Housing Market Situation in Q4 2025: Continuous Recovery from Government Measures, Signs of Stabilization, and Structural Market Adjustment

The Real Estate Information Center (REIC) of the Government Housing Bank (GHB) has revealed the housing market situation for Q4 2025, indicating an overall recovery trend quarter-on-quarter, driven by short-term economic stimulus measures (Quick Big Win) and support for the real estate business, such as reduced transfer and mortgage fees and relaxed LTV criteria. This has resulted in an increase in property transfers in Q4 compared to Q3 (QoQ), with the number of units rising by 5.7% and the value increasing by 9.3%. New residential loans nationwide also saw a 1.3% increase (QoQ). Overall, 2025 has passed its lowest point, and it is expected that the housing market in 2026 will stabilize similarly to 2025, marking a year of structural balance between demand, supply, and housing credit conditions, which is anticipated to positively impact the real estate sector and the overall Thai economy.

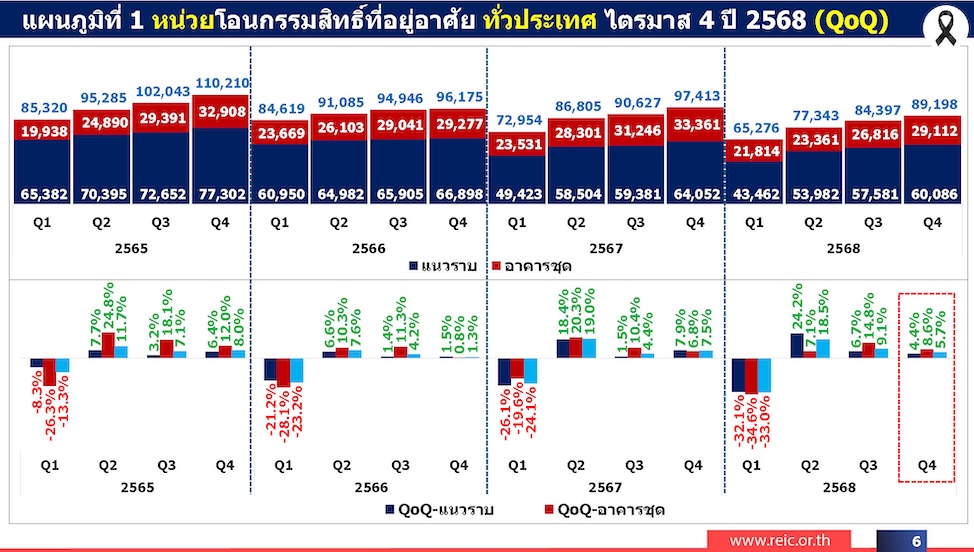

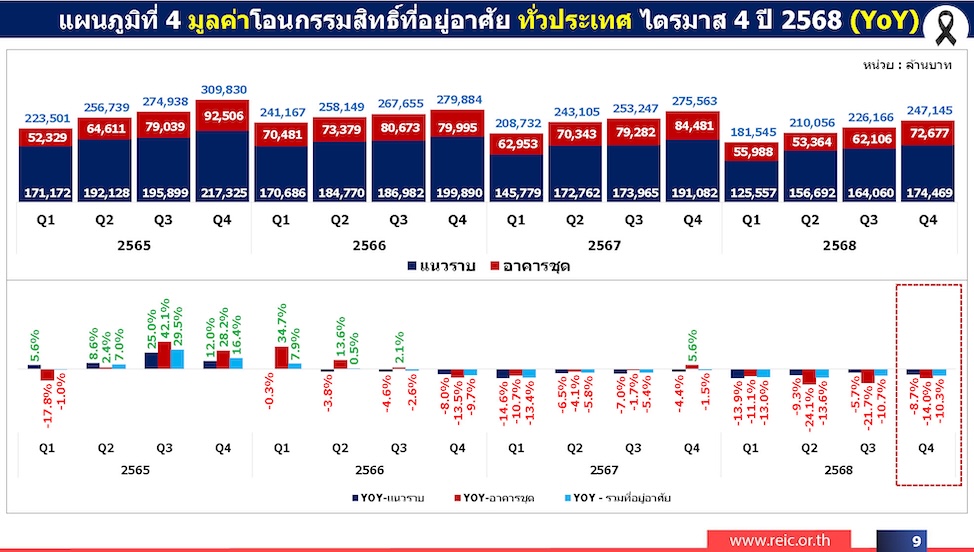

Mr. Narongpol Prapanirinthorn, Deputy Managing Director of the Marketing Group and Acting Director of the Real Estate Information Center (REIC) stated that the overall housing market situation in Q4 2025 shows continuous recovery from the previous two quarters, with demand increasing in Q4 compared to Q3 (QoQ) due to the support from reduced transfer and mortgage fees and relaxed LTV criteria, which have encouraged real housing purchase decisions. The number of property transfers nationwide in Q4 increased from Q3 (QoQ) in both units and value, with 89,198 units transferred, up by 4,801 units from 84,397 in Q3, representing a 5.7% increase (QoQ). The transfer value reached 247,145 million baht, up by 20,979 million baht from 226,166 million baht, marking a 9.3% increase (QoQ). When categorized by property type, it was found that low-rise housing accounted for 60,086 units, an increase of 4.4% (QoQ), with a value of 174,469 million baht, up by 6.3% (QoQ), while condominiums saw 29,112 units transferred, an increase of 8.6% (QoQ), with a value of 72,677 million baht, up by 17.0% (QoQ).

