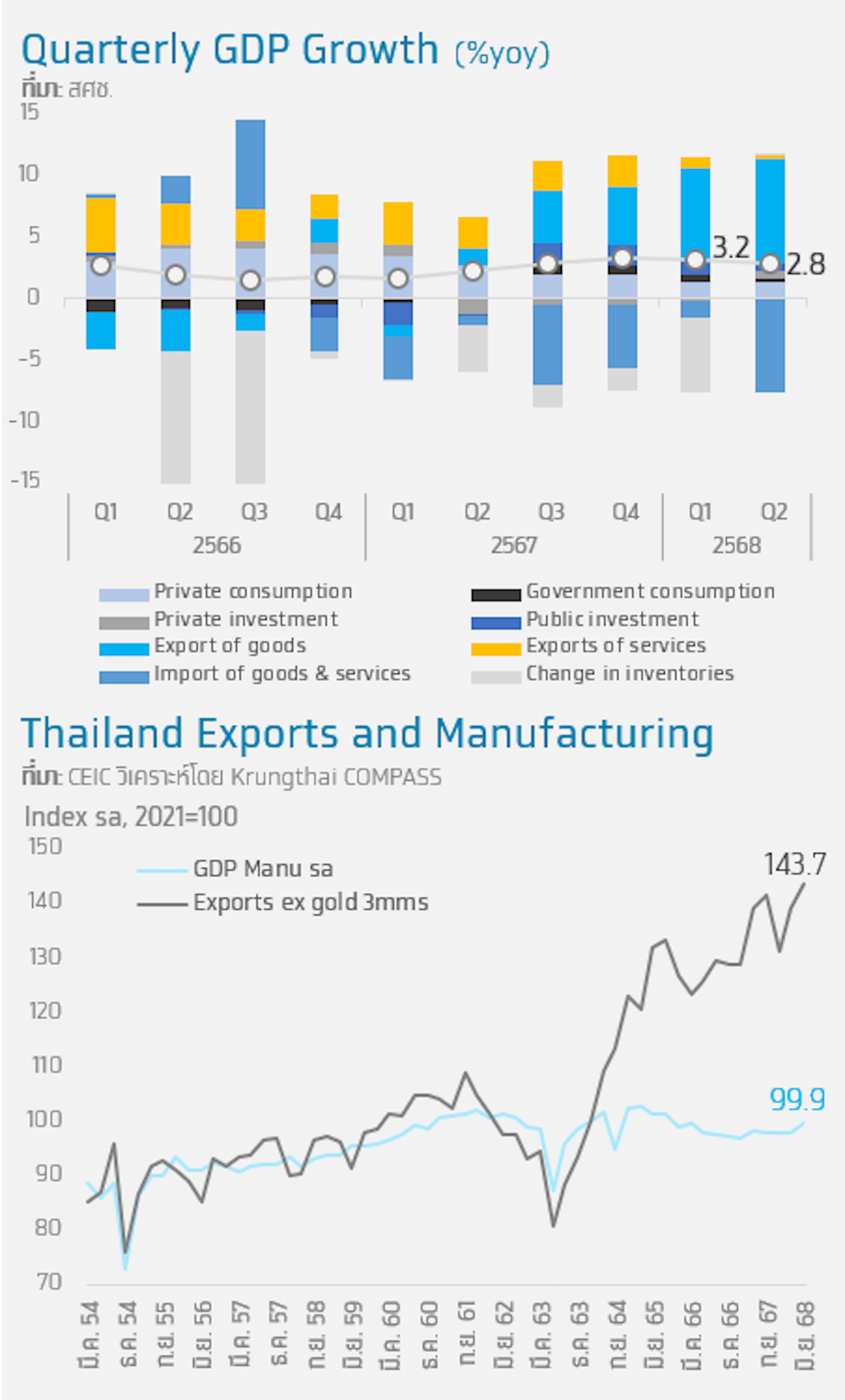

GDP in Q2 Grows 2.8%, NESDC Projects 2025 GDP Growth at 1.8-2.3%

- The Thai economy in Q2/2025 grew by 2.8% YoY due to increased exports ahead of the U.S. import tax hike and private sector investment resulting from a low base last year. The NESDC has raised its GDP forecast for 2025 to a range of 1.8%-2.3% (midpoint 2.0%) due to strong export growth in the first half of the year, coupled with a slight easing of uncertainty in global trade policies.

