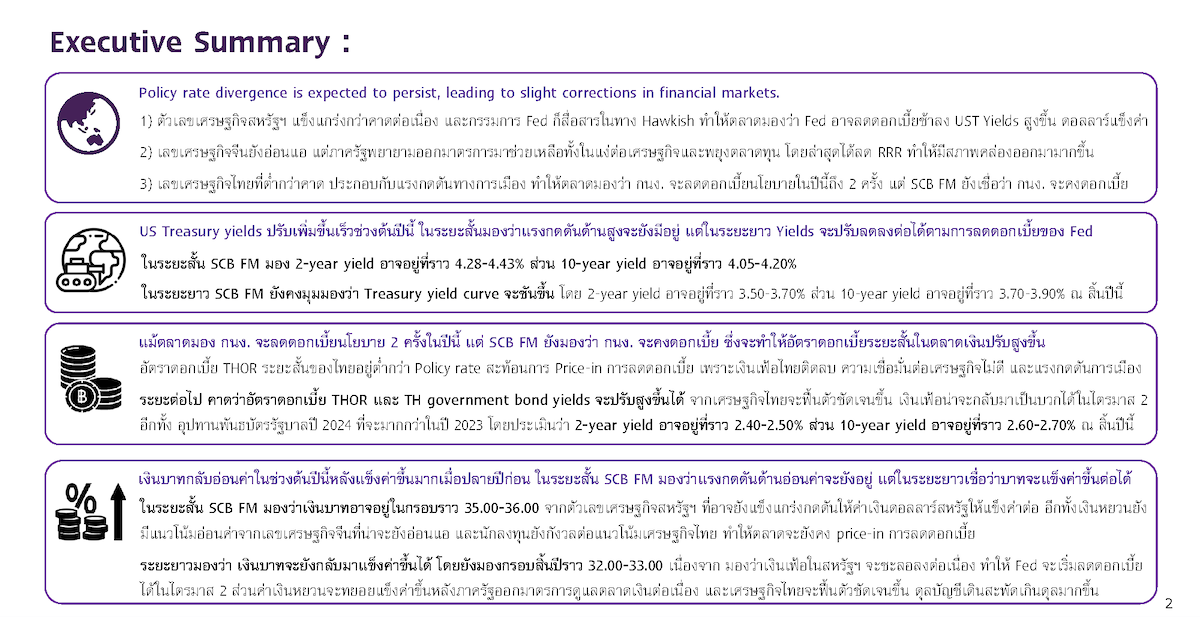

The Fed is likely to maintain interest rates in this week's meeting and signal a gradual reduction, which will continue to exert depreciation pressure on the Thai baht.

