Office Market Q4 2024

Market Overview The Bank of Thailand forecasts that the Thai economy will grow by 2.7% in 2024 and 2.9% in 2025. The tourism and services sectors are expected to perform well, while exports of electronics and machinery are anticipated to improve due to global technology growth, particularly in the hard disk drive industry, which benefits from the expansion of the Data Center sector. However, certain manufacturing sectors continue to face challenges, particularly the automotive and auto parts industries, which have weakened due to specific factors in this sector, while exports of chemicals, metals, and electrical appliances still face pressure from increased competition from China.

Global economic uncertainty and the Thai economy have significantly increased, primarily due to U.S. economic policies, particularly tax and tariff measures, which may disrupt international trade and pose risks to global economic growth.

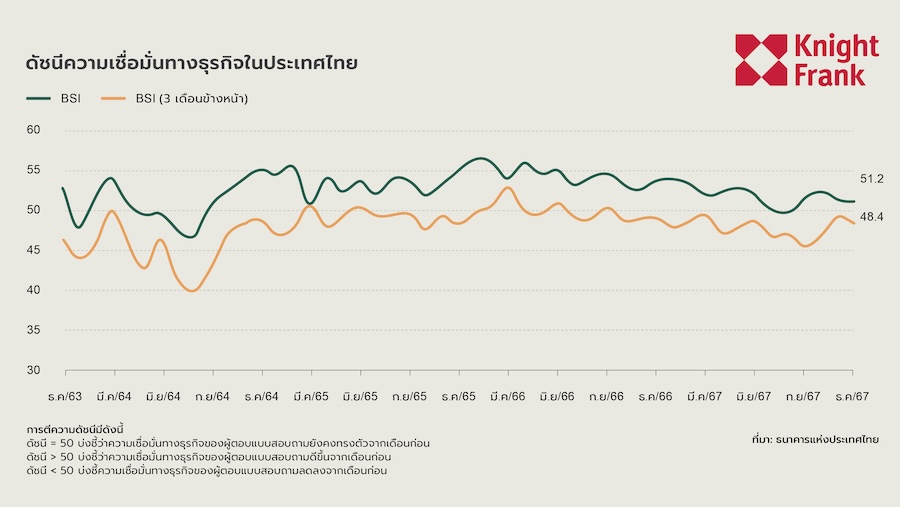

In December, the Business Sentiment Index (BSI) slightly decreased but remains on an upward trend, primarily supported by the recovery of the non-manufacturing services sector. All business sectors contributed to the recovery of confidence, with the tourism-related sectors, including hotels, restaurants, and passenger transport, showing clear recovery, supported by an increase in tourists from the U.S. and Europe during the New Year festival.

However, the BSI for the next three months continues to decline throughout 2024, with a noticeable drop in the second half of the year. During this period, the production index fell to its lowest and longest level since the COVID-19 outbreak, reflecting increased uncertainty in business outlook.

