EIC Evaluates the Trend of New Economic Stimulus Measures from the U.S. and Its Implications for the Economy and Financial Conditions

EIC Evaluates the Trend of New Economic Stimulus Measures

from the U.S. and Its Implications for the Economy and Financial Conditions

|

The large $1.9 trillion economic stimulus package that President Joe Biden is trying to push into effect is another crucial factor that will impact not only the recovery of the U.S. economy but also the recovery of the global economy, U.S. government bond yields, and the U.S. dollar, which will subsequently affect Thai government bond yields and the Thai baht as well. In this article, EIC analyzes two main issues as follows: 1) What size will the measures approved by Congress be? and 2) Will the impact of these measures cause the U.S. economy to overheat, and how will it affect U.S. government bond yields, the U.S. dollar, Thai government bond yields, and the Thai baht?

What is the trend for the new measures?

EIC expects that the Democratic Party will be able to introduce additional economic stimulus measures of around $1.5 - $1.9 trillion within the first quarter of this year through the Budget Reconciliation process.

Typically, President Biden can choose to pass measures in two ways:

- Using the Budget Reconciliation process, which requires only 50 votes from the Senate, the number of senators that the Democratic Party currently has. However, choosing to pass measures through the Budget Reconciliation process has legal limitations that may prevent the passage of measures not directly related to the budget (such as minimum wage increases and social security policies).

- Regular voting, which requires additional support from Republican Party members to achieve at least 60 votes in the Senate, making it likely that the Democratic Party may have to reduce the size of the measures. However, this method would allow for the passage of minimum wage increases.

Given the Republican Party's opposition to the measures proposed by the Democratic Party, the chances of the Democratic Party receiving the full 60 votes for regular voting are very slim. President Joe Biden has therefore chosen to use the Budget Reconciliation process to pass the measures. On February 26, 2021, the U.S. House of Representatives successfully passed the additional economic stimulus bill worth $1.9 trillion. The next step is for this new stimulus bill to receive approval from the Senate, which EIC views as more challenging than passing the House of Representatives, as this bill must receive support from all Democratic senators (or some support from Republican senators to reach 50 votes). From past indications, some Democratic senators have not agreed with the bill proposed by the House of Representatives. Therefore, EIC believes that the measures that pass the Senate may be around $1.5 - $1.9 trillion (smaller than what the House of Representatives proposed), with the most contentious issue being the proposed increase in the minimum wage from $7.25 to $15 per hour, which some senators argue is not directly related to the federal budget and thus cannot pass using Budget Reconciliation. Therefore, measures related to minimum wage increases are likely to be cut, and aid to local governments may also be smaller than what the House of Representatives proposed.

Key measures expected to be introduced in the first quarter of 2021 include:

- Direct payments of $1,400 per person

- Aid to local governments to prevent layoffs

- Extension of unemployment benefits until August 2021 (originally set to expire on March 14, 2021), including an increase in special unemployment benefits to $400 per person per week

- Measures to reopen schools and universities

- Public health measures such as vaccination and virus testing

Will the new measures cause the U.S. economy to overheat?

Recently, there have been concerns that the measures proposed by the Biden administration may be too large, potentially affecting inflation rates and the financial stability of the U.S.. Former Treasury Secretary Lawrence Summers stated that the size of the proposed measures is too large compared to the current output gap, which could lead to a rapid increase in inflation rates and impact the stability of the U.S. dollar and financial stability in the future. Moreover, the $1.9 trillion measure (equivalent to 9.1% of 2020 GDP) does not cover infrastructure and clean energy projects, which are central to Biden's policy. Therefore, using such a large amount of money for this measure may limit future public investment. Additionally, former IMF Chief Economist Olivier Blanchard agrees with Summers' concerns, stating that if the funds from previous measures ($900 billion or 4.3% of 2020 GDP), the new proposed measures ($1.9 trillion), and anticipated infrastructure projects (estimated at $800 billion or 3.8% of 2020 GDP) are combined, it would inject approximately $3.6 trillion into the U.S. economy, which is four times the output gap in the U.S. This raises the risk of the U.S. economy overheating.

