels, with increased vacancy rates in office spaces and lower rental income in retail areas, especially for projects reliant on foreign traffic.

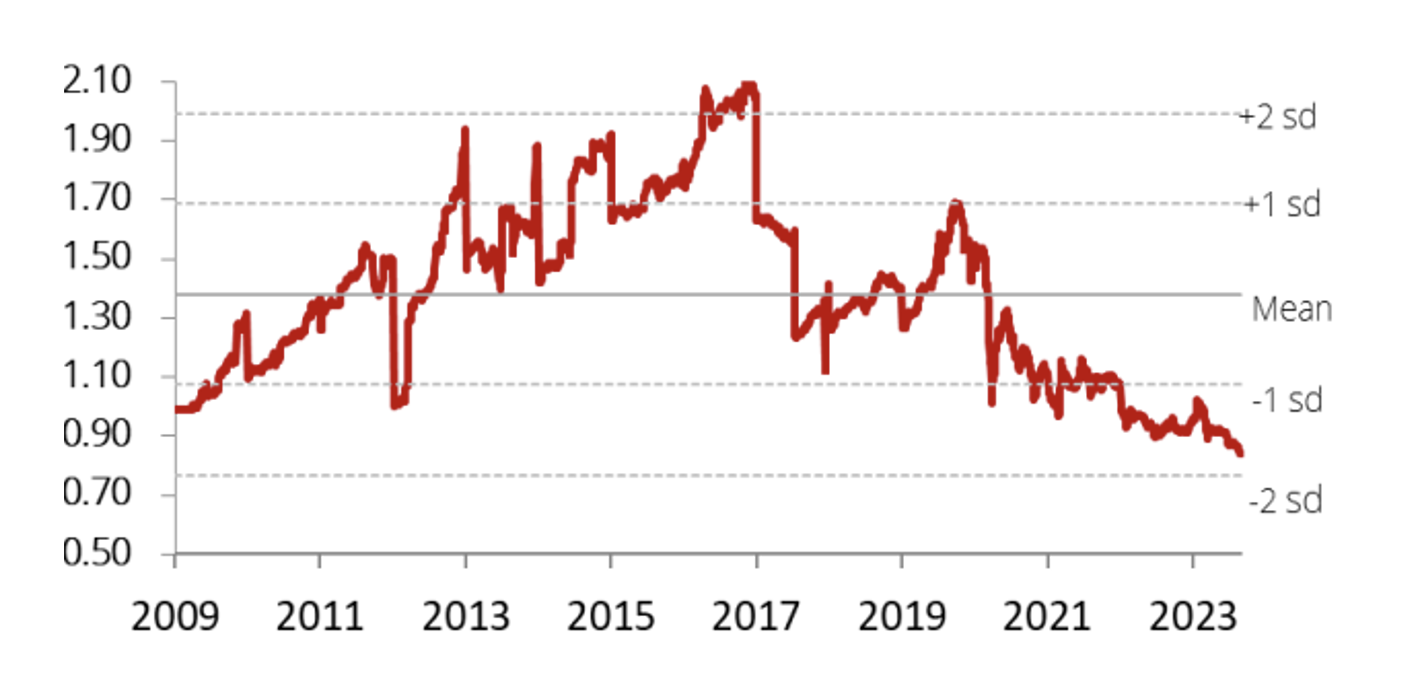

- The market prices of real estate funds are currently lower than historical levels, trading below their net asset value (NAV) at a ratio of 0.84 times, compared to 1.41 times in the past.

- Although current 10-year government bond yields are higher than during the COVID-19 period, the impacts from factors 1 and 2 have resulted in an overall spread that remains above historical averages (10-year government bond yields at the end of Q3 2023 and 2019 were 3.18% and 1.49%, respectively).

Table 3: Market Price to Net Asset Value (P/NAV) Ratio of Real Estate Funds

Source: Bloomberg, DBSVTH

Considering only the top 5 real estate funds by market capitalization with high liquidity, where market prices may not reflect appropriate values, it is found that these funds have a market price to book value (P/BV) or P/NAV ratio of 0.75 – 1.12 times, indicating that most are still trading below 1 time. This is partly due to the impact of interest rate trends resulting from central bank monetary policies on market prices and the yield spread of real estate funds.

Table 4: Market Prices and P/BV of the Top 5 Real Estate Funds by Market Capitalization

Source: SET

Note: Data as of October 27, 2023