Grade A Office Market in Bangkok Recovers: Ploenchit – Chidlom – Witthayu Leads with 4.9% Rent Increase

Mr. Panya Jenkijwatanalert, Executive Director and Head of Office Space Division Knight Frank stated that the demand for office space in Q1 2023 shows a continuous recovery trend, supported by tenants in the tourism, technology, and consumer goods sectors. Additionally, we have observed a shift in behavior among small tenants moving from home offices to office buildings due to attractive rental prices, more convenient transportation, and a variety of amenities including retail spaces.

The Thai economy in 2023 is expected to grow by 3.8%, up from last year's growth of 2.6%

The Ministry of Finance predicts that Thailand's Gross Domestic Product (GDP) in 2023 will grow by 3.8% annually, primarily driven by an increase in foreign tourist arrivals, expected to reach 27.5 million, nearly a 150% increase from last year. The domestic unemployment rate continues to decline, and average household income is rising. Private consumption is expected to grow by 3.5% annually. Business confidence is returning, and decreasing inflation will lead to a 3.6% annual increase in private investment. However, the global economic conditions of major trading partners have negatively impacted various foreign industries, leading to a forecasted slowdown in export value this year, with growth expected to be less than 1% annually.

The general inflation rate in Q1 decreased to 2.8%, remaining within the target range of 1-3% set by the Bank of Thailand. The main reason for this decline was the weakening energy prices and the high price base from the previous year. Although inflation has decreased, it remains high overall, and strong domestic consumption from the economic recovery may exert further upward pressure on prices. Therefore, the Bank of Thailand maintains its price stability policy and gradually raises the interest rate to 1.75% in line with the improving economic conditions. Additionally, it has introduced further policies, such as expanding loan limits for SMEs, as the recovery across different business sectors is uneven, with small businesses facing higher debt burdens.

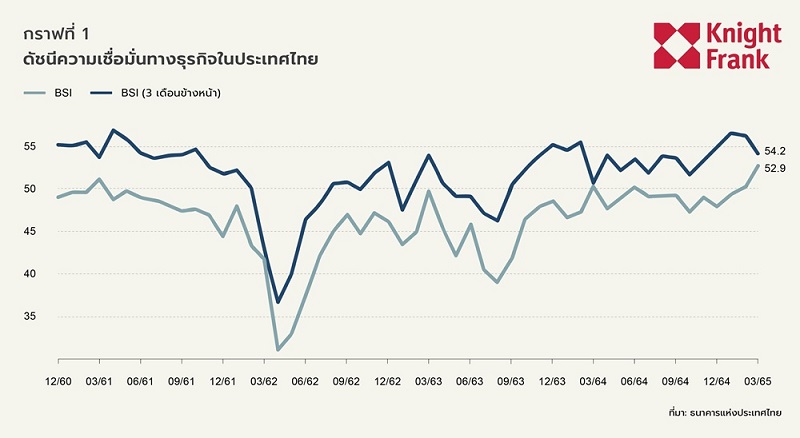

The Business Sentiment Index (BSI) in this quarter increased to 52.9 from 48.4 in the previous quarter, as companies improved their operational efficiency and production costs rose slowly in Q1. However, respondents still expressed concerns about the economic conditions of major trading partners. Decreased global demand may lead to reduced production and new exports, resulting in lower positive expectations over the next three months.

