Impact on Thailand When Biden Does Not Come with a Blue Wave

KKP Research from Kiatnakin Phatra Financial Group analyzes the "Impact on Thailand When Biden Does Not Come with a Blue Wave" and observes that:

- Biden + Split Congress = It will be difficult to pass various policies into law, especially those with significant differences in opinion, such as tax increases and minimum wage hikes.

- Trade uncertainty will decrease, but pressure on China through a multilateral approach and the desire to decouple supply chains will continue.

- Thai exports will improve in the short term due to Biden's trade policies, but Thailand will lose its competitive edge in the long term if it does not join the TPP.

After the U.S. general election concludes, Joe Biden from the Democratic Party is expected to be elected as the 46th President of the United States, while Donald Trump continues to protest the election results and will bring the matter to court to determine if there were irregularities with mail-in ballots. However, even with recounts and audits in each state, the likelihood of overturning the election results in favor of Donald Trump is low.

In terms of Congress, although the election results are not yet finalized, there is a high chance of a 'Split Congress', meaning the Democrats will control the majority in the House of Representatives while the Republicans will hold the majority in the Senate, rather than a Blue Wave (Democrats controlling both chambers). This is due to the latest scores showing Republicans leading 50-48 seats, but two Senate seats in Georgia did not have any candidates receiving over 50% of the vote, necessitating a run-off election on January 5, 2021. If the Republicans win just one seat, they will maintain a majority in the Senate; however, if the Democrats win both run-off elections, they will regain an advantage in the Senate, as the Vice President can act as a tie-breaker. This Split Congress scenario will hinder the push for policies that need to pass through Congress to become law, affecting both short-term and long-term policies, which will impact the economy and financial markets in the U.S. and abroad, including Thailand.

KKP Research assesses the direction of U.S. policies on various issues under Joe Biden's leadership and a Split Congress as follows:

