The Differences Between Real Estate Investment Trusts (REITs) and Real Estate Developers

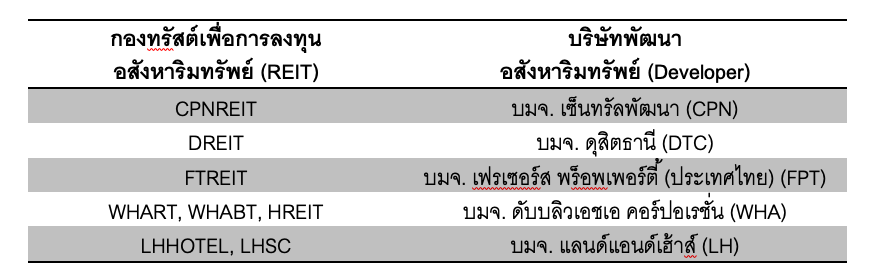

Some may wonder how investing in shares of a real estate development company (Developer) compares to REITs. We can observe that in the stock market, there are both Developer stocks and REITs with similar names investing in the assets of these developers, such as:

Additionally, there are cases where the companies are not related, such as Siam Future Public Company Limited (SF), which is a retail space Developer, compared to BKER, which is a REIT focused on investing in retail space as well. Understanding the differences between Developers and REITs will help clarify the risks and growth trends when comparing them.

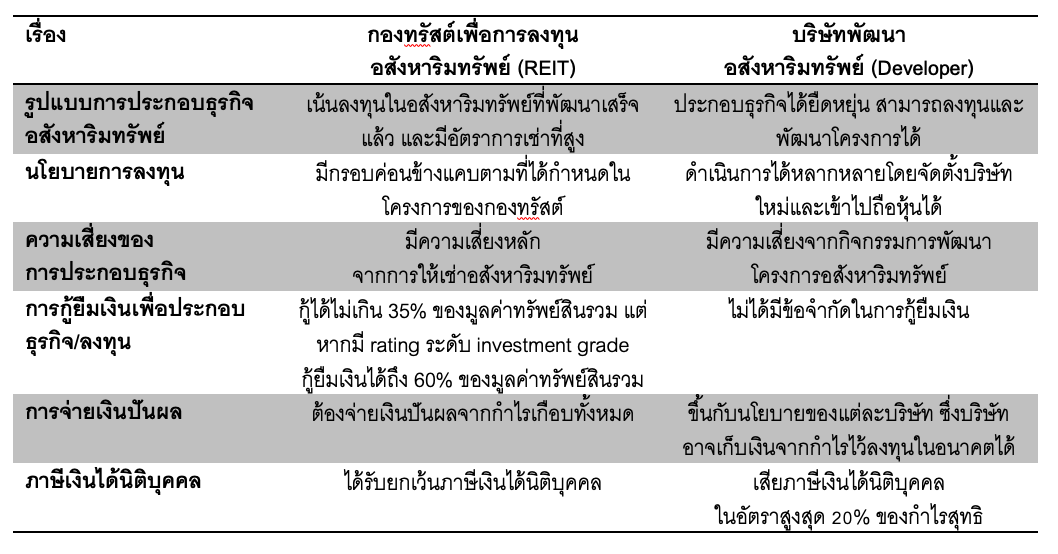

The stock exchange has categorized real estate development companies (Developers) and REITs into the same group, which is the real estate and construction business (PROPCON), but they are not in the same business category. This is partly due to the differences between Developers and REITs, which I will summarize as follows:

In terms of business operations, real estate development companies (Developers) can develop projects in both greenfield and brownfield formats or even renovate properties for different uses. This contrasts with REITs, which focus on investing in completed properties with high occupancy rates. Although regulations allow REITs to invest in greenfield projects, it is limited to 10% of the total asset value. Moreover, no REITs in Thailand have invested in such projects, as most REITs have clear investment policies focusing on specific types of properties. For example, LHHOTEL focuses on hotel properties, while GVREIT focuses on office buildings.

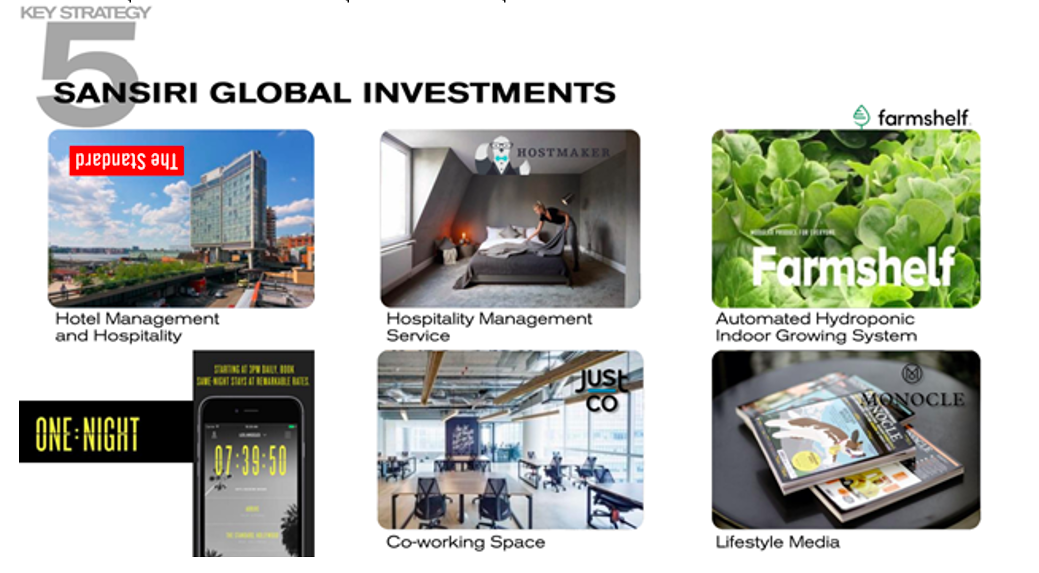

Developers have more flexibility in their business operations, such as joint ventures with other companies, leasing land for project development, managing projects for other landowners, or even engaging in other businesses not directly related to real estate development. Developers can establish new companies and hold shares in them, such as real estate agency companies, property management companies, repair and renovation companies, or even investing in startups that may enhance the supply chain or add value to real estate projects.

Examples of investments in companies not engaged in real estate development and investment by Developers:

Source: Sansiri Public Company Limited

Moreover, Developers have greater flexibility in managing the company's capital for investments and project development, such as:

- Developers do not have the same borrowing limitations as REITs, which can borrow up to 35% of the total asset value, but with a credit rating, they can borrow up to 60% of the total asset value.

- In the market, it is observed that Developers typically have a dividend payout policy of about 40% - 50% of net profit, using the remaining profit to invest in new projects. This dividend payout rate is lower than that of REITs, which must pay out at least 90% of net profit.

Although REITs focus on generating income from leasing and lack flexibility in capital management, resulting in lower returns compared to Developer companies, they carry lower risks and provide returns similar to fixed-income investments with consistent rental income from clearly defined lease agreements. Additionally, REITs have the advantage over Developers of not being subject to corporate income tax, allowing profits from leasing after expenses to be fully distributed as dividends.