However, there is another group of economists who support the proposal for large measures

and believe that it will support economic recovery rather than cause the economy to overheat. Current Treasury Secretary Janet Yellen stated that the current situation requires sufficiently large measures to help the unemployed and compensate for household income lost due to the COVID-19 crisis, and confirmed that the authorities have adequate policy tools to manage inflation in the future, with the risk of inflation rising rapidly still being limited. Yellen also predicts that the $1.9 trillion economic stimulus will help the U.S. economy achieve full employment in 2022. Furthermore, the U.S. Federal Open Market Committee (FOMC) meeting report indicated that the committee is more concerned about low inflation levels than the risk of inflation rising quickly due to additional measures, and that the anticipated increase in inflation is only temporary. IMF Managing Director Kristalina Georgieva also supports the measures, stating that using fiscal policy to assist those affected by COVID-19 is essential during a time of high uncertainty.

EIC believes that the additional economic stimulus measures will support the recovery of the U.S. economy this year, while the risk of the U.S. economy overheating or inflation rising rapidly may still be low in the short term due to:

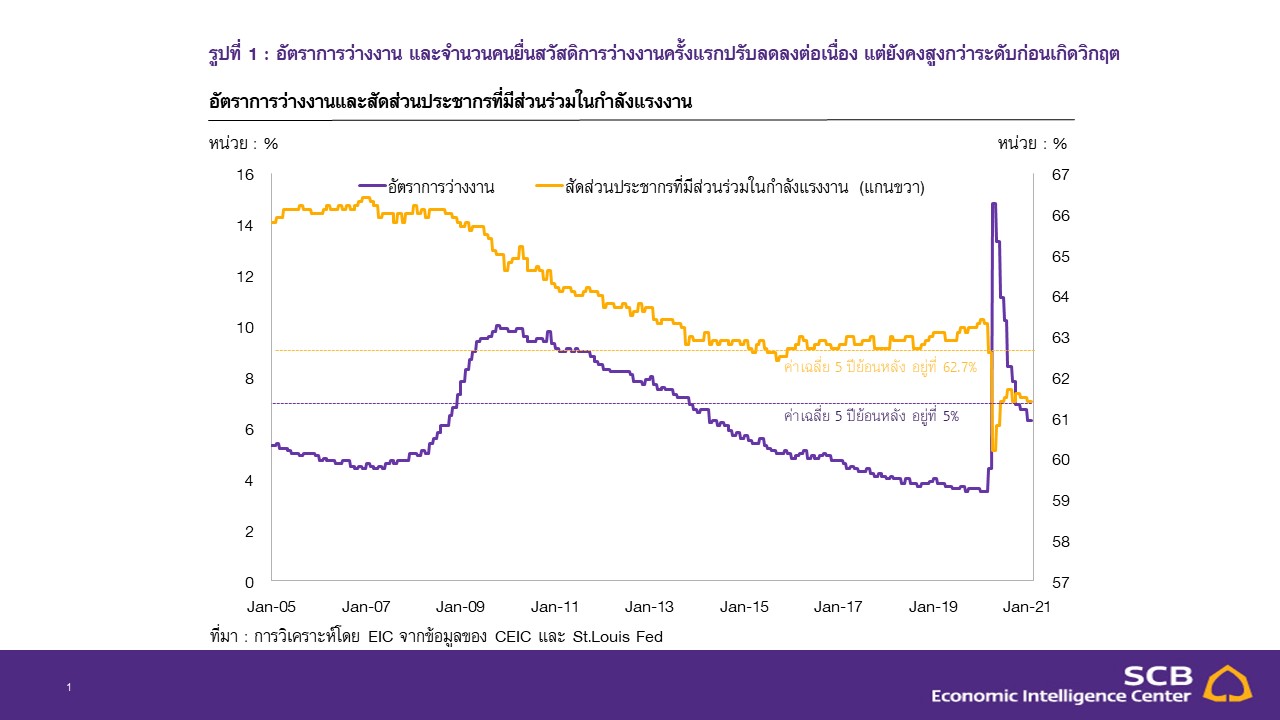

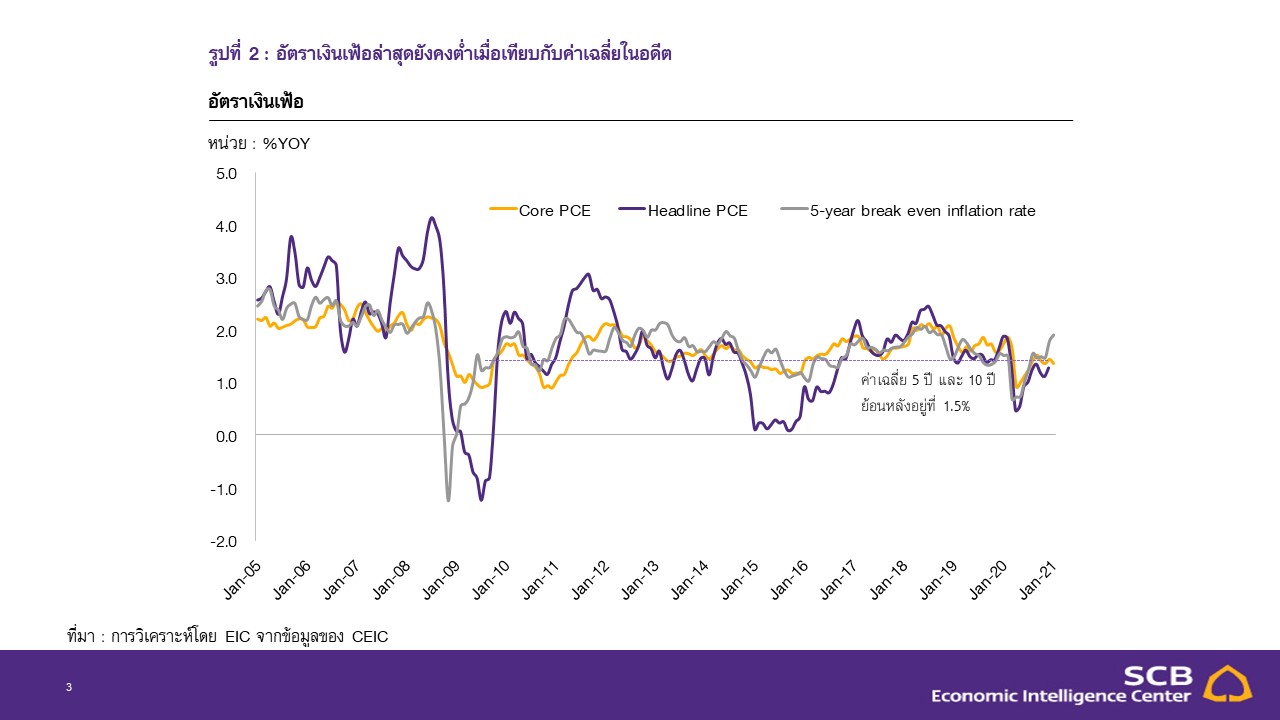

- The U.S. labor market has not yet recovered to pre-COVID-19 levels. Although U.S. GDP is expected to grow this year, the current unemployment rate is at 6.3%, which is still higher than the 5-year average of 5%. Meanwhile, the labor force participation rate is at 61.4%, which is still below the 5-year average of 62.7%. Additionally, the current inflation rate is at 1.3%, lower than the 5-year average of 1.5% and the 10-year average of 1.5%. Therefore, the new economic stimulus measures are likely to help the economy recover faster rather than cause an overheating recovery, as the economy remains below its potential level, or what is referred to as having significant "slack" in the labor market.