- Krungthai COMPASS estimates that the Thai economy will grow by 2.0% YoY in 2025, although momentum is expected to slow down following the announcement of U.S. import tax rates. While this reduces uncertainty in trade policy, it is anticipated that price competition will intensify. Additionally, the de-stocking situation in the U.S. will affect future order trends, amid risks from the impact of trade agreements with the U.S., particularly regarding transshipment taxes, which currently lack clear operational guidelines, as well as the tourism sector, which is affected by safety concerns.

GDP in Q2 2025 grew 2.8% YoY due to continuous high export growth and a significant rebound in private sector investment. The National Economic and Social Development Council (NESDC) reported economic growth figures for Q2/2025, showing a growth of 2.8% YoY, and a quarter-on-quarter growth of 0.6% QoQ SA, driven by:

- Exports of goods and services remain a key driver, with a growth rate of 14.3% YoY, marking the fifth consecutive quarter of growth, up from 13.8% YoY in the previous quarter, particularly in electronics and machinery and equipment, driven by accelerated exports ahead of the U.S. reciprocal tariff announcement. Meanwhile, tourism growth slowed to 2.7% YoY due to safety concerns affecting foreign tourists.

- Imports grew significantly at 15.3% YoY, exceeding the previous quarter's growth of 3.9%, reflecting accelerated imports for production and shipment to the U.S. before the tax measures took effect. However, there is a risk that some of these imports may have a low proportion of Thai raw materials, as production, while improving with exports, only grew by 1.7% YoY, which is a point to monitor going forward, especially concerning local content and transshipment taxes.

- Private sector investment grew 4.1% YoY, marking the first growth in four quarters, driven by investment in machinery and equipment, which expanded by 5.9% YoY, particularly in the automotive sector, while construction investment continued to contract at -2.0% YoY.

