Trends in Factory Leasing in Thailand: A Summary for 2024

Economic Overview

In 2024, Thailand's Gross Domestic Product (GDP) is projected to grow by 2.5% year-on-year (YoY), reflecting a continued recovery from 2.0% in 2023. This growth is driven by increased exports and higher government spending. In the second half of 2024, exports are expected to expand by 9.9% YoY, benefiting from global demand for products, particularly rubber, computers, and machinery. As a result, Thailand will have a trade surplus of 363.7 billion baht. The growth in exports related to the manufacturing sector has led to an increased demand for industrial space and factories that support export-oriented industries.

Supply

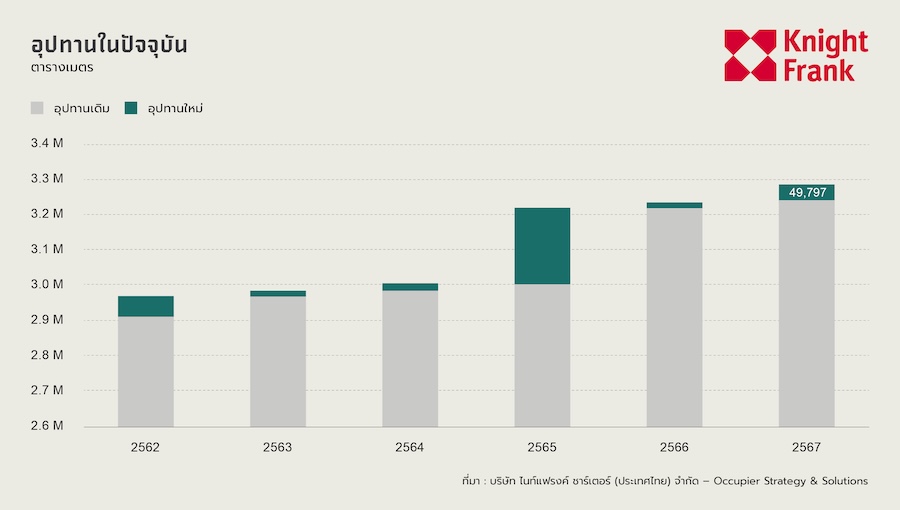

In 2024, the total area of ready-built factories is approximately 3.28 million square meters, a slight increase from 3.23 million square meters in 2023. The increase in supply of 49,797 square meters represents a year-on-year growth rate of 1.5%, which is limited and primarily comes from the expansion of existing factory projects in the Eastern Economic Corridor (EEC). This area continues to attract investors due to its proximity to key logistics routes and major industrial clusters, leading developers to cautiously expand space to meet the ongoing but not urgent demand for modern factory space.

