Knight Frank Thailand Reveals Real Estate Trends for 2025: Condos and Offices Face Oversupply, While Hotels and Factories Continue to Grow

Knight Frank Thailand, a leading real estate consultancy in Thailand, led by Mr. Nattha Khaapan, Managing Director, has unveiled research data on the real estate market trends across four sectors for 2025 during the online seminar Knight Frank Foresight 2025: Collaboration. The findings indicate that condominiums and office buildings are still facing an oversupply situation, which is putting pressure on sales rates, while the rental market is growing due to an increase in expatriates and a recovering tourism sector. The hotel sector is benefiting from the tourism rebound, and the industrial and logistics sectors continue to grow due to foreign direct investment (FDI) and the expansion of the Eastern Economic Corridor (EEC).

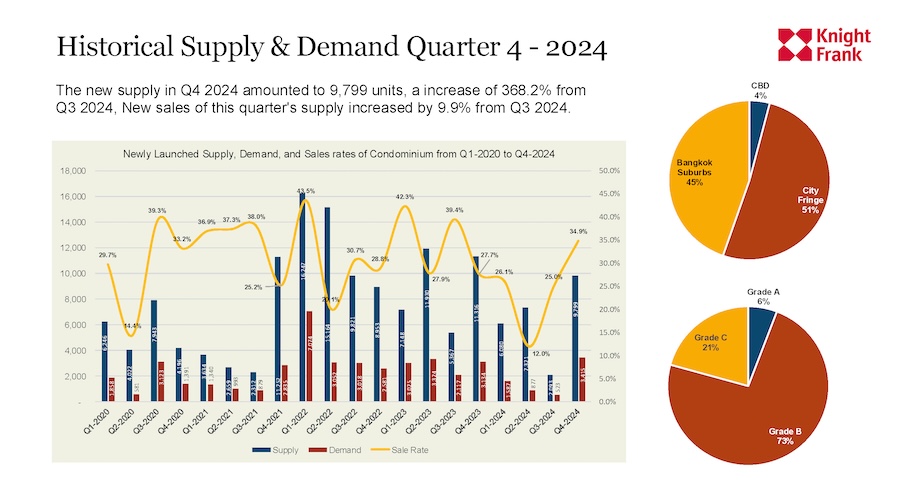

Mr. Sanchai Kueakchai, Senior Director and Head of Research and Real Estate Consulting, shared insights on the residential real estate market, stating that the condominium market in Bangkok is expected to see around 9,800 new units entering the market in the fourth quarter of 2024, a 360% increase compared to the previous quarter. However, new sales have only increased by 9.9%, keeping the overall sales ratio at 35%, below the healthy market threshold of 40%. More than 51% of this new supply is located in the outskirts of Bangkok, with 45% in suburban areas along the BTS lines. In the Central Business District (CBD), new launches have decreased, primarily consisting of Grade A projects, with the current average selling price in the CBD at 236,000 THB per square meter, while suburban areas and outskirts are at 127,000 and 72,000 THB per square meter, respectively.

For the luxury condominium market (Prime and Super Prime), priced above 200,000-250,000 THB per square meter, there has not been much change in new supply for 2024. Approximately 6,500 units are in the Super Prime category, while the Prime category has around 7,200 units, both groups achieving sales above 80%, indicating a healthy market. However, the overall real estate market remains sluggish, with expectations of fewer new projects this year compared to last year due to high supply and declining purchasing power.

Mr. Sanchai also pointed out that a potential factor to stimulate the real estate market is the increasing number of expatriates residing in Bangkok, which is expected to grow by 7.1% by the end of 2024, with the largest groups coming from China (28%), the Philippines (25%), and Japan (14%). This trend may lead to growth in the rental market, attracting investors back to condominiums in suitable locations. Additionally, the recovering tourism industry may boost demand for long-term rentals in certain areas. However, the condominium market in Bangkok will need to closely monitor economic trends and consumer purchasing power.

