In 2025, Residential Property Transfers Expected to Decline by 4% for the Third Consecutive Year; LTV Measures May Stimulate the Market but Impact Might Be Limited

- In 2025, it is anticipated that residential property transactions will continue to decline for the third consecutive year due to high economic uncertainty, weak purchasing power among certain consumer groups, and rising housing costs.

- If LTV regulations are relaxed to 100%, it could positively impact the housing market; however, the effect of this measure may not be as significant as before, given the overall financial readiness of loan applicants remains weak.

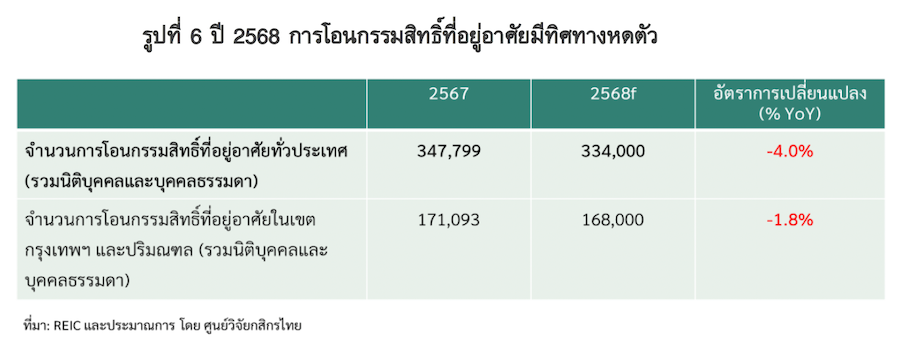

- The Kasikorn Research Center predicts that in 2025, the total number of residential property transfers nationwide, from both legal entities and individuals, will be approximately 334,000 units, reflecting a 4% decline (YoY).

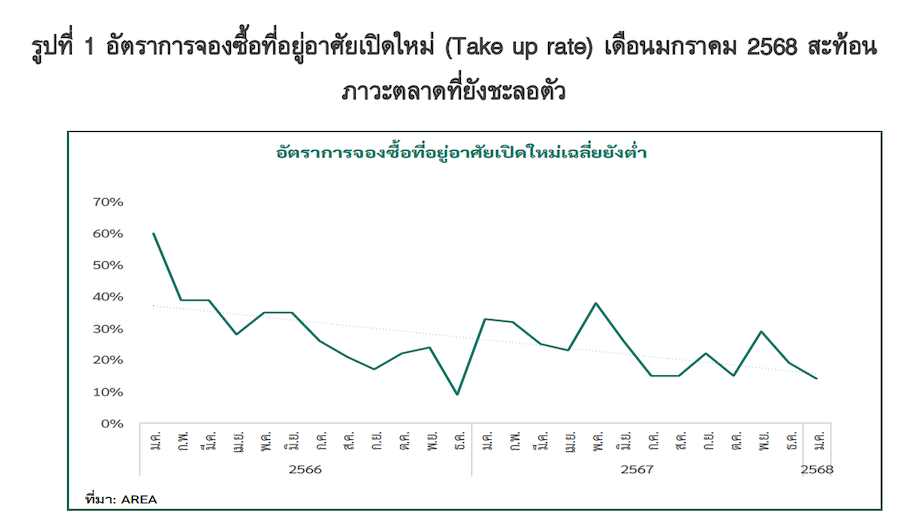

As the year 2025 begins, the demand for housing continues to show signs of slowdown from 2024. According to AREA data, the take-up rate for newly launched residential properties in Bangkok and its vicinity in January 2025 averaged 19%, a continued decline from 2024.

