Major Public Company Reports First Half 2024 Earnings, Revenue Surpasses 10 Billion

Property DNA has revealed that the first six months of 2024 have been challenging for various businesses, including the real estate sector, which is closely linked to many other industries (Supply Chain). Companies have had to devise strategies to generate revenue. Consequently, past governments have consistently implemented measures to stimulate purchasing power in the real estate market, and the current government introduced measures to boost the market in early April. These measures may have had some positive effects for certain buyer groups and price levels. However, the true impact of government measures on the market can be assessed by examining the revenue of various real estate operators.

Recently, operators in the stock market have begun to announce their earnings for the past six months. Mr. Surachet Kongcheep, Managing Director of Property DNA, believes that many operators still maintain stable revenues and continuous profits, with some achieving nearly 50% of their revenue targets for the entire year of 2024. This has alleviated concerns for the remainder of the year, and there may even be surprises at the end of the year if there is a rush to transfer ownership before the government's measures expire at the end of 2024. It is common to see a surge in ownership transfers as the deadline approaches, leading to increased sales and revenue.

Note: Some operators may provide updates later.

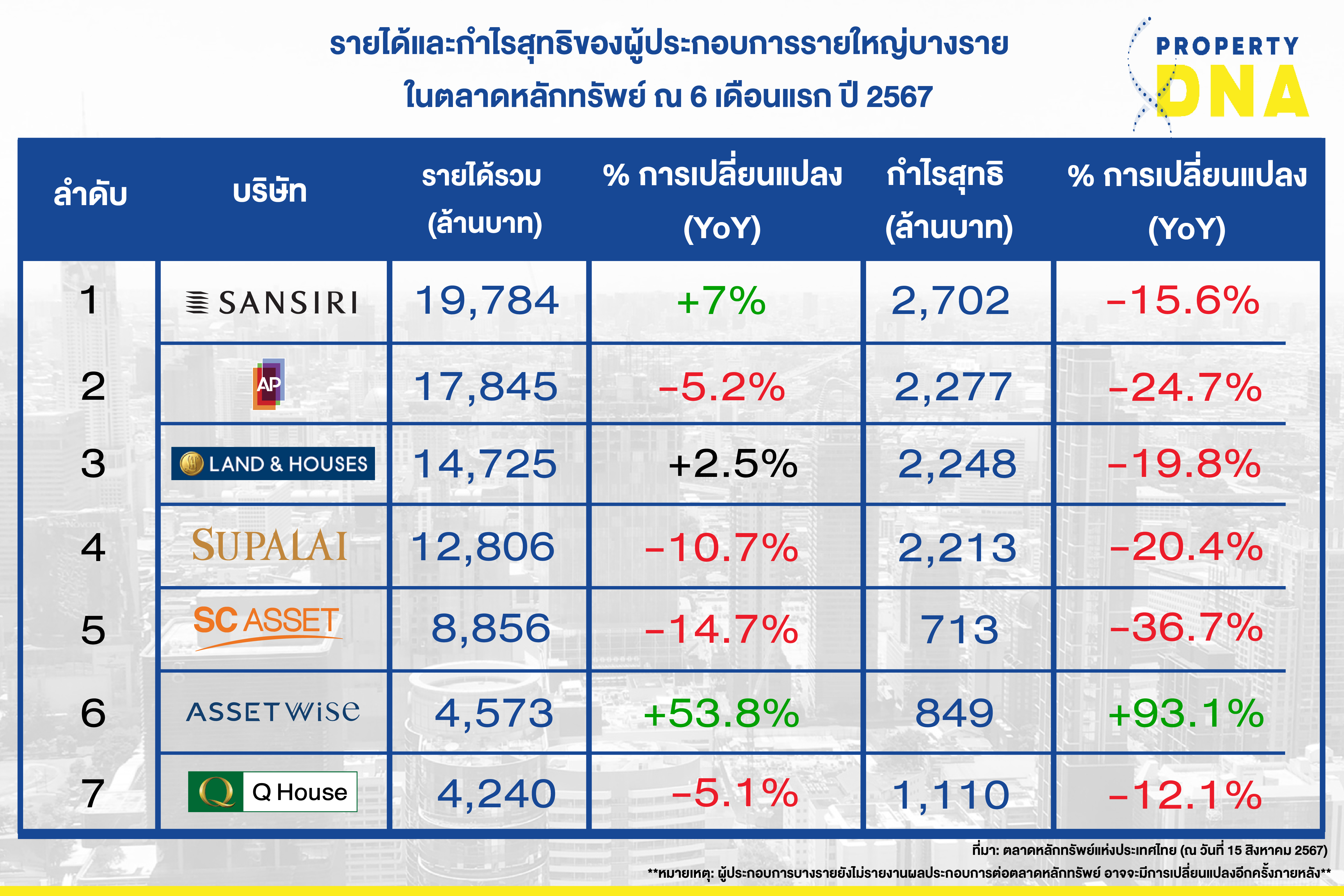

The operator with the highest revenue and profit in the first half of 2024 is Sansiri Public Company Limited, which reported revenue of 19.784 billion baht and a net profit of 2.702 billion baht from closing sales on 15 projects, resulting in a revenue increase of approximately 7% compared to the same period last year. Following in second place is AP (Thailand) Public Company Limited with total revenue of 17.845 billion baht and a net profit of 2.277 billion baht, with most revenue recognized in the second quarter. In third place is Land and Houses Public Company Limited, followed by Supalai Public Company Limited.

All four top companies reported revenues exceeding 10 billion baht and net profits above 2 billion baht. Analyzing the revenues of major operators that have announced their first half results does not clearly indicate whether the housing market is slowing down or contracting significantly, as some operators experienced only minor revenue declines compared to the same period last year. Last year was also a time when the housing market did not expand significantly, so lower revenues compared to last year might reflect signs of market slowdown.

However, a review of the revenues of stock market operators currently shows a clear increase in revenue during the second quarter of this year, likely due to government measures stimulating housing purchases. Despite challenges in securing retail loans from financial institutions, which have become stricter, along with rising interest rates and the overall economic outlook for Thailand not yet showing signs of recovery this year, some buyers who do not urgently need to purchase housing may delay their decisions. Although purchasing next year or later may require higher payments due to the absence of government purchasing power stimulation measures, rising housing prices in line with market mechanisms, and increasing construction material costs, for those ready and wanting housing, buying this year is the most suitable option. Not only can they secure housing at unchanged or minimally changed costs, but it is also a time when operators may be flexible in pricing to generate revenue for their companies.

Therefore, the remainder of 2024 presents an opportunity for operators to continue generating revenue, especially from projects that have been completed or are about to be completed and ready for ownership transfer in 2024, aligning with government measures. Operators with discontinuous projects or those not covering all price levels may need to seek additional revenue channels.

Additionally, accessing foreign purchasing power has been another avenue that many operators have been pursuing continuously over the past few years. This includes not only buyers from China but also operators expanding their markets to buyers from Taiwan, India, Dubai, Russia, and Europe, as well as buyers from Myanmar who may currently face challenges.