Supply

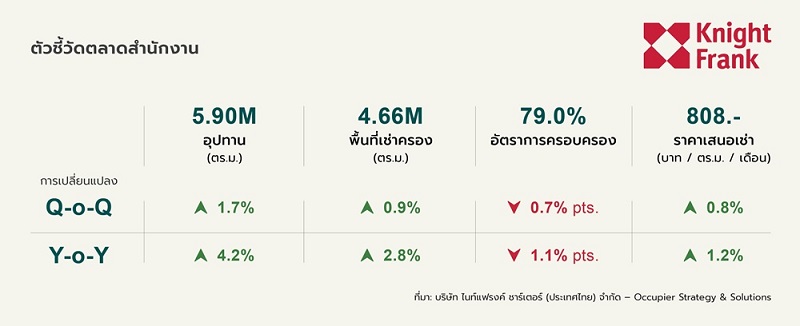

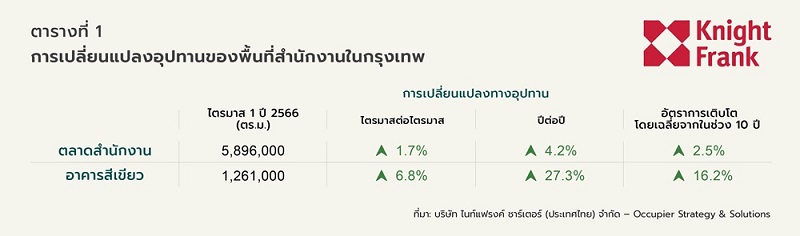

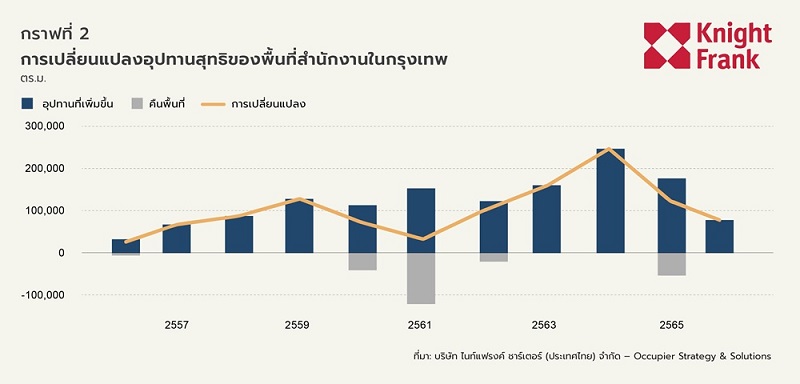

The total supply of office space in Bangkok increased by 86,000 square meters, or 1.7%, from the previous quarter, with two new buildings completed: One City Centre on Ploenchit Road, opposite Central Embassy, and The Rice at the corner of Phaholyothin Bridge. Additionally, there is new supply from the Summer Lasalle project, which is developing new space within the existing project. Since most completed buildings are certified as environmentally friendly (green buildings), the total green office space available for rent is 1,261,000 square meters, an increase of 7.3% from the previous quarter, accounting for 21% of the total market supply.

