Real Estate Loans in 2026: Limited Recovery Amid Pressures from Developers and Homebuyers

Although the data from Q1 2026 indicates that residential real estate activities are still expanding, growth for the remainder of 2026 may face more limitations in line with the economic slowdown, insufficient recovery in purchasing power, and high levels of unsold inventory. The Kasikorn Research Center believes that this situation may pressure the trend of residential real estate loans, both for property developers (Pre-Financing) and homebuyers (Post-Financing). Meanwhile, the extension of the LTV relaxation period could be a positive factor that helps ease down payment conditions for homebuyers, but the overall impact on loans may still be limited, especially if the main issue remains with purchasing power, financial stability (Balance Sheet), and the debt repayment ability of both buyers and developers.

The fragile real estate market increases pressure on the financial status of property developers and the growth of Pre-Financing loans for housing.

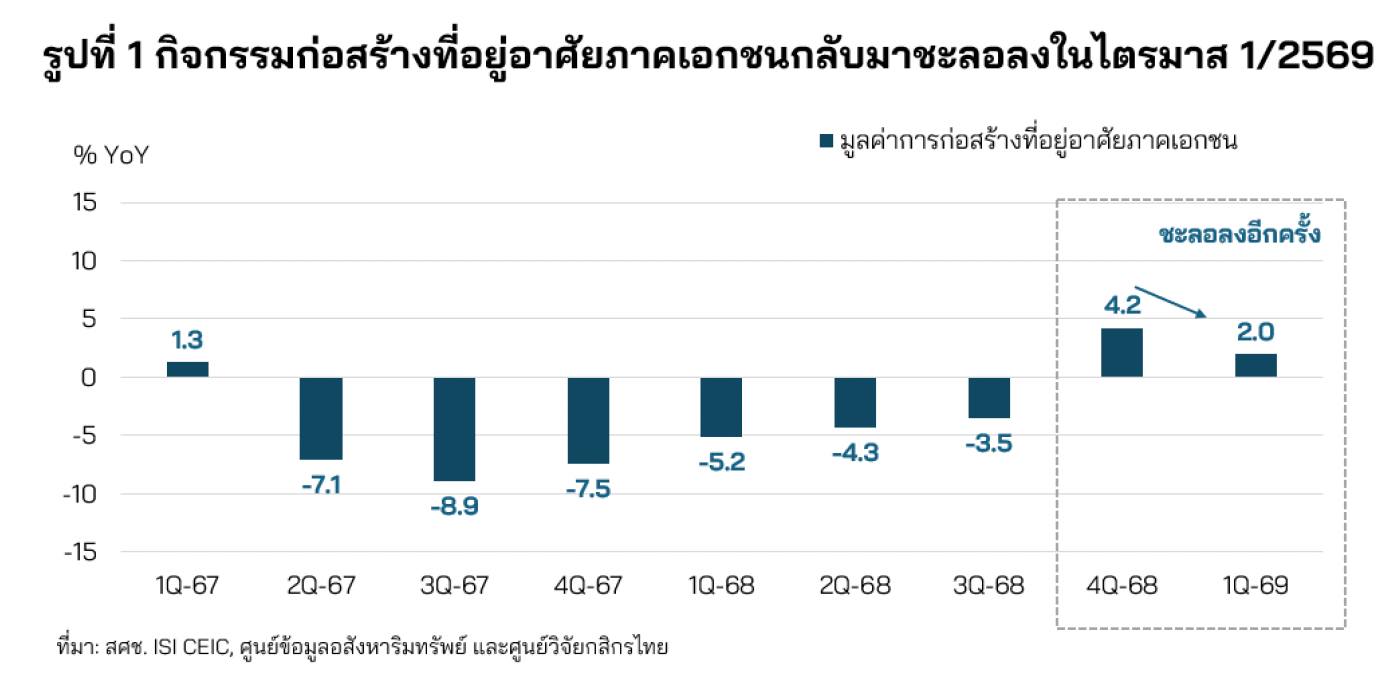

- The real estate market still shows signs of fragility, even though private sector residential construction activities expanded by 2.0% YoY in Q1 2026. However, it must be acknowledged that this reflects a slowdown after a rapid acceleration at the end of 2025 (Figure 1). Meanwhile, the weak signals in the real estate market and the challenges it faces for the remainder of 2026 may increase pressure on the financial status of project development companies. This is particularly true as unsold inventory remains high and sales/transfers are at risk of slowing down, which will affect the cash flow of operators, while financial costs and existing debt burdens remain high.

