Knight Frank Highlights Real Estate in 2024: Entering a Period of Stagnant Demand, Watch for High Reject Rates in Condos Under 3 Million and Oversupply in Office Space

Knight Frank Thailand reveals that the real estate market in 2024 still faces many risk factors, particularly in the residential, industrial, hotel, and office sectors, entering an era of overall stagnant demand, indicating a slowdown in purchasing power. Concerns remain for condos priced below 3 million, with a high reject rate reaching 50%. The office market is expected to see oversupply this year following the launch of three major mixed-use projects, although green buildings are still trending positively in line with the strong ESG movement. The industrial sector can expand due to the support from the EV market and data center businesses.

Mr. Nattha Khahapana, Managing Director of Knight Frank Thailand stated that the real estate market in 2024 is filled with challenges from various risk factors. Domestically, the country still faces low inflation, concerning household debt, rising production costs, and high interest rates affecting loan rejection rates from financial institutions, which currently stand at 40-50%, particularly for condos priced below 3 million. This reflects the purchasing power of a significant customer base in the country. Internationally, the global economy and trade face high uncertainty due to ongoing conflicts in various regions, and global financial markets are increasingly volatile due to the impact of high interest rates, affecting both directly and indirectly on the economy and the overall real estate market in Thailand.

However, there are still positive factors that may improve the outlook, such as expanding private investment and growing private consumption from the recovery of the tourism sector, along with government policies aimed at alleviating the cost of living and stimulating spending through the Easy E-Receipt

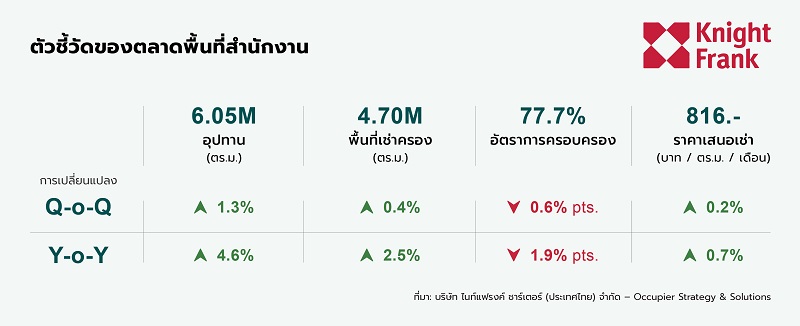

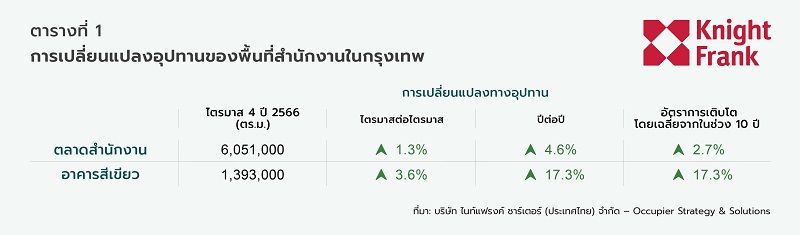

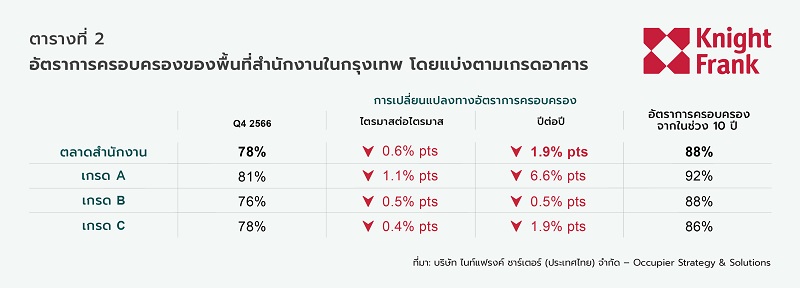

Watch for 2024: Office Supply Oversupply, but Green Buildings Continue to Grow with the ESG Trend

Mr. Panya Jenkijwatanalert, Executive Director and Head of Office Department stated that this year, the office market is entering a challenging phase due to increased supply. Although there has been a significant demand for space in 2023, the rental rates have not yet grown, leading to an oversupply situation, particularly for Grade A offices where competition is intensifying. However, there are positive signals from multinational companies looking to relocate their operations to Thailand, especially from Chinese companies in the EV sector, which are starting to seek office space in Thailand, particularly in the Ratchada area.