Future Supply

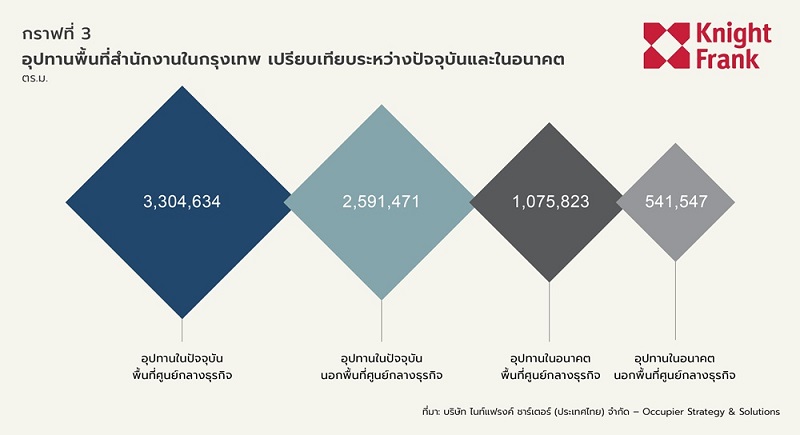

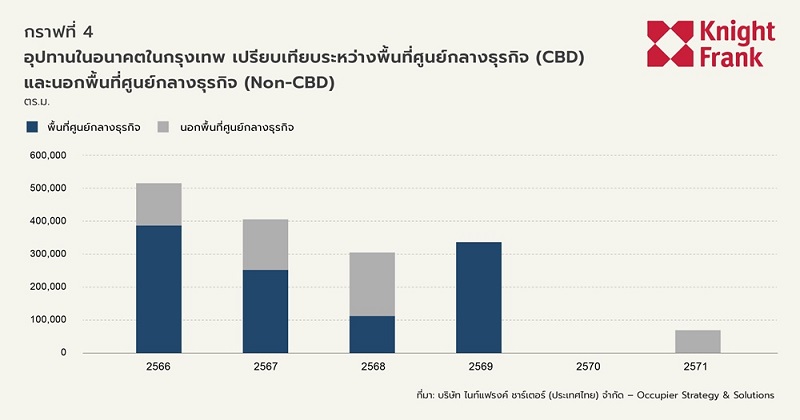

There are two new projects outside the central business district launched this quarter: Cloud 11 by MQDC in the Sukhumvit area and a horizontal office and retail space project by Property Perfect Group on Ratchadapisek Road. The new supply expected at the end of each year from 2023 to 2025 is projected to be 509,000, 402,000, and 302,000 square meters, respectively. The total future rental space is 1.62 million square meters, accounting for 27% of the current supply level, while 67% of the new supply is located in the central business district.

Demand

The net absorption of the market increased to 39,500 square meters in Q1 2023 from 20,900 square meters in Q4 2022. Last year, the net absorption of the market was 150,700 square meters, exceeding the 10-year average of 78,400 square meters. The higher average net absorption indicates that demand is recovering.

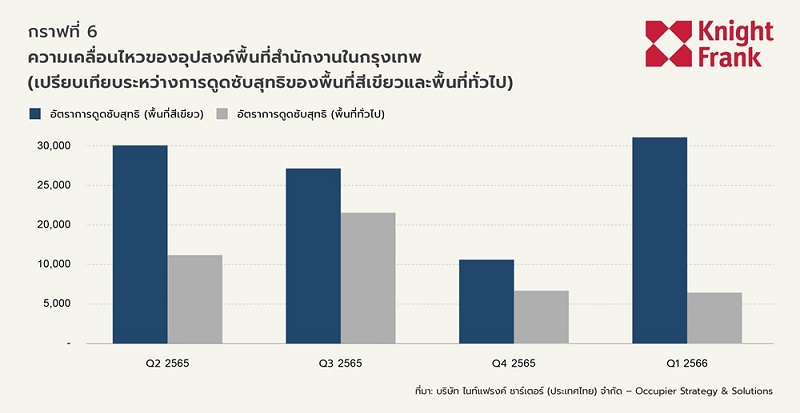

In terms of ESG, green buildings had a net absorption of 31,600 square meters, which is 7,900 square meters higher than non-environmentally friendly buildings. In terms of location, the size of rental space in Q1 was similar both inside and outside the central business district. However, we noted an increase in new demand outside the central business district, resulting in a higher net absorption of 26,000 square meters, while the central business district recorded 13,500 square meters.

