Overview of the Office Market in Bangkok Q3/2019

<\/p>

Currently, the Lumphini area has become the location with the highest occupancy rate in the central business district at 96.5%, with an average rental price increase of over 6% compared to the previous quarter. This area is in the heart of the city, surrounded by amenities such as shopping malls, parks, and luxury hotels, along with convenient transportation via the sky train, making it a relatively safe location. Meanwhile, the outer areas on the western side have the highest occupancy rate outside the central business district at approximately 98.8%.

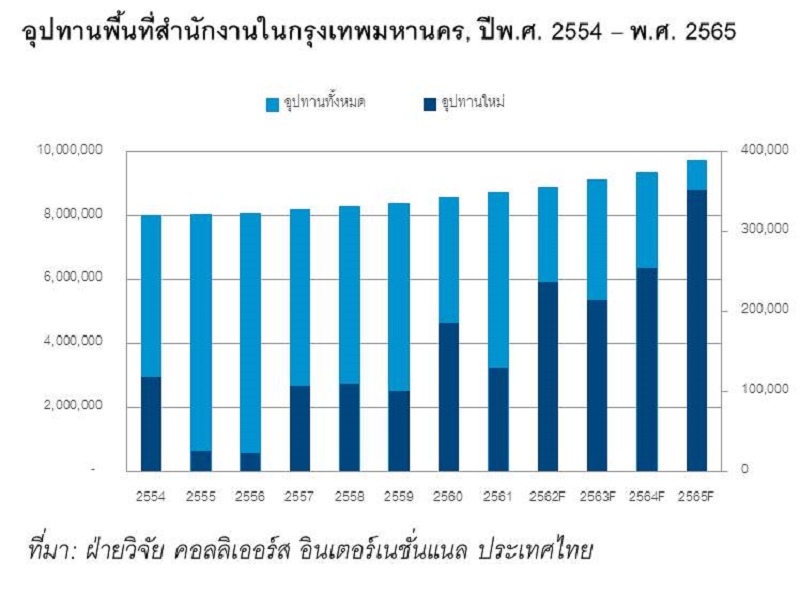

In Q3/2019, one office building was launched: “Mitrtown Office Tower” with a size of 48,000 sq.m. This brings the total number of new office buildings opened in Bangkok to three projects in the first nine months of 2019, with a total rental area of over <\/strong>116,000 <\/strong>sq.m. and a total investment value of over 42,000 million baht. This results in a total office space in Bangkok of 8.764 million sq.m. as of Q3/2019, with an expectation of an additional 77,465 sq.m. of office space to be completed in the final quarter of this year.

The average rental rate in Bangkok continues to grow across all areas, with the average rental price for Grade A office buildings in the central business district reaching as high as 1,500 - 1,600 baht per sq.m., marking the highest increase in several years. It is anticipated that the average rental price for new office buildings to be completed in the future will continue to rise beyond 1,600 baht per sq.m. per month. As of the end of Q3/2019, there was a total office space of 8,387,207 sq.m., with an overall rental rate of 95.7%, leaving only 377,692 sq.m. of vacant space.

<\/p>

Office Space Supply in Bangkok 2011 - 2022<\/span><\/p>

<\/p>

In Q3/2019, Bangkok had a total office space of 8.764 million sq.m. and launched one office project, Mitrtown Office Tower, which is part of the Samyan Mitrtown project, a mixed-use development valued at over 9,000 million baht on an area of over 14 rai, with a total usable area of 222,000 sq.m. on Phaya Thai-Rama 4 Road, developed by Golden Land Property Development Public Company Limited. The Mitrtown Office Tower has a total rental area of 48,000 sq.m. In Q3/2019, there are still approximately 1.3 million sq.m. of office space under construction, expected to be completed between 2019 and 2022. Of the total office space under construction, about 50% will be located in the central business district, and 70% will be Grade A office space. The office space expected to be completed in 2019-2020 remains limited, with 77,465 sq.m. expected to be completed in the final quarter of 2019, while 207,841 sq.m. is expected to be completed in 2020. In 2021-2022, it is anticipated that the office space to be completed each year will increase to 254,000 sq.m. and 350,000 sq.m., respectively. <\/strong> The remaining Grade A office space <\/span><\/strong> is a factor that stimulates further office development. In addition to the Mitrtown Office Tower, there are several other office projects waiting to be launched on Rama 4 Road, such as The PARQ developed by Fraser Property, which has a total rental area of 60,000 sq.m. and is expected to be completed in 2020, and the One Bangkok Phase 1 Grade A office project located on the same road, which has a total rental area of 201,000 sq.m. and is expected to be completed in Q4/2022. In 2019, another office building expected to be completed in Q4/2019 is "Spring Tower," developed by AIRA Property. Spring Tower is a Grade A office building located at Ratchathewi Intersection, comprising a total rental area of 50,000 sq.m. In addition to traditional office space, 'JustCo,' a well-known co-working space developer, will launch a project in Samyan Mitrtown with up to 12,000 sq.m. of space, officially opening in Q4/2019, indicating the growing popularity of the co-working space market. <\/p>