Thai companies are also increasingly looking for office space of all grades for their operations, focusing on price and amenities within the buildings that can support employee activities and enhance the company's image and credibility.

Meanwhile, offices with sustainability concepts are seeing an increase in demand for rentals. Mr. Ayuthaporn Buranakul, Executive Director and Head of Strategy for Service Office Space Projects, stated that currently, international clients, including leading companies in Thailand, are increasingly seeking offices with sustainability concepts (ESG: Environment, Social, and Governance), particularly Green Buildings that are gaining popularity, as well as office spaces that emphasize work-life balance, aligning with future business directions that prioritize sustainability and carbon reduction.

Residential Market Grows Slowly, Reject Rate Reaches 50%, Indicating Risks for Condos Below 3 Million

Mr. Frank Khan, Executive Director and Head of Residential Division stated that in 2024, the residential market still faces issues with loan rejections from financial institutions and rising costs for developers, making the development of products priced below 3 million baht less viable. The landed house market is entering a phase of slow growth as it is a real demand market where customers buy for living. Although demand still exists, it is not keeping pace with the increasing supply entering the market recently, with an estimated 4,000 houses expected to be sold this year.

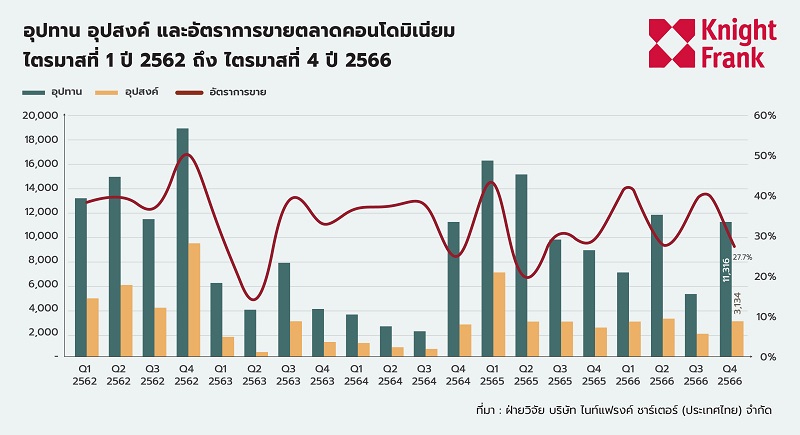

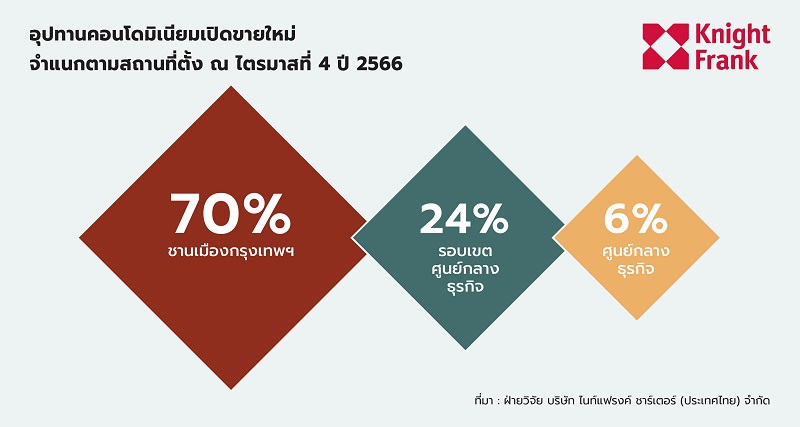

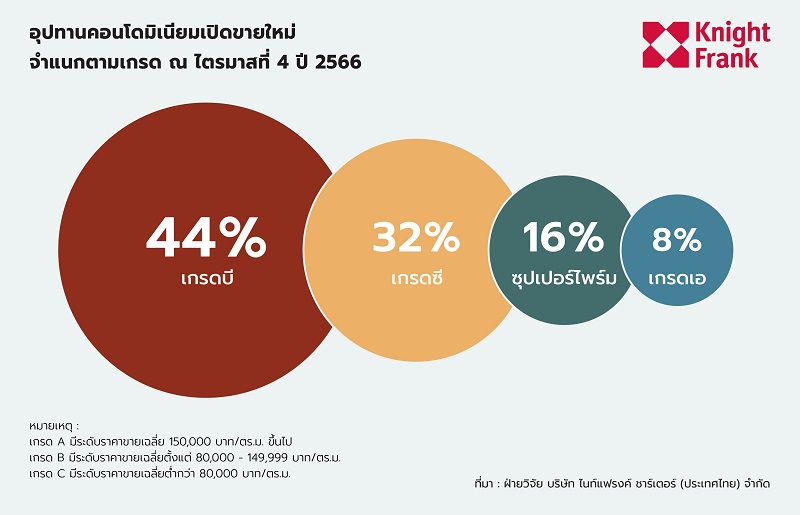

In the condo market, in 2023, there were 745,335 units launched for sale, with 527,067 units sold, accounting for 70.7%, with an average price of 145,000 baht per square meter. If we look at the sales of newly launched units each quarter, we find that only about 30% of sales have been achieved.

Particularly for condos priced below 3 million, which is a segment where many developers have launched projects, while the market for units priced between 10-15 million still performs well.

“EV-Data Centers” are Booming, Driving Industrial Sector Growth

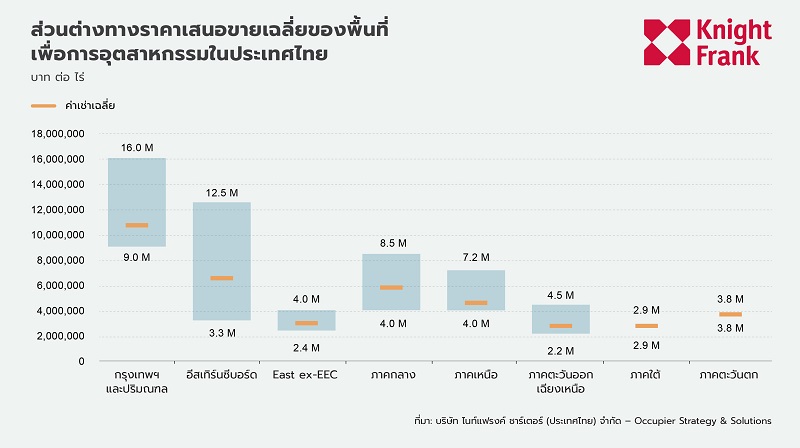

Mr. Marcus Bertenshaw, Executive Director and Head of Occupier Strategy & Solutions stated that the businesses of Data Centers and EV are two sectors to watch this year, as both domestic and foreign investors are showing interest, which is a positive sign of increasing demand in the industrial sector. In 2023, the overall industrial market has shown significant growth, with land sales reaching 8,867 rai, double that of 2022, particularly in the EV sector and electronics, which are expanding well. The Eastern Economic Corridor (EEC) remains a primary target area for investors, accounting for over 80% of all transactions.

Hotel Sector Brightens, Room Rates Surge as It Prepares for the Year of the Dragon