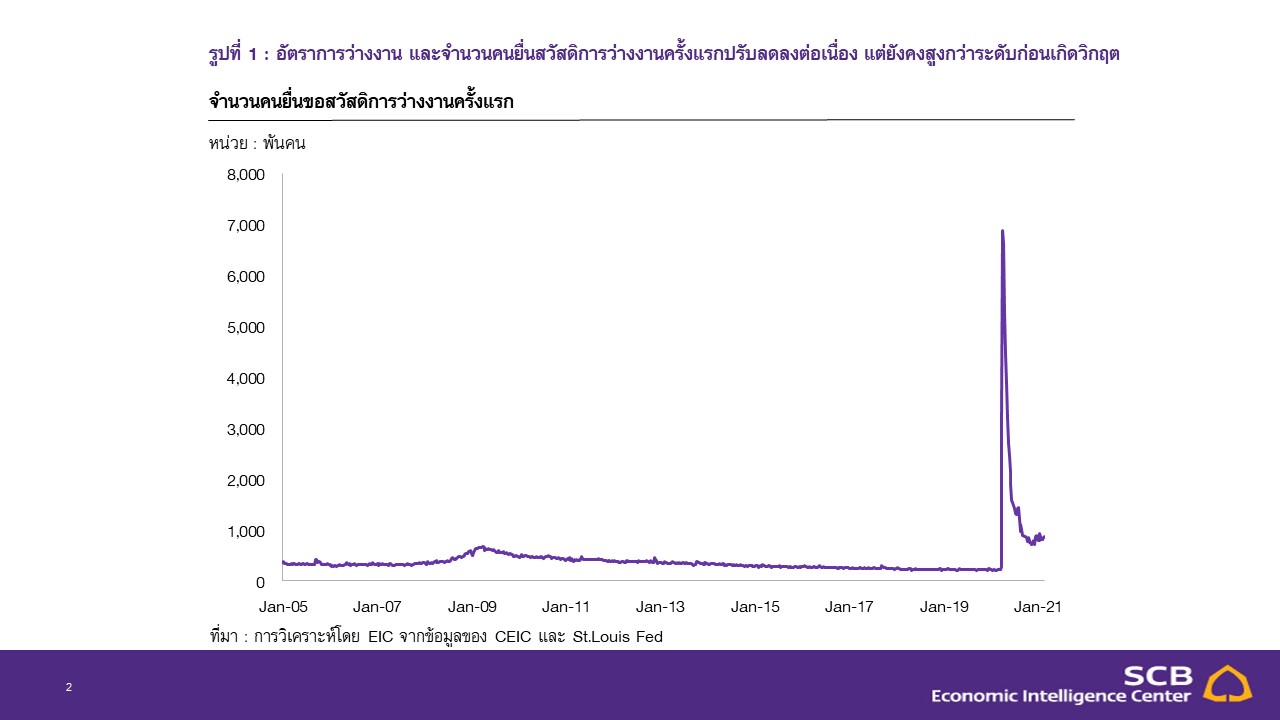

- Most of the anticipated additional measures are one-off cash injections, such as direct payments of around $1,400 per person and unemployment benefits that will decrease as the economy recovers faster than expected, as the number of unemployed will also decrease (automatic stabilizer). EIC estimates that the impact of the anticipated measures will likely stimulate the economy the most in the second quarter of 2021 and will gradually decline in subsequent quarters, thus reducing the risk

of the economy overheating or inflation rising rapidly.

However, the risk of inflation accelerating in the medium to long term remains a concern due to other structural factors that may enhance the effects of the stimulus measures, leading to inflationary pressures rising faster than expected and potentially causing financial market volatility. Examples of factors that could lead to inflation accelerating faster than expected in the medium to long term include:

- Increased liquidity in the system from both government and central bank assistance measures in the past, which is likely to continue to rise due to both asset purchase measures and this new package, could pressure prices of goods and services to rise faster than in the past.