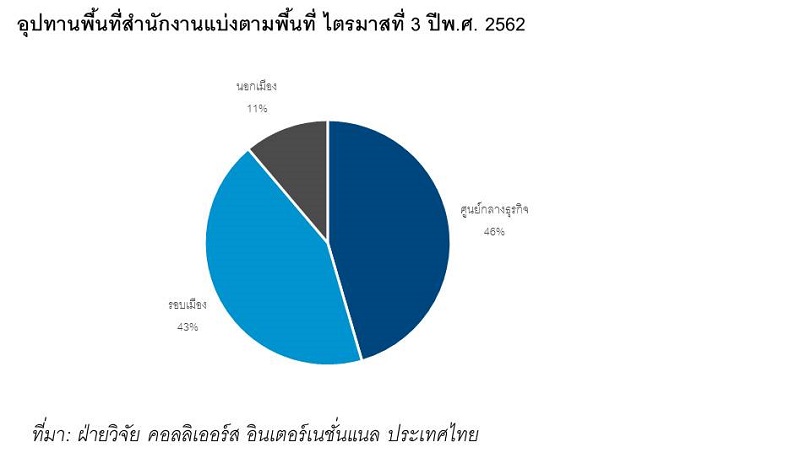

Office Space Supply by Area Q3 2019<\/span><\/p>

For areas outside the central business district, new locations for office development have emerged, such as along Ratchadapisek Road, Rama 9, Phahonyothin Road, and Vibhavadi-Rangsit Road. In Q3, several major operators launched new office projects to be developed in areas outside the central business district to accommodate urban expansion and new transportation networks under construction, particularly in the Ratchada-Rama 9 area. <\/p>