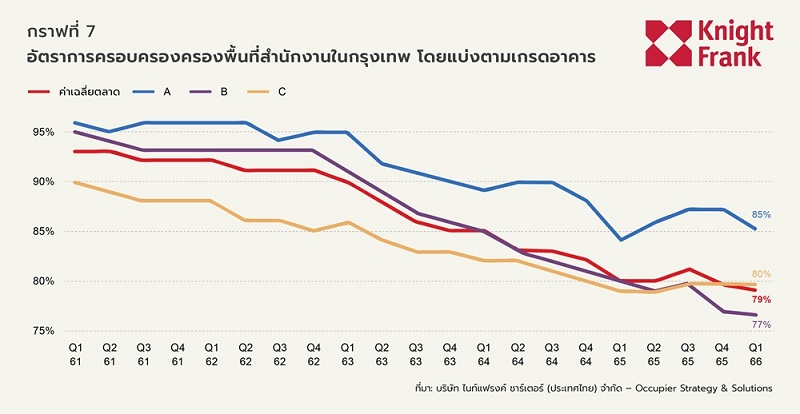

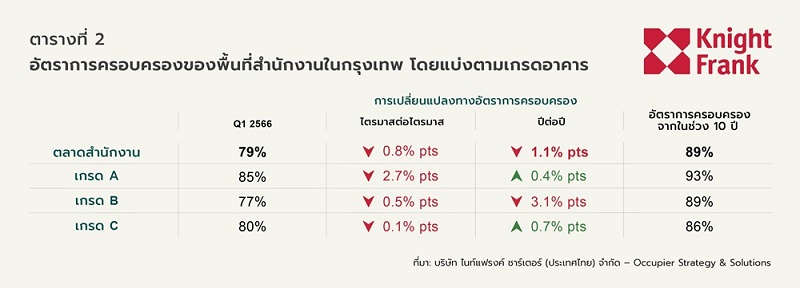

Grade A Occupancy Rate Declines the Most Despite Highest Net Absorption

The total leased area increased by 39,500 square meters, totaling 4.53 million square meters in Q1 2023, with all segments showing positive net absorption. Grade A buildings experienced the highest growth, with quarterly net absorption of 23,900 square meters due to leasing in newly completed buildings. Meanwhile, net absorption for Grade B buildings slowed this quarter, yet it remains the most popular segment over the past year, with annual net absorption of 78,200 square meters.

The market occupancy rate decreased by 0.8% from the previous quarter to 79%, with a declining trend across all segments. The occupancy rate for Grade A buildings dropped by 2.7% from the previous quarter to 85% due to pressure from new supply outpacing demand. The occupancy rate for Grade B buildings slightly decreased compared to the previous quarter but has dropped more than 3% annually, despite having the highest demand compared to other segments. Meanwhile, the occupancy rate for Grade C buildings remained stable at around 80%, with only slight changes compared to the previous quarter and last year.

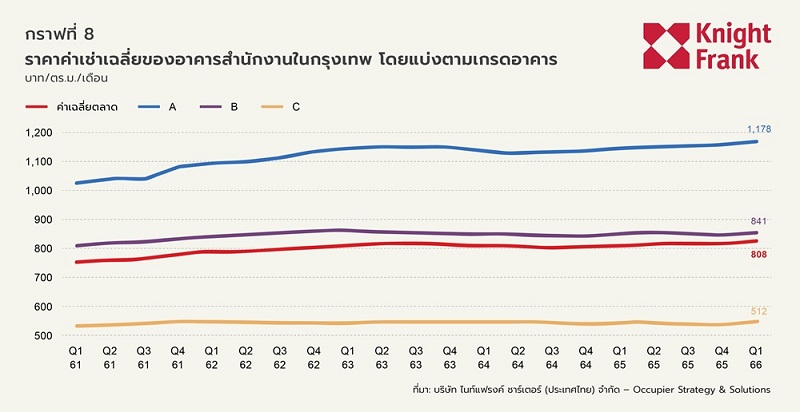

The average rent increased to 808 baht per square meter per month in Q1, with rental growth observed across all grades of buildings. Despite the overall increase in supply, many building owners raised rents after maintaining rental rates for several years.

Grade A buildings saw the highest rent increase, rising by 1% from the previous quarter to 1,178 baht, due to relatively high occupancy rates and new supply contributing to rental growth. In contrast, Grade B and Grade C buildings experienced only slight rent growth, increasing by 0.9% from the previous quarter to 841 baht and by 0.6% from the previous quarter to 512 baht, respectively.

Occupancy Rates in Most Areas Decline While Average Rental Prices Trend Upward

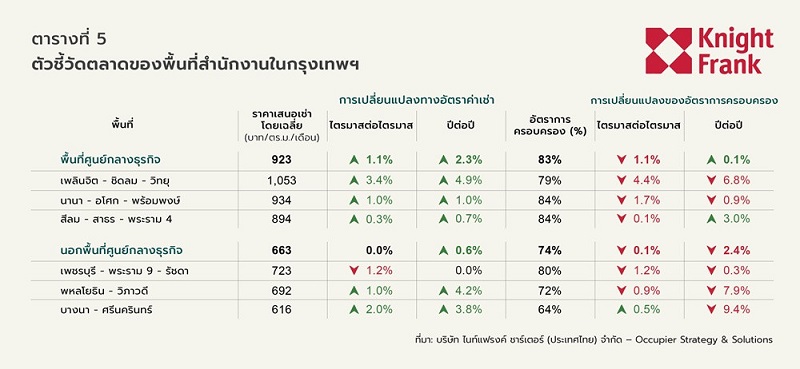

The average rental price in the central business district rose to 922 baht per square meter per month, with the average occupancy rate decreasing to 83%. Most areas experienced rental price growth, led by Ploenchit – Chidlom - Witthayu, where rental prices increased by 4.9% from last year, while occupancy rates dropped nearly 7% from last year. The best-performing area was Silom – Sathorn – Rama 9, with rental prices growing by 0.6% from last year and occupancy rates increasing by 3% from last year, aligning with net absorption figures exceeding 60,000 square meters over the past year.