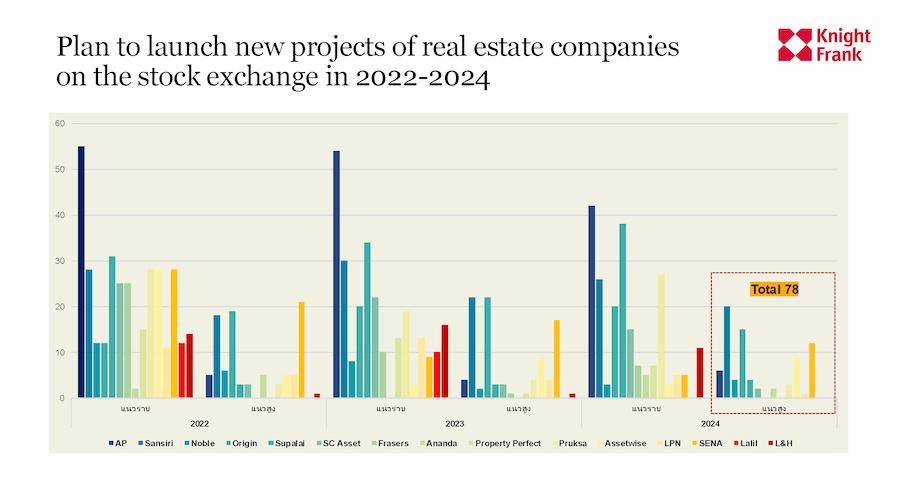

Mr. Frank Khan, Executive Director and Head of Residential, added that the real estate market in 2025 will continue to face challenges, particularly in the Bangkok condominium market, where major developers are delaying new project launches, with only 2-4 projects expected to enter the market this year. Some have begun exiting the Bangkok market to develop projects in Phuket or shift focus to single-family homes. Meanwhile, unsold condominium stock is being re-marketed at discounted prices, making this year a "buyer’s market." A noticeable shift is the growing popularity of luxury and ultra-luxury projects, which are well-received by high-net-worth individuals, with prices starting from 320,000 THB per square meter and a demand for larger units. Mixed-use projects are also gaining interest as they cater to consumers' lifestyles that prioritize reduced travel time and living in one place. Furthermore, the single-family home market remains promising, especially in the price range of 10-40 million THB, although increased competition is also making it a "buyer’s market" similar to the condominium sector. Key areas of interest for condominiums include Ploenchit, Chidlom, Rajdamri, Sathorn, and along the Chao Phraya River, where high-end projects continue to launch.

In addition to these trends, Mr. Frank noted that the demand for housing is changing, with younger buyers placing greater importance on quality of life. Convenience and connectivity to workspaces are key factors influencing housing purchase decisions. Regarding the hotel sector, Mr. Carlos Martinez, Director of Research and Real Estate Consulting, stated that Thailand's tourism sector is recovering strongly, with 35.5 million international tourists expected in 2024.

It is anticipated that this number will rise to 36-40 million in 2025. The Chinese market is beginning to recover but remains at 71% of pre-COVID levels, with an expected 9 million Chinese tourists this year. The average hotel occupancy rate in Bangkok is 79%, with room rates increasing by 7% compared to last year. In Phuket, tourist numbers have returned to pre-COVID levels at 5.3 million and are expected to increase in 2025. However, the tourism sector faces intensified competition from alternative accommodations such as Airbnb, serviced apartments, and budget hotels, which pose challenges for traditional hotels. Additionally, the country's image may be affected by crime news and travel warnings from certain countries, such as Taiwan, which could influence travel decisions among Asian tourists.

