EIC Forecasts Economic Recovery of CLMV in 2021 Will Differ, with Vietnam Recovering Faster Due to Strong Exports

EIC forecasts that the economic recovery of CLMV in 2021 will vary, with Vietnam recovering quickly and continuously due to strong exports, while other countries will recover more slowly, particularly Myanmar, which is currently facing political unrest.

.jpg)

February 18, 2021

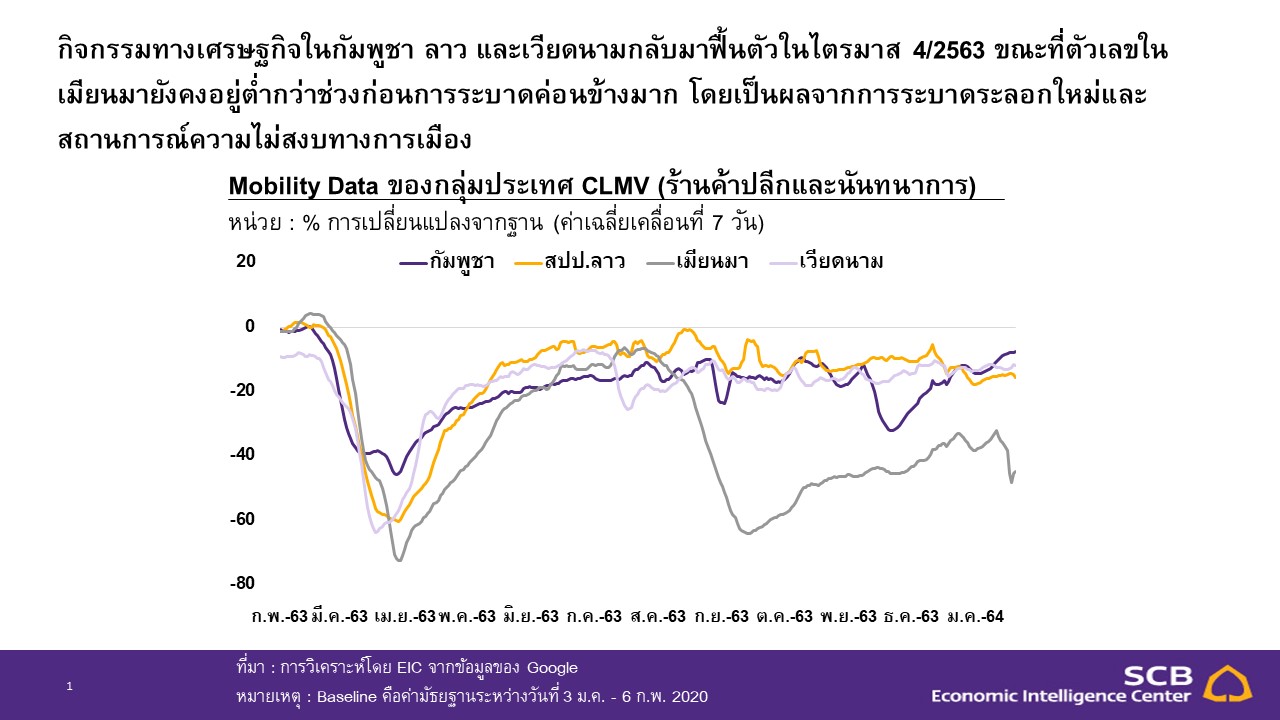

The global economic recession and the COVID-19 pandemic have severely impacted the economy of CLMV in 2020, with Vietnam and Myanmar experiencing a noticeable slowdown. Meanwhile, Laos and Cambodia faced contractions due to negative factors, with Laos struggling with a downgrade in credit rating and high public debt, limiting the scope of economic relief measures. Cambodia, on the other hand, lost its Everything But Arms trade preferences from the European Union, affecting its export sector. Overall, while the CLMV economy showed signs of recovery from its lowest point in the second quarter of 2020, the recovery has been gradual, except for Vietnam, which benefited from strong exports, particularly in electronics, and successfully controlling the COVID-19 outbreak.