Supply

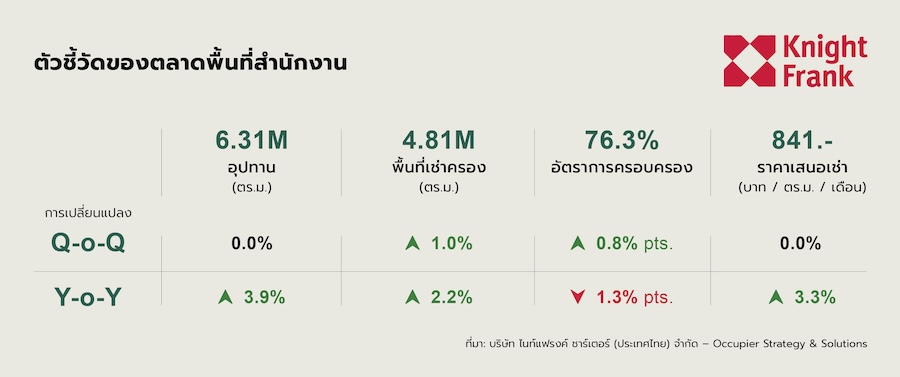

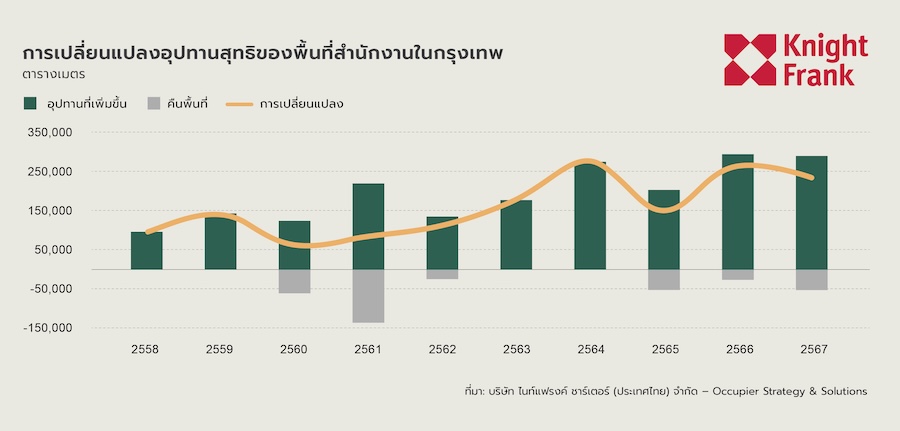

Office space in Bangkok remains stable at 6.31 million square meters, with no additions or withdrawals in supply this quarter. In 2024, total supply is expected to increase by 235,000 square meters, which is similar to the increase in 2023.

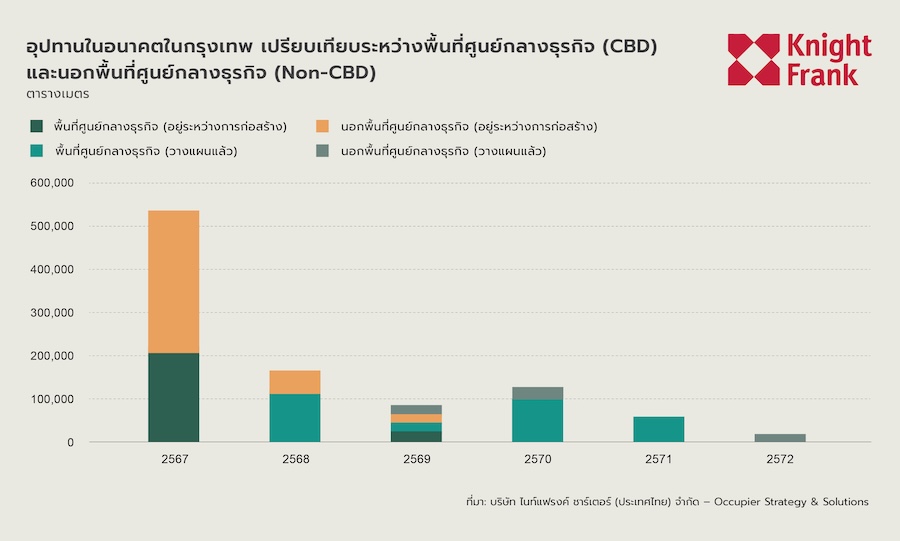

Future Supply

The total leasable area in projects under development has decreased to 1.0 million square meters, reflecting a scaling down of future projects to align with current market conditions. Currently, there is approximately 530,000 square meters under construction. It is anticipated that 2025 will see the highest volume of supply entering the market, with an expected addition of 540,000 square meters.