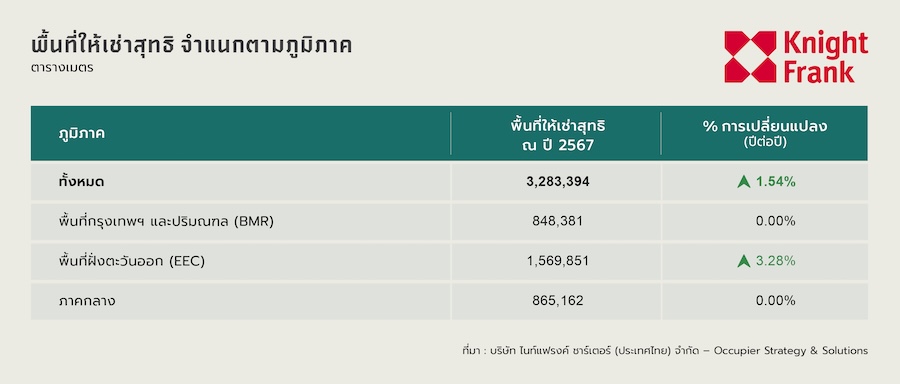

Distribution of Supply

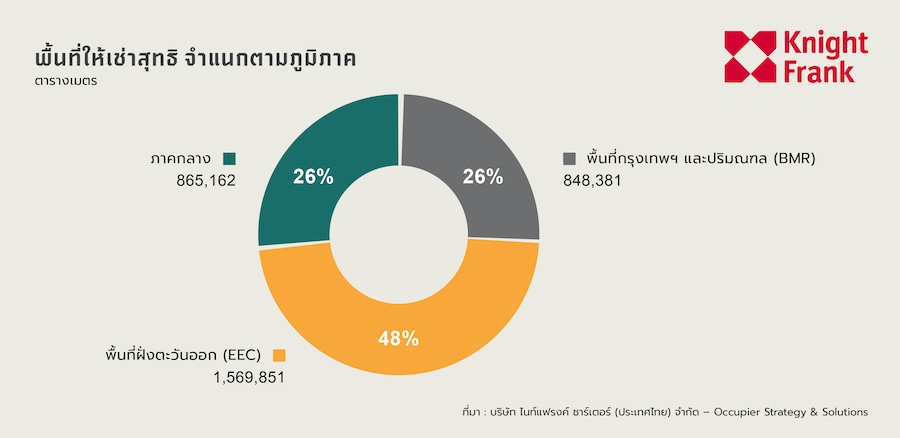

As of 2024, the Eastern Seaboard (EEC) holds the largest share of ready-built factory space at 48%, or approximately 1.57 million square meters. This area is the only one to experience significant supply growth at 3.28% compared to the previous year, reflecting ongoing demand in key provinces such as Chonburi and Rayong. Meanwhile, the Bangkok Metropolitan Region (BMR) and Central Region each account for 26%, with total areas of 848,381 square meters and 865,162 square meters, respectively. Both areas saw no new supply increase over the past year. Overall, total supply increased by 1.54% compared to the previous year, driven solely by growth in the EEC.

Demand

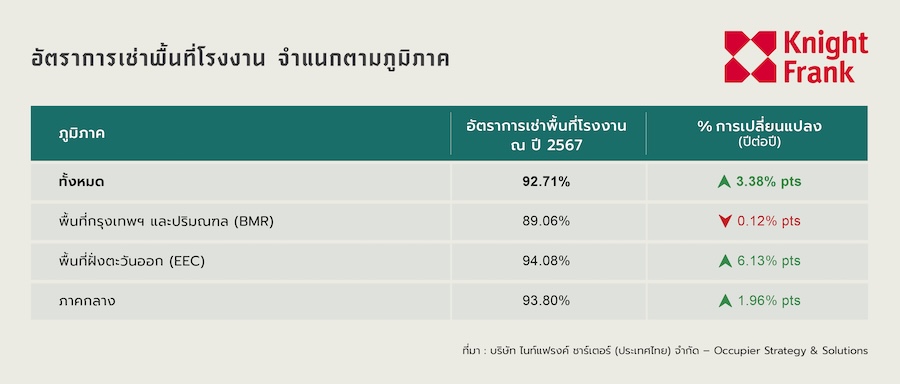

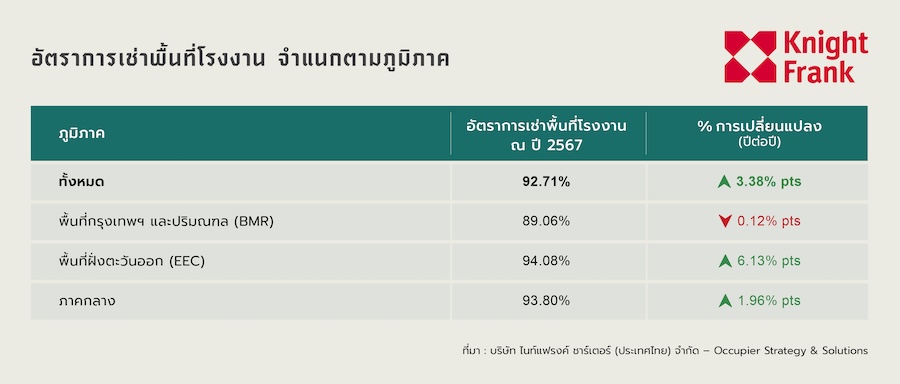

The demand for ready-built factory space in Thailand continues to rise in 2024, with approximately 3.04 million square meters leased, up from 2.90 million square meters in 2023. This indicates a net absorption of about 144,225 square meters, driven by the expansion of existing tenants and the entry of new tenants in major industrial estates.

The occupancy rate has increased to 92.7% from 89.6% in 2023, reflecting strong ongoing demand and tightening vacancy rates. This occupancy rate is the highest in the past six years and is supported by the continuous demand from export-oriented operators, particularly in the EEC, which boasts strong infrastructure and supply chain connectivity.

Despite a limited increase in new supply, the ongoing growth trend in leasing indicates a healthy balance between demand and supply, with industrial demand remaining strong amid a moderately growing economic environment.

Rental Rates

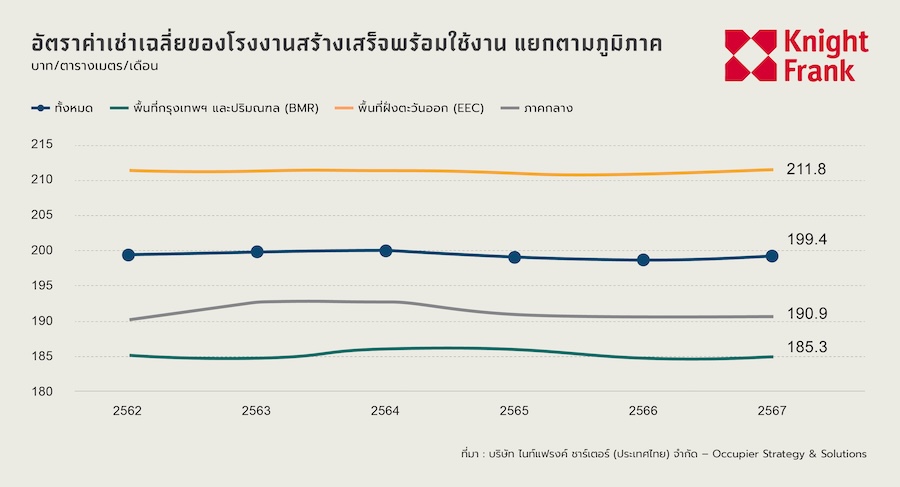

The average rental rate for ready-built factories in Thailand continues to rise, reaching 199.4 baht per square meter per month in 2024. This reflects a stable market supported by strong demand from manufacturers and export-oriented operators, particularly in high-demand areas like the EEC.