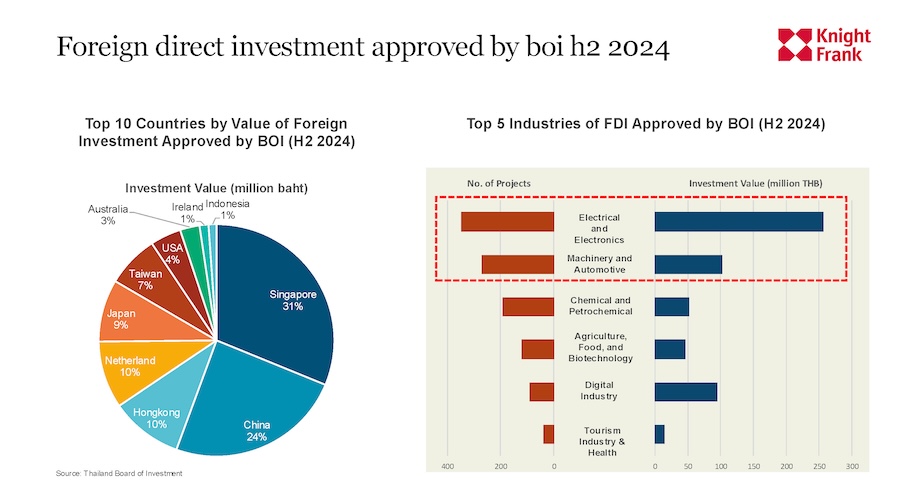

For the industrial sector, Mr. Marcus Bertenshaw, Executive Director and Head of Occupier Strategy & Solutions, revealed that Thailand's industrial and logistics sectors are experiencing strong growth, with industrial land sales reaching a record high of 12,340 rai, with over 64% of transactions occurring in the EEC. Furthermore, foreign direct investment (FDI) in the manufacturing sector has increased by 40%, amounting to 746 billion THB, and the expansion of factories has risen by 59%, demonstrating investor confidence. High-growth industries this year include electronics and semiconductors, electric vehicles (EV), and data centers. However, global trade conditions continue to impact the market, particularly U.S. retaliatory tax policies that may increase tax burdens on imports from countries with VAT systems like Thailand. The industries most likely to be affected include automotive, electronics, and food products, while trade within ASEAN and the RCEP agreement is becoming increasingly significant, prompting Thailand to accelerate the development of logistics infrastructure to support this trend.

Additionally, the logistics industry is playing an increasingly important role in supporting changing global trade trends. Knight Frank predicts that trade routes will shift, with Laem Chabang Port and the EEC Logistics Corridor becoming key hubs for cross-border transport. Meanwhile, Special Economic Zones (SEZs) and Free Trade Zones (FTZs) will be crucial factors in attracting investors to use Thailand as a primary manufacturing base.