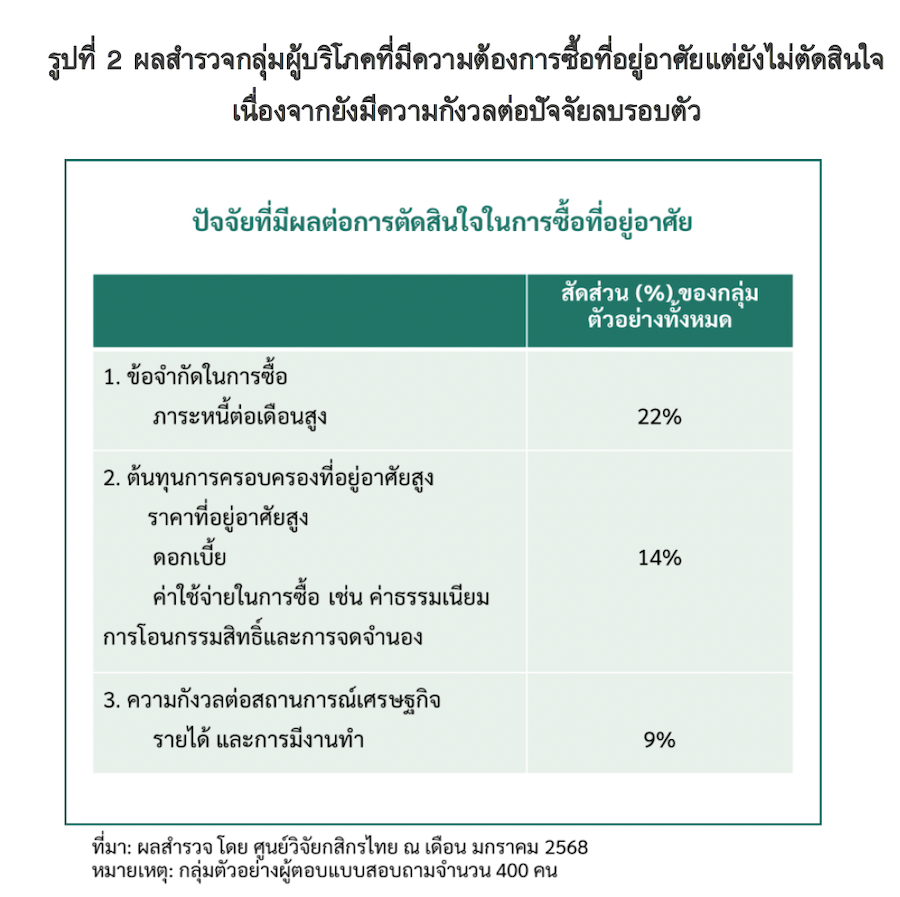

The remaining period of the year poses significant challenges for the housing market as new supportive factors remain uncertain, while the fundamental conditions of the market are still weak. A survey by the Kasikorn Research Center found that over half of respondents expressed a desire to purchase housing but have not made a decision to buy within the next 1-2 years due to various reasons.

- Constraints on purchasing power and high monthly expenses due to debts and daily living costs are significant issues for potential homebuyers. A survey by the Kasikorn Research Center revealed that over 3 out of 4 respondents from the Gen Y group, aged 28-39, which is a target demographic with high housing demand, have debt burdens (such as car loans, credit cards, and personal loans) exceeding the average of all groups by 22%.

- Rising costs of homeownership, including increased property prices and expenses related to purchasing homes, such as transfer fees, have become a concern. The measures to reduce transfer and mortgage fees ended on December 31, 2024, meaning that this year, homebuyers must pay the full fees. For instance, a property priced at 5 million baht would require the buyer to pay an additional 149,000 baht in transfer and mortgage fees.

- Economic pressures indicating a slowdown also contribute to uncertainty regarding future job security and income. A survey by the Kasikorn Research Center found that potential homebuyers in the next 1-2 years remain concerned about the future direction of the Thai economy.

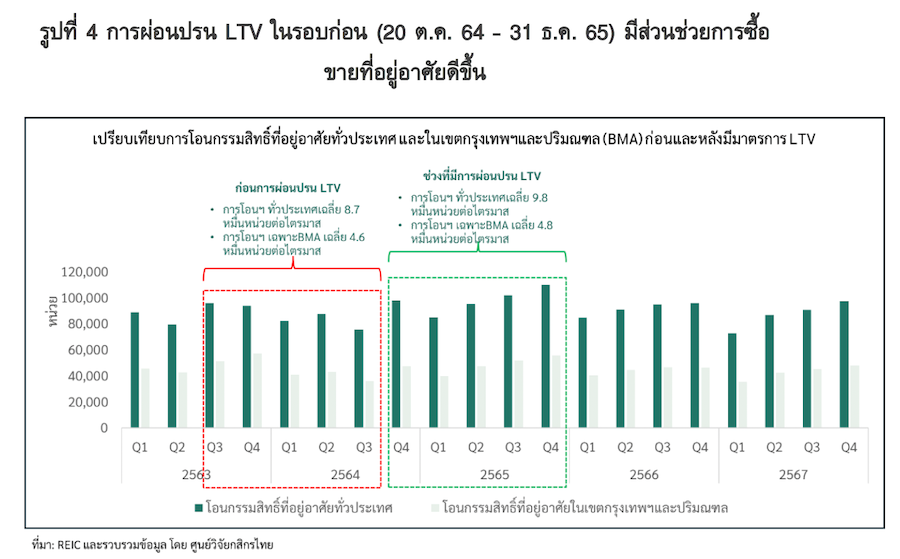

If the authorities relax LTV regulations, it could positively impact the housing market, enhancing homeownership capabilities. This was evident during the period from October 20, 2021, to December 31, 2022, when the Bank of Thailand temporarily relaxed the LTV ceiling to 100%, resulting in a 13% increase in nationwide property transfers compared to the average prior to the LTV relaxation, while transfers in Bangkok and its vicinity increased by 6%.

However, if LTV is relaxed this time, the positive impact on the housing market may not be as significant as before, as reflected in the demand for housing even in the mid to upper segments (unit prices of 7.5 million baht and above), where transfer numbers still declined by 9.3% in 2024.

The Kasikorn Research Center predicts that throughout 2025, housing transaction activities will decline for the third consecutive year, with residential property transfers nationwide from both legal entities and individuals expected to total approximately 334,000 units, reflecting a 4% decline (YoY). In Bangkok and its vicinity, the number of transfers may reach 168,000 units or a decline of about 1.8%.

Monitoring the authorities' stance on LTV measures, including conditions and timelines, as well as other measures such as tax incentives and reductions in housing transaction fees, will be crucial. If there are relaxations, it could stimulate housing demand, but the actual outcomes will still depend on economic factors, as well as the financial readiness and qualifications of individual loan applicants, given that purchasing a home is a long-term commitment amid high uncertainty regarding purchasing power and income.