EIC identifies three main factors for the economic recovery of CLMV in 2021:

1) The effectiveness of COVID-19 containment measures and the progress of widespread vaccination.

2) The size and effectiveness of government measures to mitigate the economic scarring effects while waiting for herd immunity in the region, expected to occur in 2022.

3) Country-specific risks, such as the risk of default by the Lao government and the political uncertainty erupting in Myanmar. The economic recovery trends of CLMV in 2021 can be considered on a country-by-country basis as follows:

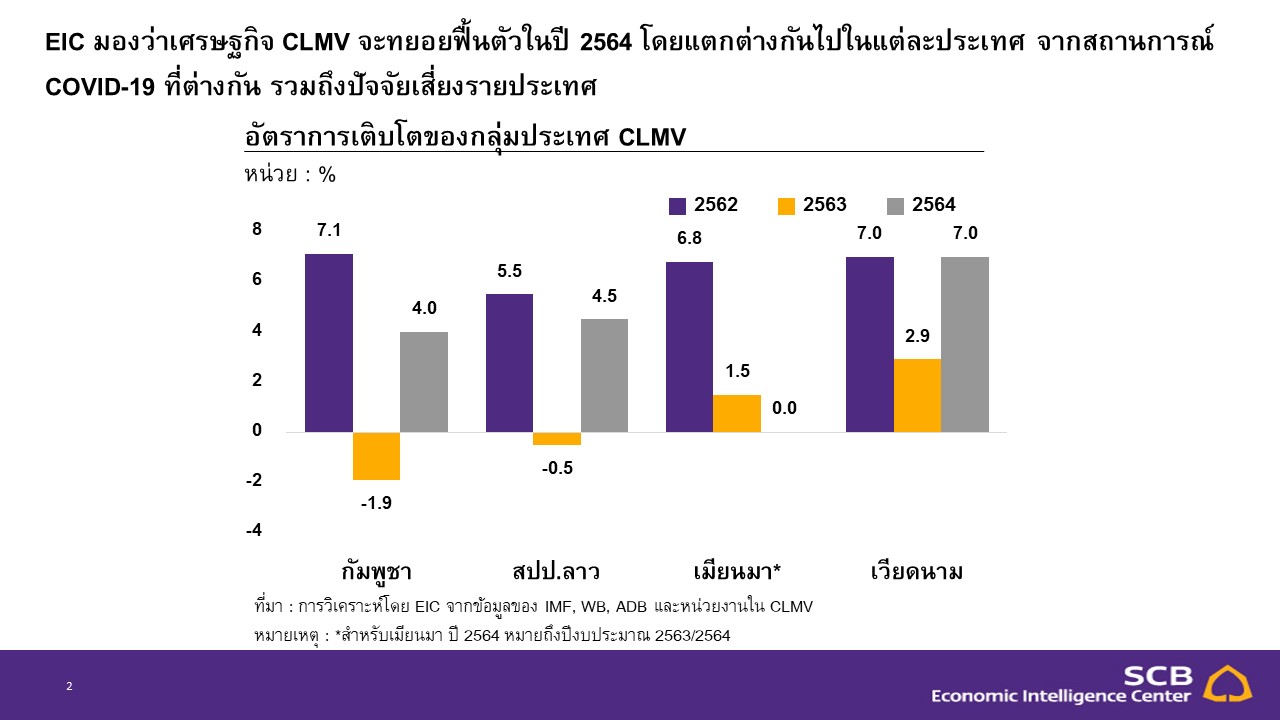

- The Vietnamese economy is expected to continue growing, with EIC forecasting a growth rate of around 7.0% in 2021 (up from 2.9% in 2020) driven by strong exports and a recovering domestic demand. However, a risk to watch is the U.S. designating Vietnam as a currency manipulator, which, while not yet resulting in additional sanctions, poses a risk to Vietnam's future exports.

- The Cambodian economy is expected to gradually recover, supported by exports to China under the recently signed China-Cambodia Free Trade Agreement (CCFTA), with growth projected at 4.0% in 2021 (up from -1.9% in 2020). However, the high dependence on foreign tourism (14% of GDP) will continue to be a major drag on Cambodia's recovery until vaccines are widely available in the region.