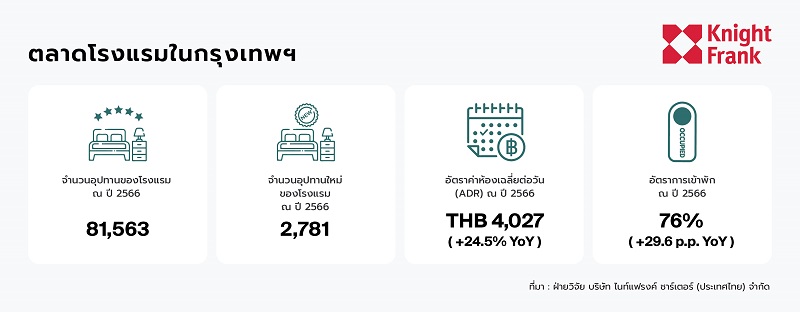

Mr. Carlos Martinez, Director of Research and Consulting stated that the hotel market is currently back to pre-COVID conditions, with room rates significantly increasing, even though the number of tourists has not yet returned to pre-COVID levels. Therefore, a major challenge for the hotel market in 2024 is whether the number of tourists will recover to pre-COVID levels. In 2023, the occupancy rate for tourists was approximately 76%, an increase of 29.6% compared to the previous year, but still below the pre-pandemic level of 84% in 2019. International tourists play a crucial role in maintaining high occupancy rates throughout 2023, ranging from 72-78%, with occupancy levels in cities not varying much across seasons, reinforcing the ability to maintain occupancy levels consistently throughout the year.

For the number of international tourists traveling to Thailand in 2023, it exceeded initial projections, nearing 30 million, with 25 million in Bangkok, an increase of 2.4 times from the previous year, accounting for 71% of the number of tourists in 2019.

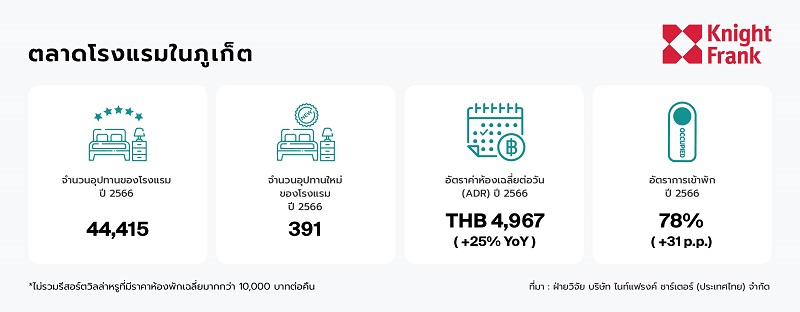

In Phuket, the total number of international tourists in 2023 was 3.86 million, recovering to 72% compared to pre-pandemic levels, and growing dramatically by 139% year-on-year. This strong figure indicates a positive and sustainable strategy for the tourism sector in Phuket, especially the recovery in the latter half of the year, and this trend is expected to continue into 2024, aiming to return to pre-pandemic levels by 2025. Domestic tourist numbers have also recovered at a reasonable rate, with 3.15 million tourists, accounting for 84% of pre-pandemic levels and a year-on-year growth rate of 36%.

Data from the Phuket Immigration Office indicates that Russian tourists are the primary group of international visitors, followed closely by tourists from China, which has been the main group from January to October 2023. It was anticipated that Chinese tourists would reclaim the top position in the latter half of 2023, as they did before the pandemic, but the growth rate did not align with expectations, and they remain in second place, with India and Australia following in third and fourth, respectively, along with Kazakhstan, the UK, and Germany.

The increase in international tourists in 2023 has significantly impacted hotel performance on the island, with an impressive average occupancy rate of 78%, up 31% from the previous year, even surpassing pre-pandemic levels. However, the occupancy rate throughout 2023 has fluctuated, starting from a peak of 90% in December to a low of 68% in September and October.

The tourism and hotel industry in 2024 shows no signs of slowing down, with expectations for more hotels to open in the coming year, anticipating up to 881 new rooms. This indicates a continuous expansion of Phuket's vibrant service landscape, reflecting an attractive and sustainable destination and a commitment to meeting the changing demands of tourists.

The current hotel market situation is quite bright, with room rates per night significantly higher than during the COVID period. However, at the same time, operational costs (Operation Cost), such as employee wages and electricity, have also risen more than profit margins. Therefore, in 2024, a major challenge will be when the number of tourists will recover to pre-COVID levels to ensure that the overall hotel business returns to a satisfactory profit level.