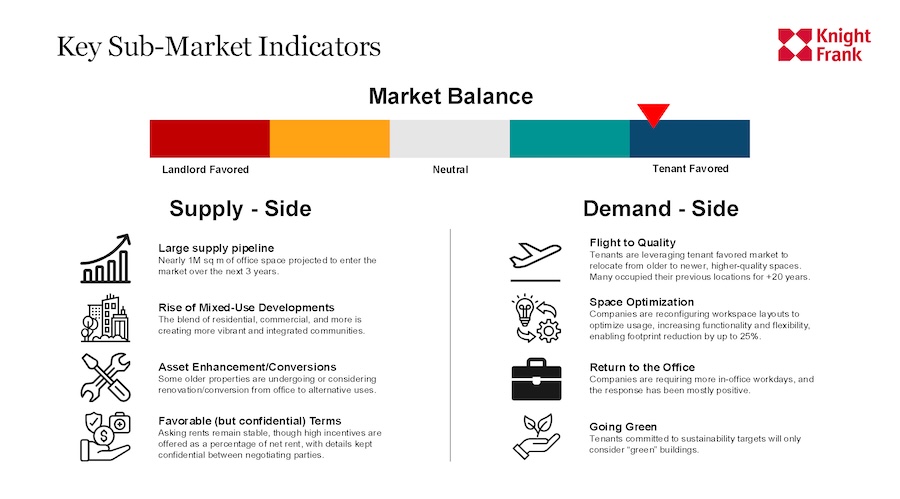

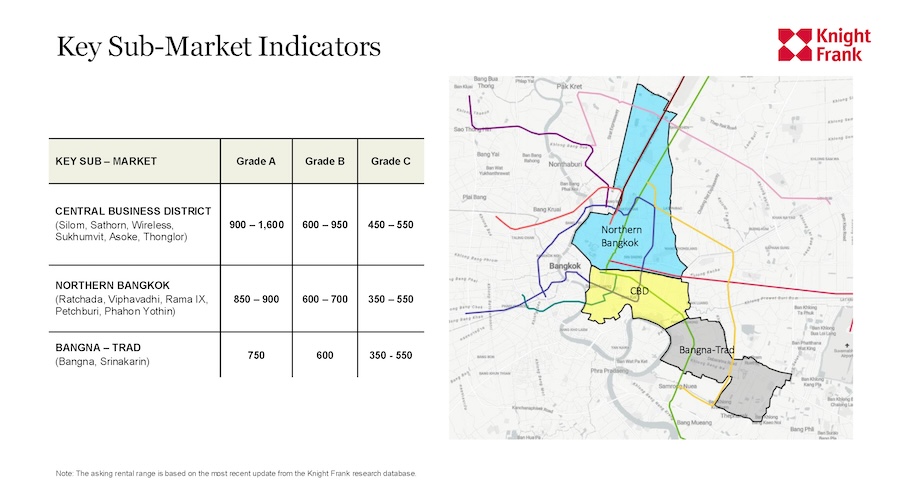

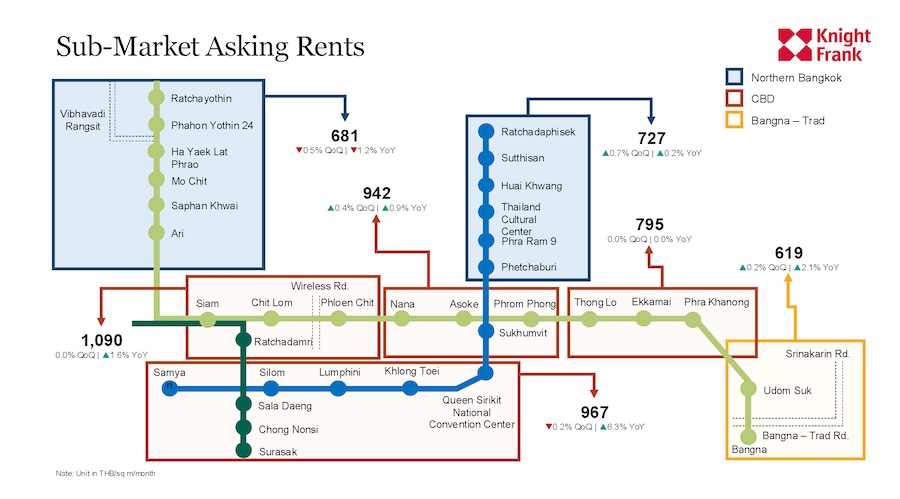

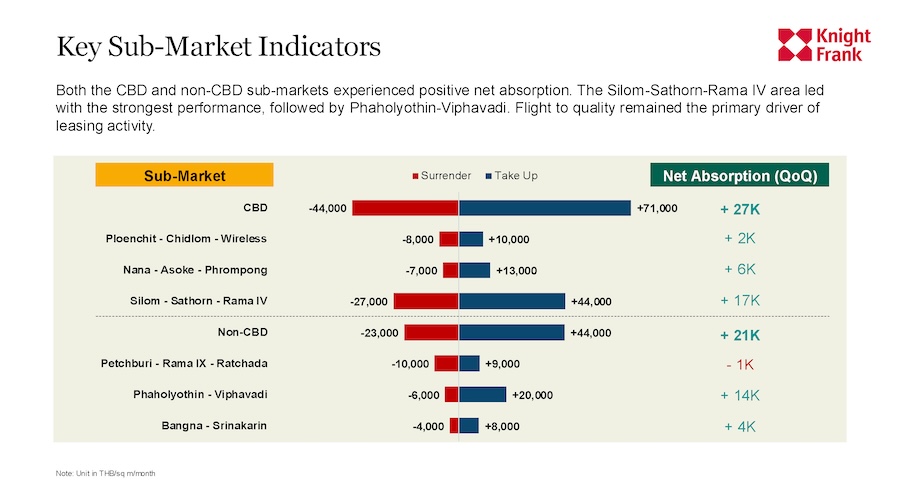

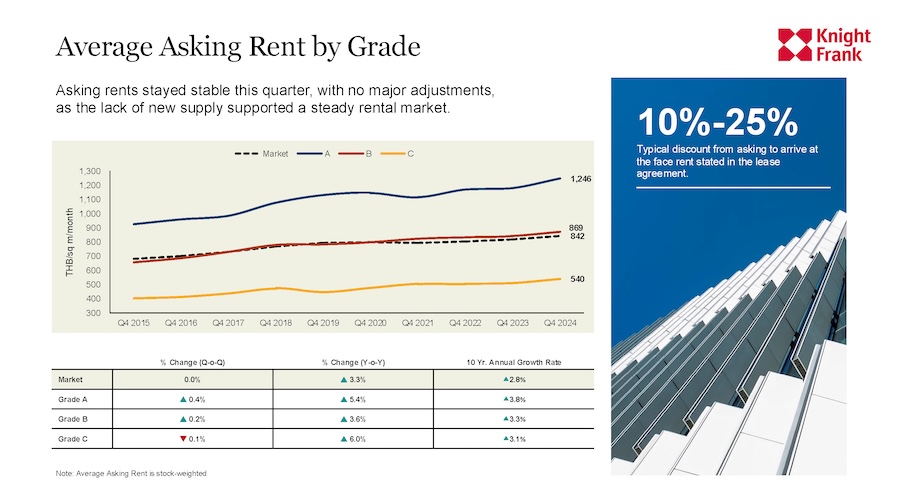

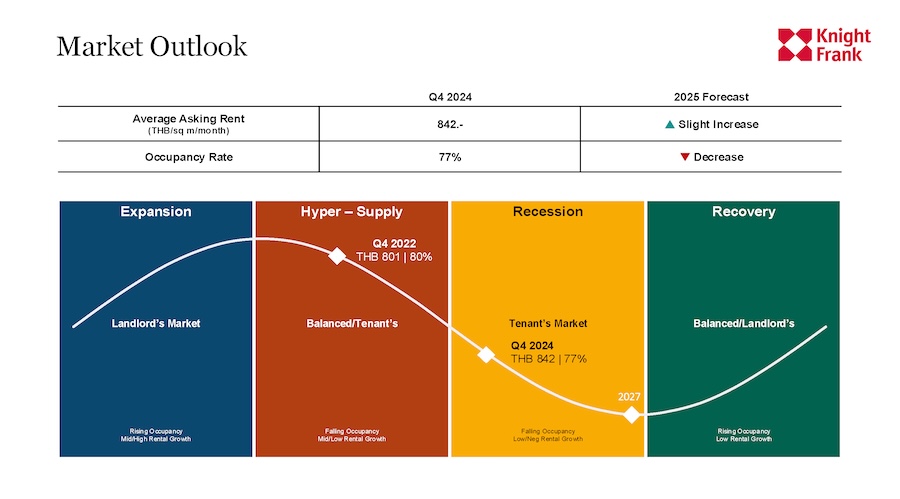

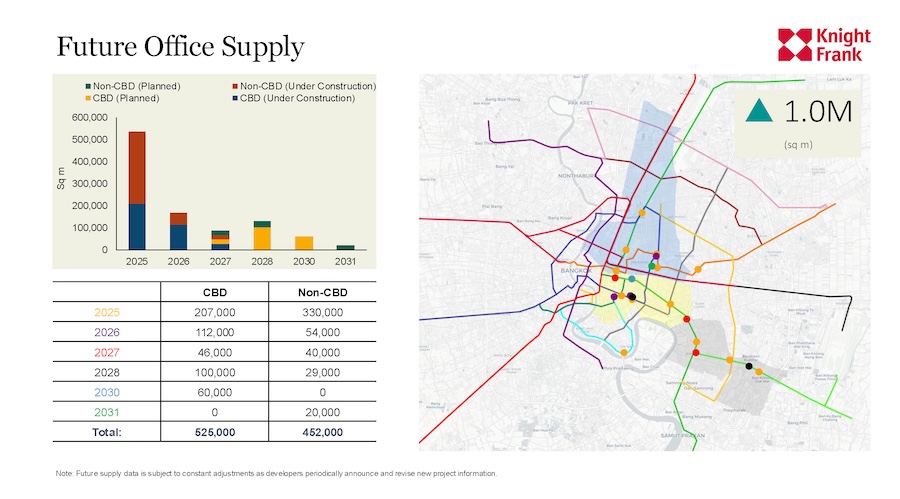

Mr. Panya Jenkijwatanalert, Executive Director and Head of Occupier Strategy & Solutions for the Office sector, revealed that the office market in Bangkok in 2024 continues to face an oversupply situation, with a total office space of 6.31 million square meters, a 4% increase from the previous year. The total leased area is 4.86 million square meters, increasing by only 2.2%, resulting in an overall market that remains a "tenant’s market" due to the continuous influx of new office buildings, particularly in the Grade A category in the CBD areas such as Silom, Sathorn, and Sukhumvit, where average rents range from 900 to 1,600 THB per square meter per month. In areas outside the CBD, such as Rama 9 and Bangna-Trad, average rents are below 1,000 THB per square meter. Although rents have remained stable or increased slightly by 3.3% compared to last year, building owners continue to offer special discounts of 10-25% to stimulate demand.