- Fiscal constraints will lead to a slow recovery for the Lao economy, with EIC forecasting a growth of 4.5% in 2021 (up from -0.5% in 2020) as the Lao government continues to face public debt management issues, limiting options for funding economic stimulus measures. Investments in various infrastructure projects from China will be a crucial support for Laos's economic growth moving forward.

- EIC has revised Myanmar's economic growth forecast down to 0.0% for the fiscal year 2020/2021 (down from 1.5% in the fiscal year 2019/2020) and still sees significant downside risks, as Myanmar is the only country in the CLMV group still facing a COVID-19 outbreak. The political uncertainty in Myanmar poses a significant risk to the region, with potential foreign sanctions impacting both Myanmar's economy and its trading partners in terms of trade and investment.

For Thailand's economy, trade and investment between Thailand and CLMV are expected to recover slowly, with considerable downside risks, particularly in trade and investment with Myanmar.

- In the second half of 2020, Thailand's exports to CLMV continued to recover slowly, while Thai direct investment (TDI) showed signs of having passed the lowest point. Overall, Thailand's exports to CLMV contracted again starting from the fourth quarter of 2020 (-12.0% YOY from -6.3% YOY in the third quarter of 2020), with the decline in exports to Myanmar (-19.1% YOY in the fourth quarter from -5.4% YOY in the third quarter) being the main drag due to the increase in infection rates affecting border control measures and putting pressure on demand for Thai goods. Meanwhile, exports to Vietnam continued to recover (growing 3.6% YOY in the fourth quarter from a contraction of -5.8% YOY in the third quarter), led by automobiles and parts. For TDI, it grew by 26.1% YOY in the third quarter of 2020, up from 3.9% YOY in the second quarter, primarily in Vietnam (49% share) and Myanmar (22% share).

- However, the recovery in 2021 is expected to be slow and uneven, in line with the recovery of the CLMV economies, and there are still high risks, especially in trade and investment in Myanmar. Trade and investment with Vietnam are expected to show a clearer recovery trend compared to other countries, following the continuous recovery of Vietnam's economy, while trade and investment with the remaining countries still face considerable risks, particularly in Myanmar, where trade and investment are likely to be delayed due to political uncertainty.

In the medium term, the Regional Comprehensive Economic Partnership (RCEP) will be another support for trade and investment in the region, as RCEP is the largest international trade agreement by economic size (29% of global GDP). The significant impacts on the economic outlook of member countries include:

- China, Japan, and South Korea will benefit the most from trade due to reduced tariff barriers, while ASEAN countries, including Thailand and CLMV countries, will benefit to a limited extent. RCEP is the first major trade agreement that reduces tariffs among the three East Asian countries, while ASEAN countries, including CLMV and Thailand, already have low tariff barriers under the ASEAN Free Trade Agreement (AFTA) and the ASEAN Plus One bilateral trade agreements with five major Asia-Pacific trading partners (China, Japan, South Korea, Australia, and New Zealand).

- CLMV countries will benefit significantly from the reduction of non-tariff trade barriers under the modern trade provisions of RCEP, particularly in services, investment, and the use of uniform rules of origin. Additionally, RCEP sets specific provisions for Cambodia, Laos, and Myanmar, which are less developed countries, allowing them time to gradually reform their laws and regulations to align with the RCEP trade network, which will have a limited impact on local businesses.

- In the long term, Thailand will benefit positively from the uniform rules of origin under RCEP, as well as developments in CLMV countries. Thailand can elevate itself to become a regional investment hub, focusing on developing high-value-added manufacturing in the country and relocating labor-intensive production to neighboring CLMV countries that are growing.

Read the full analysis at...https://www.scbeic.com/th/detail/product/7392

Author of the analysis: Dr. Kampon Adireksombat ([email protected])

(Senior Director and Head of Economic and Financial Market Research)

Dr. Paphon Kiatsakuldecha ([email protected])

Analyst

Punn Pattanasiri ([email protected])

Analyst

EIC Online: www.scbeic.com

Line: @scbeic