Land in Nakhon Pathom: Hotspot for Urban Expansion - Q1/67 Prices Surge 89.4%

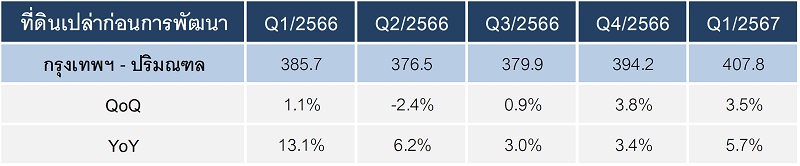

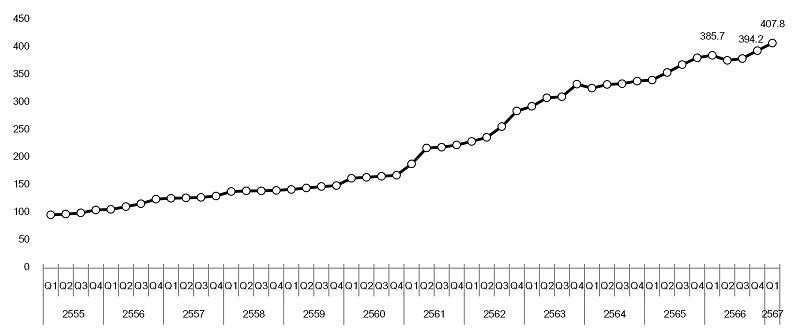

The Real Estate Information Center of the Government Housing Bank (REIC) has released a report on the Index of Vacant Land Prices Before Development in Bangkok and its Vicinity for Q1 2024 with an index value of 407.8 points, an increase of 5.7% compared to the same period last year (YoY) and a 3.5% increase compared to the previous quarter (QoQ). This indicates that the prices of vacant land before development are continuously rising, albeit at a slower rate than the average increase over the past five years before the COVID-19 crisis (2015-2019), which saw an average quarterly increase of 14.8% YoY and 4.1% QoQ.

Dr. Wichai Wiratthakhan, Inspector of the Government Housing Bank and Acting Director of the Real Estate Information Center revealed that the factors contributing to the continuous increase in the index of vacant land prices, albeit at a slowing pace, stem from the slow economic recovery both domestically and internationally in recent times. Additionally, Thailand's household debt is over 90% of GDP, and the rising interest rates remain high, affecting the ability to purchase housing. Furthermore, the land and building tax collection in 2024 does not include any measures to reduce land and building taxes, leading to a decrease in the accumulated demand for land in the Land Bank of developers. The accumulated land purchases will incur land tax liabilities, which will become a cost in future project developments.

Table 1: Index of Vacant Land Prices Before Development in Bangkok and its Vicinity for Q1 2024

Chart 1: Index of Vacant Land Prices Before Development in Bangkok - Vicinity

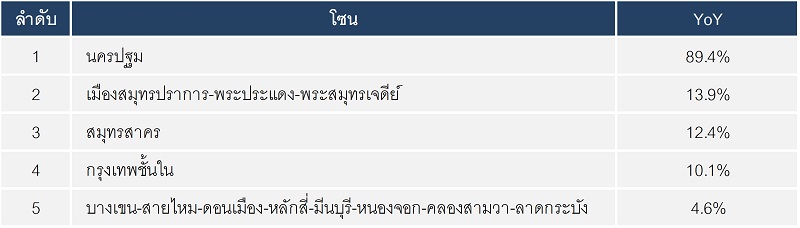

In Q1 2024, the top five zones with the highest land price growth compared to the same quarter last year (YoY) are as follows:

Rank 1: Nakhon Pathom land saw a price change of 89.4%.

Rank 2: Land in the Samut Prakan - Phra Pradaeng - Phra Samut Chedi zone experienced a price change of 13.9%.

Rank 3: Land in the Samut Sakhon zone had a price change of 12.4%.

Rank 4: Land in the inner Bangkok zone saw a price change of 10.1%.

Rank 5: Land in the Bang Khen - Sai Mai - Don Mueang - Lak Si - Min Buri - Nong Chok - Khlong Sam Wa - Lat Krabang zone experienced a price change of 4.6%.