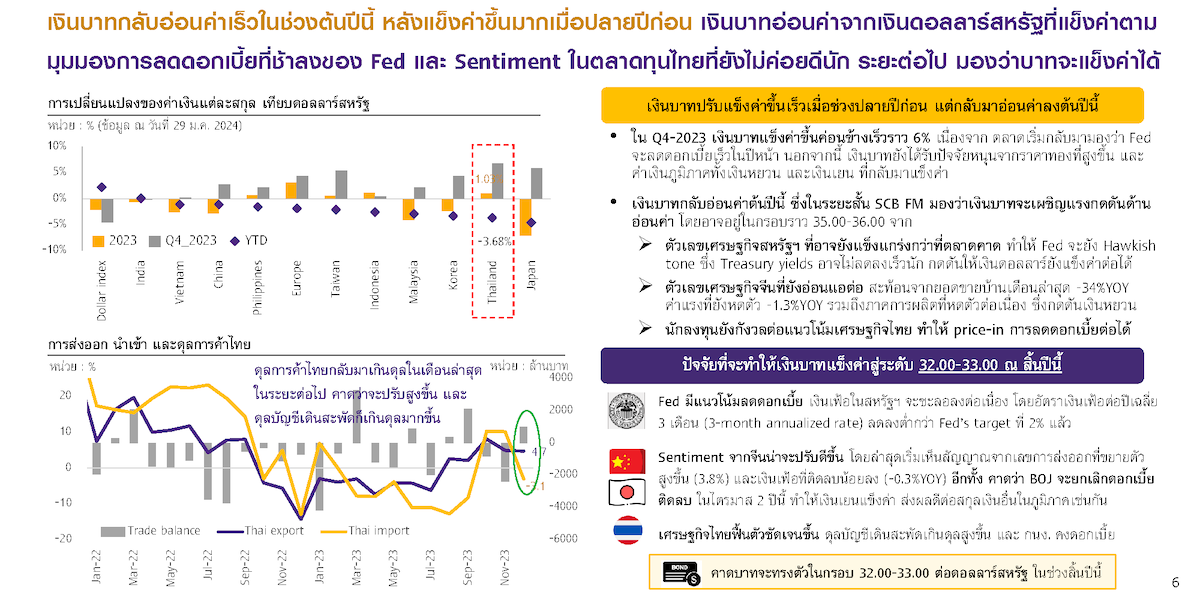

The Financial Markets Group of Siam Commercial Bank (SCB Financial Markets: SCB FM) revealed that the financial market has been quite volatile at the beginning of this year, with rising U.S. government bond yields, fluctuating capital flows, and a depreciating Thai baht. This is partly due to investors believing that the Fed will slow down and reduce interest rates less than previously anticipated after economic figures came out better than expected. SCB FM believes that in the Fed meeting on Wednesday night, the Fed will maintain interest rates as the market expects, and the Fed will first cut rates in the second quarter. Regarding Thai interest rates, it is expected that the Bank of Thailand will keep rates unchanged throughout this year, even though Thai economic figures have come out lower than expected and there are some political pressures. For the Thai baht, it is expected that in the short term, it will continue to face depreciation pressure from potentially strong U.S. economic figures, which will keep the U.S. dollar strong. Additionally, the yuan may weaken due to weak Chinese economic figures, and investors remain concerned about the recovery prospects of the Thai economy. However, it is still expected that the baht will gradually strengthen to the level of 32.00-33.00 by the end of the year.

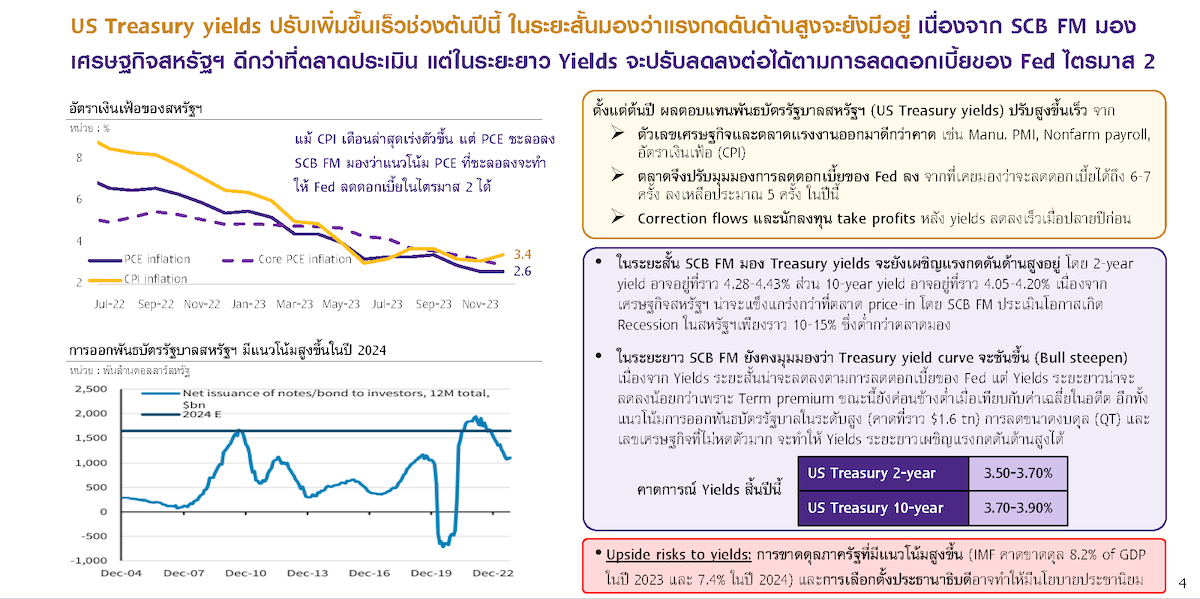

Mr. Patrick Pulia, Assistant Managing Director and Head of Financial Markets at Siam Commercial Bank Public Company Limited, stated that the financial market has been quite volatile at the beginning of this year, with rising U.S. government bond yields, fluctuating capital flows, and the Thai baht depreciating over 3% this month. This is partly due to a shift in investor sentiment regarding the monetary policy outlook of the U.S. Federal Reserve (Fed), as U.S. economic figures have consistently come out stronger than expected, and the Federal Open Market Committee (FOMC) has communicated that it is not yet time to discuss rate cuts (hawkish tone), leading the market to believe that the Fed may slow down its rate cuts. Previously, it was thought that the Fed would cut rates in March, but the latest view is that the chance of a rate cut in March is only about 50%. For the overall year, the market has adjusted its view that the Fed will cut rates less than previously thought, from an expectation of 6-7 cuts this year to only 5-6 cuts. As a result, U.S. Treasury yields have risen, along with a strengthening U.S. dollar.

