27th Anniversary of the Thai Baht Float: Strong Foreign Reserves but Economic Challenges Await

- Today marks the 27th anniversary of the announcement to float the Thai baht. This article will reflect on the weaknesses of Thailand's financial economic structure at that time and compare it with the current context to stay informed, prevent repeating past mistakes, and support the ongoing recovery path of the Thai economy.

- The current economic and financial environment in Thailand is different from that of 1997, as the issues then stemmed from over-investment and excessive spending, along with a currency peg to the dollar under a basket of currencies system. In contrast, the challenges this time are more complex and differ from 1997, as most issues are medium- to long-term.

July 2, 2024, marks the 27th anniversary of the Thai authorities' shift from a basket of currencies exchange rate system that pegged the baht to the dollar to a managed float exchange rate regime. This adjustment in Thailand's exchange rate system was a significant turning point in the country's exchange rate policy, allowing the baht to move more in line with the fundamental factors of the Thai economy compared to the previous basket peg system, which not only lacked flexibility but also did not align with the true economic fundamentals of Thailand, leading to currency attacks during that time.

The flexibility was lacking and did not correspond with the actual economic fundamentals of Thailand, which was a catalyst for the currency attack at that time.

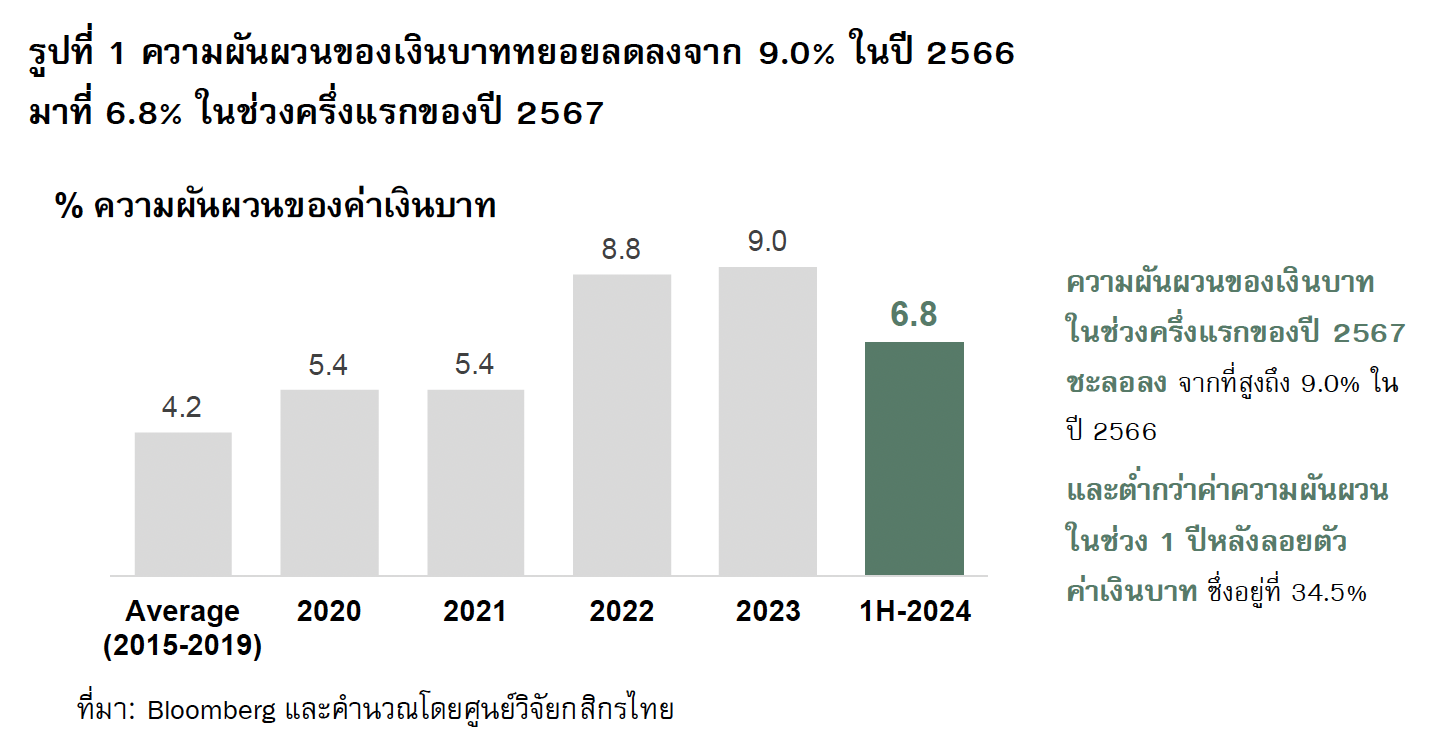

Looking back at the situation in 2024, while there is still an outflow of investment in the Thai stock and bond markets, the volatility of the baht in 2024 is showing signs of slowing down, decreasing from a high of 9.0% in 2023 to 6.8% in the first half of 2024 (Figure 1), significantly lower than the volatility of 34.5% observed in the year following the baht's float.

This reflects that under the Managed Float system, the Bank of Thailand plays a crucial role in managing movements and reducing the volatility of the baht. The challenges this year will revolve around various uncertainties, particularly regarding U.S. interest rate trends, global economic risks, capital flow directions in financial markets, and the recovery trajectory of the Thai economy.

