Thai Banking System's Hire Purchase Loans Expected to Grow 1.5% in 2024, While NPL Ratio May Rise to 2.22%, Says Kasikorn Research Center

- In 2024, the hire purchase loans of the Thai banking system are expected to return to positive growth at 1.5% due to increased new car sales, although this remains significantly lower than the over 6.0% annual growth seen five years prior to the COVID-19 crisis.

- The NPL ratio is on the rise, while price competition remains fierce due to a limited customer base.

The structure of the car hire purchase market for retail customers in Thailand is heavily weighted towards commercial banks. According to market share, it consists of commercial banks, captive finance companies, and non-bank financial service providers, respectively. Kasikorn Research Center estimates that the share of hire purchase loans from commercial banks, the largest service providers in the market, is around 60-65% of total hire purchase loans. Meanwhile, the combined share of loans from captive finance companies and other non-bank providers is about 35-40% of the total market. This share may fluctuate based on market conditions and the aggressive marketing policies of first-hand car operators, but the main market remains with commercial banks due to their larger branches and customer base.

When considering the classification of hire purchase loans by new and used cars, it is expected that the share for new cars will be around 80% and for used cars around 20%. The main players in the used car market will primarily be non-bank service providers, especially non-banks and car dealerships, while commercial banks will have a relatively small portion of used car loans, particularly among large and medium-sized banks.

Given the above picture, along with the published data that only pertains to commercial banks, this article will reference the direction of commercial bank portfolios. The analysis will primarily rely on data from the Bank of Thailand. Generally, the key factors affecting the trend of hire purchase loans will be three main parts: 1) The trend of new car sales, which will impact the influx of new loans; 2) The management policies for the quality of existing loan portfolios, especially debt write-offs, which will reduce outstanding loan balances; and 3) The repayment rates of existing loan portfolios, which depend on the conditions of initial down payments and the duration/number of repayment installments. This factor will also determine the speed of reduction in outstanding loans.

|

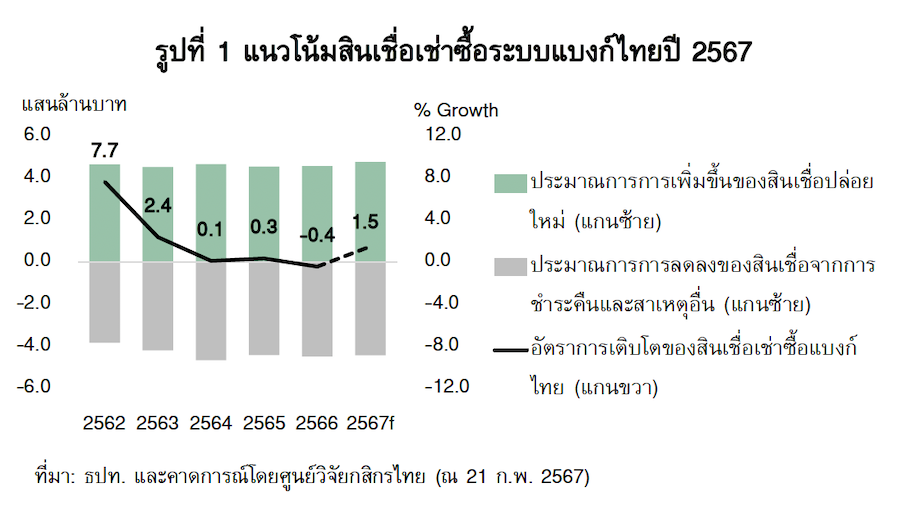

“In 2024, Thai banks' hire purchase loans hope to benefit from increased new car sales, offsetting the impact of expected debt write-offs that are anticipated to be similar to last year.” |

Looking ahead to 2024, the variables that will influence whether the growth rate of hire purchase loans can turn positive (after contracting by 0.4% in 2023) will depend significantly on new car sales and the rate of debt write-offs by operators. It is anticipated that the benefits from the acceleration of new car sales (projected at 800,000 units compared to 776,000 units in 2023) will outweigh the expected debt write-off rate in 2024, which is expected to be similar to that of 2023. Ultimately, this may lead to a reversal in outstanding hire purchase loans expanding by 1.5% to reach 1.197 trillion baht. (See Figure 1)

However, due to the still uneven economic recovery, coupled with high household debt and purchasing power issues, the growth rate of the aforementioned hire purchase loans is still considered limited, especially when compared to the period five years before COVID, which saw growth rates exceeding 6.0% annually.