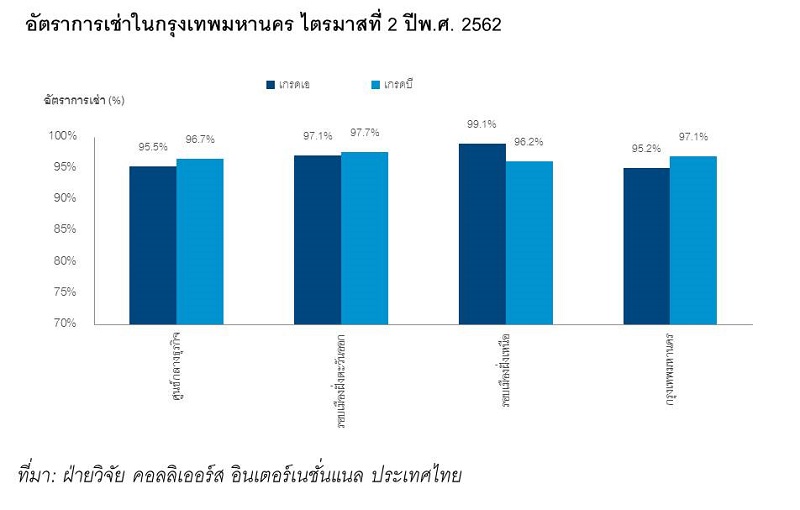

Rental Rates in Bangkok Q3 2019<\/span><\/p>

Demand for office space from clients has continued to increase, with over 125,000 sq.m. of demand for office space in Bangkok in the first nine months of 2019. The overall rental rate in Q3/2019 was 95.7%, with the Lumphini area becoming the location with the highest occupancy rate in the central business district at 96.5%. Most office buildings in the three main areas of Bangkok have an occupancy rate of nearly 100%, especially Grade A office buildings or newly completed office buildings in the past 1-3 years. Many foreign and Thai companies in Bangkok still have a demand for Grade A and B office space in the central business district (CBD), but some companies face issues with spaces that do not meet their needs, leading them to choose new office spaces outside the CBD of more than 1,000 sq.m. Meanwhile, co-working spaces have gained popularity in Bangkok, offering lower prices and greater flexibility compared to traditional office buildings. For Q3/2019, the rental rate for all Grade A offices was 95.2%, while the rental rate for all Grade B offices was 96.8%. The rental rate in the central business district was 95.6%, and the rental rate for areas outside the central business district was 95.7%. <\/p>

Annual Demand for Office Space 2011 - Q3 2019<\/span><\/p>

In the first nine months of 2019, there was a demand for office space in Bangkok of over 125,000 sq.m. and an average annual demand for office space rental increasing by more than 200,000 sq.m. per year. It is expected that the increase in rented office space will remain at this level. However, the demand for office space will depend on the political situation in Thailand and the overall global economy, which directly affects foreign companies that are the main tenants in Bangkok. However, the newly completed office space from 2021 onwards may exceed the demand for office space, and if the construction of office buildings continues to increase, it may lead to changes in the office market in Bangkok in 2021, resulting in a decrease in rental rates and negatively impacting rental prices due to increased competition in the future. <\/strong><\/p>

Average Rental Prices by Area Q3 2019<\/span><\/p>

<\/p>

The rental prices in the Bangkok office market have continued to rise over the past 1-3 years and are expected to continue to grow by approximately 3-5% in Q3/2019, depending on the building's grade and vacancy rates. Most office buildings in Bangkok that are over 15 years old cannot increase rental prices anymore. Office building owners must upgrade and develop internal systems to attract new tenants and to be able to raise rental prices. <\/strong> The rental prices are still expected to rise in the final quarter of 2019 because the vacancy rate is decreasing while demand continues to increase. The average rental price for Grade A office buildings in the central business district is approximately 1,100 baht per sq.m. per month, while the rental prices for Grade A office space in Bangkok range from approximately 900 to 1,500 baht per sq.m. However, the final rental price may be lower by 5-15% or more, depending on negotiations and the size of the space. The rental rates for office buildings in the Lumphini area, especially Grade A, are relatively high, and developers have increased rental prices in that area, resulting in an average rental price in Lumphini rising to 1,068 baht in Q3/2019. For Grade A and B office spaces in all areas of Bangkok, the average rental rates have increased by 5%-10% per year. The average rental rate for Grade A offices in the central business district is approximately 1,100 baht per sq.m. per month, while the average rental rate for Grade B offices in the central business district is 750 baht per sq.m. per month. The average rental rates for Grade A and B offices in areas outside the central business district are 940 baht and 576 baht per sq.m. per month, respectively. The average rental prices in Bangkok have continuously increased and reached the highest levels in recent years, but they remain lower than in other ASEAN capitals. However, rental prices are still expected to continue to rise, with average rents potentially exceeding 1,600 baht per sq.m. per month next year. Some Grade A office buildings in the central business district have average rental rates higher than the average rental price of 1,500 baht per sq.m., such as Park Ventures and Gaysorn Tower, two office buildings in the central business district with average rental prices reaching as high as 1,600 baht per sq.m., which is the highest average rental rate in the Bangkok office market. This is due to both buildings having occupancy rates close to 100%, and the remaining spaces are units that... <\/p>

Thank you for the information from: Research Department, Colliers International Thailand<\/strong><\/p>

<\/p>

<\/p>

<\/strong><\/p>

<\/p>  <\/strong><\/p>

<\/strong><\/p>

<\/strong><\/p>

<\/strong><\/p>

<\/strong><\/p>

<\/strong><\/p>

<\/strong><\/p>

<\/strong><\/p>

<\/strong><\/p>

<\/strong><\/p>