Increased Obstacles to Economic Stimulus Measures

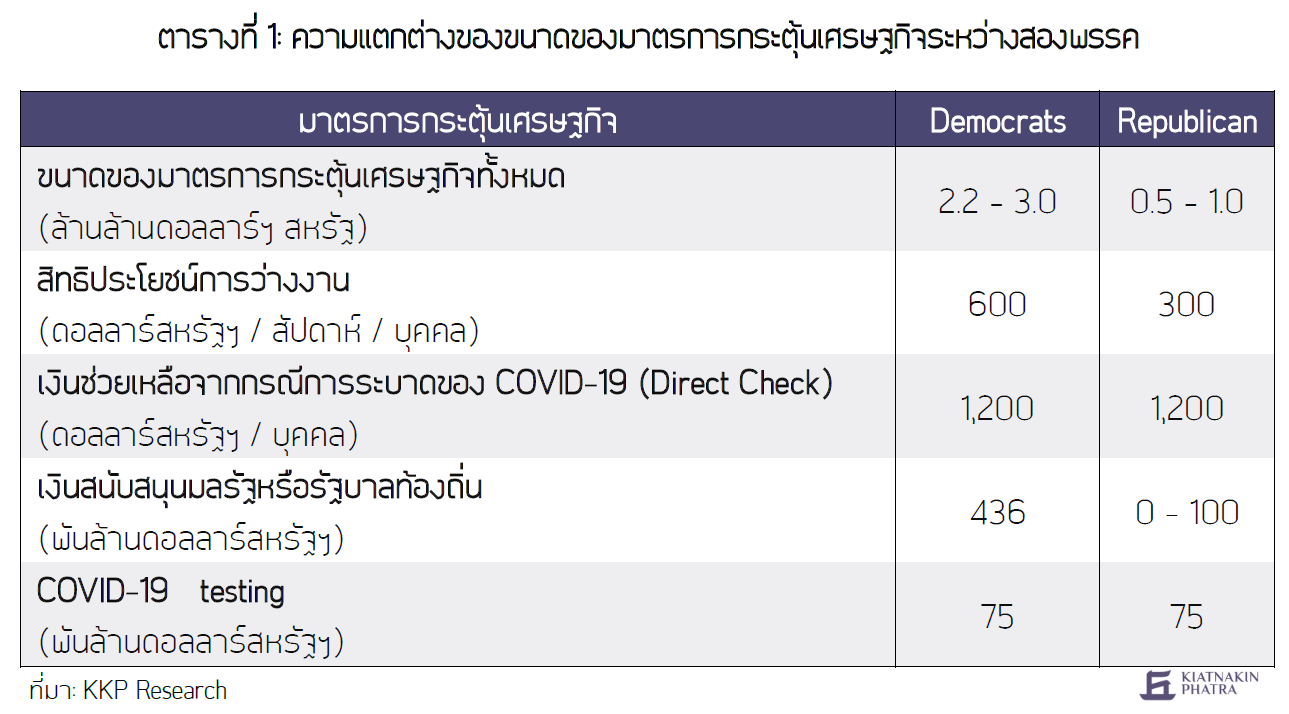

The size of the economic stimulus measures is likely to be smaller than previously discussed and may be delayed due to prolonged negotiations between the government and Congress. Although both the Democratic and Republican parties agree on the need for new relief and stimulus measures, there are still differences regarding the size of the stimulus and the intended use of funds, making it difficult to reach a consensus, posing risks to the recovery of the economy and employment in the U.S. The agreed-upon measures include sending checks to Americans of $1,200 per week per person, as well as budgets for handling COVID-19. However, contentious issues include unemployment benefits and funding for states or local governments, with the amounts proposed by Republicans being significantly lower than those of Democrats.

KKP Research believes that due to these election results and Donald Trump's refusal to accept defeat, there will be no progress in negotiations during the presidential transition period, delaying the new government's operations. Therefore, it is expected that new stimulus measures will only be implemented after the new president takes office on January 20, 2021.

Focus on Controlling COVID-19 Cases, but No Nationwide Lockdown

One of Joe Biden's top priorities upon taking office, referred to as the policy during the first 100 days of the new president, is controlling the spread of COVID-19. Under Donald Trump's leadership, the U.S. failed to manage the COVID-19 situation, leading to a continuous surge in cases. The main policies expected to be implemented include increased support for the World Health Organization (WHO), a campaign for mask-wearing, support for hospitals and healthcare personnel, and procurement of vaccines.

However, without support from Congress and various states, it will be challenging to enact laws mandating mask-wearing and to return to a nationwide lockdown like during the initial outbreak, as many states prioritize reopening their economies.

Rejoining the Paris Climate Agreement

Biden and the Democratic Party prioritize environmental issues and climate change, and they aim to have the U.S. rejoin the Paris Climate Agreement immediately upon taking office to achieve the goal of eliminating carbon emissions or “net zero emissions” by 2050. This rejoining can be done without Congressional approval. Policies that Biden is expected to push to achieve this goal include:

- (1) Increasing environmental measures in infrastructure investment.

- (2) Reducing trade taxes and promoting green investments.

- (3) Requiring businesses to report their environmental impacts and risks.

All these policies will support investments in environmental issues and accelerate the growth of the EV (electric vehicles) market, which will impact the export structures of many countries, including Thailand.

However, the cancellation of oil and natural gas drilling leases will be difficult due to a lack of support from the Republican Party, which will be a significant obstacle to the transition to renewable energy.

Tax Increases and Other Policies Will Be Difficult to Implement

Even though Biden proposes increased government spending along with corporate tax hikes to boost government revenue, a Split Congress may hinder the push for government spending, tax increases, and the passage of budgets and other policies that require legislative approval. While infrastructure investment and R&D investment are likely to be two areas where both parties can agree, Biden's three main tax policies are:

- (1) Increasing the corporate income tax from 21% to 28%.

- (2) Increasing the tax on income from global intangible assets from 10.5% to 21%.

- (3) Imposing a minimum tax of 15% on accounting income from companies with accounting profits exceeding $100 million.

All three of these proposals will not be able to proceed without Congressional approval, and the Republican Party is likely to oppose these proposals. The new government facing obstacles in raising taxes may benefit the U.S. stock market by reducing the risk that companies' revenues will be affected by tax measures under Biden's leadership, as previously feared, especially for technology stocks.