- Pent-up demand for consumption and increased excess savings. Previously, control measures prevented households from fully consuming certain goods and services. After lockdown measures ease, there is a tendency for consumption demand to increase significantly, and savings may be spent quickly, leading to rapid price increases for goods and services.

- Reduced international trade may lead to decreased supply of goods. The ongoing tension between China and the U.S. may affect global supply chains and could result in shortages of certain goods in some regions, which would lead to price increases.

- Demographic factors related to an aging population may increase prices for certain goods. The declining proportion of the working-age population and the increasing proportion of the elderly may reduce domestic production levels, leading to higher prices. Additionally, rising healthcare service costs associated with an aging population will also exert inflationary pressure.

- The psychological impact on investment trends may be less than expected. In this crisis, businesses are likely to resume investment expansion after the crisis subsides more than in previous crises, especially large businesses that can adapt to the new normal. This is different from the global financial crisis, where the root cause was excessive investment in risky assets, leading to reduced risk tolerance among businesses.

Whether the measures proposed by Biden will be too large is still difficult to assess at this time. The $1.9 trillion measure is very large compared to measures already implemented and is significantly larger than measures taken during the 2008-2009 financial crisis. Therefore, the risk of the economy overheating in the future cannot be overlooked. However, implementing additional measures is currently the most important thing to help households and businesses affected. Additionally, the impact of implementing smaller measures may be more detrimental than the impact of implementing larger measures. Thus, it is a challenge for the government to manage the risks that may arise from implementing additional measures, while preparing tools to monitor inflation and continuously watch key economic indicators to adjust measures promptly when signs of overheating economic growth are detected.

Figure 1: The unemployment rate and the number of first-time unemployment claims continue to decline but remain higher than pre-crisis levels

Source: EIC analysis based on CEIC and St. Louis Fed data

Figure 2: The latest inflation rate remains low compared to historical averages

Source: EIC analysis based on CEIC data

What is the impact of the new measures on financial conditions?

The large U.S. economic stimulus measures will lead to an increase in long-term U.S. government bond yields

and will be a factor in the strengthening of the U.S. dollar. Since January 14, 2021, when the Democratic Party proposed the $1.9 trillion measure, the yield on 10-year U.S. government bonds has risen by 28 bps to 1.41% (as of March 1, 2021), and the U.S. dollar index has slightly strengthened by 0.9% to 91 after continuously depreciating throughout 2020. This package impacts U.S. government bond yields and the U.S. dollar through the following channels:

- Increased expectations for the recovery of the U.S. economy. Before the announcement of the economic stimulus measures, a Bloomberg survey indicated that market participants estimated the U.S. economy would grow by 4.1% in 2021. However, this forecast has significantly increased to 4.9%, contrasting with the forecasts of other major economies such as the Eurozone and Japan, which have been revised downwards. At the beginning of the year, they were expected to grow by 4.6% and 2.7%, respectively, but have recently been revised down to 4.2% and 2.6% due to the government re-implementing stricter COVID-19 control measures. As a result, U.S. government bond yields have risen due to decreased demand for U.S. government bonds (safe assets), while the U.S. dollar has begun to stabilize after continuous depreciation last year, consistent with the number of short positions in the dollar also stabilizing.

- Increased expectations for U.S. inflation. The inflation forecast for the U.S. in 2021 from a Bloomberg survey as of March 1, 2021, is at 2.2%, up from the early-year forecast of 2.0%. The three-year inflation forecast for households as of January 2021 is at 3.03%, up from the previous month’s 2.90%. The anticipated increase in inflation is likely to raise the inflation risk premium, leading to a quicker rise in government bond yields.