Demand

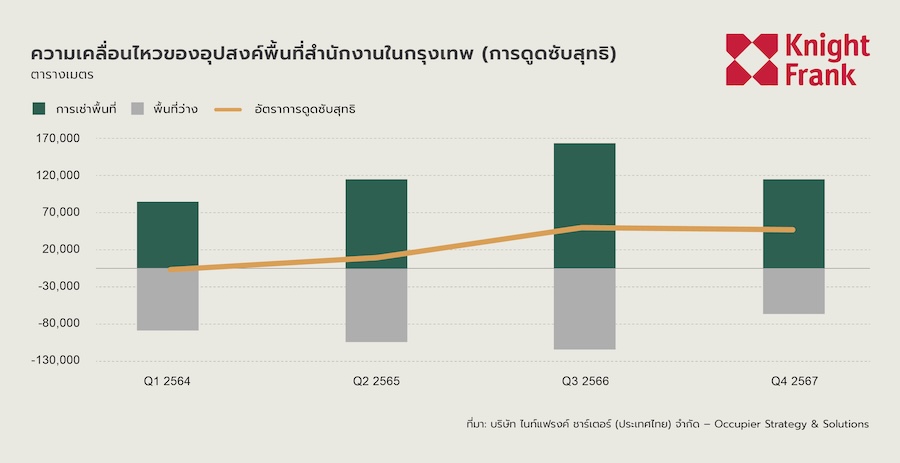

Leasing activity remains strong despite a decrease in total occupancy of 115,000 square meters, but net absorption remains robust at 48,000 square meters, close to the levels recorded in Q3, resulting in an overall increase in leased space of 1% to 4.86 million square meters.

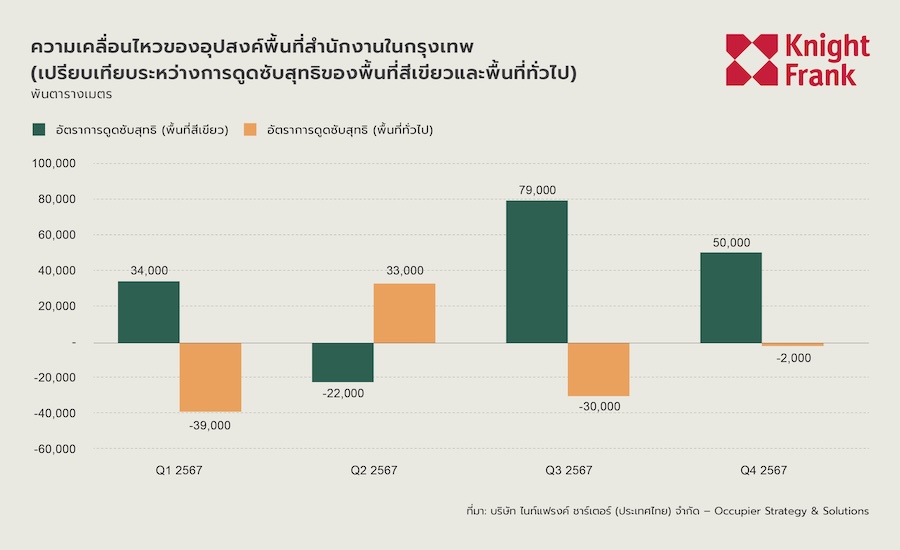

Green-certified buildings continue to attract the most interest from tenants, with a net absorption of 50,000 square meters, while non-green buildings saw a slight decrease of 2,000 square meters. The trend for office space leasing is positive in both the Central Business District (CBD) and Non-CBD areas, with net absorption of 27,000 square meters and 22,000 square meters, respectively.