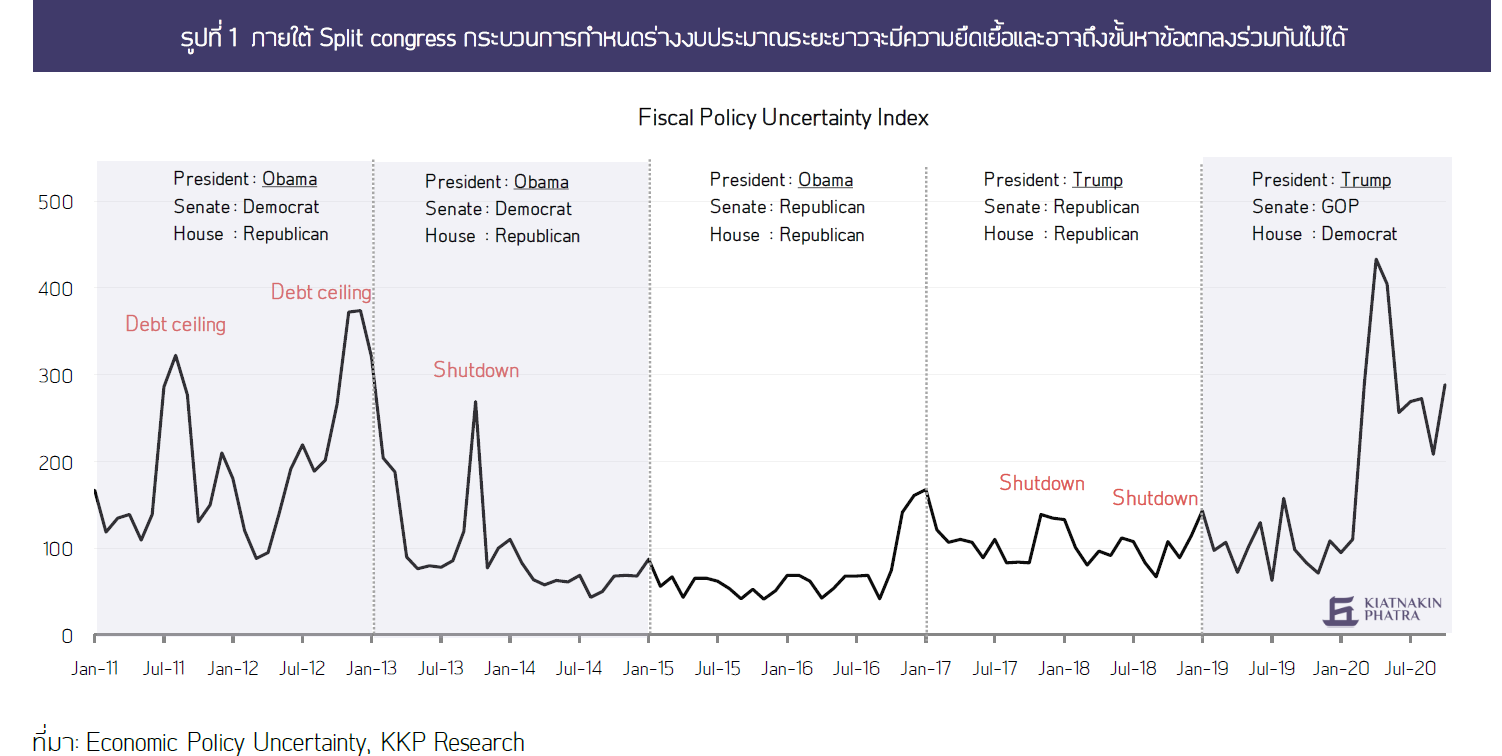

Additionally, under a Split Congress, the process of drafting long-term budgets will be prolonged and may even fail to reach a consensus. There is a risk of a government shutdown and a public debt ceiling crisis in the near future, similar to what occurred during the second half of Barack Obama's first term. Furthermore, other policies proposed by the Democrats, such as raising the minimum wage from $7.25 to $15 per hour, are likely to face opposition from the Republican Party, making it difficult to implement. The inability to raise taxes combined with limited increases in government spending will prevent the U.S. fiscal deficit from rising too high.