In the upcoming Fed meeting on Wednesday night, the Fed is expected to maintain interest rates, which aligns with market expectations. The tone of communication from the Fed that the market is watching is likely to remain hawkish, indicating that rate cuts will not happen quickly and will not be substantial, which will keep U.S. Treasury yields high. It is anticipated that the 2-year yield may be around 4.28-4.43%, while the 10-year yield may be around 4.05-4.20% during this period. In the long term, it is expected that the Treasury yield curve will steepen, with short-term yields decreasing according to the Fed fund rate, but long-term yields decreasing less due to a likely increase in term premium. Additionally, there is a trend of more government bonds being issued (estimated at around $1.6 trillion), and the Fed will continue to reduce the size of its balance sheet (quantitative tightening).

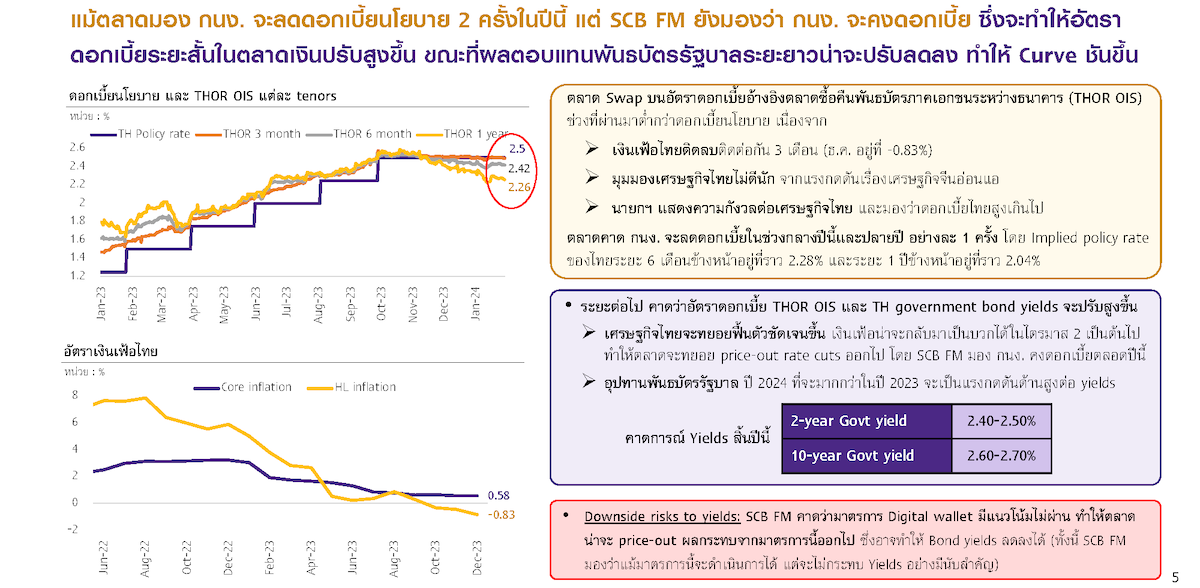

Mr. Patrick stated that the Bank of Thailand will maintain interest rates this year, even though the market expects the Bank to cut policy rates twice, as reflected in the swap market where short-term Thai interest rates are below the policy rate. The market's expectation of rate cuts is due to negative inflation in Thailand, poor confidence in the Thai economy after economic figures came out lower than expected, and political pressures suggesting that Thai interest rates are too high, which burdens household living costs. However, in the future, the THOR OIS interest rates and Thai government bond yields are expected to rise, as the market is likely to price out the possibility of rate cuts due to a clearer recovery in the Thai economy, inflation expected to return to positive in the second quarter, and an increase in government bond supply in 2024 compared to 2023. It is estimated that the 2-year yield may be around 2.40-2.50%, while the 10-year yield may be around 2.60-2.70%.

Mr. Patrick noted that the Thai baht depreciated quickly at the beginning of this year after appreciating significantly at the end of last year. The depreciation of the baht is a result of the strengthening U.S. dollar due to the Fed's slower rate cut outlook and the sentiment in the Thai capital market still being weak. For the short-term outlook, it is expected that the baht will continue to face depreciation pressure, possibly within the range of 35.00-36.00 due to: 1) U.S. economic figures that may still be stronger than the market expects, keeping the dollar strong; 2) weak Chinese economic figures putting pressure on the yuan and regional currencies; and 3) investor concerns about the Thai economic outlook.

However, in the long term, it is still expected that the baht will strengthen again due to: 1) U.S. inflation continuing to slow down, with the average annualized rate over three months dropping below the Fed's target of 2%, allowing the Fed to potentially start cutting rates in the second quarter; 2) the yuan gradually strengthening as the government continues to implement measures to stabilize the financial market, with recent signs of increased Chinese export figures and reduced negative inflation; and 3) a clearer recovery in the Thai economy, with the current account likely to show a surplus compared to last year. For these reasons, it is expected that the baht will strengthen to the level of 32.00-33.00 by the end of this year.