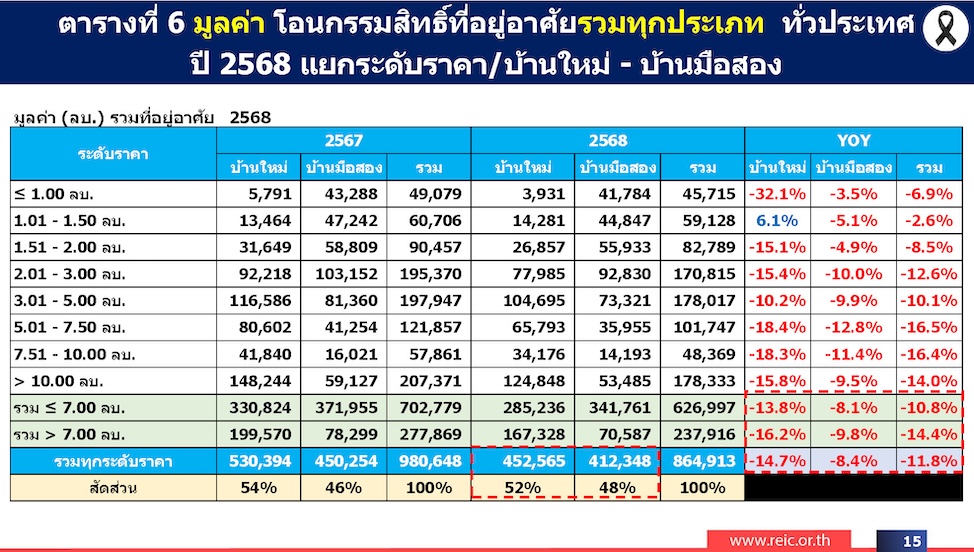

Furthermore, when examining new and second-hand homes, the market structure reflects clear changes. In Q4 2025, the total number of property transfers nationwide for new homes was 33,606 units, accounting for 38% of total transfers, down from 39%, while second-hand homes totaled 55,592 units, representing 62%, up from 61% (YoY). The value of second-hand homes remains lower. In summary for the entire year of 2025, the total number of property transfers nationwide was 316,214 units, down from 347,799 units in 2024, a decrease of 9.1%, with a total value of 864,913 million baht, down from 980,648 million baht, a decrease of 11.8%. New homes for the year totaled 112,565 units, down 13.9%, with a value of 452,565 million baht, down 14.7%. Meanwhile, second-hand homes totaled 203,649 units, down 6.2%, with a value of 412,348 million baht, down 8.4%, resulting in the market share of second-hand homes increasing to 64% of total transfers, indicating a growing structural role of the second-hand home market amid fragile purchasing power.

However, when considering specific areas, the top 10 provinces with the highest transfer values in Q4 2025 included Bangkok, Chonburi, Samut Prakan, Nonthaburi, Pathum Thani, Phuket, Chiang Mai, Rayong, Khon Kaen, and Nakhon Ratchasima. Provinces that experienced growth in transfers compared to the same quarter last year (YoY) in both units and value in Q4 included Khon Kaen and Rayong. For the top 10 provinces with the highest transfer values in 2025, the same provinces were noted, with Phuket, Rayong, and Nakhon Ratchasima showing growth in both units and value, while Khon Kaen saw an increase in units but a decrease in value.