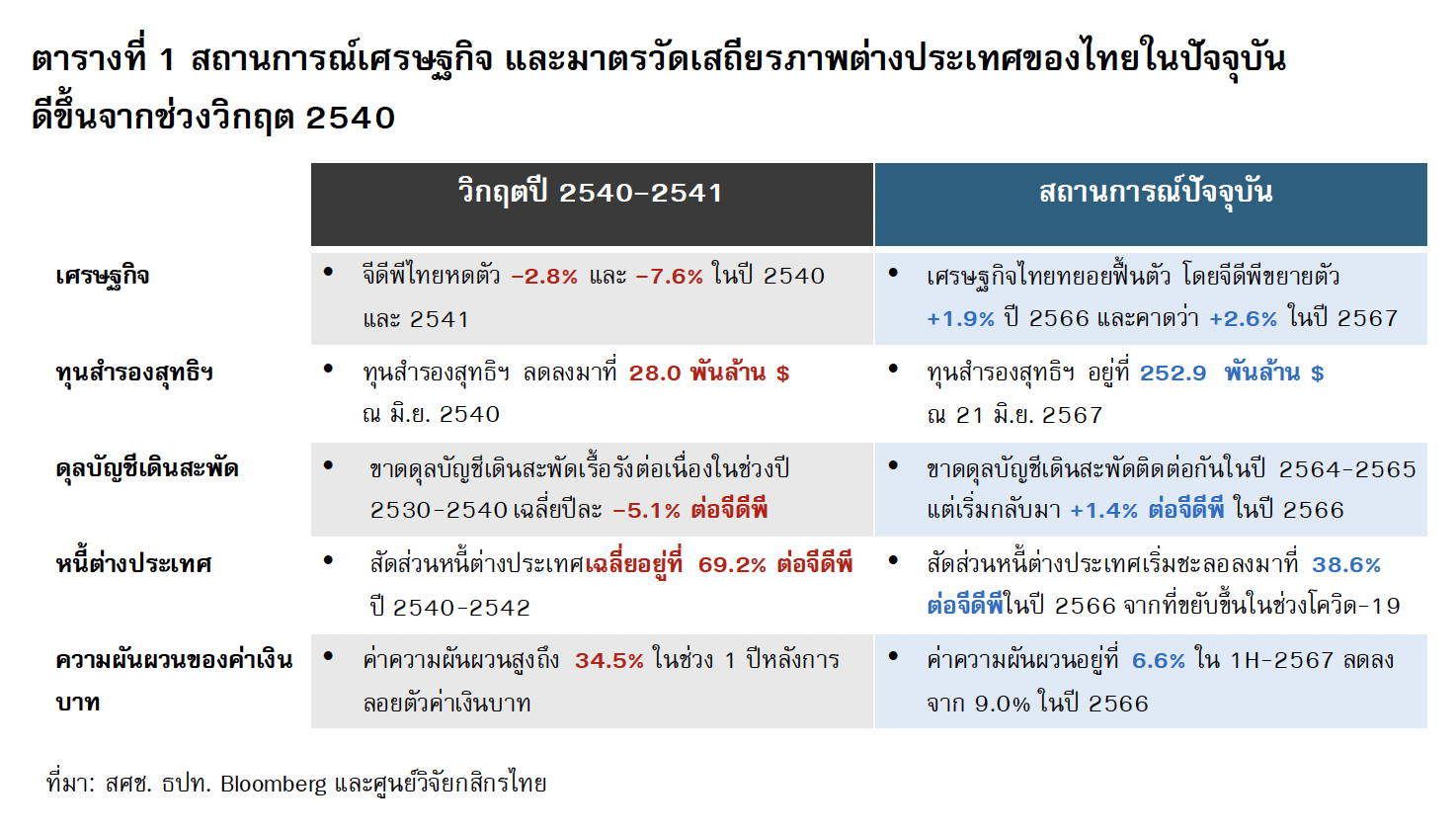

In terms of the economy, the current economic situation and various measures of Thailand's external stability have improved compared to the 1997 financial crisis (Table 1).

The Kasikorn Research Center believes that the 1997 financial crisis originated from internal imbalances and currency pegging, but the current economic situation in Thailand is gradually recovering from the impacts of COVID-19.

The 1997 financial crisis erupted from various imbalances, where the private sector and financial institutions lacked awareness of risks, overspending, and borrowing excessively, exposing them to maturity and currency mismatches, accumulating high foreign debt, and widespread speculation in the real estate market. Additionally, the overall economy faced chronic current account deficits throughout the period from 1987 to 1997, while the exchange rate was pegged to a basket of currencies, making it vulnerable to currency attacks, forcing Thai authorities to use foreign reserves to stabilize the baht. At that time, net foreign reserves dropped to just 28 billion dollars by June 1997.

Returning to the current situation, the Thai economy is gradually recovering from the COVID-19 crisis, with a clear distinction compared to the 1997 crisis: Thailand's current level of foreign reserves is significantly stronger. As of June 21, 2024, foreign reserves stand at approximately 253 billion dollars, sufficient to cover short-term foreign debt, three months of imports, and fully support currency issuance, while the ratio of foreign debt has decreased to 38.6% of GDP by the end of 2023. Authorities have also implemented measures to manage speculation in the real estate market, reflecting lessons learned from the crisis to prevent repeating past economic and financial patterns.

However, it must be acknowledged that the current economic challenges in Thailand differ from the past, as there are both immediate issues, particularly investor expectations regarding the situation and economic policies in Thailand, and challenges arising from uncertainties and structural issues that still need to be addressed, such as (1) high levels of debt in both the public and household sectors, (2) geopolitical issues and various forms of trade wars affecting the global supply chain, (3) the competitiveness of small and medium-sized enterprises, (4) preparing for Thailand's transition into an aged society, which will exacerbate labor shortages and public health burdens in the long term, and (5) preparing to cope with climate change.

It can be seen that the imbalances that arose during the 1997 crisis were gradually addressed after the baht was floated, with loans from the IMF and economic recovery measures. In contrast, the current challenges are more complex and differ from 1997, as most issues are medium- to long-term challenges that may lead to the accumulation of economic imbalances in another form. Therefore, all sectors should work together to create a new balance for the Thai economy to mitigate the impacts of structural limitations on Thailand's economic potential in the future.

[1] On July 2, 1997