The Federal Reserve May Need to Stimulate More

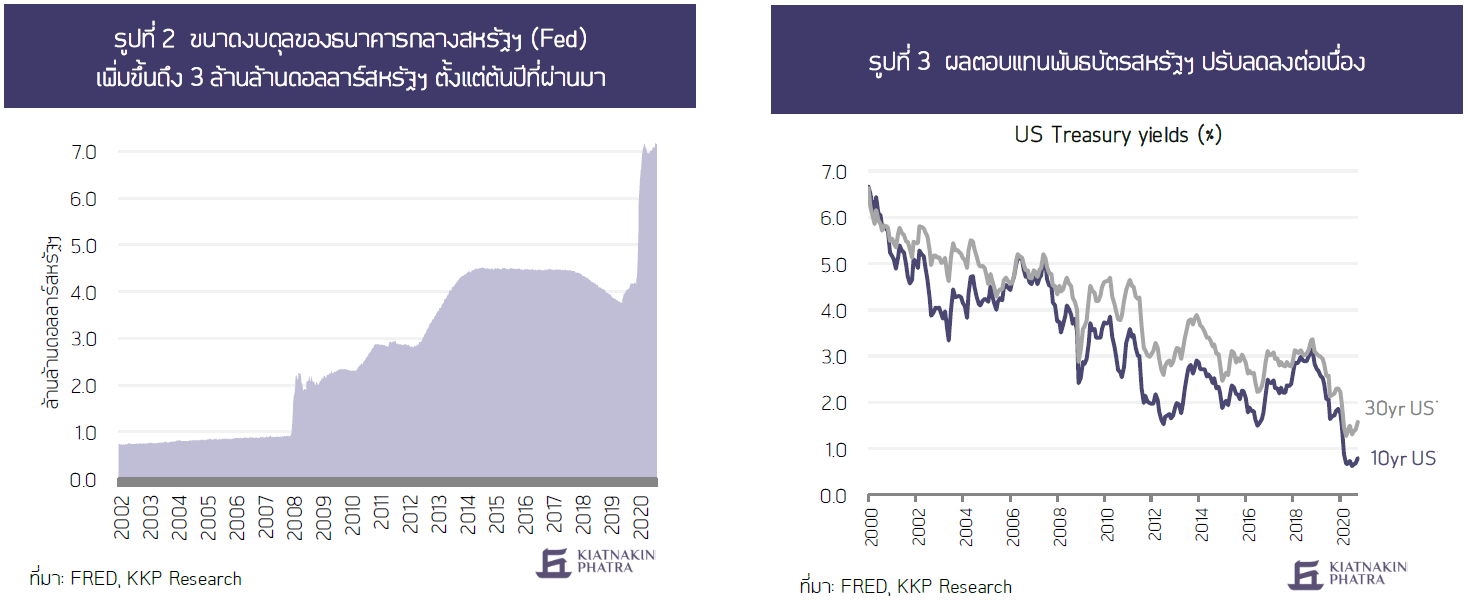

If fiscal measures cannot be implemented significantly to stimulate the economy or take longer to negotiate, it will lead to a more fragile and prolonged recovery of the U.S. economy. This may pressure the Federal Reserve to continue its accommodative policy by keeping interest rates low for an extended period and possibly increasing the amount of QE to compensate for the role of fiscal policy. However, the Fed's balance sheet has already expanded to $3 trillion since the beginning of the year and is expected to continue growing, while both short-term and long-term interest rates in the U.S. are already at the lower bound, limiting the Fed's ability to stimulate further and potentially increasing financial stability risks. However, if an effective vaccine is available and the U.S. economy can recover well, the Fed will continue its accommodative policy for a while but will not increase the amount of QE.

Pressure on China from the U.S. and the Desire to Decouple Global Supply Chains Will Continue

Biden's ascension to the presidency, replacing Trump, is expected to reduce uncertainty regarding U.S. trade policies, which have been a significant factor pressuring global trade over the past 2-3 years, to some extent. It will also help improve trade relations between the U.S. and China and other countries compared to Trump's trade war using import tariffs.

However, China's rapid rise as an economic superpower and its technological advancements will remain a threat in the eyes of the U.S., regardless of which party is in power.

KKP Research from Kiatnakin Phatra believes that pressure from the U.S. on China will continue. In the short term, Biden may not adjust import tariffs as a bargaining tool, but in the long term, the policy to pressure China will shift towards forming alliances to limit China's power, such as bringing the U.S. back into the Trans-Pacific Partnership (TPP) and foreign policy initiatives like the Indo-Pacific Strategy. While trade uncertainties may decrease, tensions between China and the U.S. will persist, along with geopolitical issues in the South China Sea, which may impact Thailand.