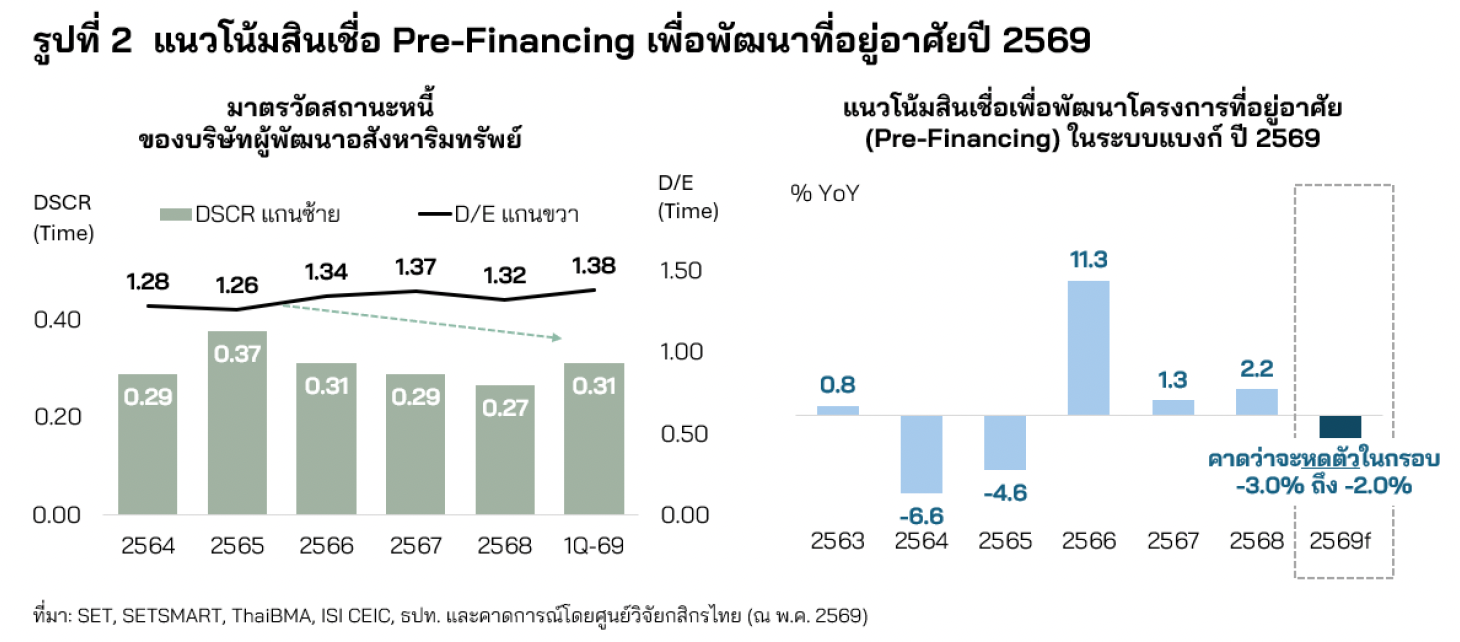

- The credit risk of project developers is increasing amid liquidity challenges and a tougher fundraising environment. The financial strain on property developers has been reflected in declining financial ratios over the past three years (Figure 2), particularly the debt-to-equity ratio (D/E), which is around 1.3-1.4 times. Meanwhile, the Debt Service Coverage Ratio (DSCR) is approximately 0.30 times, indicating that cash flow from operations is insufficient to cover debts due within a year, especially for operators with high unsold inventory who rely heavily on external funding.This pressure is beginning to translate into credit risk and fundraising constraints for operators, as evidenced by signs of credit rating downgrades among property development companies. Additionally, the bond market is becoming more challenging for fundraising, with long-term bond issuance volume in the first four months of 2026 down -27.6% YoY.

Similarly, the outstanding loans for residential development (Pre-Financing) in the commercial banking system contracted by -6.5% YoY in Q1 2026, with declines in both horizontal housing and condominiums (-7.9% YoY and -4.0% YoY, respectively) amid cautious signals from both financial institutions and operators, in line with the trend of slowing new project launches, focusing on clearing inventory and maintaining liquidity rather than expanding investments. The Kasikorn Research Center estimates that this trend may extend into the second half of the year, predicting that Pre-Financing loans for residential development in the banking system may contract by approximately -3.0% to -2.0% in 2026, compared to a growth of 2.2% in 2025 (Figure 2).

Fragile purchasing power is also a limitation on the recovery of housing loans in the banking system (Post-Financing).