Market Dynamics by Segment

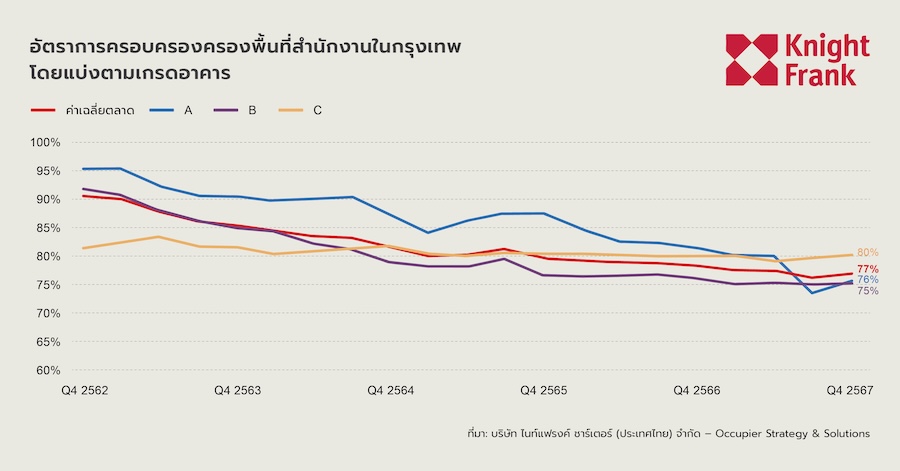

Due to reduced supply pressure and increased demand, the overall occupancy rate in the market increased by 1% to 77%, marking the first increase since Q3 2023. The occupancy rate improved across all grades, with Grade A showing the most significant increase of 2.1% to 76%, reflecting a continued trend towards seeking high-quality buildings, while Grade B has the lowest occupancy rate at 75%, and Grade C remains the leader with the highest occupancy rate at 80%.

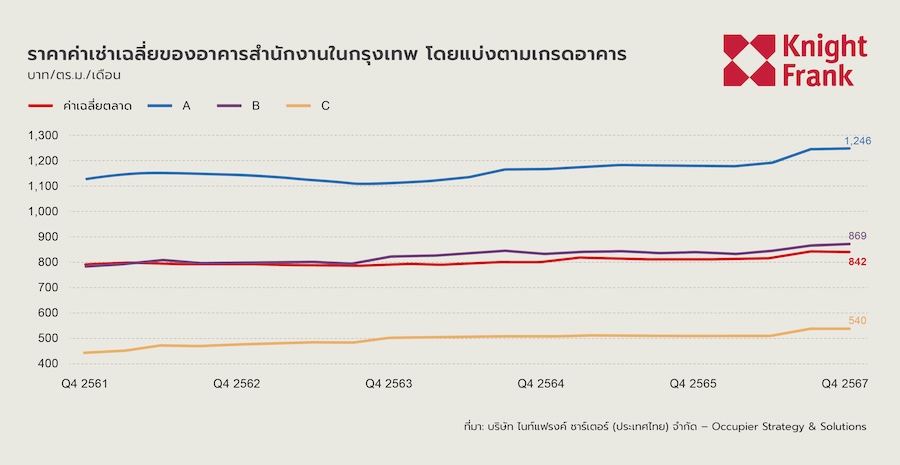

The overall market rental price remains stable at 842 baht per square meter per month, unchanged quarter-on-quarter but up 3.3% year-on-year. The average rent for Grade A increased by 0.4% quarter-on-quarter, reaching a new market high of 1,246 baht per square meter per month, while Grade B increased slightly by 0.2% to 869 baht. In contrast, Grade C remains stable, with a slight decrease to 540 baht.

Market Dynamics by Area

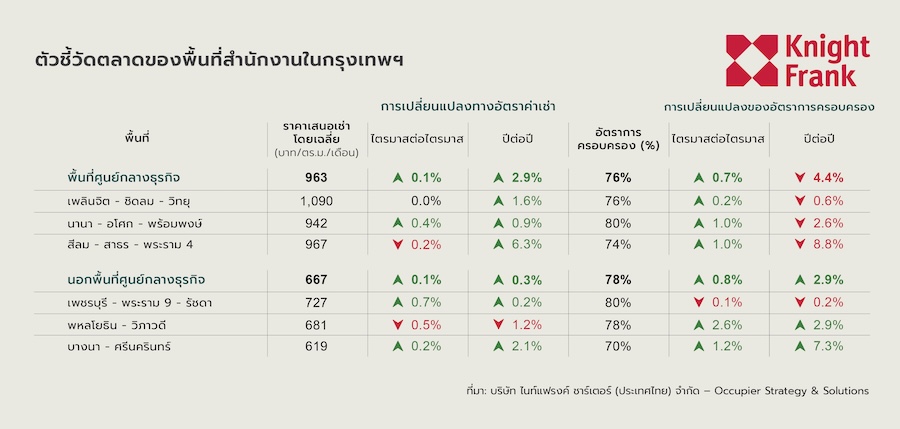

The Central Business District (CBD) saw a slight increase in rental prices, with the average rent rising by 0.1% quarter-on-quarter to 963 baht/sq.m./month. The occupancy rate increased to 76%, up 0.7% quarter-on-quarter.