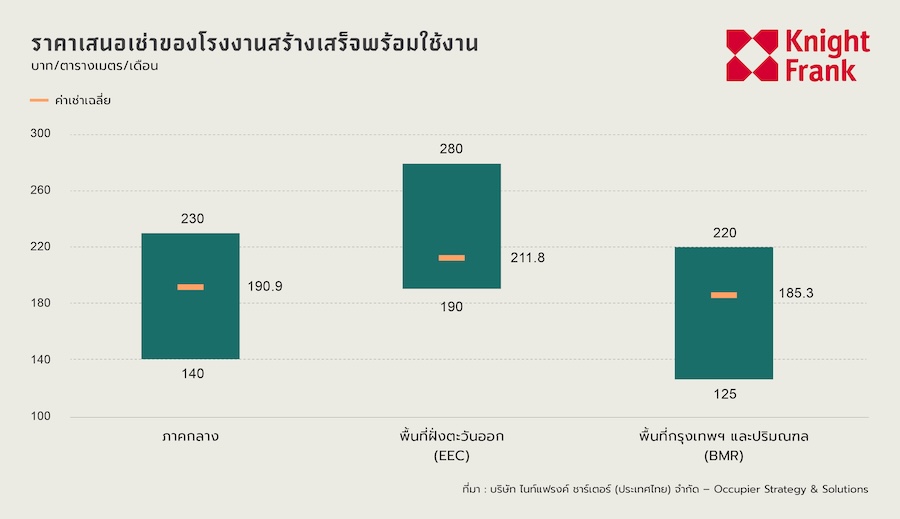

Average Rental Rates by Area

- EEC: has the highest average rental rate at 211.8 baht/sq.m./month, driven by land constraints and its strategic role within the framework of the Eastern Economic Corridor.

- Central Region: with an average rent of 190.9 baht/sq.m./month, which has significantly increased in recent years due to its growing role as a logistics and manufacturing hub.

- Bangkok and Metropolitan Region (BMR): despite having the most competitive rental rate at 185.3 baht/sq.m./month, it has shown considerable volatility due to changing demand dynamics and space constraints in various sub-locations.

Between 2019 and 2024, rental rates across all areas have shown moderate but uneven growth, with clear increases in certain areas such as the Central Region, indicating market tightness in leading industrial locations. The rental trend is expected to continue rising, especially in areas where demand outpaces new supply.

“The current high rental rates reflect Thailand's potential as a regional manufacturing base. The tight supply in high-potential areas like the EEC, combined with the demand from tenants focused on technology and sustainability, will support continued rental increases, particularly for factories that meet future needs.”

— Marcus Berthenshaw, Partner and Head of Industrial Strategy, Knight Frank Thailand Market Review and Trends

The factory leasing market in Thailand remains strong, with a good balance between new supply and increasing demand. With an occupancy rate of 92.7%, the highest in six years, it reflects Thailand's role as a regional manufacturing hub, particularly in the EEC area. Demand remains highly resilient, driven by continuous export growth, supportive government policies, and ongoing infrastructure development.

Several key factors may influence future factory market trends:

- Demand Driven by FDI: Foreign Direct Investment (FDI), particularly from China and Japan, is expected to remain a key driver of demand for ready-built factories, as investors are attracted by stable macroeconomic conditions, comprehensive free trade agreements, and government-supported incentives.

- Supply Constraints in High-Potential Areas: Due to limited new supply and land scarcity in key areas like the EEC, competition for high-quality space is likely to intensify, driving rental rates upward in the short term.

- Rising Construction Costs: Developers face higher construction and financing costs, which may reduce speculative development and tighten the supply growth trajectory if rental rates do not incentivize further investment.

- Distribution of Industrial Estates: Due to infrastructure constraints and high rental rates in the EEC, investors and developers may start to consider emerging areas, such as the high-speed rail route in the Northeast (HSR) and logistics centers in the central region.

- Sustainability and Automation: Tenants are increasingly prioritizing environmentally friendly buildings that support automation. Developers who can offer energy-efficient spaces aligned with ESG principles are likely to lease faster and command higher rents.

In summary, Thailand's ready-built factory sector is entering a more mature cycle, with selective growth, higher occupancy rates, and stable upward rental rates. Developers and investors who can adapt to tenant demands, encompassing technology, sustainability, and location flexibility, will be well-positioned to seize opportunities from market growth in the future.