Credit Rating: Another Indicator for Assessing Rental Payments in Real Estate Funds

Real estate investment trusts (REITs) are primarily engaged in leasing properties. Some types of real estate must generate income by leasing to a single master lessee, and may hire a property or hotel manager to manage the properties and pay rent to the REIT, such as hotel and hospital properties.

The master lease may take the form of fixed rent, which specifies a set amount, and/or variable rent, which may be determined based on the performance of the master lessee. Notably, the criteria for variable rent have changed from the previous stipulation that variable rent must not exceed 50% of the fixed rent, according to the announcement by the Securities and Exchange Commission (SEC) No. Tor Jor. 39/2564.

Examples of REITs that generate income through master leases:

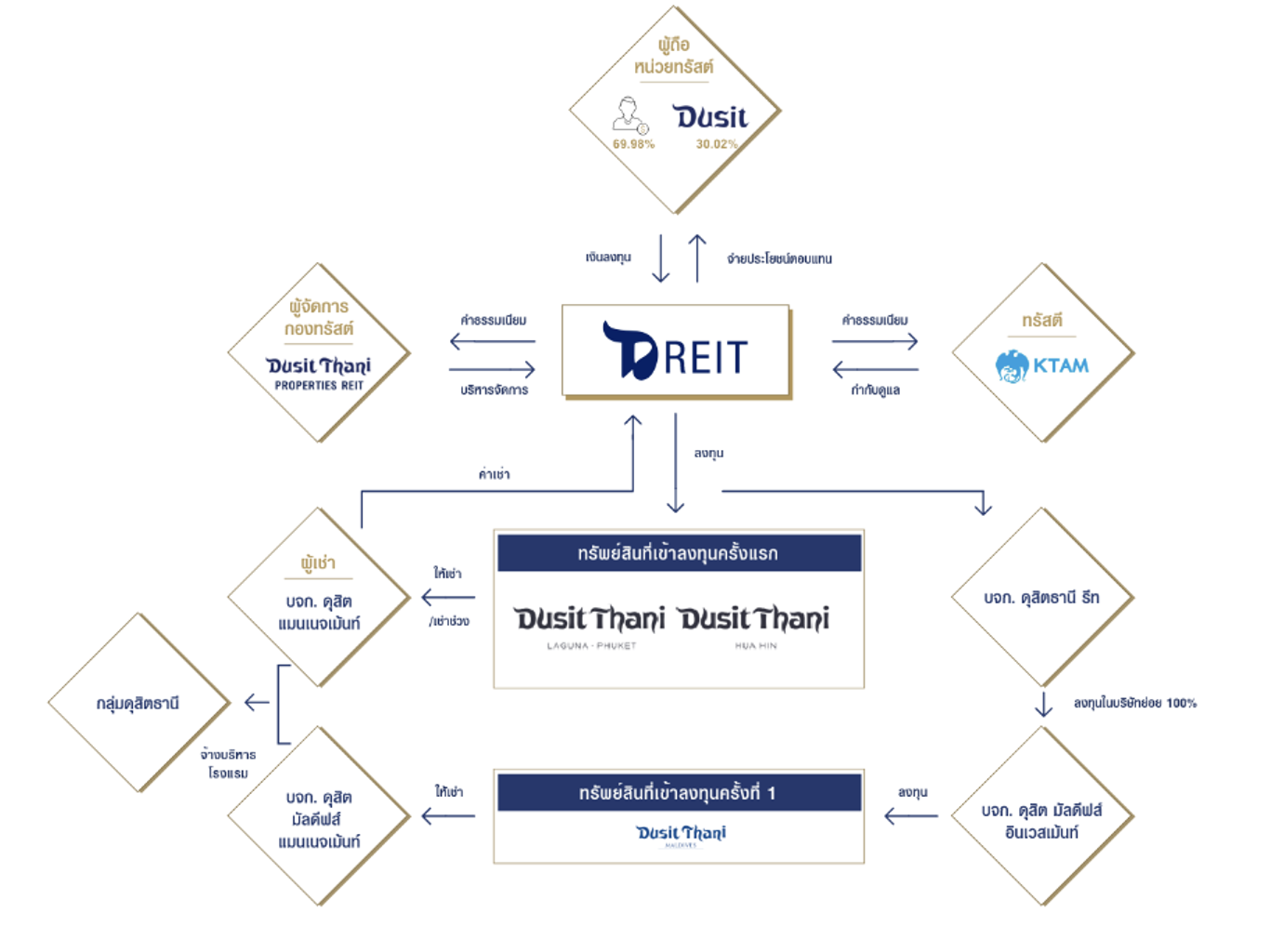

Dusit Thani Real Estate Investment Trust and Leasehold Rights (“DR EIT”)

Source: Dusit Thani Real Estate Investment Trust and Leasehold Rights

However, if a REIT's rental income relies solely on one master lessee, during normal business conditions, the master lessee is likely to be able to pay both fixed and variable rent as per the lease agreement. But in times of business difficulties, the master lessee may not generate sufficient income to meet the rental obligations to the REIT. This could lead to the REIT not only losing income and being unable to distribute returns, but also needing to find a new master lessee due to the breach of contract by the current master lessee. Finding a new master lessee and considering changes can take time, as it requires presentation to the unitholders for approval and may impact the REIT's performance due to the need to reassess lease terms, rental rates, and the hotel brand that may change with a new lessee.

Typically, the first master lessee is often the seller of the property to the REIT (Sponsor) or a subsidiary of the Sponsor. If the master lessee has strong financial stability, it reduces the risk of lease default and inability to pay rent to the REIT. Analyzing this factor may involve considering the credit rating of the master lessee or its parent company.

Establishing the Credit Rating of the Master Lessee or its Parent Company

The credit rating of the master lessee or its parent company can be another factor that investors can use to assess the risk that the master lessee may not be able to pay rent to the REIT, which could affect dividends, especially if the performance of the leased property is impacted. However, it does not directly measure the ability to generate income and profitability of the investment property or the REIT's revenue.

References

- Announcement by the Securities and Exchange Commission No. Tor Jor. 39/2564 regarding the issuance and offering of trust units of real estate investment trusts (No. 20)

- Announcement by the Securities and Exchange Commission No. Tor Jor. 49/2555 regarding the issuance and offering of trust units of real estate investment trusts (Compilation)

- Definition of Credit Rating Symbols

https://www.trisrating.com/files/2416/6391/4118/Symbol-t_23_Sep_2022.pdf