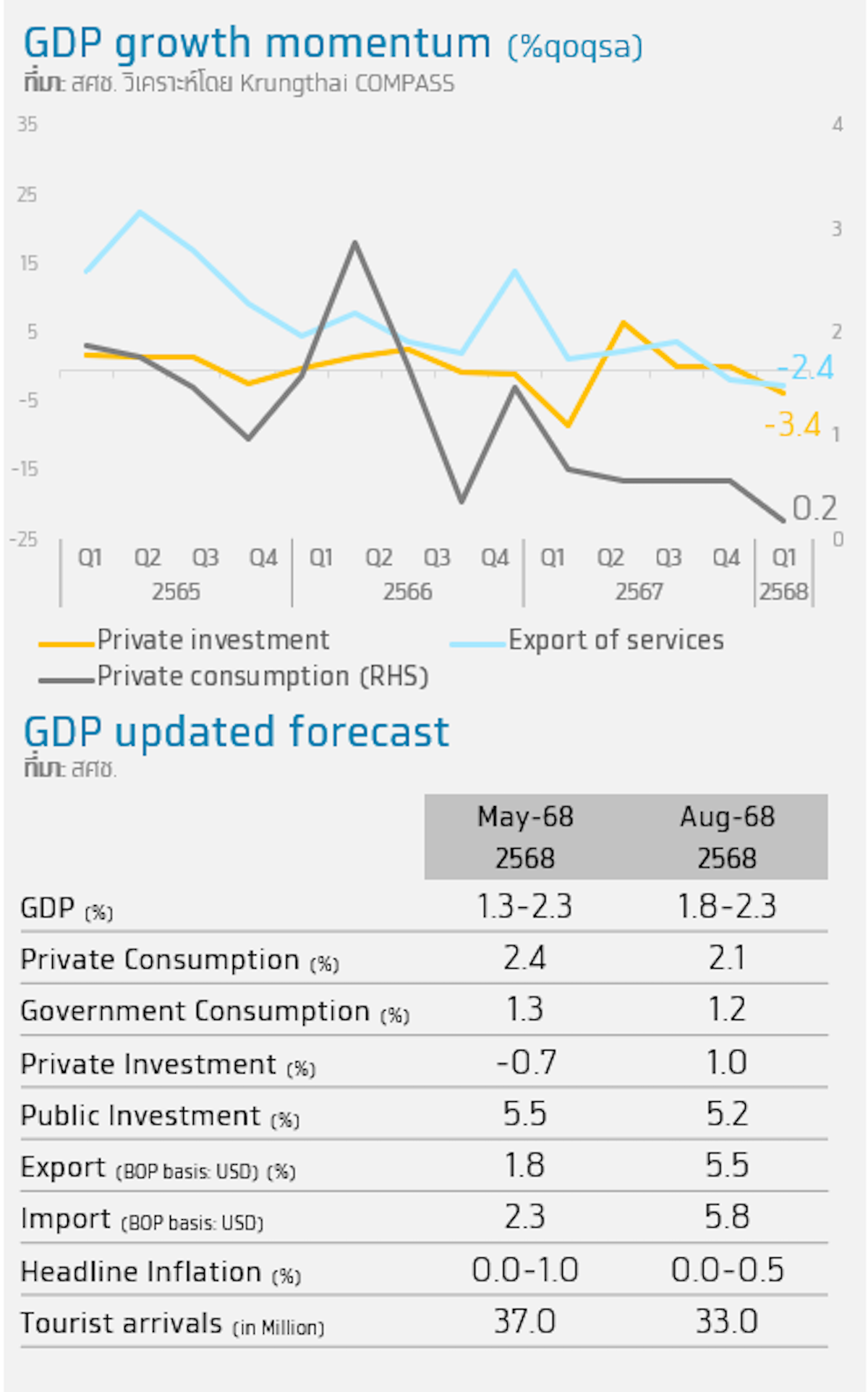

Despite the economy growing by 2.8% YoY in Q2, momentum has weakened in several areas:

- Private sector investment contracted by -3.4% QoQ SA, primarily due to investment in machinery and equipment. Although this quarter showed growth compared to the same period last year, it reflects a low investment climate with high uncertainty. Additionally, the continuity of investment in automobiles, which has just returned to growth for the first time in five quarters, needs to be monitored.

- Service exports contracted by -2.4% QoQ SA, continuing from the previous quarter's contraction of -1.5% QoQ SA, due to a decline in tourists from almost all East Asian countries, particularly from China, resulting in a -12.2% YoY drop in tourist numbers this quarter, reflecting growing safety concerns, although long-haul tourists partially compensated.

- Furthermore, private consumption grew only slightly at 0.2% QoQ SA, particularly in service spending, reflecting household vulnerability impacted by economic uncertainty.

The outlook for the Thai economy in 2025 is projected by the NESDC to grow in the range of 1.6% to 2.3% (midpoint 2.0%) due to risk factors: 1) the impact of U.S. import tax measures on Thai goods, 2) fluctuations in the global economy and trade volume due to U.S. tariffs, and 3) a slowdown in the tourism sector. The NESDC has revised its forecast for foreign tourists down to 33 million from 37 million estimated in May. However, the NESDC sees supportive factors for the economy this year, including 1) government spending support, particularly investment spending, and 2) improved private sector investment in machinery and equipment.

Implications:

- Krungthai COMPASS assesses that although the economy in Q2 2025 grew well at 2.8% YoY, the main drivers of the economy are expected to slow down following the announcement of U.S. import tax rates. While this reduces uncertainty in trade policy, it is anticipated that many countries will accelerate the disposal of goods to third markets, leading to intensified price competition.