- Market expectations regarding the Fed's potential tapering of monetary policy may occur sooner than expected. EIC estimates that the Fed will maintain its policy interest rate until 2024, as the current monetary policy framework has been adjusted to Average Inflation Targeting (AIT). Under this framework, the Fed does not need to tighten monetary policy immediately when inflation approaches or hits 2% in any given month, but will consider the average annual inflation rate of 2%. However, the recovery of the U.S. economy and the potential rapid rise in inflation will pressure market participants to believe that the Fed may begin tapering its asset purchases sooner. A Bloomberg survey conducted from January 15 to 20, 2021, indicated that 88% of respondents believe that the Fed's future policy will involve tapering asset purchases rather than increasing them, with about 50% believing that the Fed will begin this process within the next 7 to 12 months. Historically, there have been instances where the Fed announced tapering of asset purchases ahead of investor expectations (Taper Tantrum on May 22, 2013), causing the yield on 10-year U.S. government bonds to rise by 11 bps within just one day and increase by another 85 bps over three months.

However, the severity of the impact of rising long-term government bond yields on financial conditions will also depend on other factors:

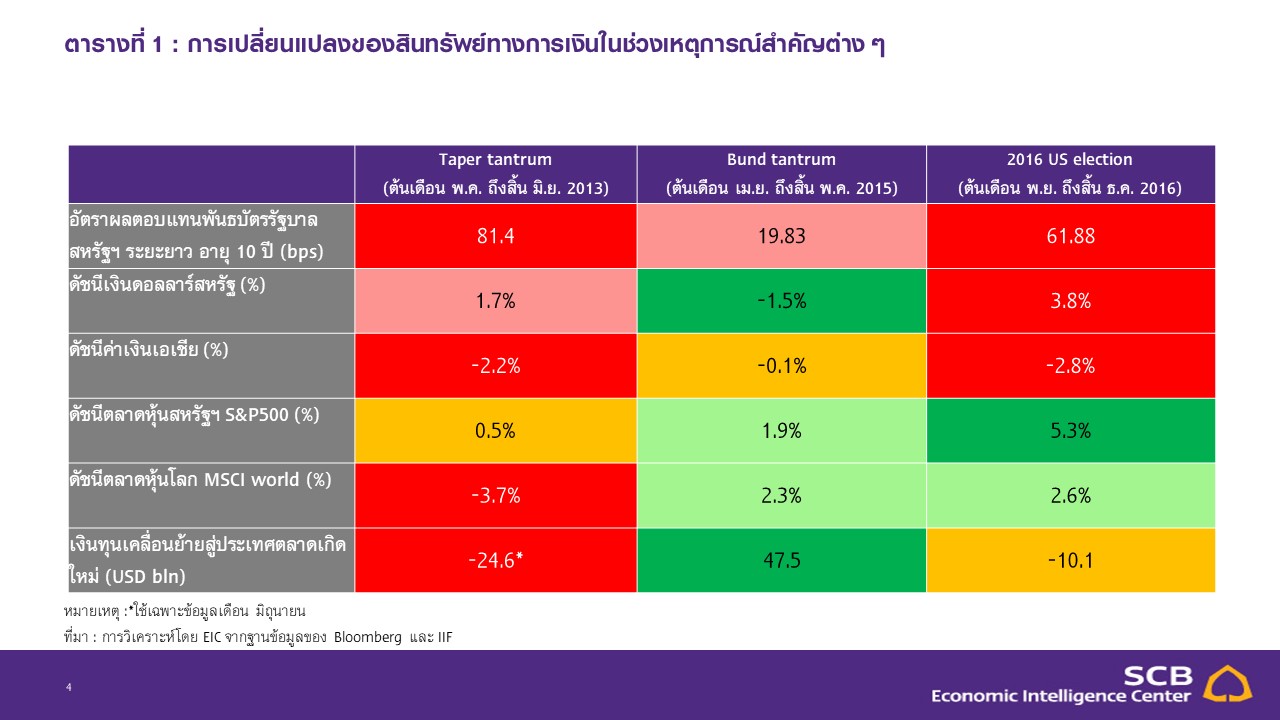

- If investors' outlook on the economy remains positive, the impact on financial conditions will be less severe. The reasons for the rise in U.S. government bond yields may stem from both a shift in investors' outlook on the economy and/or a change in monetary or fiscal policy direction. EIC has found that an increase in government bond yields resulting solely from a change in monetary policy without an improvement in economic outlook tends to have a more negative impact on financial conditions. During the Taper Tantrum, the U.S. dollar strengthened, capital flowed out of emerging markets rapidly, global stock markets declined, and Asian currencies depreciated, which is different from 