Moreover, there will continue to be a trend of decoupling between the U.S. and Chinese economies (US-China economic decoupling) in terms of investment and global supply chains, likely moving away from China back to the U.S. or diversifying to other regions to reduce reliance on imports from China, which may also affect supply chains in Thailand.

Impact on the Thai Economy

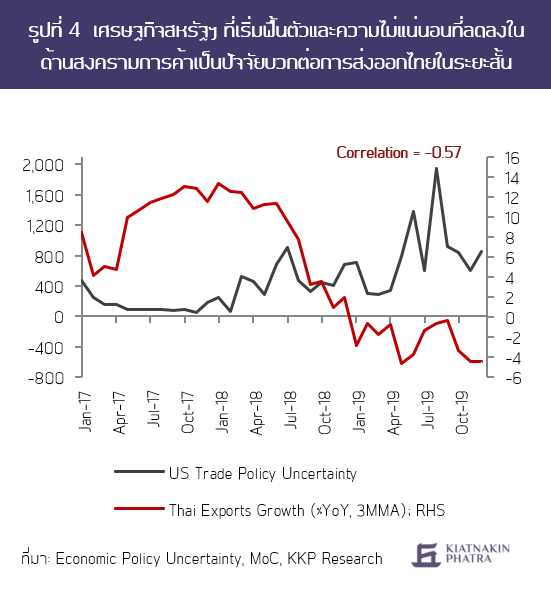

The reduction in trade war uncertainties is a positive factor for Thai exports in the short term. The U.S. economy is expected to recover and likely increase infrastructure investments, coupled with decreased uncertainties regarding the trade war with China, which will lead to improved Thai exports (as shown in the graphs) due to increased demand for imports from the U.S.

However, Thailand may not benefit significantly from the relocation of foreign companies' production bases out of China, partly because (1) U.S. and Chinese companies in high-tech and high value-added manufacturing are likely to reshore to protect their technology, and (2) Thailand lacks the competitive edge to attract investment compared to several countries in the region, especially Vietnam.

Both in high-technology and labor-intensive industries (see KKP Research, "Thai Economy: Can't Go Back, Can't Move Forward Without Technology"), which will limit foreign investment and technology transfer to Thailand.

In the long term, Thailand's manufacturing and export sectors will face increased competition if Thailand does not join the TPP. Although signing the trade agreement requires Congressional approval, which is likely to be contested by both parties, many Republican representatives are supportive of free trade and joining the TPP. Therefore, if the U.S. rejoins, the costs of Thailand not participating in the TPP will significantly increase, as the U.S. is a major buyer in Thailand's export market. Vietnam, a key competitor that is already a member of the CPTPP, will fully benefit from its advantages in labor-intensive industries due to lower wages.

In addition to impacting the competitiveness of Thai exports, this may also affect foreign investors' decisions to invest or relocate their bases, particularly for Japanese investors who are also in the CPTPP, potentially leading to risks of production bases moving out of Thailand due to rules of origin that grant special tariff rates only to products produced and using materials from TPP member countries.

The Thai baht is likely to appreciate in the near term if Biden's COVID-19 control policies succeed and effective vaccines become widely available, supporting a faster and stronger recovery of the global and U.S. economies, leading to a risk-on market environment and increased demand for risk assets, including assets in emerging markets.

Alternatively, if the number of infections remains high, vaccine uncertainty persists, and U.S. stimulus measures are limited, the likelihood of the Federal Reserve needing to stimulate more will increase, which will support a weaker U.S. dollar even if the market returns to a risk-off stance.

Both scenarios support a trend of a weaker U.S. dollar in the near future and a stronger Thai baht against the dollar, which will impact the recovery of Thailand's export sector.

If tensions in the South China Sea escalate, it will pose a dangerous risk to Thai trade. Although trade uncertainties may decrease under Biden compared to Trump, the trend of forming trade blocs with countries in the South China Sea to exclude China and continued support for Taiwan through arms sales may increase the chances of regional tensions and conflicts in the South China Sea. While Thailand may not be directly affected by border disputes, the proportion of Thai trade passing through the South China Sea is high, with the Center for Strategic and International Studies (CSIS) estimating that 74% of all Thai trade passes through the South China Sea. Although the chances may be low, if tensions do escalate, it will inevitably impact Thai trade.

SOURCE: thaipublica