Land in the suburban areas of Bangkok and its vicinity has seen significant price changes due to urban expansion, the development of expressways, and plans for new and extended rail mass transit projects, making it easier for residents in the suburbs to commute to and from the city. Additionally, land prices in the suburbs remain relatively low, allowing for the development of horizontal housing projects that align with the purchasing power of those seeking affordable housing.

In contrast, central urban locations have seen price increases, but the rate of change is not as high due to the limited availability of vacant land before development and the already high prices of urban land, resulting in lower growth rates compared to suburban areas of Bangkok and its vicinity. Some developers are increasingly interested in developing residential projects in inner Bangkok, particularly high-rise housing projects, which aligns with survey data from Q4 2023 indicating a significant number of new condominium projects launched in that area, increasing by 10.8%.

Table 2: Zones with the Highest Price Change Rates - Top 5 for Q1 2024

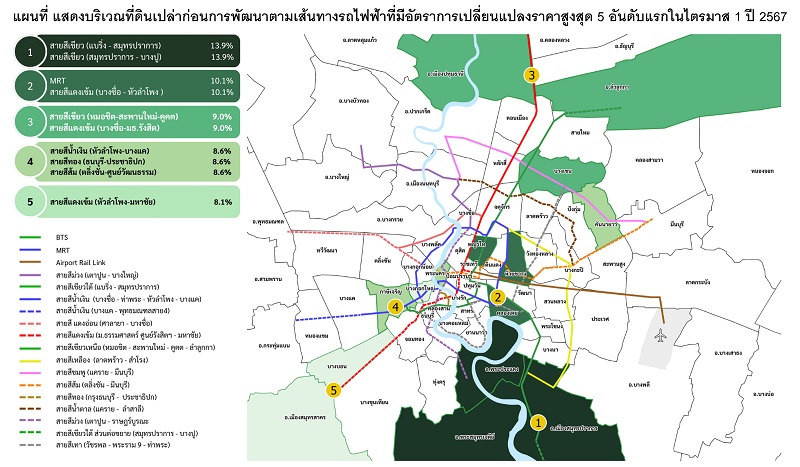

For vacant land prices before development along the routes with electric trains in Q1 2024, the top five electric train routes with the highest land price growth compared to the same quarter last year (YoY) are primarily located in areas where electric train projects are already operational and future projects connecting to key commercial areas. The details are as follows:

Rank 1: Green Line (Samut Prakan - Bang Pu) is a future project, while Green Line (Bearing - Samut Prakan) is already operational, with index values of 265.1 points and 261.2 points, respectively, showing a land price growth rate of 13.9% YoY. The land prices in Phra Pradaeng and Phra Samut Chedi have seen significant increases, while some areas in Samut Prakan, such as Thaiban and Thaiban Nuea, have also experienced price increases.

Rank 2: Blue Line (MRT) is already operational, while the Dark Red Line (Bang Sue - Hua Lamphong) is a future project, with index values of 522.0 points and 513.8 points, respectively, showing a land price growth rate of 10.1% YoY. The land prices in Phaya Thai, Khlong Toei, and Huai Khwang have seen significant increases.

Rank 3: Green Line (Mo Chit - Saphaan Mai - Khu Khot) is already operational, while the Dark Red Line (Bang Sue - Thammasat University Rangsit) is partially operational, with index values of 486.8 points and 479.3 points, respectively, showing a land price growth rate of 9.0% YoY. The land prices in Bang Khen, Lam Luk Ka, Pathum Thani, and Sam Khok have seen significant increases.

Rank 4: Blue Line (Hua Lamphong - Bang Khae) is already operational, while the Gold Line (Thonburi - Prachathipok) is also operational, and the Orange Line (Taling Chan - Cultural Center) is a future project, with index values of 503.1 points, 495.9 points, and 488.2 points, respectively, showing a land price growth rate of 8.6% YoY. The land prices in Phra Nakhon, Khan Na Yao, and Phasi Charoen have seen significant increases.

Rank 5: Dark Red Line (Hua Lamphong - Mahachai) is a future project, with an index value of 476.9 points and a land price growth rate of 8.1% YoY. The land prices in Samut Sakhon, Bang Bon, and Bangkok Yai have seen significant increases.

Table 3: Index of Vacant Land Prices Before Development Along Electric Train Routes with the Highest Changes - Top 5 for Q1 2024