2015 when global financial conditions did not tighten significantly. In 2016, the rise in U.S. government bond yields was due to both uncertainty from the recent elections and the Fed's interest rate hikes, leading to a stronger U.S. dollar and a significant increase in U.S. stock markets. However, with the global economic outlook improving as well, capital flows did not exit emerging markets as much (Table 1).

- Weak foreign economic conditions will further negatively impact investor confidence at that time. For example, during the Taper Tantrum in May 2013, China's economy was slowing significantly, leading to a deterioration in investor sentiment towards emerging markets, resulting in rapid capital flows back into the U.S., a decline in EM market indices, and a strengthening of the U.S. dollar against regional currencies, severely impacting global financial conditions. However, during the rapid rise in U.S. government bond yields in 2015 and 2016, if investors still had a positive outlook on the Chinese economy, global financial conditions did not deteriorate significantly, as global stock market indices continued to rise and capital flows out of emerging markets were less than during the Taper Tantrum.

Table 1: Changes in Financial Assets During Various Significant Events

Note: *Data for June only

Source: EIC analysis based on Bloomberg and IIF data

EIC has therefore revised its forecast for the yield on 10-year Thai government bonds at the end of 2021 to 1.9 - 2.0% (up from 1.5 - 1.6%) in line with the upward trend of long-term U.S. government bond yields and the gradual recovery of the Thai economy. Regarding the Thai baht, EIC maintains its forecast that the baht at the end of 2021 will remain stable

within the range of 29.5 - 30.5 baht per U.S. dollar, as the U.S. dollar is not depreciating and is expected to remain stable.

Additionally, Thailand's current account balance is only slightly in surplus. (Details of the forecast for Thai government bond yields and the Thai baht can be found in the Q1 2021 Outlook, which can be downloaded from the website www.scbeic.com in mid-March.)