- Ploenchit-Chidlom-Witthayu rental prices remained unchanged at 1,090 baht/sq.m., with the rental rate increasing by 0.2% quarter-on-quarter to 76%.

- Nana-Asoke-Phrom Phong saw a rental price increase of 0.4% quarter-on-quarter to 942 baht/sq.m., with a slight rental rate increase of 1.0% quarter-on-quarter to 80%.

- Silom-Sathorn-Rama 4 is the only area in the CBD to experience a slight decrease in rental prices, down 0.2% quarter-on-quarter to 967 baht/sq.m. However, the rental rate increased by 1.0% quarter-on-quarter to 74%.

Non-Central Business District (Non-CBD) rental prices increased slightly, with the average rent rising by 0.1% quarter-on-quarter to 667 baht/sq.m./month. The rental rate increased to 78%, up 0.8% quarter-on-quarter.

- Phetchaburi-Rama 9-Ratchada has the highest rental rate in the Non-CBD at 80%, despite a rental price increase of 0.7% quarter-on-quarter to 727 baht/sq.m.

- Phaholyothin-Vibhavadi saw a rental price decrease of 0.5% quarter-on-quarter to 681 baht/sq.m., but the rental rate increased by 2.6% quarter-on-quarter to 78%.

- Bangna-Srinakarin experienced a rental rate increase of 1.2% quarter-on-quarter to 70%, while rental prices increased slightly by 0.2% quarter-on-quarter to 619 baht/sq.m.

Review and Trends

In the latest quarter, the office market in Bangkok maintained a stable area of 6.31 million square meters, with no increase or decrease in supply. In 2024, the market saw a total supply increase of 235,000 square meters, similar to last year's rate, while the scaling down of future projects has reduced future supply to 1.0 million square meters. Leasing activity remains strong, with a net absorption of 48,000 square meters, resulting in a 1% increase in occupied space to 4.86 million square meters.

Notably, green-certified buildings have been able to attract significant demand, with a net absorption of 50,000 square meters compared to a slight decrease in non-green buildings. Both in the Central Business District (CBD) and Non-CBD areas, there is a positive trend, with net absorption of 27,000 square meters and 22,000 square meters, respectively.

The market is entering a period of significant change due to high supply pressure and evolving demand. It is expected that in 2025, there will be an addition of new space up to 540,000 square meters, which is considered the highest in the near future. Property owners will need to strategize to ensure their assets remain competitive, with Grade A buildings likely to benefit from their premium status due to tenant preferences for high quality, fully equipped facilities, and modern digital infrastructure integration.

For owners of older buildings, the decision to renovate or change properties, including defining the scope of improvements, will become increasingly important. Renovation costs will depend on the building's characteristics, location, size, necessary upgrades, and existing facilities, which need to be assessed based on the specific characteristics of each property.

Mr. Panya Jenkijwatanalert, Partner and Managing Director of the Office Space Division emphasized that “Currently, office buildings of all grades are continuously being developed and improved. Grade A buildings now have fully equipped facilities to meet tenant demands, while Grade B and C buildings should undergo retrofitting and improvements to retain existing tenants and attract more new clients”.

Another significant trend gaining attention is the return to traditional office work models. Some businesses are beginning to reduce remote work policies by increasing the number of days employees are required to work in the office or even returning to full onsite work. This change is becoming more popular, as employees respond positively to the structured environment and social and collaborative benefits of working in an office.

Although companies in Thailand that mandate employees to return to the office are fewer than the average in the Asia-Pacific (APAC) region , those operating in this manner face lower turnover rates and higher acceptance, indicating a stable return to office work models, albeit occurring in a limited manner.