For the outlook in 2025, Mr. Panya predicts that overall rental rates will continue to decline, with the current occupancy rate at 77%, down 1.3% from the previous year, and expected to decrease further until 2027 before the market reaches a more balanced state. Key factors affecting the market include the trend of "Flight to Quality," where organizations are moving to higher-quality buildings, space optimization, and a focus on environmentally friendly buildings. The market recovery is expected to occur after 2027 when new supply begins to decrease and the market adjusts to a balance between building owners and tenants once again.

Mr. Nattha Khaapan, Managing Director of Knight Frank Thailand, concluded, "Knight Frank's research data highlights the diverse trends in Thailand's real estate market for 2025, reflecting the economy, purchasing power, and changing consumer behaviors. While the condominium market still faces oversupply, the demand for larger units and prime locations will be key driving factors. Meanwhile, the office sector continues to grapple with excess supply, and building owners must enhance quality and sustainability standards to retain and attract new tenants. Conversely, the hotel industry and manufacturing sector are buoyed by recovering tourism and foreign investment, particularly in the EEC, reflecting Thailand's potential as a regional economic hub. Knight Frank Thailand believes this presents significant opportunities for investors and developers who can adapt their strategies to align with the market, focusing on innovation, project development that meets demand, and sustainable management to build long-term resilience."