The Long-Term Impact of the New Measures on the Economy

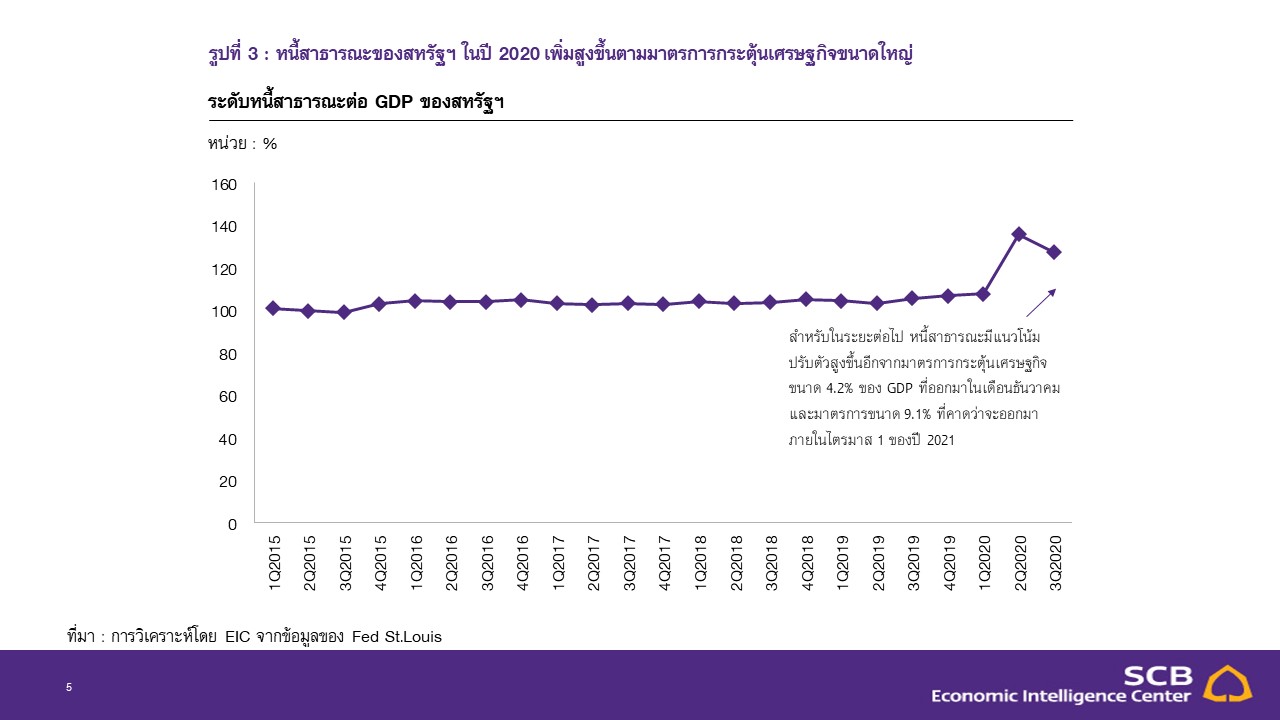

The effects of the large measures not only raise concerns about the overheating

of the economy but also the rising burden of public debt. The latest level of U.S. public debt is at 127.3% of GDP, and if the government introduces additional large measures, public debt will increase rapidly, which could pose a risk to the growth of the U.S. economy in the future. This is because the rising public debt will increase the tax burden on households and businesses. Additionally, the increased debt level will lead to higher yields on government bonds and corporate bonds, which will reduce incentives for business investment and may decrease overall productivity and wage levels, negatively impacting long-term economic growth.

Figure 3: U.S. Public Debt Increased in 2020 Following Large Economic Stimulus Measures

Source: EIC analysis based on Fed St. Louis data

However, even though U.S. public debt is at a high level, EIC believes that the impact on fiscal sustainability will still be limited because:

- Current interest rates are low and are expected to remain low. The low interest rates mean that the interest burden of U.S. public debt remains at only 1.7% of GDP (similar to the global financial crisis in 2008, even though the current level of public debt is nearly double). With this low interest burden, the overall tax burden and the risk of future defaults are not expected to rise significantly, and it is anticipated that

it will not lead to significant reductions in private sector investment. - There is expected to be significant investment in infrastructure, which is part of Biden's core policy, that will help the economy grow well in the long term. For example, investments in clean energy technology and 5G technology will help improve U.S. economic growth in the long term through increased productivity, unlike general income compensation measures that focus on accelerating private consumption and employment in the short term.

Given the current environment where borrowing does not carry a high interest burden, along with the government's ability to increase investment to restructure the economy as proposed, the impact of this large debt may not significantly affect fiscal sustainability. Therefore, implementing large measures may not be as detrimental as it seems in a situation where households and businesses face economic scars from the COVID-19 crisis. However, risks and fiscal sustainability remain issues to monitor, particularly regarding the risk of a fiscal cliff and rapidly increasing public debt due to lower-than-expected government revenue (from various tax increases under Biden's policy).

Analysis from... https://www.scbeic.com/th/detail/product/7419

By: Dr. Kampon Adireksombat ([email protected])

Senior Director and Head of Economic and Financial Market Research

Wachirawat Banchuen ([email protected])

Senior Economist

Dr. Paphon Kiatsakuldecha ([email protected])

Analyst

Pongsakorn Srisakawakul

Analyst

Economic Intelligence Center (EIC)

Siam Commercial Bank Public Company Limited

EIC Online: www.scbeic.com

Line: @scbeic