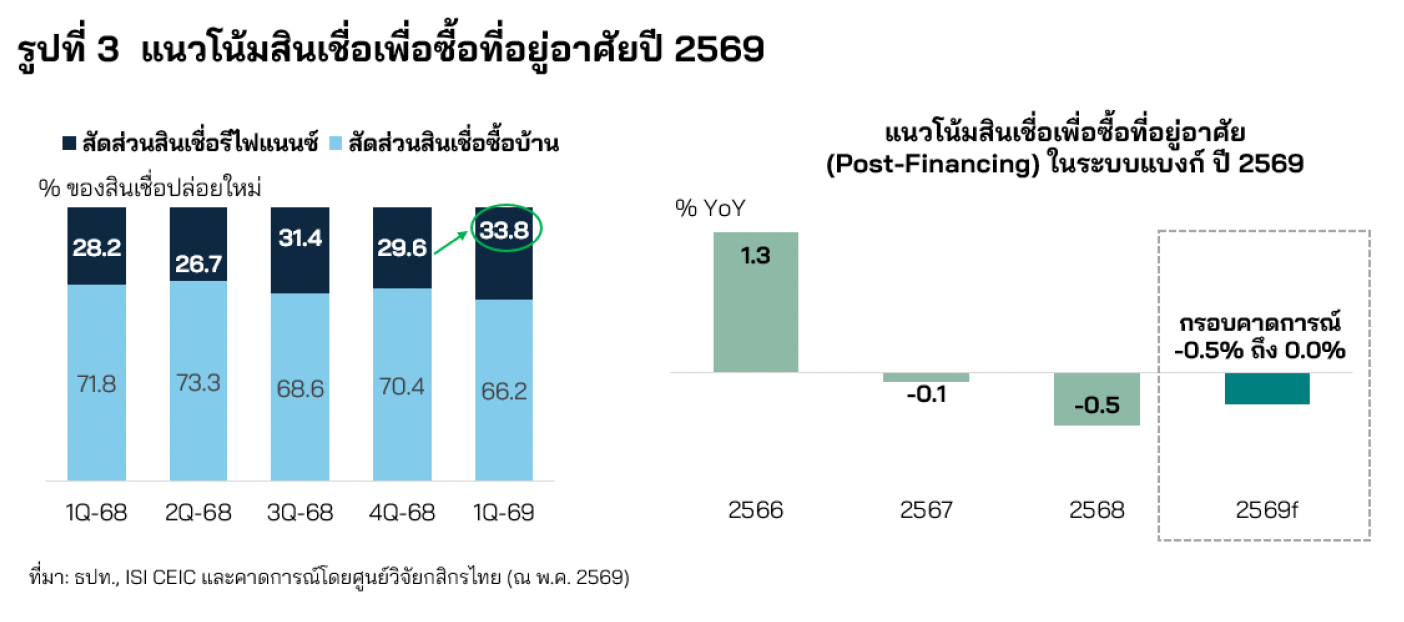

- On the homebuyer side, housing loans (Post-Financing) still show weak signals. Although housing loans in Q1 2026 returned to growth at 1.0% YoY, after contracting -0.5% YoY in Q4 2025, this should be interpreted cautiously as part of it is due to a low base in the same period last year when homebuyers were awaiting the consideration of extending the measures to reduce transfer and mortgage fees and the relaxation of LTV criteria. When looking at the details, it is evident that the growth in new loan disbursements does not reflect the overall demand for housing, as part of it comes from refinancing existing borrowers, which accounted for 33.8% of all new loan disbursements in Q1 2026. Additionally, the declining Loan to Value (LTV) ratio in both the segment of homes priced below 10 million baht and above 10 million baht reflects that financial institutions are becoming more cautious in considering housing loan approvals, limiting the momentum from new loans.

For the overall picture in 2026, the Kasikorn Research Center believes that housing loans in the commercial banking system may not expand, with a forecast range of -0.5% to 0.0%, reflecting a rather limited recovery trend, especially if domestic purchasing power does not fully recover, household debt remains high, and the debt repayment ability of buyers is pressured under a slowing economy. While the demand for housing may still exist, some borrowers may face limitations in obtaining loans, particularly among the middle to lower-income groups with high existing debt burdens, leading to cautious home loan approvals (Figure 3).

- Regarding the extension of the LTV relaxation period, the Kasikorn Research Center views it as a positive factor that supports the clearing of housing inventory for operators and helps sustain the recovery of the real estate sector to some extent. This measure helps reduce down payment constraints and provides more flexibility for certain buyer groups, especially those with stable incomes and the ability to repay debts.

However, the positive impact on housing loans in 2026 may still be limited, as the main conditions for market recovery in the remaining year are not solely dependent on the LTV ceiling, but also on purchasing power, income, existing debt burdens, and household repayment ability. Under an economy that still faces risks and is likely to slow down, financial institutions may continue to consider new loan approvals cautiously. Even if LTV criteria allow for higher loan disbursements, in practice, loans may not be issued at full collateral value of 100% in all cases, especially for borrowers with high debt burdens, uncertain incomes, or increased credit risks. Therefore, the relaxation of LTV is likely to play a role as a market support measure and reduce down payment burdens rather than being a primary factor that clearly drives housing loans to expand. Meanwhile, the main expectations for the recovery of housing loan activities still hinge on the economic situation and household income scenarios.

In summary, real estate loans in the banking system in 2026 are likely to face pressure on both Pre-Financing loans for residential project developers and Post-Financing loans for homebuyers. Pre-Financing loans are pressured by the overall weak trend in the real estate market, as well as the credit risks and fragile financial status of project developers. Meanwhile, Post-Financing loans are constrained by slowly recovering purchasing power/household income, high debt burdens, and weakened repayment abilities. Although LTV measures may help support the market to some extent, they are unlikely to reverse the loan direction clearly if the fundamental issues remain with the balance sheet quality of both operators and households.