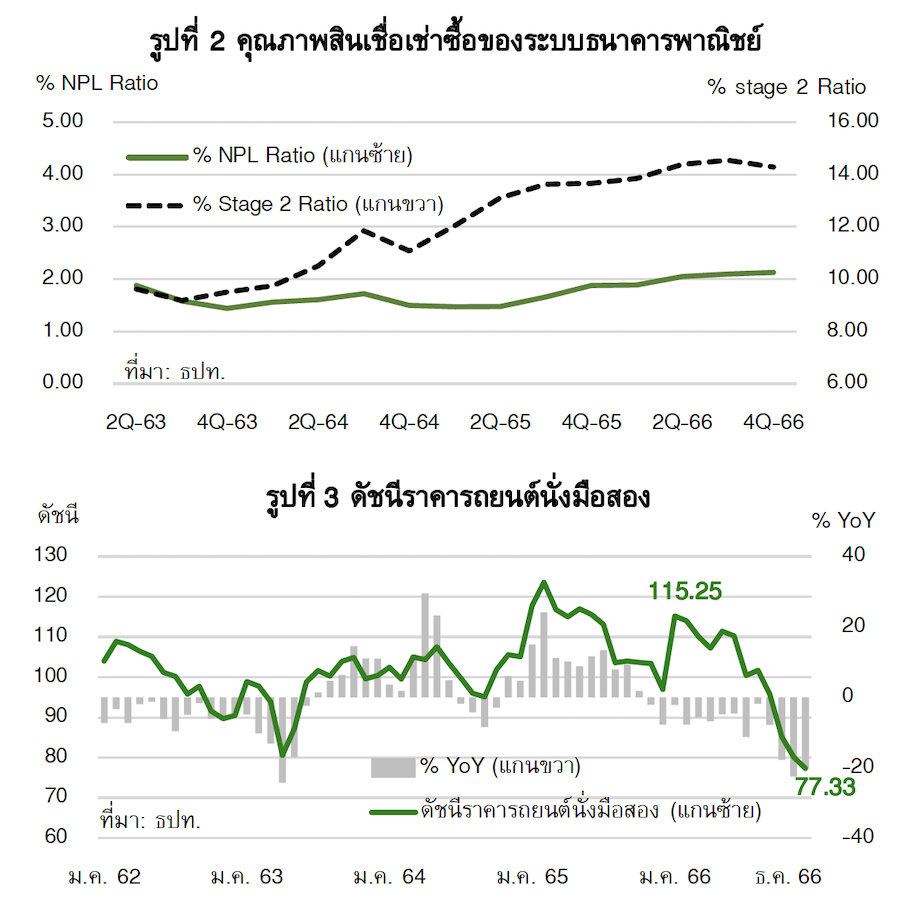

The situation of non-performing loans (NPLs) in hire purchase loans remains a concern. According to data from the Bank of Thailand, the NPLs of hire purchase loans in the commercial banking system increased from 2.51 billion baht at the end of 2022, accounting for 1.89% of total hire purchase loans, to 2.51 billion baht, representing 2.13% of total loans.

|

“However, the still uneven economic recovery pressures the issuance of hire purchase loans to remain below pre-COVID levels, raising concerns about debt quality.” |

For 2024, Kasikorn Research Center predicts that the outstanding NPLs will continue to rise from 2.51 billion baht to 2.66 billion baht, which is an increase at a slowing rate for the second consecutive year, even though Stage 2 loans remain relatively high. This is due to the view that service providers will focus more on debt restructuring, following government policies, and will continue to rapidly write off bad debts. Additionally, the repayment behavior of debtors during times of income to maintain their vehicles from being repossessed also prevents the debt status from quickly flowing into Stage 3 (NPLs). These various factors, combined with a larger loan base, are expected to push the NPL ratio to 2.22% of total hire purchase loans in 2024, up from 2.13% in 2023.

In addition to the trends in loans and debt quality mentioned above, Kasikorn Research Center has views on other issues related to the business strategies of service providers as follows:

- Main hire purchase loan providers, such as commercial banks, will continue to adopt a cautious lending policy, focusing on potential customer groups with medium to high income and purchasing power, including electric vehicles as an alternative family car, which may include interest-free hire purchase programs or low-interest installment plans over a longer period.

for over a year as an option for consumers, while continuing to reduce the weight of used car loan issuance.“Price competition among operators remains high, amid a limited potential customer base, while operators must also focus on additional business areas,”

such as cash-for-car programs to maintain profitability.”

- Price competition is expected to remain intense among target customer groups, amid high competition among operators and a limited potential customer base. Meanwhile, the trend of domestic interest rates is expected to decline, which will positively affect the cost for service providers and help them have more flexibility in approving loans.

- Hire purchase loan providers may increase marketing efforts in cash-for-car loans, which offer high returns, to maintain profitability amid limited growth in new loans.

Factors to monitor include the popularity of electric vehicles (BEV) and regulations from the authorities. In the past, the popularity of BEV vehicles has impacted the competitiveness of car manufacturers and the group of captive finance service providers that primarily market traditional combustion engine vehicles. Therefore, in the near future, it will be essential to monitor the strategic adjustments of combustion engine manufacturers, as well as the potential entry of BEV manufacturers into the hire purchase loan market, which will affect the competitive landscape going forward. Additionally, regulatory guidelines that are gradually being implemented and are under scrutiny include responsible and fair lending criteria, which are expected to apply to non-bank service providers once the hire purchase decree comes into effect. Kasikorn Research Center views that these guidelines will likely be a negative factor for the overall hire purchase loan market rather than a positive one, and operators will need to plan accordingly.

[1] Based on data from the Thai Hire Purchase Business Association in 2018, which found that the market share of hire purchase loans was 64.5% for commercial banks, followed by 29.0% for captive finance providers and 6.5% for non-bank providers.