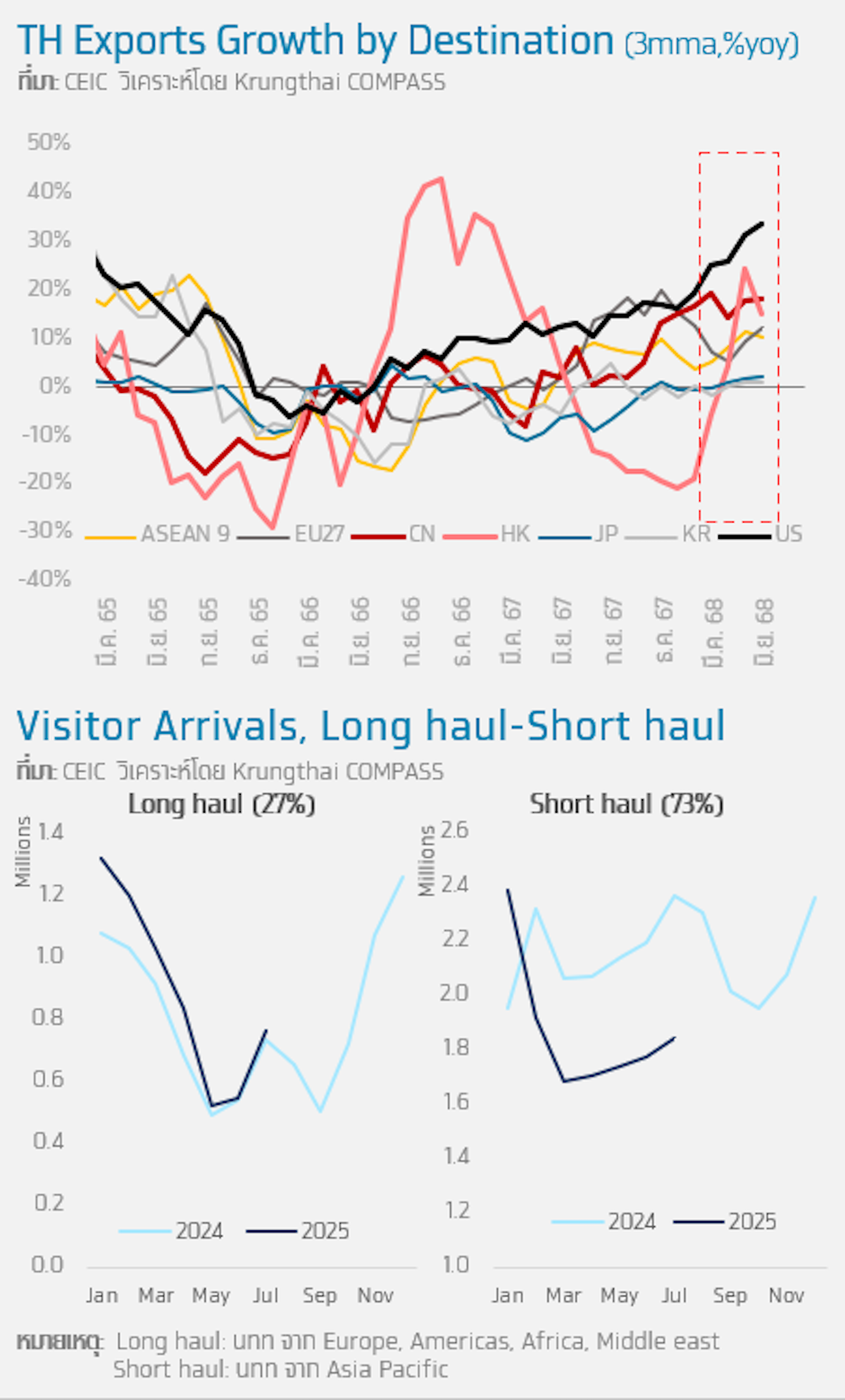

- Additionally, the acceleration of exports in the first half of the year has resulted in the U.S. holding high inventory levels that may meet demand in 2025. The average monthly export value to the U.S. from March to June 2025 reached $6 billion, higher than the average of $4.8 billion in Q4 2024. Future orders will depend on the U.S.'s ability to de-stock amid inflation that may rise again due to tariffs. There are also risks regarding potential sectoral tariffs on semiconductor products, which Thailand has previously exported well, accounting for over 6% of Thailand's export value to the U.S.

- Tourism faces greater risks of slowdown than expected, even though in the first half of the year, the number of long-haul tourists, who tend to spend more, grew by over 17.4% YoY and partially compensated for short-haul tourists. However, short-haul tourists still account for a significant 73% of total foreign tourists, necessitating a rapid restoration of confidence.

- Krungthai COMPASS believes that the Thai economy in 2025 will grow at 2.0% YoY, with the second half of the year expected to slow down to 1.0% YoY from 3.0% YoY in the first half, amid risks from the impact of trade agreements with the U.S., particularly regarding transshipment taxes, which currently lack clear operational guidelines, posing challenges to the adaptability of Thailand's supply chain.