What Happens to the Residential Real Estate Sector When Interest Rates Rise

Assistant Professor Dr. Sukulpath Koompaisarn

Department of Real Estate Development Innovation

In mid-2022, the world faced a crisis following the COVID-19 pandemic, which severely impacted the global economy, particularly the tourism industry. As the COVID-19 situation began to improve, a new crisis emerged immediately due to the Russian military's invasion of Ukraine around the end of February 2022. This is a matter of international politics that the author cannot critique or guide, as it involves decisions made by the leaders of Russia and Ukraine on the global stage. However, the fallout from the Ukraine war has had a severe impact on the global economy, which was starting to recover. This is because both Russia and Ukraine are significant sources of valuable minerals such as uranium and iron, especially oil and natural gas. Russia is the third-largest oil producer in the world, with a production and export volume of 10.7 million barrels per day. When the European Union (EU) collectively suspended the purchase of gas and oil from Russia, it led to an energy crisis across Europe, with oil and natural gas prices increasing by 75% to 120% in several European countries, including Germany, France, Italy, and the United Kingdom. Since oil is a raw material for transportation, rising transportation costs inevitably lead to significant increases in the prices of various goods across agriculture, industry, and services due to higher production costs (Cost-Push Inflation). In other words, if producers cannot bear the increased costs, they will have to raise the prices of goods and services. Additionally, some Russian products, such as wheat, soybeans, fertilizers, and various grains, have also been suspended from trade by the EU, the United States, and Australia. With fewer products available in those markets but increased demand, prices have risen. Consumers are looking to buy more goods and services (Demand-Pull Inflation), and with insufficient supply in the market, sellers have raised their prices accordingly. This issue of rising prices is not limited to Europe; it has also affected Thailand, as evidenced by the daily increases in oil prices during the first quarter of 2022 and the rising costs of essential construction materials like rebar and structural steel. This situation has led to a state of "Inflation", with Thailand currently experiencing an inflation rate of 7.1%, the highest in 14 years (May 2022 - Bank of Thailand).

To mitigate the severe impacts of inflation, the government often employs monetary policy by "raising the policy interest rate" to draw large amounts of money back into financial institutions, reducing investment or spending, and curbing the outflow of money from the country, which helps strengthen the exchange rate. However, increasing interest rates also affects the real estate sector, particularly impacting "homebuyers or mortgage borrowers", who will face higher repayment burdens.

Typically, the Bank of Thailand considers adjusting interest rates at a moderate pace to minimize severe impacts on the overall economy, usually adjusting by no more than 0.25%. For example, the latest policy interest rate (June 8, 2022) was 0.5%. However, financial institutions predict that the policy interest rate will likely increase by 0.25% within the third quarter of 2022, as the Bank of Thailand needs to find ways to slow down the outflow of money to countries with higher interest rates.

The policy interest rate may not directly impact the Thai real estate sector significantly, but it does affect financial institutions, which have the most influence on real estate businesses. Both real estate developers and buyers rely on loans from financial institutions. This article will analyze clear figures showing how much additional burden homebuyers will face if financial institution loan interest rates increase by just 0.25%.

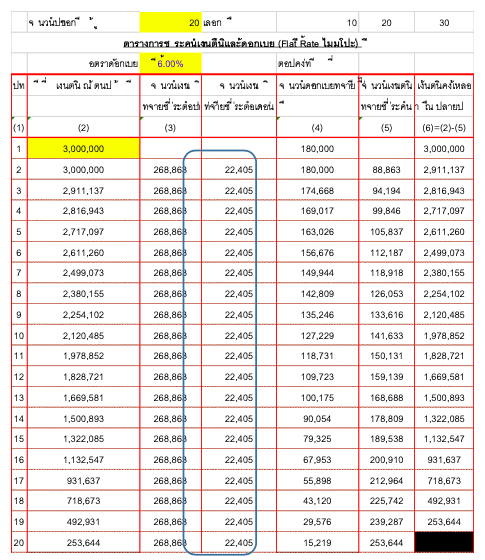

Currently, the average loan interest rate for home purchases (Minimum Retail Rate: MRR) is approximately 6.0% (as of June 17, 2022, from five major banks). Assuming the author purchases a condominium priced at 3,000,000 baht with a loan term of 20 years without refinancing or making extra payments during the 20 years.

Table 1: Principal of 3,000,000 Baht at an Interest Rate of 6.0% for a 20-Year Loan

From Table 1, if the author borrows 3,000,000 baht from the bank under the stated conditions, the monthly repayment of principal and interest would be approximately 22,405 baht, or about 268,863 baht per year. However, if the bank raises the interest rate by 0.25% to 0.50%, the author will face increased repayment amounts as shown in Table 2.

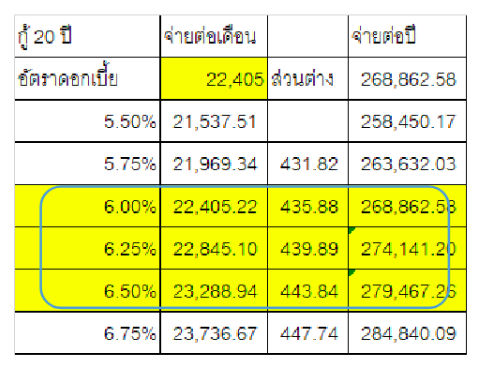

Table 2: Additional Monthly Payments if Interest Rates Increase by 0.25% and 0.50%

If the interest rate increases by 0.25%, the author would need to pay 22,845 baht per month, an increase of 440 baht. This translates to an additional annual cost of 5,280 baht. If the interest rate increases by 0.50%, the total monthly payment would be 23,288.94 baht, an increase of approximately 884 baht, resulting in an annual increase of about 10,605 baht.

While the additional payment amounts may not seem significant, they can add up considerably in the case of purchasing a more expensive home. For buyers with lower monthly incomes, these additional payments could mean sacrificing other essential expenses such as food and transportation, creating a burden for those with limited monthly income.

In summary, the global economic situation, characterized by widespread inflation, has led central banks in many countries to announce increases in policy interest rates. This, in turn, forces financial institutions to raise loan interest rates, whether MRR or MLR (Minimum Loan Rate) for large borrowers, resulting in increased monthly payments for borrowers. For many families, these additional payments represent a significant household burden.

As homebuyers, we can strive to pay off loans as quickly as possible, known as "prepayment," to reduce the principal. As the principal decreases, the interest to be paid also reduces. Alternatively, refinancing may be considered based on the most suitable conditions from the bank for the borrower. Personally, I believe that the best way to reduce debt is to avoid borrowing altogether, or if borrowing is necessary, it should be for essential needs such as housing, education, business expansion, or medical expenses. Additionally, it is crucial to understand the conditions of the loan, the interest rates, and to always be prepared for the possibility of fluctuating interest rates. If rates rise or fall, do not panic but be prepared.

Finally, on behalf of the Master of Science program in Real Estate Development Innovation, I encourage all readers to prepare themselves mentally and emotionally for rising inflation, increasing prices of goods and services, and potential economic downturns. I hope everyone can navigate through any crises that may arise successfully. In the next article, I will look at the perspective of entrepreneurs regarding how they will respond if loan interest rates rise.