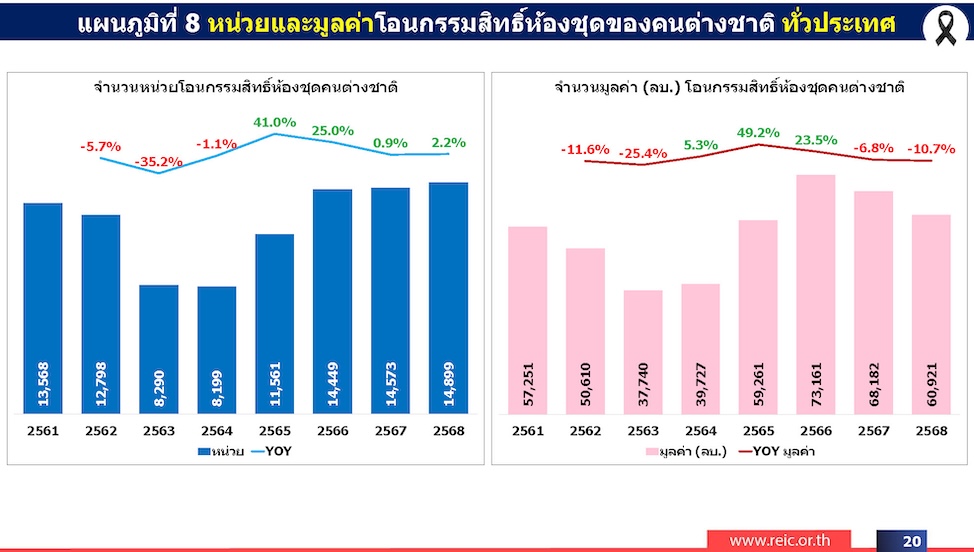

Additionally, in Q4 2025, there were positive signs in the foreign condominium buyer segment, with 3,888 units transferred to foreigners, an increase of 1.1% (QoQ) and up 9.3% compared to the same period last year (YoY). Although the value grew only slightly year-on-year, the number of units increased at a higher rate, reflecting a trend of "average unit prices decreasing," especially for mid-range purchases. For the entire year of 2025, foreigners transferred a total of 14,899 condominium units, an increase of 2.2% from the previous year (YoY), while the transfer value was 60,921 million baht, down 10.7% (YoY). The proportion of transfers by foreigners accounted for 14.7% of total condominium unit transfers and 25.0% of total condominium transfer value nationwide. By nationality, the main buyer group remained Chinese, despite a decrease in both units and value, with 4,940 units transferred in 2025, down 12.9% from the previous year, with a value of 18,585 million baht, down 30.0%. Nevertheless, Chinese buyers still held the highest share at 33% of units and 31% of total transfer value, while notable growth was seen from buyers from Russia and Taiwan, indicating a diversification of foreign demand towards new countries, including those buying for actual residence, long-term stays, and investment for rental purposes, which will enhance the flexibility of the Thai condominium market.

In terms of housing loans, which also reflect increased demand, in Q4 2025, the total value of new personal housing loans nationwide was 148,748 million baht, up 1.3% compared to Q3 2025 (QoQ), which had a value of 146,834 million baht, benefiting from two ongoing real estate stimulus measures. However, for the entire year of 2025, new personal housing loans nationwide totaled 539,065 million baht, down 7.8% (YoY) from 584,843 million baht, reflecting the caution of financial institutions and household debt constraints.

The outlook for the housing market in 2026 indicates that the Thai economy remains fragile but still has opportunities amid the crisis. It is projected that GDP growth in 2026 will expand between 1.5-2.5 (median 2.0), with household debt remaining high, pressuring purchasing power. However, the government has short-term economic stimulus policies (Quick Big Win) to address household debt issues, such as debt closure programs, which will ease the debt burden on citizens. Interest rates are expected to trend downward, and the number and income from tourists are anticipated to recover following the establishment of the government, with ongoing policies and economic stimulus measures expected to positively impact exports and industrial production, as well as the expansion of private consumption. REIC estimates that in 2026, the housing market will remain stable, with a baseline scenario predicting a total of 314,593 property transfers nationwide, a decrease of 0.5% compared to 2025 (YoY), which had 316,214 units, and an estimated value of approximately 858,453 million baht, down 0.7% compared to 2025 (YoY), which had a value of 864,913 million baht. It is also projected that new personal housing loans nationwide in 2026 will amount to approximately 539,062 million baht, similar to 2025, which had a value of 539,065 million baht.

In summary, 2025 was a year in which the Thai housing market declined in both unit numbers and value, although the final quarter began to recover due to the Quick Big Win measures and the reduction of transfer and mortgage fees, as well as relaxed LTV criteria. However, the recovery remains limited. In 2026, the economy is expected to stabilize, marking a period of structural balance between demand, supply, and domestic credit conditions, which is anticipated to positively impact the real estate sector and the overall Thai economy.