The average rental price in areas outside the central business district remained stable at 662 baht per square meter per month, while the occupancy rate decreased by 2.6% from the previous quarter to 74%. Most major areas saw rental price increases, except for the Phetchaburi – Rama 9 – Ratchada area, where the occupancy rate dropped by 1.2% from the previous quarter.

Due to some buildings adjusting their pricing strategies, the Phaholyothin – Vibhavadi area had the highest net absorption this quarter, but the occupancy rate decreased by 0.9% from the previous quarter. Meanwhile, the average rental price in the Bangna – Srinakarin area increased due to limited remaining buildings and rising rents, with a growth rate of 2% from the previous quarter. The occupancy rate slightly increased by 0.5% from the previous quarter due to new supply entering the market since the previous quarter.

Market Trends

The demand for office buildings in Bangkok in Q1 2023 shows a recovery trend, similar to the national economy. Positive net absorption has been recorded for four consecutive quarters, resulting in an annual absorption rate of 145,000 square meters. However, the increase in new supply of 86,000 square meters.

The market occupancy rate in Q1 2023 decreased to 79%, while the average rental price for office space increased again in 2023, rising by 0.9% from the previous quarter or 1.2% from last year to 808 baht per square meter per month. The increase in rent is attributed to new buildings setting higher rental prices and existing buildings raising rents after returning to normalcy post-COVID.

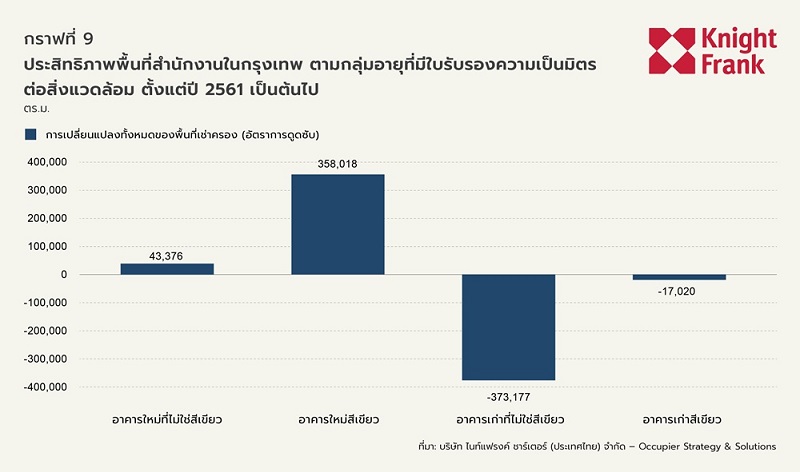

It is well-known that many new office spaces will enter the market, which may impact existing buildings, especially older ones. Knight Frank conducted a study to assess the performance of all office buildings constructed before and after 2000 over the past five years, finding that older buildings lost 390,000 square meters of occupancy, while new buildings gained 401,000 square meters of occupancy.

Furthermore, regarding sustainability issues, we observed that older buildings with environmental certifications, such as LEED and WELL, lost only 17,000 square meters of occupancy compared to a loss of 373,000 square meters in older buildings without certifications. The results align with newly completed buildings after 2000, where certified new buildings gained 358,000 square meters of occupancy, while new buildings without certifications gained only 43,000 square meters.

This study underscores the differences in performance between older and newer buildings and the importance of upgrading facilities to meet ESG standards. Buildings that proactively adapt to these standards will be more successful in retaining tenants than those that do not. Moreover, it is evident that older buildings that have upgraded their facilities to meet standards can compete in the market.